Catering and Food Service Contractor Market Size

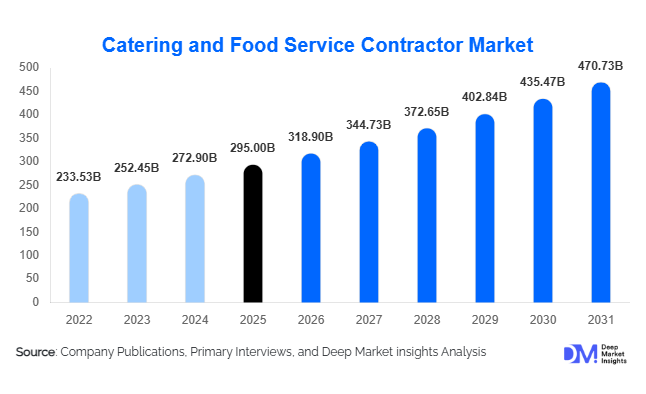

According to Deep Market Insights, the global catering and food service contractor market size was valued at USD 295.0 billion in 2025 and is projected to grow from USD 318.90 billion in 2026 to reach USD 470.73 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by the increasing outsourcing of non-core services across corporate, healthcare, and institutional sectors, along with rising demand for efficient, scalable, and compliant food service operations. Organizations are increasingly relying on professional catering contractors to enhance cost control, ensure food safety, and deliver consistent quality across locations.

Key Market Insights

- Outsourced catering services dominate the market, with organizations focusing on operational efficiency and cost optimization.

- Corporate and healthcare sectors are the largest demand generators, accounting for a significant share of long-term contracts globally.

- North America leads the global market, supported by mature outsourcing practices and large institutional infrastructure.

- Asia-Pacific is the fastest-growing region, driven by industrialization, urbanization, and expanding workforce populations.

- Technology integration, including AI-based menu planning and supply chain optimization, is transforming service delivery.

- Sustainability and health-focused catering are emerging as key differentiators in competitive bidding processes.

What are the latest trends in the catering and food service contractor market?

Digitalization and Smart Kitchen Adoption

Catering contractors are increasingly adopting digital technologies such as AI-driven demand forecasting, automated procurement systems, and IoT-enabled kitchen equipment. These innovations are improving operational efficiency, reducing food waste, and enabling real-time monitoring of food quality and inventory. Mobile-based ordering systems and contactless dining solutions are also gaining traction, particularly in corporate campuses and educational institutions. This digital shift is enhancing customer experience while helping contractors manage costs and improve margins in a competitive environment.

Shift Toward Sustainable and Health-Centric Catering

Sustainability and nutrition-focused offerings are becoming central to catering contracts. Contractors are incorporating locally sourced ingredients, reducing food waste, and adopting eco-friendly packaging solutions. At the same time, there is rising demand for customized meal plans, including vegan, organic, and medically tailored diets. Corporate wellness programs and healthcare institutions are driving this trend, encouraging catering providers to innovate with healthier menus and transparent nutritional information. Sustainability credentials are increasingly influencing contract awards, especially among multinational clients.

What are the key drivers in the catering and food service contractor market?

Rising Outsourcing of Food Services

Organizations across industries are increasingly outsourcing catering services to specialized contractors to focus on core business functions. This trend is particularly strong in corporate offices, hospitals, and educational institutions, where operational efficiency and compliance are critical. Outsourcing enables cost savings, standardized service quality, and scalability, making it a key growth driver for the market.

Expansion of Institutional Infrastructure

Global investments in healthcare, education, and industrial infrastructure are significantly boosting demand for catering services. Hospitals, universities, and large manufacturing facilities require reliable food service operations, creating long-term contract opportunities for catering providers. The expansion of these sectors, particularly in emerging economies, is fueling steady market growth.

Growth in Workforce and Corporate Ecosystems

The rise of large office complexes, IT parks, and industrial hubs is driving demand for workplace catering solutions. Employers are increasingly offering food services as part of employee welfare initiatives, enhancing productivity and satisfaction. This trend is particularly prominent in rapidly urbanizing regions, where workforce density is increasing.

What are the restraints for the global market?

Volatility in Raw Material and Operational Costs

Fluctuations in food ingredient prices, labor costs, and logistics expenses pose significant challenges for catering contractors. Fixed-price contracts can compress margins during periods of cost inflation, making it essential for companies to adopt flexible pricing models and efficient supply chain strategies.

Stringent Regulatory and Food Safety Requirements

Catering providers must comply with diverse food safety standards, labor regulations, and hygiene protocols across different regions. Ensuring compliance increases operational complexity and costs, particularly for multinational contractors operating in multiple jurisdictions. Non-compliance risks can lead to contract termination and reputational damage.

What are the key opportunities in the catering and food service contractor industry?

Expansion in Emerging Markets

Rapid industrialization and urbanization in Asia-Pacific, the Middle East, and Africa are creating significant opportunities for catering contractors. Governments are investing heavily in healthcare, education, and infrastructure, leading to increased demand for institutional catering services. Companies entering these markets can secure long-term contracts and benefit from high growth potential.

Technology-Driven Service Innovation

The integration of advanced technologies such as AI, automation, and data analytics presents opportunities to enhance efficiency and customer experience. Smart kitchens, predictive analytics, and digital engagement platforms enable contractors to optimize operations, reduce waste, and offer personalized services. Technology adoption also helps differentiate providers in competitive bidding processes.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 295 Billion |

| Market Size in 2026 | USD 318.90 Billion |

| Market Size in 2031 | USD 470.73 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

Contract catering continues to dominate the global catering services market, accounting for approximately 42% of the total market share in 2025. This dominance is primarily driven by the increasing preference of large organizations for outsourced food service management, allowing them to focus on core operations while ensuring consistent quality, hygiene compliance, and cost efficiency. The long-term contractual nature of this segment creates predictable revenue streams for service providers, encouraging investments in technology-enabled kitchen operations, centralized procurement systems, and standardized menu planning. The growth of corporate campuses, IT parks, manufacturing clusters, and institutional facilities has further reinforced demand for structured catering contracts, particularly in urbanized economies.A key driver of growth in the contract catering segment is the rising emphasis on operational efficiency and regulatory compliance. Organizations are increasingly seeking vendors capable of meeting stringent food safety standards, nutritional requirements, and sustainability benchmarks. Additionally, digital transformation in catering operations, including AI-based demand forecasting and automated inventory management, is improving service consistency and reducing wastage, thereby strengthening the adoption of contract-based models. Event catering and concession services are also expanding rapidly, supported by the resurgence of large-scale social gatherings, sports tournaments, concerts, exhibitions, and tourism-related activities. The rebound in global travel and hospitality sectors has further amplified demand for flexible, high-volume catering solutions capable of handling fluctuating customer inflows.

End-Use Industry Insights

The corporate sector remains the leading end-use industry, accounting for approximately 28% of the global market share. This dominance is driven by the rapid expansion of office spaces, multinational headquarters, and IT-enabled service hubs that prioritize employee welfare through structured meal programs. Corporate catering is increasingly viewed as a strategic tool for employee satisfaction, productivity enhancement, and workplace engagement, leading to long-term outsourcing contracts with professional catering firms. The integration of wellness-focused menus, calorie-controlled meals, and diverse cuisine options is further strengthening demand in this segment.Healthcare is emerging as the fastest-growing end-use segment, supported by the expansion of hospitals, specialty care centers, and elderly care facilities. The growing importance of therapeutic nutrition, dietary customization, and hygiene-compliant meal preparation is significantly increasing reliance on professional catering services within healthcare institutions. This segment is further strengthened by aging populations in developed economies and rising healthcare investments in emerging markets. Educational institutions also represent a substantial demand base, driven by government-funded mid-day meal programs, private school expansions, and university campus developments. Industrial and manufacturing sectors contribute steadily to demand due to large workforce concentrations requiring cost-effective, high-volume meal provisioning. Across all end-use industries, the leading growth driver remains the increasing outsourcing of non-core functions to specialized catering providers capable of delivering standardized, scalable, and compliant food services.

Service Delivery Insights

Full-service catering dominates the service delivery landscape, accounting for approximately 55% of the total market share. This model is preferred due to its comprehensive offering, which includes food preparation, menu design, procurement, logistics, on-site service management, and post-service cleanup. Clients increasingly favor end-to-end solutions that minimize operational complexity while ensuring consistency in quality and service delivery. Full-service providers are investing heavily in centralized kitchens, advanced supply chain systems, and workforce training programs to enhance efficiency and service reliability.The primary growth driver for full-service catering is the increasing demand for turnkey solutions in large-scale facilities such as corporate campuses, hospitals, and educational institutions. Organizations are shifting toward integrated service models that combine cost optimization with enhanced employee or customer experience. Managed services are also gaining traction as they offer flexible staffing, procurement optimization, and performance-based contracts. These models allow clients to adjust service levels based on demand fluctuations while maintaining budget control. The growing adoption of hybrid service delivery models that combine in-house and outsourced operations is further shaping the competitive landscape of this segment.

Pricing Model Insights

Cost-plus contracts represent nearly 38% of the global catering services market, making them one of the most widely adopted pricing models. This approach allows service providers to recover operational costs while earning a fixed margin, making it particularly suitable in environments with volatile food prices and fluctuating demand. Clients benefit from transparency in cost structures, while providers gain protection against input cost inflation, especially in raw materials and logistics.The key driver for the growth of cost-plus models is the increasing unpredictability in global food supply chains, influenced by climate conditions, geopolitical tensions, and transportation disruptions. Fixed-price contracts remain widely used in stable institutional environments where demand patterns are predictable, such as corporate cafeterias and educational institutions. However, revenue-sharing models are gaining traction in concession-based services, particularly in airports, stadiums, and entertainment venues, where revenue potential is directly linked to footfall and consumer spending behavior. The evolution of hybrid pricing strategies that combine fixed and variable components is also becoming increasingly common, enabling better risk distribution between clients and service providers.

Cuisine Type Insights

Multi-cuisine offerings dominate the global catering market, accounting for approximately 47% market share. This dominance is driven by globalization, workforce diversity, and increasing consumer exposure to international food cultures. Organizations are increasingly offering varied menus that include Asian, European, Middle Eastern, and local cuisines to accommodate diverse employee preferences. The emphasis on inclusivity and employee satisfaction has made multi-cuisine catering a standard offering in corporate and institutional environments.The leading driver of growth in this segment is the rising demand for customization and dietary flexibility. Catering providers are increasingly incorporating vegetarian, vegan, gluten-free, and health-specific meal options to align with evolving consumer health awareness. Specialized diet catering is emerging rapidly, particularly in healthcare and wellness-focused corporate environments, where nutritional precision and dietary compliance are critical. The integration of nutrition analytics and personalized meal planning tools is further enhancing service differentiation. Additionally, cultural diversity in urban workplaces is accelerating the demand for globally inspired menus, reinforcing the importance of culinary variety in sustaining customer satisfaction.

Organization Size Insights

Large enterprises account for more than 60% of the catering services market, primarily due to their extensive operational scale and multi-location requirements. These organizations typically engage in long-term outsourcing agreements to ensure standardized food service delivery across multiple facilities. The need for consistency, compliance, and scalability makes large enterprises the most attractive client base for global catering providers. They also have higher budgets for premium services, advanced kitchen infrastructure, and wellness-oriented meal programs.The key growth driver in this segment is the expansion of multinational corporations and global business networks requiring centralized catering management systems. Medium and small enterprises are gradually increasing adoption, particularly in urban and semi-urban areas, where outsourced catering is becoming more cost-effective than in-house operations. The rise of co-working spaces and shared office environments is also contributing to demand among smaller organizations. Flexible contract structures and modular service offerings are enabling catering providers to penetrate this segment more effectively, supporting long-term market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Catering and Food Service Contractor Market Segmentations

By Service Type

- Contract Catering

- Concession Catering

- Event Catering

- Industrial Catering

- Institutional Catering

- Hospitality Catering Services

By End-Use Industry

- Corporate & Business Offices

- Healthcare Facilities

- Education Institutions

- Industrial & Manufacturing Sites

- Defense & Government Institutions

- Sports & Leisure Facilities

- Travel & Tourism

By Service Delivery Mode

- Full-Service Catering

- Food Preparation & Delivery Only

- Managed Services

By Pricing Model

- Fixed Price Contracts

- Cost-Plus Contracts

- Revenue Sharing Models

By Cuisine Type

- Local/Regional Cuisine

- International Cuisine

- Multi-Cuisine

- Specialized Diet Catering

Regional Insights

North America

North America holds the largest share of approximately 32% in 2025, with the United States being the dominant contributor. The region benefits from a highly mature outsourcing ecosystem, strong corporate infrastructure, and widespread adoption of institutional catering services. The key driver of regional growth is the increasing demand for workplace wellness programs and outsourced facility management services across corporate, healthcare, and educational sectors. Organizations are prioritizing employee satisfaction through diversified meal offerings and nutrition-focused menus. Additionally, the presence of large-scale catering service providers and advanced food technology adoption further strengthens market leadership in this region.

Europe

Europe accounts for around 28% of the global market, driven by strong demand from countries such as the United Kingdom, Germany, and France. The region is characterized by a strong emphasis on sustainability, food quality, and regulatory compliance. One of the primary drivers of regional growth is the increasing focus on environmentally responsible catering practices, including locally sourced ingredients, waste reduction initiatives, and carbon footprint minimization. Premium catering services are also gaining traction, particularly in corporate and hospitality sectors. The expansion of healthcare infrastructure and aging population demographics further contribute to steady demand for institutional catering solutions.

Asia-Pacific

Asia-Pacific is the fastest-growing region, registering a CAGR exceeding 9%, driven by rapid industrialization, urbanization, and expansion of corporate sectors in countries such as China and India. The key growth driver is the increasing outsourcing of food services in both public and private sectors, supported by rising disposable incomes and changing lifestyle patterns. The expansion of IT hubs, manufacturing zones, and educational institutions is significantly boosting demand for large-scale catering operations. Additionally, government initiatives supporting workforce nutrition programs and infrastructure development are accelerating market penetration across emerging economies in the region.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth, supported by large-scale infrastructure projects, tourism expansion, and increasing expatriate workforce populations. Countries such as the United Arab Emirates and Saudi Arabia are major contributors due to their rapid urban development and hospitality sector growth. The primary driver of regional demand is the rising number of mega-projects, including smart cities, airports, and industrial zones that require large-scale catering solutions. Additionally, the growing hospitality and religious tourism sectors further strengthen demand for high-volume, culturally diverse catering services capable of serving international populations.

Latin America

Latin America is witnessing moderate but consistent growth, led by Brazil and Mexico. The region’s expansion is primarily driven by increasing investments in corporate infrastructure, healthcare facilities, and educational institutions. A key growth driver is the gradual shift toward outsourcing non-core services as organizations seek cost optimization and operational efficiency. The expansion of urban centers and rising corporate presence of multinational companies are also contributing to increased demand for professional catering services. Although the market remains relatively price-sensitive, improving economic stability and rising awareness of outsourced food service benefits are expected to support long-term growth.

Key Players in the Catering and Food Service Contractor Market

- Compass Group

- Sodexo

- Aramark

- Elior Group

- ISS A/S

- Delaware North

- CH&CO Group

- NTUC Foodfare

- DO & CO AG

- Gate Gourmet

- Albron

- BaxterStorey

- Wilson Vale

- Ovations Food Services

- TajSATS Air Catering