Weissbier Market Size

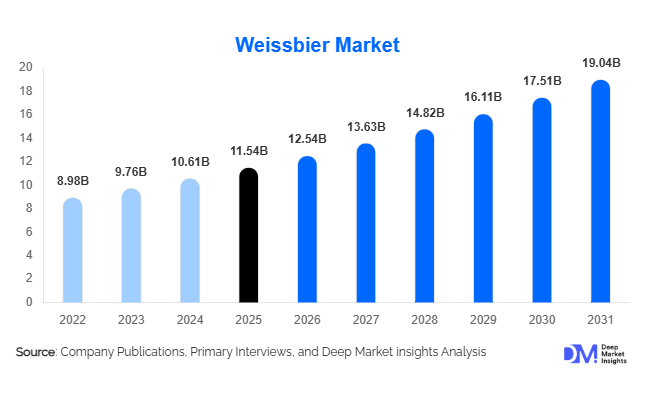

According to Deep Market Insights, theglobal Weissbier market size was valued at USD 11.54 billion in 2025 and is projected to grow from USD 12.54 billion in 2026 to reach USD 19.04 billion by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The Weissbier market growth is primarily driven by the increasing premiumization of alcoholic beverages, rising consumer demand for authentic craft-style wheat beers, and expanding adoption of flavored and alcohol-free wheat beer variants across developed and emerging economies.

Key Market Insights

- Premium and craft Weissbier products are gaining strong traction globally, driven by consumer preference for artisanal brewing methods, authentic Bavarian flavors, and premium drinking experiences.

- Alcohol-free Weissbier is emerging as one of the fastest-growing categories, supported by health-conscious consumers, wellness trends, and stricter alcohol consumption regulations.

- Europe dominates the global Weissbier market, with Germany remaining the largest producer and consumer due to its strong brewing heritage and export leadership.

- Asia-Pacific is the fastest-growing regional market, led by rising premium beer demand in China, India, Japan, South Korea, and Southeast Asia.

- E-commerce and direct-to-consumer beer sales are reshaping distribution channels, allowing specialty wheat beer brands to expand market accessibility beyond traditional retail.

- Sustainable brewing technologies and recyclable packaging adoption are accelerating, as breweries increasingly focus on energy-efficient production and environmentally responsible operations.

Weissbier Market Latest Trends

Alcohol-Free and Low-ABV Weissbier Expanding Rapidly

Consumer demand for healthier alcoholic beverage alternatives is driving rapid expansion of alcohol-free and low-alcohol Weissbier products globally. Health-conscious consumers increasingly seek beverages that retain traditional wheat beer flavor profiles while reducing alcohol intake and calorie consumption. Breweries across Germany, Japan, and the United States are investing heavily in advanced dealcoholization technologies to improve taste retention and product quality. Alcohol-free Weissbier is also benefiting from rising sports-oriented marketing campaigns due to its isotonic characteristics and refreshment positioning. Retailers are allocating greater shelf space to wellness-oriented beer categories, while restaurants and hospitality venues are increasingly incorporating low-ABV wheat beer options into premium beverage menus.

Craft and Flavored Wheat Beer Innovation Accelerating

Craft breweries worldwide are introducing innovative Weissbier variants featuring fruit infusions, barrel aging, spice blends, and seasonal formulations. Consumers, particularly millennials and Gen Z demographics, increasingly prefer differentiated beer experiences over conventional lagers. Tropical fruit-infused, citrus-flavored, and botanical wheat beers are witnessing rising popularity across North America and Asia-Pacific. Small and mid-sized breweries are leveraging localized flavor experimentation to create region-specific premium offerings. Seasonal beer festivals, brewery taprooms, and social media-driven beverage culture are also accelerating awareness and trial consumption of specialty Weissbier products. This innovation trend is strengthening premium pricing opportunities and expanding consumer engagement within the global wheat beer category.

Weissbier Market Drivers

Rising Global Premiumization of Beer Consumption

The increasing global shift toward premium alcoholic beverages is a major driver supporting Weissbier market expansion. Consumers are increasingly prioritizing product authenticity, artisanal brewing heritage, and differentiated taste experiences over mass-market lagers. Weissbier benefits strongly from its Bavarian brewing tradition, smooth texture, and naturally fruity flavor profile. Urban consumers with rising disposable incomes are increasingly willing to pay premium prices for imported and specialty wheat beer products. This trend is particularly visible across North America, Europe, China, Japan, and India, where premium beer consumption is expanding rapidly within younger demographics and affluent urban populations.

Expansion of Craft Brewery Ecosystems

The rapid expansion of craft breweries globally continues supporting Weissbier production and innovation. Independent breweries across the United States, Germany, Belgium, Australia, and India are increasingly producing localized Hefeweizen, Dunkelweizen, and flavored wheat beer variants. Brewery taprooms, experiential hospitality venues, and microbrewery tourism are contributing significantly to consumer awareness and category growth. Craft breweries are also adopting direct-to-consumer business models and digital marketing strategies to expand customer engagement. The growing popularity of brewery-led experiences and seasonal beer launches continues accelerating premium wheat beer demand globally.

Global Market Restraints

Volatility in Raw Material and Packaging Costs

Weissbier production is highly dependent on wheat malt, barley, hops, and energy-intensive brewing operations. Fluctuations in agricultural commodity prices due to climate variability, geopolitical disruptions, and supply chain instability continue impacting brewery operating margins. Rising glass bottle and aluminum packaging costs are also creating financial pressure for premium beer manufacturers. Smaller craft breweries are particularly vulnerable due to limited procurement scale advantages and lower pricing flexibility compared to multinational brewers.

Stringent Alcohol Regulations and Taxation

Government regulations surrounding alcohol advertising, distribution licensing, labeling requirements, and excise taxation continue restricting market growth in several countries. High alcohol taxes in Europe and parts of Asia raise end-user pricing, affecting affordability for middle-income consumers. Distribution restrictions and regional licensing frameworks in emerging economies also create market entry challenges for imported Weissbier brands. In addition, cultural and religious limitations on alcohol consumption in parts of the Middle East and Asia continue constraining long-term market penetration.

Weissbier Industry Key Opportunities

Growth of Premium Beer Demand in Emerging Markets

Emerging economies across Asia-Pacific and Latin America present substantial opportunities for Weissbier producers. Rising urbanization, expanding middle-class populations, and growing nightlife culture are accelerating premium beer consumption in countries such as China, India, Vietnam, Brazil, and Mexico. Younger consumers increasingly prefer imported and craft-style alcoholic beverages over standard lagers. International brewers are expanding local brewing operations, strategic partnerships, and premium hospitality collaborations to capitalize on this demand transition. Growing beer café culture and experiential dining trends are further strengthening opportunities for premium wheat beer adoption.

Sustainable and Organic Brewing Expansion

Consumer interest in sustainable beverage manufacturing is creating strong opportunities for breweries adopting environmentally responsible operations. Organic wheat sourcing, recyclable packaging, renewable energy utilization, and water-efficient brewing systems are increasingly becoming key brand differentiators. European and North American consumers are particularly supportive of eco-certified brewing operations and sustainable supply chains. Government sustainability incentives and green manufacturing financing programs are also encouraging breweries to modernize production infrastructure. Premium consumers increasingly associate sustainability with higher-quality products, strengthening long-term pricing potential for environmentally focused Weissbier brands.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.54 Billion |

| Market Size in 2026 | USD 12.54 Billion |

| Market Size in 2031 | USD 19.04 Billion |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Hefeweizen remains the dominant product type segment within the Weissbier market, accounting for approximately 38% of global demand in 2025. Its leadership position is supported by strong consumer preference for traditional unfiltered wheat beer with characteristic banana and clove flavor notes. Dunkelweizen and Weizenbock products are also witnessing rising popularity among craft beer enthusiasts seeking richer and more complex flavor profiles. Alcohol-free Weissbier is emerging as the fastest-growing product category due to rising health consciousness and demand for moderate drinking alternatives. Flavored wheat beer variants, including citrus-infused and berry-infused products, are increasingly attracting younger consumers across North America and Asia-Pacific. Premium and craft Weissbier products continue generating stronger profit margins compared to mass-market wheat beer offerings.

Brewing Style Insights

Traditional Bavarian-style Weissbier dominates the global market with nearly 42% share due to strong consumer association with authenticity and heritage brewing standards. German breweries continue leading exports of premium Bavarian wheat beers globally. American wheat beer styles are gaining traction through localized craft brewery innovation and experimentation with fruit-forward flavor profiles. Belgian-inspired wheat beers are also witnessing increasing demand among specialty beer consumers seeking differentiated premium experiences. Barrel-aged and seasonal Weissbier variants are expanding rapidly within limited-edition craft beer portfolios, particularly in the United States and Western Europe. These specialty products are increasingly positioned within high-value premium beverage categories.

Packaging Insights

Glass bottle packaging continues to dominate the Weissbier market, accounting for approximately 47% of global market value in 2025. Premium wheat beer brands strongly favor glass packaging to preserve flavor quality and reinforce traditional Bavarian presentation aesthetics. Returnable bottle systems remain widely utilized across Europe due to strong sustainability regulations and circular economy initiatives. Aluminum cans are witnessing rapid growth across North America and Asia-Pacific because of portability, convenience, and lower transportation costs. Keg and draught packaging formats remain highly important for bars, pubs, brewery taprooms, and hospitality venues. Multipack packaging solutions are also expanding through supermarket and hypermarket retail channels targeting home consumption demand.

Distribution Channel Insights

Supermarkets and hypermarkets represent the leading distribution channel for Weissbier products, accounting for nearly 34% of global sales due to broad product availability and expanding premium beer shelf allocation. Specialty liquor stores and beer-focused retail chains continue playing an important role in premium and imported wheat beer sales. On-trade distribution through bars, pubs, breweries, restaurants, and hotels remains highly significant for premium craft Weissbier consumption. Online alcohol retailing is emerging as one of the fastest-growing channels globally as digital commerce platforms improve product accessibility and direct-to-consumer brewery sales. Subscription-based beer clubs and brewery-operated delivery services are also gaining popularity among premium beer consumers seeking curated craft beer experiences.

Consumer Demographic Insights

Millennials account for the largest consumer demographic within the Weissbier market, representing approximately 36% of global consumption in 2025. This segment strongly favors premium beverages, experiential consumption, and craft brewery culture. Gen Z consumers are increasingly influencing demand for flavored, low-alcohol, and visually differentiated wheat beer products through social media-driven beverage trends. Gen X consumers continue supporting stable demand for traditional imported Weissbier products, particularly in Europe and North America. Health-conscious consumers are increasingly adopting alcohol-free and organic wheat beer variants, while craft beer enthusiasts continue driving demand for limited-edition and specialty brewing styles.

Explore more data points, trends and opportunities Download Free Sample Report

Weissbier Market Segmentations

By Product Type

- Hefeweizen

- Kristallweizen

- Dunkelweizen

- Weizenbock

- Berliner Weisse

- Alcohol-Free Weissbier

- Flavored Weissbier

- Organic Weissbier

- Craft Weissbier

- Premium Weissbier

By Brewing Style

- Traditional Bavarian Style

- Belgian-Inspired Wheat Beer

- American Wheat Beer

- Hybrid Wheat Ale

- Barrel-Aged Weissbier

- Seasonal / Limited Edition Weissbier

By Alcohol Content

- Low Alcohol

- Standard Alcohol

- Premium Strength

- Strong Wheat Beer

By Packaging Type

- Glass Bottles

- Aluminum Cans

- PET Bottles

- Kegs

- Draught Packaging

- Multipack Formats

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Liquor Stores

- Specialty Beer Stores

- Bars & Pubs

- Restaurants & Hotels

- Online Retail & E-commerce

- Direct-to-Consumer Brewery Sales

Regional Insights

Europe

Europe dominates the global Weissbier market with approximately 46% market share in 2025. Germany remains the largest producer and consumer globally, contributing nearly 24% of worldwide demand due to its deeply rooted wheat beer brewing heritage and strong export capabilities. Bavaria continues serving as the global production center for premium Weissbier brands. The United Kingdom, Belgium, France, Italy, and the Netherlands are also experiencing growing demand for premium and craft wheat beer products. Rising tourism, beer festivals, and premium hospitality demand continue supporting market expansion across Europe.

North America

North America accounts for nearly 27% of the global Weissbier market, led primarily by the United States. The expansion of craft brewery ecosystems across the U.S. has significantly increased localized Hefeweizen and flavored wheat beer production. Consumers increasingly prefer seasonal and premium beer offerings over traditional mass-market lagers. Canada is also witnessing rising demand for imported European wheat beers and craft-inspired domestic products. Brewery taprooms, experiential hospitality venues, and digital alcohol retailing continue supporting premium beer adoption throughout the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to register CAGR exceeding 10% during the forecast period. China leads regional growth through rising middle-class disposable incomes and increasing premium beer consumption. Japan remains a mature market with strong demand for low-alcohol and premium wheat beer products. India is rapidly emerging as an important growth market due to urbanization, expanding nightlife culture, and rising craft brewery penetration across metropolitan cities. South Korea, Vietnam, and Thailand are also witnessing rising adoption of imported and specialty wheat beer categories driven by younger consumers and hospitality sector expansion.

Latin America

Latin America is experiencing steady growth in Weissbier demand, particularly in Brazil and Mexico. Brazil’s premium beer market expansion and strong social drinking culture are supporting imports and localized wheat beer production. Mexican consumers are increasingly exploring craft and imported beer categories through premium bars and tourism-oriented hospitality venues. Fruit-infused and tropical-flavored wheat beer variants are particularly gaining popularity within regional craft brewery ecosystems.

Middle East & Africa

The Middle East & Africa region currently represents a smaller share of the global Weissbier market but offers strong long-term premiumization opportunities. The UAE and South Africa are leading regional demand due to tourism, expatriate populations, and luxury hospitality sector expansion. Premium hotels, sports venues, and international restaurants are driving specialty beer consumption across key urban centers. South Africa’s growing craft brewery industry is also supporting regional premium wheat beer awareness and consumption growth.

Key Players in the Weissbier Market

- Paulaner Brauerei Gruppe

- Erdinger Weissbräu

- Weihenstephan Brewery

- Anheuser-Busch InBev

- Carlsberg Group

- Heineken N.V.

- Molson Coors Beverage Company

- Asahi Group Holdings

- Ayinger Privatbrauerei

- Sierra Nevada Brewing Co.