Global Bakery Market Size

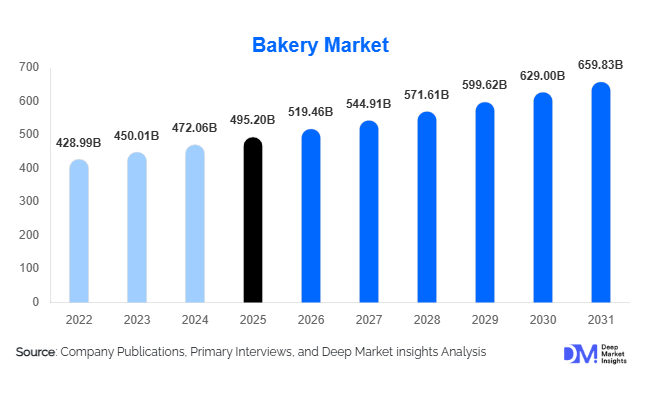

According to Deep Market Insights, the global bakery market size was valued at USD 495.2 billion in 2025 and is projected to grow from USD 519.46 billion in 2026 to reach USD 659.83 billion by 2031, expanding at a CAGR of 4.9% during the forecast period (2026–2031). The bakery market growth is primarily driven by rising consumption of convenience foods, increasing demand for premium and artisanal bakery products, expansion of organized retail channels, and growing consumer preference for healthier bakery formulations such as whole-grain, high-protein, gluten-free, and low-sugar products. Continuous innovation in frozen bakery technologies, automated production systems, and clean-label ingredients is further supporting industry expansion across both developed and emerging economies.

Key Market Insights

- Bread and rolls remain the largest product category, accounting for nearly 42% of global bakery market revenue due to their staple food status across most countries.

- Frozen bakery products are among the fastest-growing segments, driven by demand from foodservice operators, hotels, cafés, and quick-service restaurants seeking operational efficiency.

- Europe dominates the global bakery market, supported by strong bakery traditions, high per-capita bread consumption, and advanced manufacturing infrastructure.

- Asia-Pacific is the fastest-growing regional market, fueled by urbanization, rising disposable incomes, modern retail penetration, and changing dietary preferences.

- Health-focused bakery products are gaining market share, including gluten-free, organic, vegan, whole-grain, and protein-fortified offerings.

- Automation and digital manufacturing technologies are increasingly being deployed to improve productivity, consistency, energy efficiency, and quality control across bakery operations.

Global Bakery Market Latest Trends

Premiumization and Artisan Bakery Expansion

Consumers are increasingly moving beyond conventional packaged bakery products and seeking premium, artisanal, and specialty baked goods. Demand for sourdough breads, handcrafted pastries, premium cakes, specialty cookies, and regional bakery products has accelerated across North America, Europe, and major Asia-Pacific cities. Premium bakery products are benefiting from consumer willingness to pay higher prices for perceived quality, authenticity, natural ingredients, and unique flavor profiles. Retailers and manufacturers are responding by expanding premium product portfolios and investing in in-store bakery formats that offer fresh and customized products. Premiumization is also extending into packaged bakery categories through premium ingredients, gourmet fillings, clean-label formulations, and limited-edition product launches.

Health-Oriented Product Innovation

Health and wellness trends are significantly reshaping bakery product development globally. Consumers increasingly demand products that align with nutritional goals while maintaining taste and convenience. Whole-grain breads, gluten-free products, high-protein snacks, reduced-sugar cakes, vegan pastries, and fiber-enriched bakery products are experiencing above-average growth. Manufacturers are incorporating functional ingredients such as plant proteins, seeds, ancient grains, probiotics, and natural sweeteners to address evolving consumer preferences. Clean-label initiatives are also becoming a major differentiator, with brands reducing artificial preservatives, colors, and additives. This trend is particularly strong among younger consumers and urban populations seeking healthier alternatives without sacrificing convenience.

Global Bakery Market Drivers

Rising Demand for Convenience Foods

Convenience remains one of the strongest growth drivers for the bakery industry. Busy lifestyles, increasing urbanization, and rising workforce participation are encouraging consumers to choose ready-to-eat and on-the-go food products. Bakery products offer affordability, portability, extended shelf life, and versatility across multiple meal occasions. Bread, muffins, bagels, croissants, snack cakes, and cookies continue to serve as convenient breakfast, snack, and meal accompaniment options. Growth in convenience-oriented consumption is particularly evident across emerging economies where modern retail infrastructure and packaged food penetration are expanding rapidly.

Expansion of Organized Retail and Foodservice Networks

The rapid growth of supermarkets, hypermarkets, convenience stores, café chains, quick-service restaurants, and online grocery platforms has significantly improved accessibility to bakery products. Modern retail formats provide broader product assortments, stronger brand visibility, and improved cold-chain infrastructure for frozen bakery products. Simultaneously, the expansion of foodservice establishments worldwide is generating substantial demand for buns, rolls, croissants, pastries, desserts, and frozen bakery solutions. The foodservice sector increasingly relies on standardized bakery products that ensure consistency and operational efficiency.

Global Bakery Market Restraints

Raw Material Price Volatility

The bakery industry remains highly exposed to fluctuations in wheat, flour, sugar, edible oils, dairy products, eggs, and cocoa prices. Climate variability, geopolitical disruptions, agricultural supply shortages, and transportation costs contribute to pricing volatility. Manufacturers often face challenges in passing cost increases directly to consumers, resulting in margin pressure. Sustained inflationary environments can also impact consumer purchasing behavior, particularly in price-sensitive markets where bakery products compete on affordability.

Health Concerns Related to Refined Ingredients

Growing awareness regarding obesity, diabetes, cardiovascular diseases, and excessive sugar consumption presents challenges for traditional bakery products. Consumers are increasingly scrutinizing ingredient lists and nutritional content. Regulatory initiatives targeting sugar reduction, nutritional labeling, and healthier food choices are compelling manufacturers to reformulate products. Companies that fail to adapt to changing health preferences may face slower growth and reduced market relevance in the long term.

Global Bakery Industry Key Opportunities

Functional and Nutritional Bakery Products

The functional foods movement presents a substantial growth opportunity for bakery manufacturers. Consumers are increasingly seeking products that deliver nutritional benefits beyond basic sustenance. High-protein breads, fiber-enriched products, keto-friendly bakery items, fortified breakfast products, and gut-health formulations incorporating probiotics are creating new revenue streams. Functional bakery products typically command premium pricing while addressing consumer demand for wellness-focused food choices. Companies investing in nutritional innovation are expected to benefit from higher margins and stronger brand differentiation.

Frozen Bakery and Emerging Market Expansion

Frozen bakery products represent one of the most attractive growth opportunities within the industry. Foodservice operators, hotels, cafés, and retailers increasingly prefer frozen dough and ready-to-bake products due to labor savings, reduced waste, and improved consistency. Simultaneously, emerging markets such as India, Indonesia, Vietnam, Saudi Arabia, and Brazil are witnessing rapid growth in bakery consumption driven by urbanization and rising disposable incomes. Investments in cold-chain infrastructure and modern retail formats are creating favorable conditions for frozen bakery expansion across these high-growth regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 495.20 Billion |

| Market Size in 2026 | USD 519.46 Billion |

| Market Size in 2031 | USD 659.83 Billion |

| CAGR | 4.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bread and rolls dominate the global bakery market, accounting for approximately 42% of total market revenue in 2025. The category benefits from its status as a daily staple food across developed and emerging economies alike. Packaged bread remains the largest sub-segment, while artisanal and specialty breads are expanding rapidly due to premiumization trends. Cakes and pastries represent the second-largest product category, supported by celebrations, gifting occasions, and café culture expansion. Biscuits and cookies continue to experience strong demand because of their convenience, portability, and long shelf life. Frozen bakery products represent the fastest-growing product segment, supported by increasing adoption across foodservice and retail sectors. Growth in frozen dough, ready-to-bake pastries, and frozen bread products is being driven by labor shortages and demand for operational efficiency among commercial food operators.

Ingredient Profile Insights

Conventional bakery products continue to account for approximately 76% of global market revenue due to their affordability, widespread availability, and established consumer preferences. However, health-oriented ingredient profiles are gaining market share at a faster pace than traditional products. Whole-grain bakery products are witnessing robust growth as consumers seek higher fiber intake and improved nutritional value. Gluten-free bakery products are benefiting from increased diagnosis of gluten intolerance as well as broader lifestyle adoption. Organic bakery products are expanding rapidly in developed markets, supported by clean-label preferences and sustainability considerations. High-protein and vegan bakery categories are also emerging as important growth areas, particularly among younger consumers and fitness-conscious demographics.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 38% of global bakery sales. Their extensive product assortment, promotional activities, and convenience continue to attract consumers across all demographic groups. Convenience stores play a significant role in urban markets, particularly for impulse purchases and on-the-go consumption. Specialty bakery stores and independent bakeries maintain strong positions in premium and artisanal product categories, where freshness and customization are valued. Online retail channels are among the fastest-growing distribution segments as consumers increasingly embrace digital grocery shopping and direct-to-consumer bakery deliveries. Foodservice distributors are becoming increasingly important due to rising demand from cafés, restaurants, hotels, and institutional buyers.

End-Use Insights

Household consumers account for approximately 68% of global bakery demand, making retail consumption the largest end-use segment. Bread, cookies, cakes, and breakfast bakery products remain integral components of daily diets across most countries. Foodservice operators represent the fastest-growing end-use category, driven by the expansion of quick-service restaurants, cafés, coffee chains, hotels, and bakery cafés. Institutional demand from schools, hospitals, and corporate cafeterias continues to provide stable purchasing volumes. Industrial food manufacturers also contribute significantly through demand for bakery ingredients and semi-finished bakery products used in frozen foods, sandwiches, desserts, and snack applications. Growing exports of frozen bakery products are creating additional demand across international foodservice and retail markets.

Explore more data points, trends and opportunities Download Free Sample Report

Bakery Market Segmentations

By Product Type

- Bread & Rolls

- Cakes & Pastries

- Biscuits & Cookies

- Crackers & Crispbreads

- Breakfast Bakery Products

- Frozen Bakery Products

- Other Bakery Products

By Ingredient Profile

- Conventional Bakery Products

- Organic Bakery Products

- Gluten-Free Bakery Products

- High-Protein Bakery Products

- Whole Grain Bakery Products

- Low-Sugar Bakery Products

- Vegan Bakery Products

- Clean-Label Bakery Products

By Freshness/Form

- Fresh Bakery Products

- Frozen Bakery Products

- Shelf-Stable Bakery Products

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Bakery Stores

- Independent Bakeries

- Online Retail & E-Commerce

- Foodservice Distributors

- Club Stores & Cash-and-Carry

By End User

- Household Consumers

- Foodservice Operators

- Institutional Buyers

- Industrial Food Manufacturers

Regional Insights

North America

North America accounted for approximately 27% of global bakery market revenue in 2025. The United States dominates regional demand due to its large packaged food industry, advanced retail infrastructure, and strong consumer spending power. Demand for premium, organic, gluten-free, and high-protein bakery products continues to rise across the region. Canada is experiencing steady growth in artisan bakery products and clean-label offerings, while Mexico benefits from strong consumption of bread, pastries, and sweet baked goods.

Europe

Europe remains the largest regional market, accounting for approximately 33% of global bakery industry revenue in 2025. Germany, France, Italy, the United Kingdom, Spain, and Poland represent major production and consumption centers. Bread remains deeply embedded in European dietary habits, while premium pastries and artisanal products continue to drive value growth. Strong bakery traditions, advanced manufacturing capabilities, and widespread consumer acceptance of premium products support Europe's leadership position. Sustainability, organic ingredients, and clean-label formulations are increasingly influencing product innovation throughout the region.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of global bakery revenue in 2025 and represents the fastest-growing regional market. China leads regional consumption through its expanding middle class and rapid urbanization. India is expected to register the fastest growth globally, with bakery demand increasing at more than 8% CAGR through 2031. Japan and South Korea maintain mature bakery markets characterized by premium and innovative products. Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are benefiting from rising disposable incomes, westernization of diets, and modern retail expansion.

Latin America

Latin America represented approximately 9% of global bakery market revenue in 2025. Brazil remains the largest regional market, supported by high bread consumption and a growing packaged food industry. Mexico follows closely, driven by demand for sweet baked goods, tortillas, pastries, and convenience foods. Increasing supermarket penetration and rising urbanization are supporting long-term market expansion throughout the region.

Middle East & Africa

The Middle East & Africa accounted for approximately 7% of global bakery demand in 2025. Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Turkey represent key growth markets. Rising urbanization, growing tourism sectors, expanding foodservice industries, and increasing disposable incomes are driving bakery consumption. Premium bakery products, frozen bakery imports, and café culture expansion are contributing significantly to regional growth. Investments in food manufacturing infrastructure are further strengthening local production capabilities.

Key Players in the Global Bakery Market

- Grupo Bimbo

- Mondelez International

- Associated British Foods

- General Mills

- Nestlé

- Flowers Foods

- Yamazaki Baking

- Aryzta AG

- Britannia Industries

- Barilla Group

- Lantmännen Unibake

- Kellanova

- Campbell Soup Company

- Finsbury Food Group

- Hostess Brands