Global Virtual Restaurant & Ghost Kitchens Market Size

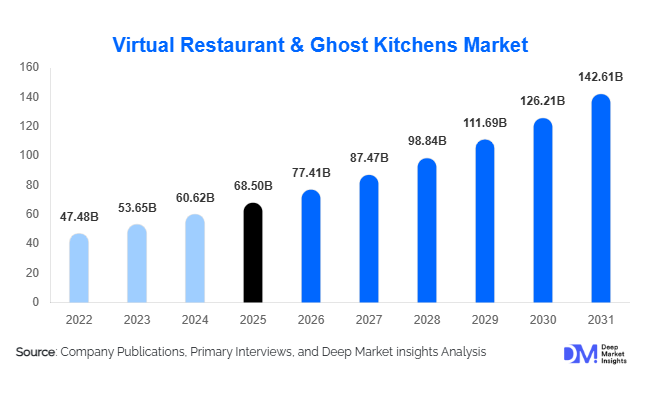

According to Deep Market Insights, the global virtual restaurant & ghost kitchens market size was valued at USD 68.5 million in 2026 and is projected to grow from USD 77.4 million in 2027 to reach USD 142.61 million by 2031, expanding at a CAGR of 13.0% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of food delivery ecosystems, rising demand for convenience-based dining, and increasing adoption of asset-light restaurant models that eliminate the need for traditional dine-in infrastructure. The shift toward digital-first food consumption, coupled with the rise of aggregator platforms and cloud kitchen networks, has fundamentally transformed how foodservice businesses scale globally.

Key Market Insights

- Delivery-first consumption is redefining the foodservice industry, with virtual restaurants becoming the default growth model for urban food demand.

- Cloud kitchen platforms are scaling rapidly across Tier 1 and Tier 2 cities, enabling multi-brand operations from centralized infrastructure.

- Asia-Pacific is emerging as the fastest-growing region, driven by high mobile penetration and booming food delivery ecosystems in India and China.

- North America dominates in market share, supported by strong QSR penetration and venture-backed ghost kitchen expansion.

- Multi-brand virtual restaurant strategies are gaining traction, allowing operators to run multiple cuisines from a single kitchen.

- AI and automation are reshaping operations, improving demand forecasting, inventory control, and delivery efficiency.

What are the latest trends in the virtual restaurant & ghost kitchens market?

Multi-Brand Virtual Kitchen Expansion

Operators are increasingly adopting multi-brand strategies where a single kitchen operates several virtual restaurant labels simultaneously. This allows businesses to target different consumer segments such as burgers, pizza, healthy meals, and Asian cuisine without expanding physical infrastructure. This model significantly improves asset utilization rates and revenue density per kitchen. It also enables rapid testing of new food concepts with minimal capital risk, making it one of the most dominant operational trends globally.

AI-Driven Kitchen Automation and Optimization

Artificial intelligence is playing a critical role in optimizing kitchen operations, from predicting order volumes to managing ingredient inventory and reducing food waste. AI-based systems are increasingly integrated with delivery platforms to streamline order batching and delivery routing. Robotics and semi-automated kitchen equipment are also being deployed to improve consistency and reduce dependency on manual labor, enhancing scalability in high-demand urban zones.

What are the key drivers in the virtual restaurant & ghost kitchens market?

Explosion of Online Food Delivery Platforms

The rapid penetration of food delivery platforms is the strongest driver of market growth. Consumers are increasingly shifting toward app-based ordering due to convenience, speed, and wide cuisine availability. This structural shift has created a strong demand base for delivery-only kitchens that operate without dine-in services, enabling scalable and cost-efficient food production models.

Cost Efficiency and Capital-Light Expansion Models

Ghost kitchens eliminate the need for expensive real estate, dine-in staff, and interior infrastructure. This reduces operational costs significantly compared to traditional restaurants. As a result, both startups and established QSR chains are using virtual kitchen models to expand into new geographies with lower financial risk and faster time-to-market.

Rising Demand for Food Variety and On-Demand Consumption

Consumers increasingly prefer diverse food options available on-demand. Virtual kitchens enable operators to launch multiple cuisine brands from a single facility, offering flexibility and variety without additional infrastructure costs. This demand for culinary experimentation is driving sustained market expansion globally.

What are the restraints for the global market?

High Dependency on Aggregator Platforms

Most virtual restaurants rely heavily on third-party delivery platforms, which charge high commission fees ranging between 15–35%. This reduces profit margins and limits direct customer relationships, making operators vulnerable to platform policy changes and pricing pressures.

Operational Complexity and Brand Dilution

Managing multiple virtual brands from a single kitchen creates operational challenges in quality control, consistency, and delivery timing. Without strong process automation, there is a risk of brand dilution and customer dissatisfaction, particularly in high-order-volume environments.

What are the key opportunities in the virtual restaurant industry?

Hyperlocal Kitchen Network Expansion

Expanding dense networks of micro-fulfillment kitchens in urban areas presents a major opportunity. These kitchens reduce delivery times and improve food freshness while enabling companies to penetrate high-demand zones more efficiently. Emerging economies with high population density present particularly strong growth potential for hyperlocal expansion models.

Direct-to-Consumer (D2C) Food Brands

Virtual restaurants are increasingly shifting toward D2C models using proprietary apps and websites. This reduces dependency on aggregators and improves customer retention through loyalty programs and personalized offers. Brands that build strong digital ecosystems are expected to achieve higher margins and stronger long-term scalability.

Franchise-Based Cloud Kitchen Expansion

Franchise-led ghost kitchen models are emerging as a scalable expansion strategy. By licensing virtual brands and kitchen infrastructure, companies can expand rapidly into new regions without heavy capital investment. This model is particularly attractive in emerging markets where local franchise partnerships accelerate market entry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.5 Billion |

| Market Size in 2026 | USD 77.41 Billion |

| Market Size in 2031 | USD 142.61 Billion |

| CAGR | 13% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Business Model Insights

The global virtual restaurant and cloud kitchen market is undergoing rapid transformation as foodservice operators increasingly adopt asset-light and technology-enabled operating models. Shared cloud kitchen platforms continue to dominate the competitive landscape, accounting for nearly 32% of the global market share in 2025. Their dominance is primarily attributed to the operational efficiency they provide by allowing multiple food brands to operate from a single kitchen infrastructure. This model significantly reduces upfront capital expenditure, minimizes rental costs, and improves kitchen utilization rates, making it highly attractive for startups as well as established restaurant operators. Shared kitchen operators are increasingly offering integrated services such as procurement support, delivery logistics, kitchen analytics, workforce management, and digital marketing solutions, further strengthening adoption across urban markets.Restaurant chains launching virtual brands within existing kitchen facilities are emerging as one of the fastest-growing business models globally. Traditional restaurant operators are increasingly utilizing underutilized kitchen capacity to introduce delivery-only brands that target different consumer demographics without impacting their primary dine-in identity. This strategy enables restaurant groups to diversify revenue streams, increase kitchen productivity, and offset fluctuating dine-in traffic. Large quick-service restaurant chains are particularly active in deploying multi-brand virtual strategies to penetrate new delivery segments and maximize customer acquisition through online food platforms.Virtual restaurant brands operating entirely within third-party kitchens are also gaining substantial momentum due to their low entry barriers and high scalability potential. Entrepreneurs and food startups are increasingly entering the market without investing in physical storefronts, thereby reducing operational risk while benefiting from growing digital food consumption trends. In addition, franchise-based cloud kitchen expansion models are emerging across developing economies, enabling rapid regional penetration with lower capital requirements. Strategic partnerships between kitchen operators, delivery aggregators, and food technology companies are further reshaping the competitive landscape and accelerating market consolidation globally.

Application Insights

Quick Service Restaurants (QSRs) continue to represent the dominant application segment within the global cloud kitchen and virtual restaurant market. The segment’s leadership is primarily driven by rising consumer demand for affordable, convenient, and fast meal delivery solutions. QSR operators are increasingly leveraging ghost kitchens to accelerate geographic expansion while minimizing infrastructure investments associated with traditional dine-in outlets. The ability to serve high-volume orders efficiently through optimized kitchen workflows has significantly improved profit margins for QSR-focused virtual brands.The rapid adoption of online food delivery applications and increasing consumer preference for digitally accessible meal options have further strengthened QSR demand within the cloud kitchen ecosystem. Large international restaurant chains are integrating delivery-only formats to target densely populated urban clusters and underserved suburban regions. Menu engineering, data analytics, and AI-driven customer personalization are increasingly being utilized to optimize product offerings and enhance order frequency among digitally engaged consumers.Institutional catering applications, including healthcare facilities, educational institutions, corporate offices, and industrial food supply services, are witnessing steady adoption of centralized cloud kitchen models. Organizations are increasingly outsourcing food preparation operations to technologically advanced kitchen providers capable of maintaining food quality consistency, hygiene compliance, and large-scale production efficiency. The growing need for customized meal programs, dietary management, and contactless food distribution has further strengthened demand within the institutional catering segment.Food delivery platforms themselves are becoming increasingly active participants within the cloud kitchen industry. Major aggregators are investing in proprietary kitchen networks and exclusive virtual restaurant partnerships to secure greater control over food supply chains and improve delivery economics. Platform-owned kitchens enable delivery companies to optimize service quality, reduce delivery times, and increase customer retention through exclusive menu offerings. The integration of predictive analytics and real-time demand mapping is further enabling delivery platforms to identify high-demand locations and deploy kitchen infrastructure strategically.

Distribution Channel Insights

Third-party food delivery aggregators continue to dominate the global distribution landscape, accounting for the majority of virtual restaurant order volumes worldwide. Their leadership is primarily supported by extensive customer reach, advanced logistics capabilities, and integrated digital payment ecosystems. Consumers increasingly prefer aggregator platforms due to the convenience of accessing multiple restaurant options, real-time order tracking, promotional discounts, and flexible payment solutions within a single application environment.The rapid expansion of smartphone penetration and digital payment adoption across both developed and emerging economies has further accelerated reliance on third-party ordering platforms. Aggregators are continuously investing in route optimization technologies, AI-driven customer recommendation engines, and delivery fleet expansion to improve operational efficiency and reduce order fulfillment times. The increasing availability of subscription-based delivery memberships and loyalty rewards programs is also strengthening customer engagement across online delivery ecosystems.Hybrid distribution models that combine aggregator visibility with direct-ordering capabilities are emerging as the most sustainable long-term strategy within the industry. Many restaurant operators are utilizing third-party platforms primarily for customer acquisition while encouraging repeat customers to transition toward direct ordering through loyalty incentives and exclusive promotions. This hybrid approach helps operators maintain broad market visibility while improving profitability and strengthening long-term customer retention.Subscription-based food delivery services and membership-driven meal programs are also gaining traction in major metropolitan markets. Consumers increasingly value predictable meal planning, discounted recurring deliveries, and customized subscription packages tailored to dietary preferences. This trend is particularly strong among working professionals, fitness-conscious consumers, and urban households seeking convenience-driven dining solutions. Technological integration, personalized recommendation systems, and AI-powered consumer analytics are expected to further transform distribution strategies across the global virtual restaurant ecosystem.

Customer Segment Insights

Urban millennials and Generation Z consumers represent the largest customer segment within the global cloud kitchen and virtual restaurant market. Their dominance is largely driven by high smartphone usage, strong digital engagement, and a growing preference for convenience-oriented consumption patterns. Younger consumers increasingly prioritize speed, affordability, and app-based accessibility when purchasing meals, making them highly responsive to virtual restaurant offerings. Social media influence, digital food marketing, and online brand visibility also play a major role in shaping purchasing behavior within this demographic.Working professionals continue to represent a highly valuable recurring demand segment due to increasingly hectic lifestyles and limited time availability for meal preparation. The rising prevalence of remote work and hybrid employment models has further increased dependence on food delivery services across urban areas. Cloud kitchens are responding by offering diversified menu options, faster delivery timelines, and customizable meal packages designed specifically for office workers and home-based professionals.Health-conscious consumers are emerging as a rapidly growing customer category, driving significant demand for specialized virtual brands focused on organic foods, calorie-controlled meals, vegan diets, protein-rich offerings, and wellness-oriented nutrition solutions. Consumers are increasingly seeking transparency regarding ingredient sourcing, nutritional value, and sustainable packaging practices. This trend has encouraged cloud kitchen operators to develop premium healthy-eating concepts and collaborate with nutrition-focused food brands.Family households continue to represent a stable and important customer base for value-oriented multi-cuisine offerings. Families increasingly prefer bundled meal packages, group-order discounts, and affordable combination menus that cater to varying taste preferences within households. Virtual restaurants are expanding family-focused offerings through larger portion sizes, regional cuisine diversity, and child-friendly menu customization. Increasing urbanization and changing family consumption patterns are expected to sustain demand growth within this segment over the forecast period.

Consumer Demographics Insights

The 25–40 age group remains the dominant demographic segment within the virtual restaurant market, supported by high disposable income levels, strong digital literacy, and frequent usage of online food delivery applications. Consumers within this age bracket are highly accustomed to app-based purchasing behavior and demonstrate strong willingness to experiment with new food concepts and digital dining experiences. The segment also benefits from rising urban employment levels and increasingly convenience-driven lifestyles.Younger consumers between 18–25 years of age play a critical role in driving experimentation and innovation within the market. This demographic is highly influenced by social media trends, influencer marketing, and viral food concepts, making them early adopters of emerging virtual restaurant brands. Limited-edition menu items, fusion cuisines, and visually appealing food presentations are particularly effective in attracting younger consumers across online platforms.Middle-income urban populations represent the largest volume-based consumer segment globally. Rising middle-class expansion across developing economies has significantly increased demand for affordable and accessible food delivery solutions. Consumers within this demographic prioritize convenience, value pricing, and delivery reliability, making cloud kitchen models highly attractive in densely populated metropolitan areas.Premium consumers are increasingly shifting toward gourmet virtual restaurant concepts that provide restaurant-quality dining experiences within home environments. High-income urban consumers are demonstrating growing interest in premium ingredients, chef-curated menus, artisanal food offerings, and personalized meal experiences. This trend is encouraging luxury dining brands and fine-dining restaurants to establish delivery-only premium virtual brands to capitalize on changing consumption preferences.

Explore more data points, trends and opportunities Download Free Sample Report

Virtual Restaurant & Ghost Kitchens Market Segmentations

By Business Model

- Shared Kitchen / Cloud Kitchen Platforms

- Independent Ghost Kitchens

- Virtual Restaurant Brands

- Restaurant Chain Virtual Brands

By Kitchen Type

- Centralized Industrial Cloud Kitchens

- Decentralized Micro-Kitchens

- Franchise-Based Ghost Kitchens

By Order Channel / Platform

- Third-Party Aggregator Platforms

- Direct-to-Consumer (D2C) Channels

- Hybrid Ordering Systems

By Cuisine Type

- Fast Food & Burgers

- Asian Cuisine

- Pizza & Italian Cuisine

- Healthy & Organic Meals

- Desserts, Beverages & Snacks

By End-Use Industry

- Quick Service Restaurants (QSRs)

- Full-Service Restaurants

- Retail & Grocery Prepared Food Services

- Institutional & Catering Services

Regional Insights

North America

North America accounts for approximately 38% of the global cloud kitchen and virtual restaurant market share in 2025, making it the largest regional market worldwide. The United States continues to dominate regional revenue generation due to the strong presence of advanced food delivery ecosystems, high consumer spending on convenience foods, and significant venture capital investment within the food technology sector. Major metropolitan cities across the U.S. are witnessing rapid expansion of delivery-only restaurant concepts driven by rising labor costs, increasing urban rental expenses, and changing consumer dining preferences.Another major driver supporting regional growth is the increasing consumer preference for convenience-oriented lifestyles and on-demand food services. The rising popularity of subscription-based meal delivery services, premium virtual dining concepts, and health-focused delivery brands is reshaping market dynamics across North America. Canada is also witnessing steady growth due to increasing urbanization, rising immigrant populations driving cuisine diversification, and growing investments in digital foodservice infrastructure.

Europe

Europe represents nearly 25% of the global market share, led by the United Kingdom, Germany, and France. The region’s cloud kitchen market is characterized by strong consumer demand for premium-quality delivery meals, increasing digitalization within the foodservice industry, and rising adoption of sustainable business practices. European consumers increasingly prioritize food quality, ingredient transparency, and environmentally responsible operations, encouraging virtual restaurant operators to invest in eco-friendly packaging and sustainable sourcing strategies.Government regulations supporting digital transformation, food safety compliance, and sustainability initiatives are also contributing to market development across Europe. The region’s strong emphasis on reducing food waste and promoting environmentally sustainable delivery operations is encouraging investments in efficient kitchen technologies and optimized logistics systems. Furthermore, increasing cross-border investments by global delivery platforms and restaurant chains are strengthening market penetration across emerging European urban centers.

Asia-Pacific

Asia-Pacific holds approximately 30% share of the global market and is projected to remain the fastest-growing regional segment during the forecast period. Rapid urbanization, expanding middle-class populations, and strong smartphone penetration are major drivers supporting market growth across the region. India and China remain the dominant markets due to their massive food delivery ecosystems, rising disposable incomes, and increasing consumer preference for convenience-oriented dining solutions.Southeast Asian economies including Indonesia, Thailand, Vietnam, and Singapore are also emerging as attractive growth markets due to expanding internet penetration, rising urban food consumption, and increasing investments by international delivery aggregators. The growing popularity of digital-first dining experiences and social commerce-driven food ordering is expected to sustain long-term regional growth.

Latin America

Latin America represents approximately 3% of the global market, with Brazil and Mexico emerging as the leading countries within the region. Increasing urbanization, growing internet accessibility, and expanding middle-income populations are key drivers supporting market growth. Younger consumers across major cities are increasingly adopting app-based food ordering services due to convenience, affordability, and greater cuisine variety.Cloud kitchens are particularly attractive within Latin America due to their lower operational costs compared to traditional restaurant models. Operators are increasingly targeting densely populated urban regions where demand for affordable meal delivery continues to rise. Local cuisine-focused virtual brands and value-driven meal offerings are gaining strong traction among price-sensitive consumers, while international food chains are increasingly utilizing delivery-only formats to strengthen regional expansion.

Middle East & Africa

The Middle East & Africa region accounts for nearly 4% of the global market share, led primarily by the United Arab Emirates and Saudi Arabia. High disposable income levels, strong digital adoption, and increasing demand for premium food delivery services are major drivers supporting cloud kitchen market growth across the Middle East. Consumers in Gulf countries demonstrate strong preference for convenience-oriented dining solutions, luxury food offerings, and technologically advanced delivery experiences.Africa is gradually emerging as a promising growth market due to rising urbanization, expanding internet penetration, and improving smartphone accessibility. Countries such as South Africa and Kenya are witnessing increasing adoption of online food delivery applications among younger urban consumers. The growing presence of regional food delivery startups, combined with increasing investments in logistics infrastructure and digital payment systems, is expected to accelerate long-term cloud kitchen market growth across the African continent.

Key Players in the Virtual Restaurant & Ghost Kitchens Market

- CloudKitchens

- Rebel Foods

- Kitopi

- Kitchen United

- Ghost Kitchen Brands

- Reef Technology

- Zuul Kitchens

- Virtual Dining Concepts

- DoorDash Kitchens

- Deliveroo Editions

- Swiggy (Cloud Kitchen Operations)

- Oyo Kitchens

- Foodpanda Kitchen Network

- Wonder Group

- Tata Neu Kitchens