Vertical Hydroponic Lettuce Market Size

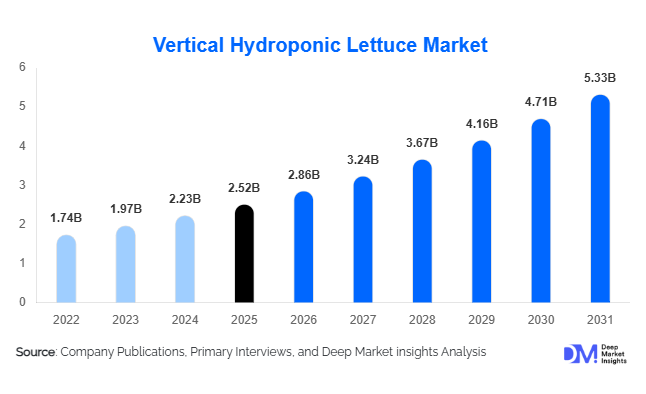

According to Deep Market Insights, the global vertical hydroponic lettuce market size was valued at USD 2.52 billion in 2025 and is projected to grow from USD 2.86 billion in 2026 to reach USD 5.33 billion by 2031, expanding at a CAGR of 13.3% during the forecast period (2026–2031). The market growth is primarily driven by increasing adoption of controlled environment agriculture (CEA), rising consumer demand for pesticide-free leafy greens, growing concerns regarding food security, and advancements in LED lighting, automation, and hydroponic cultivation technologies. Vertical hydroponic lettuce has emerged as one of the most commercially viable crops within vertical farming systems due to its short growth cycle, high productivity, and suitability for year-round indoor cultivation.

Key Market Insights

- Vertical hydroponic lettuce production is becoming a cornerstone of urban agriculture, enabling year-round cultivation close to consumption centers while reducing transportation costs and food waste.

- LED lighting and AI-enabled environmental controls are significantly improving farm economics, allowing commercial operators to increase yields while lowering resource consumption.

- North America dominates the global market, supported by large-scale commercial vertical farms, strong retailer partnerships, and growing demand for locally sourced produce.

- Asia-Pacific is the fastest-growing regional market, driven by food security initiatives, urban population growth, and government investments in smart agriculture.

- Retail grocery chains represent the largest demand channel, with supermarkets increasingly sourcing hydroponic lettuce to ensure freshness, traceability, and year-round availability.

- Automation, robotics, and renewable energy integration are emerging as key competitive differentiators for commercial producers worldwide.

Vertical Hydroponic Lettuce Market Drivers

Growing Demand for Sustainable Agriculture

Water scarcity, climate variability, and pressure on arable land are driving the adoption of resource-efficient agricultural systems. Vertical hydroponic lettuce production uses up to 95% less water than conventional farming while delivering significantly higher yields per square meter. Governments and food retailers are increasingly incorporating sustainability targets into procurement strategies, creating favorable conditions for market expansion. The ability to produce lettuce throughout the year without seasonal limitations further enhances the attractiveness of hydroponic systems.

Rising Consumer Preference for Fresh and Pesticide-Free Produce

Consumers are increasingly prioritizing food safety, freshness, and transparency in food sourcing. Hydroponically grown lettuce offers pesticide-free production, consistent quality, and superior shelf life compared to conventionally grown alternatives. As awareness of food safety and environmental sustainability grows, retailers and foodservice operators are expanding their procurement of locally produced hydroponic lettuce. This trend is particularly evident in developed markets where consumers are willing to pay premium prices for fresh and sustainably produced vegetables.

Advancements in Controlled Environment Agriculture Technologies

Technological innovation continues to improve the economics of vertical farming. Energy-efficient LED lighting systems, advanced climate-control platforms, nutrient management software, and automation technologies are reducing operating costs while increasing yields. The integration of renewable energy systems and smart farm management platforms is further enhancing production efficiency. These developments are enabling commercial operators to scale production and compete more effectively with traditional agriculture.

Vertical Hydroponic Lettuce Market Restraints

High Capital Investment Requirements

Establishing a commercial vertical hydroponic lettuce farm requires substantial upfront investment in infrastructure, lighting systems, automation equipment, climate-control technologies, and water management systems. Large-scale facilities often require multi-million-dollar capital commitments, creating barriers for new entrants and extending investment payback periods. Access to financing remains a critical challenge for many operators, particularly in emerging markets.

Energy Cost Volatility

Electricity represents one of the largest operational expenses in vertical hydroponic farming. Fluctuations in energy prices can significantly affect profitability, particularly in regions with high electricity costs. Although LED efficiency continues to improve, energy-intensive lighting and climate-control systems remain essential for production. Managing energy consumption and integrating renewable power sources are becoming increasingly important strategic priorities for market participants.

Vertical Hydroponic Lettuce Industry Key Opportunities

Government-Supported Food Security Programs

Food security concerns are creating substantial growth opportunities for vertical hydroponic lettuce producers. Countries with limited arable land and high dependence on food imports are actively supporting controlled environment agriculture through grants, tax incentives, and infrastructure investments. Programs in Singapore, the UAE, Saudi Arabia, Japan, and South Korea are encouraging the deployment of vertical farming facilities to enhance domestic food production. Companies that align with national food resilience objectives are well positioned to benefit from long-term policy support and investment incentives.

Expansion of Ready-to-Eat and Fresh-Cut Salad Markets

The growing popularity of packaged salads, convenience foods, and healthy eating habits is creating strong demand for premium-quality lettuce. Food processors, meal-kit providers, and quick-service restaurant chains require reliable access to fresh leafy greens with consistent quality standards. Vertical hydroponic lettuce producers can capitalize on this demand through long-term supply agreements and premium product offerings. As global consumption of fresh-cut salads continues to rise, commercial growers are expected to benefit from expanding downstream demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.52 Billion |

| Market Size in 2026 | USD 2.86 Billion |

| Market Size in 2031 | USD 5.33 Billion |

| CAGR | 13.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Variety Insights

Butterhead lettuce continues to dominate the global vertical hydroponic lettuce market, accounting for approximately 31% of total revenue in 2025. Its leadership is primarily driven by strong consumer preference for its soft texture, mild flavor profile, and premium positioning in fresh salad mixes and gourmet retail offerings. Retailers and foodservice operators consistently favor butterhead varieties due to their strong visual appeal, uniform growth patterns in controlled environments, and high acceptance in ready-to-eat formats, which collectively strengthen its commercial scalability within indoor farming systems.Romaine lettuce remains the second most significant variety, supported by sustained demand from quick-service restaurant chains and packaged salad manufacturers that prioritize structural integrity and extended shelf life. Loose leaf varieties are expanding rapidly, driven by their shorter cultivation cycles, faster harvest turnover, and suitability for continuous harvesting models, making them highly attractive for high-efficiency vertical farming operations. Specialty lettuce varieties such as oak leaf, Batavia, and Lollo Rosso are increasingly positioned in premium retail segments where differentiation, color variety, and gourmet presentation enhance consumer value perception. Additionally, mixed baby leaf products are witnessing strong momentum as urban consumers increasingly prioritize convenience, nutritional diversity, and portion-controlled fresh produce solutions.

Hydroponic System Insights

Nutrient Film Technique (NFT) systems remain the leading hydroponic method, contributing approximately 38% of total industry revenue in 2025. Their dominance is largely driven by high water-use efficiency, low nutrient wastage, and strong compatibility with scalable vertical rack structures, which collectively enable consistent production cycles in controlled environments. NFT systems are particularly favored in commercial facilities where operational predictability, low maintenance requirements, and rapid crop turnover are essential for profitability.Deep Water Culture (DWC) systems continue to maintain strong adoption due to their ability to provide stable root-zone oxygenation and consistent nutrient availability, which supports high biomass yields and crop uniformity. Drip hydroponic systems are gaining traction among mid-scale growers because of their precision nutrient delivery, adaptability across different crop varieties, and ease of system customization for hybrid farming models. Emerging aeroponic-hydroponic hybrid systems are being driven by innovation-focused growers seeking maximum yield efficiency with minimal water and nutrient input, making them increasingly relevant in advanced research facilities and high-tech urban farms.

Infrastructure Type Insights

Warehouse-based vertical farms represent the dominant infrastructure category, accounting for approximately 42% of global market value. Their leadership is driven by the ability to fully control environmental conditions such as temperature, humidity, and light intensity, enabling uninterrupted year-round production regardless of external climate variability. The scalability of warehouse structures also supports industrial-level output, making them highly attractive for institutional investors and large retail supply contracts.Building-integrated farms are expanding steadily, primarily driven by urbanization trends, limited availability of arable land, and increasing demand for locally produced food within city centers. Greenhouse-vertical hybrid systems are gaining momentum as they combine natural sunlight utilization with controlled environment agriculture, reducing energy dependency while maintaining yield consistency. Shipping container farms are emerging as a flexible and modular solution, driven by decentralized food production needs, military and remote-site applications, and small-scale commercial farming initiatives targeting hyperlocal distribution networks.

Distribution Channel Insights

Direct-to-retail channels dominate the market, accounting for approximately 36% of global demand, with growth driven by increasing retailer focus on supply chain transparency, product freshness, and traceability. Supermarkets and grocery chains are strengthening partnerships with vertical farming operators to ensure consistent year-round supply of pesticide-free leafy greens, which significantly enhances category penetration in modern retail formats.Foodservice distribution is emerging as a high-growth channel, driven by rising demand from restaurant chains, hotels, and institutional caterers seeking reliable, locally sourced produce that supports menu consistency and sustainability commitments. Direct-to-consumer channels, including subscription-based delivery models and e-grocery platforms, are expanding rapidly in urban regions due to increasing consumer preference for farm-to-home freshness and digital purchasing convenience. Wholesale markets continue to play a supporting role in developing regions where controlled environment agriculture penetration is still in early stages, serving as a transitional distribution layer between traditional and modern supply systems.

End-Use Insights

Retail consumption remains the largest end-use segment, accounting for approximately 44% of total market demand in 2025. This dominance is driven by rising consumer awareness of healthy eating habits, increasing preference for pesticide-free produce, and growing demand for consistent year-round availability of fresh leafy greens in supermarkets and grocery stores.Foodservice and hospitality represent one of the fastest-growing end-use categories, driven by restaurant chains and hospitality operators increasingly prioritizing locally sourced, high-quality produce to enhance menu differentiation and sustainability positioning. Food processing companies are expanding procurement of hydroponically grown lettuce for packaged salads and ready-to-eat meals, driven by demand for extended shelf life and consistent product quality. Institutional catering, including hospitals, corporate cafeterias, and educational institutions, is also increasing adoption as part of broader sustainability initiatives and efforts to improve nutritional standards in large-scale meal provisioning.

Farm Scale Insights

Large-scale commercial farms dominate the market with nearly 48% of global revenue, driven by economies of scale, high automation adoption, and integration of advanced climate control and monitoring technologies. These facilities are primarily supported by long-term retail contracts and institutional supply agreements, which ensure stable revenue streams and operational efficiency.Medium-scale farms are growing steadily as they focus on regional supply networks and hybrid distribution strategies targeting supermarkets and foodservice operators. Their growth is supported by modular system investments and increasing access to mid-level automation technologies. Small-scale farms continue to play a crucial role in urban agriculture ecosystems, community-supported agriculture programs, and hyperlocal distribution models, with growth driven by government initiatives promoting food security and localized production systems in densely populated urban regions.

Explore more data points, trends and opportunities Download Free Sample Report

Vertical Hydroponic Lettuce Market Segmentations

By Lettuce Variety

- Butterhead Lettuce

- Romaine Lettuce

- Loose Leaf Lettuce

- Crisphead Lettuce

- Specialty Lettuce

By Hydroponic Cultivation System

- Nutrient Film Technique (NFT)

- Deep Water Culture (DWC)

- Drip Hydroponic Systems

- Ebb & Flow Systems

- Wick Systems

- Aeroponic-Hydroponic Hybrid Systems

By Vertical Farm Infrastructure Type

- Warehouse-Based Vertical Farms

- Shipping Container Vertical Farms

- Building-Integrated Vertical Farms

- Greenhouse-Vertical Hybrid Farms

- Modular Indoor Farm Systems

By Automation Level

- Manual Operations

- Semi-Automated Farms

- Fully Automated Farms

By Lighting Technology

- LED Grow Lighting

- Fluorescent Lighting

- High Intensity Discharge (HID) Lighting

- Hybrid Lighting Systems

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 38% of global vertical hydroponic lettuce demand in 2025. Growth in this region is primarily driven by strong investment in controlled environment agriculture infrastructure, widespread adoption of advanced automation technologies, and robust participation from large retail chains integrating locally grown produce into mainstream supply networks. The United States leads regional expansion due to significant venture capital funding in vertical farming startups, increasing consumer preference for pesticide-free produce, and strong demand from foodservice operators. Canada’s growth is supported by urban agriculture initiatives, government-backed sustainability programs, and rising demand for locally sourced fresh produce in major metropolitan areas.

Europe

Europe accounts for approximately 27% of global market revenue, with growth driven by strong regulatory emphasis on sustainability, carbon reduction targets, and food security resilience strategies. The Netherlands acts as a leading innovation hub, supported by advanced greenhouse technologies and research-driven agricultural practices. Germany, the United Kingdom, France, and Nordic countries are increasingly adopting hydroponic systems due to rising energy efficiency investments, consumer demand for environmentally responsible food production, and policy support for urban farming solutions. The region’s growth is further reinforced by strong retail demand for traceable and low-carbon food supply chains.

Asia-Pacific

Asia-Pacific represents approximately 22% of global demand and is the fastest-growing regional market, driven by rapid urbanization, rising middle-class consumption, and strong government investment in smart agriculture infrastructure. China leads regional growth through large-scale deployment of indoor farming systems and integration of artificial intelligence in agricultural production. Japan’s leadership in automated plant factories and precision agriculture technologies continues to accelerate productivity improvements. Singapore’s aggressive food security strategy is a major growth driver, supported by limited arable land and high import dependency, while South Korea is investing heavily in agri-tech innovation. Australia’s growth is primarily driven by climate variability challenges and increasing demand for resilient food production systems.

Latin America

Latin America accounts for approximately 6% of global revenue, with growth driven by increasing urban population density, rising consumer demand for premium fresh produce, and gradual modernization of agricultural supply chains. Brazil, Mexico, and Chile are emerging as key adoption markets where investments in controlled environment agriculture are gradually increasing. Growth is supported by improving access to agricultural technology, rising interest from private investors, and increasing awareness of water-efficient farming practices in regions facing climatic variability.

Middle East & Africa

The Middle East & Africa region represents approximately 7% of global demand, with growth strongly driven by acute water scarcity challenges, high dependence on food imports, and government-led food security initiatives. The UAE and Saudi Arabia are leading adopters due to large-scale investments in vertical farming infrastructure aimed at reducing import dependency and improving domestic food resilience. Africa’s growth, particularly in South Africa, is supported by increasing adoption of sustainable agriculture technologies, urban population growth, and rising interest in climate-resilient farming solutions that reduce reliance on traditional water-intensive agriculture systems.

Key Players in the Vertical Hydroponic Lettuce Market

- AeroFarms

- Plenty Unlimited

- Bowery Farming

- Gotham Greens

- GoodLeaf Farms

- Kalera

- Jones Food Company

- Spread Co.

- Mirai Co.

- Sky Greens

- iFarm

- Vertical Farm Systems

- Crop One Holdings

- Green Sense Farms

- Elevate Farms