Sparkling Water Market Size

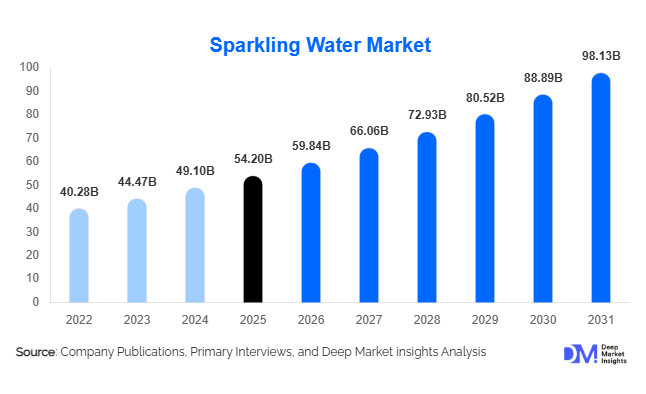

According to Deep Market Insights, the global sparkling water market size was valued at USD 54.2 billion in 2025 and is projected to grow from USD 59.84 billion in 2026 to reach USD 98.13 billion by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The sparkling water market growth is primarily driven by increasing consumer preference for healthier beverage alternatives, rising awareness regarding sugar reduction, and the rapid expansion of premium and functional hydration products across both developed and emerging economies.

Key Market Insights

- Consumers are rapidly shifting away from sugary carbonated beverages, accelerating global demand for zero-calorie and low-sugar sparkling water products.

- Functional sparkling water categories are expanding significantly, including vitamin-infused, electrolyte-enhanced, probiotic, and adaptogenic beverages targeting wellness-focused consumers.

- North America dominates the global sparkling water market, supported by strong health-conscious beverage consumption and premium retail penetration.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, rising disposable incomes, and increasing adoption of Western beverage consumption patterns.

- Sustainable packaging innovations are reshaping industry competition, with aluminum cans and recycled PET packaging gaining significant traction.

- Digital commerce and direct-to-consumer subscription models are transforming distribution strategies and improving customer engagement globally.

Sparkling Water Market Latest Trends

Functional and Wellness-Oriented Sparkling Water Expansion

The sparkling water industry is increasingly moving toward functional hydration solutions that offer benefits beyond traditional refreshment. Manufacturers are launching products enriched with vitamins, minerals, probiotics, adaptogens, collagen, electrolytes, and natural caffeine to target health-conscious consumers seeking wellness-driven beverages. Functional sparkling water is gaining strong traction among millennials, fitness-focused consumers, and urban professionals who prefer beverages supporting immunity, digestive health, energy, and mental wellness. Beverage companies are also introducing botanical flavor combinations and clean-label formulations that appeal to consumers seeking minimally processed ingredients. This trend is helping manufacturers achieve higher profit margins while strengthening brand differentiation in an increasingly competitive market.

Sustainable Packaging and Premiumization Trends

Sustainability has become a defining trend within the global sparkling water market. Beverage companies are increasingly adopting recyclable aluminum cans, lightweight bottles, recycled PET (rPET), and biodegradable packaging solutions to reduce environmental impact and comply with tightening regulations on single-use plastics. Consumers are actively favoring brands associated with environmentally responsible packaging and carbon-neutral manufacturing practices. Simultaneously, premiumization is reshaping product positioning across developed markets. Premium sparkling mineral water in glass bottles, imported European brands, and luxury hydration products are witnessing rising demand within hospitality, foodservice, and upscale retail channels. Limited-edition flavors, artisanal sourcing, and sophisticated branding strategies are further elevating sparkling water as a premium lifestyle beverage category.

Sparkling Water Market Drivers

Rising Health and Wellness Awareness

Growing awareness regarding obesity, diabetes, and excessive sugar consumption is one of the primary growth drivers for the sparkling water market. Consumers are increasingly reducing intake of traditional carbonated soft drinks and replacing them with healthier hydration alternatives. Government sugar taxes, nutritional labeling regulations, and public health campaigns across North America and Europe are accelerating this shift toward zero-sugar beverages. Sparkling water products are benefiting strongly because they provide carbonation and flavor experiences without the high calorie content associated with conventional sodas. The global wellness movement, combined with preventive healthcare trends, continues to support strong long-term demand growth for sparkling water products.

Rapid Product Innovation and Flavor Diversification

Continuous innovation in flavors and functional ingredients is significantly expanding the consumer base for sparkling water globally. Beverage manufacturers are introducing exotic fruit flavors, herbal infusions, seasonal product launches, and wellness-focused beverages to maintain consumer engagement and encourage repeat purchases. Younger consumers increasingly prefer novelty-driven beverage experiences, prompting companies to invest heavily in research and development. Functional sparkling water products containing probiotics, electrolytes, natural caffeine, and vitamins are becoming particularly popular within fitness and lifestyle-oriented demographics. This innovation-driven environment is enabling companies to access premium price points while expanding category penetration into new consumer segments.

Sparkling Water Market Restraints

Pricing Sensitivity in Emerging Economies

Sparkling water products often carry significantly higher retail prices compared to conventional bottled water and carbonated soft drinks, particularly in emerging economies. Premium imported mineral sparkling water products face additional transportation and packaging costs, limiting affordability among middle-income consumers. In several developing regions, consumers continue prioritizing affordability over premium wellness beverages, which restricts large-scale penetration. Economic fluctuations and inflationary pressures may further challenge market expansion in price-sensitive markets where premium beverage categories remain relatively nascent.

Environmental Concerns and Packaging Regulations

The bottled beverage industry faces growing criticism regarding plastic waste generation and environmental sustainability. Governments across Europe, North America, and parts of Asia are implementing stricter regulations on single-use plastics, recycling targets, and extended producer responsibility obligations. Sparkling water manufacturers must invest heavily in sustainable packaging transitions, recycling infrastructure, and low-carbon operations to remain compliant and maintain consumer trust. Rising raw material costs for aluminum, PET resin, and logistics also place pressure on operating margins across the industry.

Sparkling Water Industry Key Opportunities

Alcohol Alternative Beverage Positioning

One of the strongest opportunities within the sparkling water market is the growing consumer movement toward alcohol moderation and mindful drinking. Younger consumers increasingly seek sophisticated non-alcoholic beverages that provide social drinking experiences without alcohol content. Premium sparkling water products with botanical flavors, cocktail-inspired formulations, and elegant glass packaging are being positioned as substitutes for alcoholic beverages in restaurants, bars, lounges, and social events. This trend is creating substantial opportunities for sparkling water brands to expand into hospitality and nightlife consumption channels while attracting wellness-oriented consumers seeking healthier lifestyle choices.

Expansion Across Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East represent major untapped growth opportunities for sparkling water manufacturers. Rising urbanization, expanding middle-class populations, growing modern retail infrastructure, and increasing health awareness are accelerating demand for healthier packaged beverages in countries such as China, India, Indonesia, Brazil, Saudi Arabia, and the UAE. Beverage companies are localizing flavor profiles, packaging formats, and pricing strategies to improve accessibility in these high-growth markets. Rapid expansion of café culture, premium hospitality, and digital grocery delivery platforms is further supporting sparkling water adoption across emerging regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 54.20 Billion |

| Market Size in 2026 | USD 59.84 Billion |

| Market Size in 2031 | USD 98.13 Billion |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Natural sparkling mineral water remains the dominant product category globally, accounting for approximately 42% of total market revenue in 2025. Consumers continue to associate naturally sourced mineral sparkling water with premium quality, purity, and wellness benefits. Flavored sparkling water is rapidly expanding due to increasing demand among younger consumers seeking taste variety and sugar-free refreshment alternatives. Functional sparkling water products enriched with vitamins, electrolytes, and probiotics represent one of the fastest-growing product segments, particularly within North America and Asia-Pacific. Premium imported sparkling water brands continue to maintain strong growth in luxury hospitality and fine dining establishments, while private-label sparkling water is expanding steadily across supermarkets and discount retail chains.

Application Insights

Daily hydration applications account for the largest share of sparkling water consumption globally, representing nearly 46% of market demand in 2025. Consumers increasingly incorporate sparkling water into everyday beverage routines as a healthier substitute for soft drinks. Fitness and sports hydration applications are expanding rapidly due to demand for electrolyte-enhanced and wellness-focused sparkling beverages among active consumers. Cocktail and mixology applications are also witnessing strong growth as sparkling water becomes a key ingredient in premium non-alcoholic beverages and low-calorie cocktails. Workplace consumption is increasing steadily as employers introduce healthier beverage options within corporate wellness programs. Hospitality applications, including restaurants, airlines, hotels, and entertainment venues, are further driving premium sparkling water demand worldwide.

Distribution Channel Insights

Hypermarkets and supermarkets dominate sparkling water distribution globally, accounting for approximately 34% of market sales in 2025. Large retail formats provide strong shelf visibility, promotional pricing opportunities, and convenient access to mass-market consumers. Convenience stores continue to play a major role in impulse purchases and on-the-go beverage consumption. Online retail and direct-to-consumer channels are among the fastest-growing distribution segments due to increasing adoption of digital grocery platforms and subscription-based beverage purchasing models. Beverage companies are investing heavily in e-commerce partnerships, personalized digital marketing, and recurring delivery services to strengthen customer retention. Foodservice distribution channels, including restaurants, cafés, and hotels, remain particularly important for premium sparkling water brands targeting affluent consumers.

Consumer Demographic Insights

Millennials represent the largest consumer demographic within the sparkling water market, accounting for nearly 37% of global demand in 2025. This segment demonstrates strong preference for wellness-oriented beverages, sustainable packaging, and innovative flavor experiences. Generation Z consumers are emerging as the fastest-growing demographic due to strong alignment with functional beverages, clean-label products, and lifestyle-focused branding. Health-conscious adults and fitness-oriented consumers continue driving demand for electrolyte-based and vitamin-infused sparkling water products. Premium urban consumers are contributing significantly to luxury sparkling water growth through demand for imported mineral water brands and premium hospitality experiences. Family consumers are also increasingly purchasing multipack sparkling water products for healthier household hydration consumption.

Packaging Type Insights

PET bottles remain the leading packaging format globally, accounting for approximately 48% of market revenue in 2025 due to affordability, portability, and widespread retail adoption. Small-format PET bottles dominate convenience retail and impulse consumption channels, while larger family-size formats continue to perform strongly in supermarkets and warehouse retail. Aluminum cans are gaining market share rapidly due to sustainability advantages, superior recyclability, and premium branding opportunities. Glass bottles continue to dominate the luxury and hospitality segments, particularly among imported European sparkling mineral water brands positioned within fine dining and premium hotel channels. Sustainable packaging solutions, including recycled PET and biodegradable materials, are increasingly becoming critical competitive differentiators across the market.

Explore more data points, trends and opportunities Download Free Sample Report

Sparkling Water Market Segmentations

By Product Type

- Natural Sparkling Mineral Water

- Flavored Sparkling Water

- Functional Sparkling Water

- Caffeinated Sparkling Water

- Unsweetened Sparkling Water

- Sweetened Sparkling Water

- Sparkling Water Mixers

- Private Label Sparkling Water

- Premium Luxury Sparkling Water

By Packaging Type

- PET Bottles

- Aluminum Cans

- Glass Bottles

- Sustainable Packaging

- Multipack Packaging

- On-the-Go Packaging

By Flavor Profile

- Plain/Unflavored

- Fruit Flavors

- Herbal & Botanical Flavors

- Functional Flavor Blends

- Seasonal & Limited-Edition Flavors

By Distribution Channel

- Hypermarkets & Supermarkets

- Convenience Stores

- Online Retail/E-commerce

- Specialty Stores

- Foodservice & HoReCa

- Vending Machines

- Direct-to-Consumer Channels

- Club Stores & Warehouse Retail

By Consumer Demographics

- Millennials

- Generation Z

- Health-Conscious Adults

- Fitness & Lifestyle Consumers

- Premium Urban Consumers

- Family Consumers

Regional Insights

North America

North America accounted for approximately 36% of the global sparkling water market in 2025, making it the largest regional market worldwide. The United States dominates regional demand due to strong consumer awareness regarding sugar reduction, premium beverage consumption, and wellness-oriented lifestyles. Flavored and functional sparkling water categories are particularly popular across the U.S. market, supported by aggressive product innovation and retail expansion by major beverage companies. Canada is also witnessing strong growth due to rising health-conscious consumption patterns and increasing premium beverage penetration. Sustainability-focused packaging adoption and strong e-commerce beverage sales continue supporting regional market expansion.

Europe

Europe represented nearly 30% of global market share in 2025 and remains one of the most mature sparkling water markets globally. Germany continues to maintain one of the highest per-capita sparkling water consumption rates worldwide due to longstanding cultural preference for carbonated mineral water. France and Italy remain major exporters of premium sparkling mineral water brands, while the United Kingdom is witnessing rapid growth in flavored and functional sparkling beverages. Sustainability regulations, strong clean-label demand, and premium hospitality consumption continue driving innovation across the European market.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market through 2031, with CAGR expected to exceed 12%. China is witnessing rapid adoption of sparkling water products among urban millennials seeking healthier beverage alternatives and premium lifestyle products. Japan demonstrates strong demand for functional sparkling beverages and convenience-oriented packaging formats. India is emerging as a high-potential market due to urbanization, expanding middle-class incomes, rising health awareness, and rapid modern retail expansion. Australia and South Korea continue to exhibit strong premium beverage demand supported by wellness trends and evolving consumer preferences.

Latin America

Latin America accounted for nearly 8% of global sparkling water demand in 2025. Brazil remains the dominant regional market due to growing middle-class consumption and increasing preference for flavored sparkling beverages. Mexico and Chile are also witnessing rising sparkling water penetration as consumers gradually reduce sugary soft drink intake. International beverage companies are increasingly expanding local production and distribution capabilities across Latin America to improve market accessibility and reduce import dependency.

Middle East & Africa

The Middle East and Africa region is emerging as a promising market for premium sparkling water products. GCC countries, particularly the UAE and Saudi Arabia, are experiencing rising demand for imported luxury sparkling mineral water through upscale hospitality and retail channels. High-income consumers within the Middle East increasingly prefer premium hydration products associated with wellness and luxury lifestyles. South Africa remains the leading African market due to expanding organized retail and growing consumer awareness regarding healthier beverage alternatives. Tourism and hospitality growth across the region continue supporting premium sparkling water demand.

Key Players in the Sparkling Water Market

- Nestlé S.A.

- PepsiCo Inc.

- The Coca-Cola Company

- Danone S.A.

- Keurig Dr Pepper Inc.

- National Beverage Corp.

- Sanpellegrino S.p.A.

- Talking Rain Beverage Company

- Gerolsteiner Brunnen GmbH & Co. KG

- Ferrarelle Società Benefit S.p.A.

- Spindrift Beverage Co.

- Polar Beverages

- RHODIUS Mineralquellen und Getränke GmbH & Co. KG

- VOSS Water

- Nongfu Spring Co., Ltd.