Global Sashimi Market Size

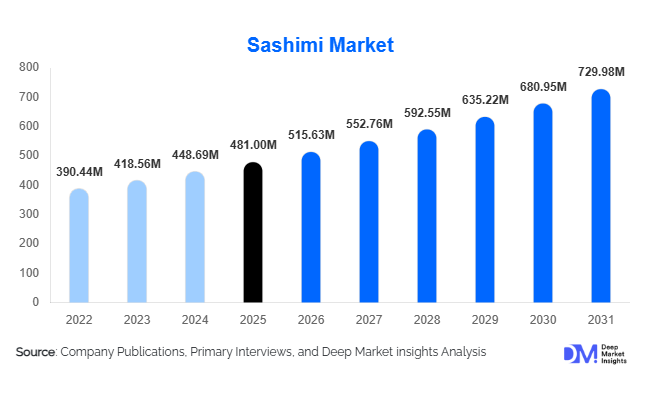

According to Deep Market Insights, the global sashimi market size was valued at USD 481 million in 2025 and is projected to grow from USD 515.63 million in 2026 to reach USD 729.98 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The growth of the global sashimi market is primarily driven by rising consumer preference for premium seafood products, increasing adoption of Japanese cuisine worldwide, growing demand for high-protein and omega-3-rich diets, and significant improvements in cold-chain logistics that enable wider distribution of sashimi-grade seafood. The market is also benefiting from the expansion of premium dining establishments, rapid growth of sushi restaurant chains, and increasing availability of ready-to-eat sashimi products through retail and e-commerce channels. Sustainability initiatives in aquaculture, digital seafood traceability systems, and advancements in ultra-low-temperature freezing technologies are further strengthening market growth globally.

Key Market Insights

- Red fish sashimi, led by salmon and tuna, accounts for the largest share of global consumption, representing approximately 44% of total market revenue.

- Foodservice channels dominate the market, contributing nearly 68% of global demand due to the popularity of sushi restaurants and Japanese fine dining establishments.

- Asia-Pacific remains the largest regional market, accounting for approximately 42% of global sashimi consumption, driven by Japan, South Korea, China, and Southeast Asia.

- Middle East & Africa is the fastest-growing regional market, supported by luxury hospitality expansion, premium tourism, and increasing seafood imports.

- Farmed seafood is increasingly replacing wild-caught supply, improving consistency, sustainability, and year-round product availability.

- Traceability technologies, blockchain integration, and sustainability certifications are becoming major competitive differentiators across premium seafood supply chains.

Global Sashimi Market Latest Trends

Growing Adoption of Sustainable and Traceable Seafood

Sustainability has become one of the most influential trends shaping the global sashimi market. Consumers, retailers, and foodservice operators are increasingly prioritizing seafood products sourced through responsible fishing and certified aquaculture practices. Certifications such as MSC and ASC are gaining wider acceptance among premium restaurants and retailers seeking to strengthen sustainability credentials. In parallel, seafood companies are implementing blockchain-enabled traceability systems that allow customers to verify the origin, harvesting method, transportation route, and quality assurance standards of sashimi-grade seafood. This trend is particularly strong in Europe, North America, and developed Asian markets where environmental awareness influences purchasing decisions. Suppliers capable of offering transparent and traceable seafood products are increasingly commanding premium pricing and long-term supply contracts.

Expansion of Retail and Ready-to-Eat Sashimi Products

The sashimi market is witnessing a gradual shift from exclusive restaurant consumption toward retail and direct-to-consumer channels. Supermarkets, premium grocery chains, convenience stores, and online seafood platforms are expanding their ready-to-eat sashimi offerings. Consumers increasingly seek restaurant-quality seafood experiences at home, encouraging growth in packaged sashimi trays, vacuum-sealed portions, and meal kits. Enhanced cold-chain infrastructure and ultra-low-temperature freezing technologies have enabled retailers to offer sashimi-grade products while maintaining freshness and food safety standards. This trend is particularly evident in North America and Europe, where retail penetration is creating new growth opportunities beyond traditional foodservice channels.

Global Sashimi Market Drivers

Increasing Demand for High-Protein and Functional Foods

Consumer preference for nutrient-dense foods is significantly boosting demand for sashimi products worldwide. Rich in omega-3 fatty acids, lean protein, vitamins, and essential minerals, sashimi aligns with health-focused dietary trends including ketogenic, low-carbohydrate, paleo, and high-protein eating patterns. Rising awareness regarding cardiovascular health and weight management has further strengthened demand among affluent urban consumers. As health-conscious eating continues to gain momentum globally, sashimi is increasingly positioned as a premium functional food option.

Global Expansion of Japanese Cuisine

Japanese cuisine has evolved from a niche culinary category into a mainstream global dining trend. Sushi chains, Japanese restaurants, and Asian fusion establishments continue to expand across North America, Europe, the Middle East, and emerging Asian economies. Growing familiarity with Japanese food culture has significantly increased consumer acceptance of raw seafood products, directly supporting sashimi consumption. International tourism, cultural exchange, and social media exposure have further accelerated the globalization of Japanese cuisine and premium seafood dining experiences.

Advancements in Cold-Chain and Freezing Technologies

Modern cold-chain infrastructure and super-freezing technologies have transformed the global sashimi supply chain. Ultra-low-temperature storage allows seafood to retain freshness, texture, nutritional value, and food safety standards over extended transportation distances. These advancements have enabled sashimi-grade seafood to reach inland cities and emerging consumer markets that were previously inaccessible. Continuous investment in refrigeration logistics, processing facilities, and quality assurance systems is expected to remain a major growth catalyst for the industry.

Global Sashimi Market Restraints

Raw Material Supply Volatility

The sashimi market remains highly dependent on premium seafood species such as tuna, salmon, yellowtail, and sea bream. Seasonal fluctuations, fishing quotas, climate variability, and regulatory restrictions can significantly affect supply availability and pricing. These factors contribute to procurement uncertainty and create challenges for processors, distributors, and foodservice operators seeking stable supply chains. Rising feed costs within aquaculture industries further influence production economics and product pricing.

Stringent Food Safety Requirements

As sashimi is consumed raw, maintaining strict food safety standards throughout harvesting, processing, transportation, storage, and preparation remains critical. Any breakdown in cold-chain integrity can result in product quality deterioration and reputational damage. Regulatory compliance costs continue to rise as governments strengthen food safety requirements for seafood imports and domestic distribution. Consumer concerns regarding contamination, parasites, and freshness remain barriers to broader market penetration in certain regions.

Global Sashimi Market Industry Key Opportunities

Sustainable Aquaculture Expansion

The growing emphasis on sustainable seafood production presents substantial opportunities for market participants. Investment in advanced aquaculture systems enables consistent year-round supply while reducing dependence on wild-caught fisheries. Sustainable salmon, yellowtail, and sea bream farming operations are expanding globally to meet increasing demand from retailers and foodservice operators. Producers with strong environmental credentials are expected to capture premium market positioning and strengthen relationships with global restaurant chains and supermarket groups.

Emerging Premium Seafood Markets

Rapid income growth across China, India, Vietnam, Thailand, Indonesia, Saudi Arabia, and the UAE is creating new opportunities for sashimi suppliers. Rising middle-class populations and increasing exposure to international dining experiences are driving demand for premium seafood products. Luxury hospitality developments, upscale retail formats, and expanding Japanese restaurant networks in these markets are expected to generate significant incremental demand over the next decade.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 481.00 Million |

| Market Size in 2026 | USD 515.63 Million |

| Market Size in 2031 | USD 729.98 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Red fish sashimi continues to dominate the global market, contributing approximately 44% of total revenue, supported by strong consumer affinity for high-fat, premium-textured seafood such as tuna and salmon. The leading driver of growth in this segment is the global premiumization of seafood consumption, reinforced by the rapid expansion of Japanese dining culture and sushi-focused restaurant chains across both developed and emerging economies. Tuna and salmon remain the most widely consumed varieties due to their consistent supply chains, strong brand familiarity among consumers, and adaptability across both foodservice and retail applications. White fish sashimi, including yellowtail, sea bream, flounder, and snapper, represents the second-largest product category and is increasingly driven by rising demand for authentic Japanese culinary experiences, particularly among consumers seeking lighter taste profiles and diversified seafood options beyond traditional red fish offerings. Shellfish and cephalopod sashimi, including scallops, shrimp, octopus, and squid, are expanding steadily, with growth primarily driven by chef-led culinary innovation, fine dining experimentation, and increasing incorporation into fusion cuisine menus across premium restaurants. Specialty categories such as sea urchin, luxury roe, and seasonal high-value seafood products continue to command strong margins, with demand driven by exclusivity, gastronomic prestige, and their positioning within high-end dining and gifting culture. Plant-based sashimi alternatives, while still niche, are emerging in response to sustainability concerns and the growing vegan and flexitarian consumer base, with innovation in texture replication and seafood analog development acting as a key long-term growth catalyst.

Form Insights

Fresh and chilled sashimi products account for approximately 63% of global demand, primarily driven by consumer expectations of superior texture, sensory quality, and authenticity associated with traditional sushi and sashimi consumption. The leading growth driver in this segment is the sustained expansion of restaurant culture and sushi-specific dining formats, where freshness remains a critical quality benchmark. However, frozen and super-frozen sashimi formats are experiencing accelerated growth, supported by advancements in cryogenic freezing technologies and improved cold-chain logistics that preserve texture, flavor, and food safety standards over long distribution cycles. The expansion of frozen sashimi is further driven by increasing globalization of seafood trade, enabling producers to serve distant markets efficiently while maintaining product integrity. Retail penetration in emerging markets is also reinforcing demand for frozen formats, as consumers seek accessible, longer-shelf-life premium seafood options outside traditional restaurant environments.

Distribution Channel Insights

Foodservice remains the dominant distribution channel, accounting for approximately 68% of global sashimi market revenue, with growth primarily driven by the rapid proliferation of Japanese restaurants, sushi chains, fine dining establishments, and luxury hospitality venues worldwide. The key driver of this dominance is the consumer preference for professionally prepared sashimi, where safety, presentation, and authenticity are critical value propositions that require skilled culinary expertise. Retail distribution is expanding at a strong pace, supported by rising at-home dining trends, increased availability of premium packaged seafood, and growing consumer confidence in refrigerated and ready-to-eat formats. The primary growth driver in retail is lifestyle-driven demand for convenience without compromising quality, particularly in urban markets. Online distribution channels are also gaining momentum, driven by advancements in cold-chain-enabled logistics infrastructure and the increasing penetration of e-commerce grocery platforms. This shift is further accelerated by digitally native consumers who prioritize convenience, product transparency, and direct-to-consumer sourcing models for premium seafood products.

End User Insights

Restaurants represent the largest end-user segment, contributing approximately 58% of global sashimi demand, with growth driven by expanding global appetite for authentic Japanese dining experiences and increasing consumer willingness to pay for premium culinary experiences. The core driver of this segment is the experiential nature of sashimi consumption, where freshness, presentation, and chef expertise significantly influence demand. Hotels and luxury hospitality establishments form a rapidly growing end-user category, fueled by expansion in international tourism, rising luxury travel expenditure, and the integration of premium Japanese cuisine into high-end hospitality offerings. Retail consumers are increasingly contributing to market growth through rising household consumption of packaged sashimi products, driven by convenience-oriented lifestyles and increasing familiarity with Japanese cuisine. Corporate catering, premium events, and banquet services are also emerging as significant growth areas, supported by increasing corporate spending on executive hospitality, experiential dining, and premium seafood-based menu offerings in developed economies.

Sourcing Method Insights

Aquaculture-sourced seafood accounts for approximately 57% of global sashimi production and continues to expand its share, primarily driven by sustainability imperatives, improved production scalability, and the need for consistent year-round supply. The leading driver in this segment is the global shift toward environmentally responsible seafood production, supported by advancements in farming technologies and certification frameworks that ensure traceability and quality assurance. Farmed salmon, yellowtail, and sea bream have become essential to meeting rising global demand while reducing pressure on wild fisheries. Wild-caught seafood continues to hold strong relevance in premium market segments, particularly for species such as bluefin tuna and other high-value fish that are associated with scarcity and exclusivity. The primary driver in wild-caught sourcing is luxury positioning and flavor differentiation, although regulatory constraints and sustainability concerns are gradually encouraging increased reliance on responsibly farmed alternatives.

Explore more data points, trends and opportunities Download Free Sample Report

Sashimi Market Segmentations

By Product Type

- Red Fish Sashimi

- White Fish Sashimi

- Shellfish & Cephalopod Sashimi

- Premium & Specialty Sashimi

- Plant-Based Sashimi

By Form

- Fresh/Chilled Sashimi

- Frozen Sashimi

- Super Frozen Sashimi

By Packaging Format

- Bulk Foodservice Packs

- Retail Trays

- Vacuum Packs

- Modified Atmosphere Packaging (MAP)

- Ready-to-Eat Sashimi Kits

By Distribution Channel

- Foodservice

- Retail Stores

- Online Channels

By End User

- Restaurants

- Hotels

- Retail Consumers

- Corporate Catering

- Travel & Hospitality

- Premium Events & Banquets

Regional Insights

Asia-Pacific

Asia-Pacific leads the global sashimi market with approximately 42% of total revenue, driven primarily by deep-rooted cultural integration of raw seafood consumption and exceptionally high per-capita seafood intake. Japan remains the largest individual market, accounting for nearly 22% of global demand, with its leadership driven by longstanding culinary traditions, established seafood supply chains, and strong domestic consumption patterns. The key growth driver across the broader Asia-Pacific region is rapid urbanization combined with rising disposable incomes, which is fueling expansion in premium dining and restaurant penetration. China is emerging as a major growth engine, supported by increasing consumer exposure to Japanese cuisine, expanding middle-class expenditure on premium seafood, and rapid growth in Japanese restaurant chains across major urban centers. Additional markets such as South Korea, Taiwan, Singapore, and Thailand are also contributing to regional expansion through tourism-driven demand and evolving dining preferences.

North America

North America accounts for approximately 28% of global sashimi revenue, with the United States representing the majority share at nearly 19%. Growth in this region is primarily driven by increasing health consciousness among consumers, strong acceptance of sushi culture, and the integration of Japanese cuisine into mainstream dining habits. A key driver is the diversification of dietary preferences, influenced by multicultural populations and rising demand for high-protein, low-fat seafood options. Canada is also witnessing steady growth supported by premium foodservice expansion and increased availability of high-quality seafood in retail environments. The region continues to benefit from strong restaurant penetration and evolving consumer perception of sashimi as a healthy and premium dining choice.

Europe

Europe represents approximately 20% of global sashimi consumption, with major contributions from the United Kingdom, Germany, France, Italy, Spain, and the Netherlands. Growth is primarily driven by increasing consumer interest in Japanese cuisine and the rising popularity of experiential dining across urban centers. A major regional driver is the strengthening emphasis on sustainability and seafood traceability, which is shaping both consumer preferences and regulatory frameworks. This has led to increased demand for certified sustainable seafood products across both foodservice and retail channels. The expansion of premium grocery retail formats and greater availability of imported high-quality seafood are further supporting market penetration across the region.

Latin America

Latin America accounts for approximately 4% of global sashimi market revenue, with Brazil, Mexico, Chile, and Peru serving as the primary markets. The leading growth driver in the region is rising disposable income levels combined with the gradual expansion of premium dining culture in major urban centers. Consumer awareness of Japanese cuisine is increasing through international tourism and restaurant proliferation. Chile plays a particularly important role due to its position as a major global salmon producer, which strengthens regional integration into the global sashimi supply chain and supports export-driven growth. Expanding middle-class consumption patterns are expected to further accelerate market development in the region.

Middle East & Africa

The Middle East and Africa region accounts for approximately 6% of global demand but is the fastest-growing regional market, driven primarily by luxury tourism expansion, high-income consumer segments, and rapid development of premium hospitality infrastructure. The United Arab Emirates, Saudi Arabia, and Qatar are leading markets, where growth is supported by increasing penetration of high-end Japanese restaurants and global fine dining concepts. A key driver in this region is the expansion of luxury hospitality and experiential tourism offerings, particularly within major metropolitan and resort destinations. Rising expatriate populations and international culinary influence are also contributing to increased acceptance and consumption of sashimi across the region.

Key Players in the Global Sashimi Market

- Mowi

- SalMar

- Leroy Seafood Group

- Cermaq

- Thai Union Group

- Nippon Suisan (Nissui)

- Maruha Nichiro

- Mitsubishi Corporation Seafood

- Austevoll Seafood

- Grieg Seafood

- Bakkafrost

- Dongwon Industries

- Cooke Aquaculture

- Kyokuyo

- Clearwater Seafoods