Sushi Market Size

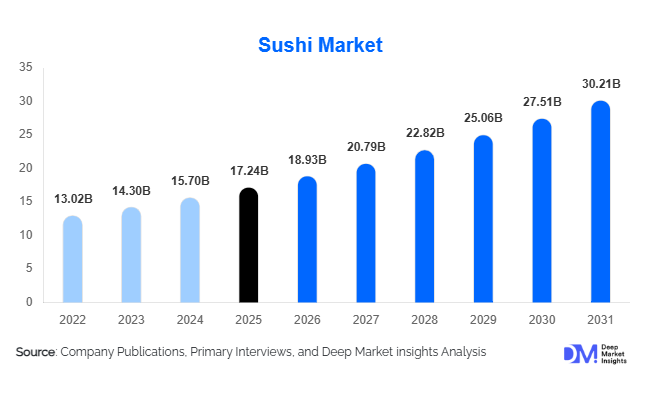

According to Deep Market Insights, the global sushi market size was valued at USD 17.24 billion in 2025 and is projected to grow from USD 18.93 billion in 2026 to reach USD 30.21 billion by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The sushi market growth is primarily driven by rising global demand for Japanese cuisine, increasing consumer preference for healthy ready-to-eat meals, and rapid expansion of organized sushi restaurant chains across developed and emerging economies.

Key Market Insights

- Sushi consumption is increasingly shifting toward premium and health-oriented meal options, supported by rising awareness regarding seafood nutrition and protein-rich diets.

- Retail packaged sushi is expanding rapidly across supermarkets and convenience stores, driven by growing demand for fresh grab-and-go food products.

- Asia-Pacific dominates the global sushi market, led by strong domestic consumption in Japan, China, and South Korea.

- North America remains one of the fastest-growing regional markets, supported by rising popularity of Japanese cuisine and food delivery platforms.

- Plant-based and sustainable sushi offerings are gaining traction globally, particularly among environmentally conscious consumers in Europe and North America.

- Technological integration, including robotic sushi preparation, AI-enabled inventory systems, and automated conveyor-belt dining formats, is transforming operational efficiency across the industry.

Sushi Market Latest Trends

Rise of Plant-Based and Sustainable Sushi

The global sushi market is witnessing strong growth in plant-based and sustainable sushi offerings as consumers increasingly prioritize environmental sustainability and ethical seafood sourcing. Restaurants and manufacturers are introducing vegan sushi variants featuring plant-based tuna, salmon substitutes, tofu fillings, seaweed proteins, and vegetable-based ingredients. Sustainability certifications related to seafood sourcing are becoming important differentiators for premium sushi brands. Growing concerns regarding overfishing, marine biodiversity loss, and seafood traceability are encouraging operators to diversify ingredient sourcing and invest in sustainable procurement programs. Supermarkets and retail sushi brands are also expanding vegan sushi assortments to cater to flexitarian consumers seeking healthier and environmentally friendly alternatives.

Technology-Driven Sushi Preparation and Delivery

Automation and smart kitchen technologies are increasingly reshaping sushi preparation and distribution globally. Conveyor-belt sushi restaurants integrated with RFID tracking systems, robotic sushi rollers, automated rice preparation systems, and AI-driven demand forecasting tools are improving efficiency while reducing food wastage. Delivery-oriented sushi chains are investing heavily in temperature-controlled logistics and cloud kitchen infrastructure to support online food ordering growth. Digital ordering systems, QR-code menus, and app-based loyalty platforms are enhancing customer engagement and operational scalability. In addition, advanced packaging technologies are helping retailers improve shelf life and freshness standards for packaged sushi products distributed through supermarkets and convenience stores.

Sushi Market Drivers

Growing Demand for Healthy and Protein-Rich Foods

Rising global health consciousness is one of the primary factors driving sushi market expansion. Consumers increasingly perceive sushi as a healthier alternative to traditional fast food because of its lean protein content, omega-3 fatty acids, low saturated fat composition, and balanced nutritional profile. Salmon and tuna sushi products are particularly popular among health-conscious consumers seeking nutrient-rich meal options. Urban consumers, millennials, and younger demographics are increasingly shifting toward seafood-based diets and lighter meal formats, further supporting demand for sushi products globally. The growing popularity of Japanese cuisine and wellness-focused dining trends is also positively influencing long-term market growth.

Rapid Expansion of Organized Sushi Restaurant Chains

The global expansion of sushi-focused restaurant chains, conveyor-belt dining formats, and Japanese quick-service restaurants is significantly accelerating market growth. Franchising models and standardized operational systems have enabled sushi brands to scale rapidly across North America, Europe, Southeast Asia, and the Middle East. Major metropolitan cities are witnessing increasing penetration of sushi restaurants across premium dining, mid-scale dining, and fast-casual formats. The integration of digital ordering systems and food delivery partnerships has further improved accessibility and repeat consumer purchases. Cloud kitchen models focused exclusively on sushi delivery are also emerging rapidly in urban centers.

Global Market Restraints

Volatility in Seafood Prices

The sushi market remains highly dependent on seafood supply chains, making it vulnerable to fluctuations in tuna, salmon, eel, crab, and shrimp prices. Seasonal fishing restrictions, climate-related disruptions, international trade regulations, and overfishing concerns often create supply instability and increase raw material costs. Price volatility directly affects restaurant profitability and retail pricing strategies, especially in premium sushi segments dependent on imported seafood. Smaller operators with limited procurement scale are particularly vulnerable to sudden cost increases, which can negatively impact operating margins.

Food Safety and Shelf-Life Challenges

Sushi products require strict hygiene protocols, cold-chain management, and temperature-controlled logistics because of the perishability of raw seafood ingredients. Risks associated with bacterial contamination, parasites, and improper seafood handling continue to present operational challenges for restaurants and packaged sushi manufacturers. Compliance with international food safety standards, seafood traceability regulations, and import inspection procedures increases operating complexity and costs. Retail sushi operators also face challenges in maintaining freshness while minimizing food wastage and inventory losses.

Sushi Industry Key Opportunities

Expansion of Retail Packaged Sushi

The rapid expansion of organized retail infrastructure presents major growth opportunities for packaged sushi manufacturers globally. Supermarkets, hypermarkets, and convenience stores are increasingly dedicating refrigerated shelf space to ready-to-eat sushi products due to rising demand for convenient healthy meals. Retail sushi kiosks and in-store preparation counters are expanding significantly across North America and Europe. Improvements in packaging technologies and cold-chain logistics are enabling broader geographic penetration while maintaining product freshness. This trend is expected to create substantial growth opportunities for manufacturers investing in scalable centralized production systems and automated packaging facilities.

Growth of Premium Omakase and Experiential Dining

The premium dining segment is creating new opportunities for luxury sushi experiences globally. Affluent consumers are increasingly seeking chef-led omakase dining formats that emphasize exclusivity, authenticity, and premium imported seafood ingredients. Luxury hotels, resorts, and fine-dining establishments are expanding Japanese culinary offerings to cater to high-income travelers and experiential diners. Omakase restaurants in cities such as Tokyo, Dubai, Singapore, London, Paris, and New York are witnessing strong demand growth. Integration of cultural storytelling, personalized tasting menus, and sustainable seafood sourcing is further differentiating premium sushi brands in competitive urban markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17.24 Billion |

| Market Size in 2026 | USD 18.93 Billion |

| Market Size in 2031 | USD 30.21 Billion |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Maki sushi dominates the global sushi market, accounting for the largest share due to its affordability, wide flavor variety, and adaptability to regional taste preferences. Uramaki and specialty rolls have gained significant popularity across North America and Europe because they incorporate localized ingredients such as cream cheese, avocado, spicy sauces, and cooked seafood. Nigiri sushi remains highly popular in premium dining and omakase restaurants, particularly in Japan and luxury urban markets globally. Sashimi continues to hold a strong position among health-conscious consumers seeking high-protein and low-carbohydrate meal options. Frozen and ready-to-eat sushi products are also expanding rapidly due to growth in retail packaged food consumption and online delivery services. Plant-based and vegan sushi categories are emerging strongly, particularly among younger demographics and environmentally conscious consumers seeking sustainable food alternatives.

Application Insights

Foodservice applications continue to dominate the sushi market, driven by strong global demand for dine-in Japanese cuisine experiences. Sushi restaurants, conveyor-belt chains, quick-service Japanese outlets, and hotel dining establishments account for the majority of global consumption volumes. Retail applications are rapidly gaining traction through packaged sushi sales in supermarkets, convenience stores, and specialty Asian grocery chains. Corporate catering, airline catering, and rail catering are emerging as important niche applications due to sushi’s premium image and compact packaging suitability. Household consumption is also rising significantly as consumers increasingly purchase chilled and ready-to-eat sushi products for home dining. Growth in online food delivery applications has further accelerated demand for sushi across urban markets globally.

Distribution Channel Insights

Foodservice remains the dominant distribution channel in the global sushi market, supported by strong consumer preference for freshly prepared sushi and experiential dining formats. Sushi restaurants and quick-service Japanese chains continue expanding aggressively across major metropolitan markets. Retail distribution through supermarkets, hypermarkets, and convenience stores is witnessing rapid growth due to rising demand for grab-and-go meal solutions. Online delivery platforms are emerging as one of the fastest-growing channels, particularly among younger urban consumers who prioritize convenience and digital ordering experiences. Cloud kitchen models focused exclusively on sushi preparation are expanding rapidly across Asia-Pacific, North America, and the Middle East. Direct-to-consumer mobile applications and loyalty-based subscription systems are also helping brands strengthen customer retention and repeat purchases.

Consumer Type Insights

Individual consumers represent the largest share of sushi demand globally, driven by rising urbanization, increasing disposable incomes, and evolving dietary preferences. Younger consumers and working professionals are major contributors to growth due to strong demand for convenient, healthy meal options. Family consumption is increasing steadily, particularly through retail packaged sushi and casual dining restaurant formats that offer affordability and menu variety. Corporate consumers are contributing to demand through catering services, business events, and premium workplace dining programs. Tourist and hospitality-driven consumption remains highly important in premium hotel and resort markets where sushi is positioned as a luxury culinary experience.

Price Range Insights

Mid-range sushi accounts for the largest share of the global market because it balances affordability with quality dining experiences. Quick-service sushi chains and casual Japanese dining formats are expanding aggressively within this category across urban centers globally. Premium sushi products and omakase dining experiences are witnessing strong growth among affluent consumers willing to pay higher prices for imported seafood, chef expertise, and exclusive culinary experiences. Economy sushi products sold through convenience stores and supermarkets remain highly popular in Japan, South Korea, and several Western markets due to their affordability and accessibility. Luxury sushi continues expanding as an ultra-premium segment supported by tourism, fine dining, and luxury hospitality industries.

Explore more data points, trends and opportunities Download Free Sample Report

Sushi Market Segmentations

By Product Type

- Nigiri Sushi

- Maki Sushi

- Sashimi

- Chirashi Sushi

- Inari Sushi

- Pressed Sushi

- Vegetarian & Vegan Sushi

- Frozen & Ready-to-Eat Sushi

By Ingredient Type

- Fish & Seafood-Based Sushi

- Meat-Based Sushi

- Vegetarian Sushi

- Vegan Sushi

By Distribution Channel

- Foodservice

- Retail

- Online & Delivery Platforms

- Institutional Sales

By Price Range

- Economy Sushi

- Mid-Range Sushi

- Premium Sushi

- Luxury/Omakase Sushi

By Consumer Type

- Individual Consumers

- Families

- Corporate Consumers

- Tourists & Hospitality Consumers

Regional Insights

North America

North America accounted for nearly 27% of the global sushi market in 2025 and remains one of the fastest-growing regional markets globally. The United States dominates regional demand due to the widespread popularity of Japanese cuisine, rapid expansion of sushi restaurant chains, and increasing health-conscious dining trends. Major cities such as New York, Los Angeles, Chicago, and Miami continue witnessing strong premium sushi demand. Retail packaged sushi sales are also increasing rapidly through supermarkets and convenience store networks. Canada is witnessing steady growth supported by urban multicultural populations and increasing demand for fresh ready-to-eat meals.

Europe

Europe is emerging as a major growth hub for sushi consumption, particularly across the United Kingdom, Germany, France, Italy, and Spain. Consumers in the region are increasingly embracing Japanese cuisine, premium seafood products, and healthy dining alternatives. Retail packaged sushi has gained strong traction through supermarket chains and convenience stores across Western Europe. London and Paris have become important centers for premium omakase dining and fusion sushi concepts. Sustainability concerns are also encouraging demand for responsibly sourced seafood and vegan sushi alternatives across European markets.

Asia-Pacific

Asia-Pacific dominated the global sushi market with approximately 43% market share in 2025. Japan remains the largest market globally due to deeply rooted cultural consumption patterns, high seafood intake, and extensive restaurant infrastructure. China is emerging as a rapidly growing market supported by urbanization, rising disposable incomes, and increasing exposure to Japanese cuisine. South Korea and Singapore continue demonstrating strong demand for premium sushi products due to high seafood consumption and advanced foodservice industries. India and Southeast Asian countries are also witnessing rising demand through organized restaurant expansion and food delivery adoption.

Latin America

Latin America is gradually developing into a promising sushi market led by Brazil, Mexico, Chile, and Peru. Brazil represents the largest regional market due to its strong Japanese diaspora population and established fusion sushi culture. Mexico is witnessing rapid expansion of sushi restaurant chains and delivery-oriented Japanese cuisine formats. Increasing middle-class spending and growing consumer interest in international cuisine are positively supporting market growth across the region.

Middle East & Africa

The Middle East & Africa region is witnessing rising sushi demand due to tourism growth, luxury hospitality expansion, and increasing expatriate populations. The UAE remains the dominant regional market supported by Dubai’s premium dining ecosystem and strong international tourism inflows. Saudi Arabia is also emerging as a promising market due to urban development and increasing consumer spending on premium dining experiences. Luxury hotels and fine-dining establishments across the Gulf region continue expanding Japanese cuisine offerings to cater to affluent international travelers and business consumers.

Key Players in the Sushi Market

- Kura Sushi Inc.

- Sushiro Global Holdings Ltd.

- Genki Sushi Co., Ltd.

- YO! Sushi

- Zensho Holdings Co., Ltd.

- Bento Sushi

- Hissho Sushi

- Hama Sushi

- Sushi Train

- Marine Foods Corporation