Agricultural Waste Market Size

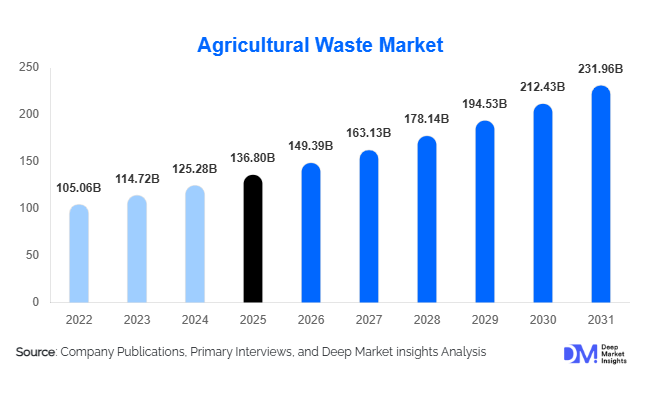

According to Deep Market Insights, the global agricultural waste market size was valued at USD 136.8 billion in 2025 and is projected to grow from USD 149.39 billion in 2026 to reach USD 231.96 billion by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The agricultural waste market growth is primarily driven by the increasing adoption of circular economy practices, rising investments in biomass-based renewable energy, and growing demand for sustainable agricultural and industrial raw materials derived from crop residues, livestock waste, and agro-industrial by-products.

Key Market Insights

- Agricultural waste is increasingly being utilized for renewable energy generation, particularly in biomass power plants, compressed biogas facilities, and second-generation biofuel production.

- Governments worldwide are implementing strict regulations on crop residue burning, accelerating investments in organized waste collection and processing infrastructure.

- Asia-Pacific dominates the global agricultural waste market, supported by extensive crop cultivation, rising biomass availability, and expanding renewable energy programs in China and India.

- Europe remains the technology leader, driven by advanced anaerobic digestion systems, circular economy policies, and strong adoption of organic waste recycling.

- Biochar, bioplastics, and bio-based chemicals are emerging as high-growth application areas, creating new commercial opportunities for agricultural waste valorization.

- Technology integration, including AI-enabled biomass logistics, automated waste segregation, and advanced pyrolysis systems, is improving operational efficiency across the value chain.

What are the latest trends in the agricultural waste market?

Expansion of Waste-to-Energy Infrastructure

One of the most prominent trends in the agricultural waste market is the rapid expansion of waste-to-energy infrastructure globally. Governments and private companies are increasingly investing in biomass power generation, compressed biogas plants, and ethanol production facilities utilizing agricultural residues such as rice straw, corn stover, wheat straw, and sugarcane bagasse. This trend is particularly strong in countries such as India, China, Brazil, Germany, and the United States, where renewable energy targets and decarbonization initiatives are driving long-term investments. Biomass pellets and renewable natural gas are gaining commercial traction as industries seek low-carbon fuel alternatives. Utilities and industrial manufacturers are increasingly integrating biomass co-firing technologies to reduce dependence on coal and fossil fuels.

Rise of Circular Bioeconomy and Bio-Based Products

The agricultural waste market is witnessing growing demand for bio-based industrial products including bioplastics, biochemicals, biochar, and sustainable packaging materials. Agricultural residues are increasingly being processed into renewable feedstocks for the chemicals, construction, packaging, and consumer goods industries. Companies are focusing on converting lignin, cellulose, and starch-rich agricultural waste into high-value industrial products with lower environmental impact. Circular bioeconomy initiatives across Europe and North America are further encouraging industrial adoption. In addition, carbon credit programs and sustainability-linked financing are supporting investments in agricultural waste valorization projects, making agricultural waste a strategic raw material in low-carbon industrial supply chains.

What are the key drivers in the agricultural waste market?

Increasing Renewable Energy Demand

The growing global demand for renewable energy is one of the primary drivers of the agricultural waste market. Agricultural residues are increasingly used for biomass electricity generation, biogas production, bioethanol manufacturing, and renewable natural gas applications. Governments across major economies are offering subsidies, feed-in tariffs, tax incentives, and renewable fuel mandates to encourage biomass utilization. Rising volatility in fossil fuel prices and increasing pressure to achieve carbon neutrality targets are accelerating investments in biomass energy infrastructure. Countries such as China, India, Germany, and the United States are significantly expanding agricultural waste-based energy projects to strengthen energy security while reducing greenhouse gas emissions.

Growing Focus on Sustainable Waste Management

Environmental concerns associated with open-field burning and landfill disposal of agricultural waste are driving the adoption of organized waste management solutions. Governments are implementing stricter emission regulations and promoting sustainable residue management practices to combat air pollution and soil degradation. Agricultural waste is increasingly being converted into compost, organic fertilizers, and soil conditioners that improve soil fertility and reduce chemical fertilizer dependency. The rise of organic farming and regenerative agriculture practices is further boosting demand for recycled agricultural waste products. Public awareness regarding sustainable farming practices and climate-resilient agriculture is also contributing to long-term market growth.

What are the restraints for the global market?

Fragmented Collection and Supply Chain Challenges

A major restraint in the agricultural waste market is the fragmented nature of biomass collection systems. Agricultural residues are geographically dispersed and highly seasonal, making transportation and feedstock aggregation operationally challenging. Small-scale farming structures in developing economies further increase collection inefficiencies and logistics costs. Inconsistent supply chains can disrupt biomass processing operations and reduce plant utilization rates, particularly for large-scale waste-to-energy facilities and industrial biorefineries.

High Capital Investment Requirements

Advanced agricultural waste processing technologies such as anaerobic digestion, pyrolysis, gasification, and biorefining require substantial capital investments in machinery, storage systems, and transportation infrastructure. Limited financing access and inconsistent policy implementation in certain developing economies continue to slow market penetration. In addition, fluctuations in feedstock availability and biomass pricing can impact project profitability, creating investment uncertainty for market participants.

What are the key opportunities in the agricultural waste industry?

Carbon Credit and Biochar Commercialization

The expansion of carbon trading mechanisms and carbon sequestration initiatives is creating substantial opportunities for agricultural waste processors. Biochar production is emerging as a particularly attractive segment because of its ability to improve soil health while capturing carbon for long-term storage. Governments and environmental organizations are increasingly supporting biochar adoption through climate financing programs and carbon offset incentives. Companies investing in carbon-negative agricultural waste processing technologies are expected to benefit from additional revenue streams linked to sustainability and emission reduction targets.

Development of Bio-Based Industrial Materials

Agricultural waste is increasingly being utilized for manufacturing sustainable industrial materials including biodegradable plastics, packaging materials, pulp substitutes, insulation products, and specialty chemicals. Rising restrictions on petroleum-based plastics and growing ESG commitments among manufacturers are accelerating demand for renewable feedstocks derived from agricultural residues. This transition toward bio-based industrial production presents significant opportunities for both existing biomass processors and new entrants focused on sustainable material innovation. Emerging applications in low-carbon construction materials and green chemicals are expected to further diversify revenue streams across the agricultural waste value chain.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 136.80 Billion |

| Market Size in 2026 | USD 149.39 Billion |

| Market Size in 2031 | USD 231.96 Billion |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Waste Type Insights

Crop residue waste continues to dominate the global agricultural waste market, accounting for nearly 46% of total market share in 2025, and it remains the most influential feedstock category due to its massive availability and strong integration into modern bioenergy and circular economy systems. The large-scale production of rice straw, wheat straw, corn stover, sugarcane bagasse, and other cereal and cash crop residues across major agricultural economies such as Asia-Pacific, North America, and parts of Europe ensures a consistent and low-cost raw material base for multiple downstream applications. The key growth driver for this segment is the accelerating shift toward renewable energy generation and decarbonization policies, which are encouraging the conversion of agricultural residues into biomass fuels, biochar, and industrial heat energy. Additionally, rising restrictions on open-field burning of crop residues in countries like India, China, and the United States are further strengthening the structured collection and commercialization of this waste stream.Forestry and agro-forestry residues are also witnessing rising global adoption, particularly in biomass pellet manufacturing, pulp substitution, and industrial heating applications. The main growth driver in this segment is the increasing global demand for sustainable alternatives to fossil fuels and wood-based raw materials. Industrial sectors in Europe and Japan are especially reliant on imported biomass pellets derived from forestry and agricultural residues to meet stringent carbon neutrality targets. The expansion of district heating systems and biomass co-firing in thermal power plants is further accelerating demand for these residues.

Processing Technology Insights

Anaerobic digestion remains the leading processing technology segment, accounting for approximately 24% of the global agricultural waste market in 2025. This technology is widely used for converting organic waste such as livestock manure and food-based agricultural residues into biogas and renewable natural gas. The primary growth driver for anaerobic digestion is the global push toward renewable energy diversification, supported by strong government incentives, feed-in tariffs, and carbon reduction mandates. Increasing investments in decentralized energy systems, particularly in rural and agricultural regions, are also enhancing adoption. Furthermore, technological advancements improving methane yield efficiency and lowering operational costs are making anaerobic digestion more economically attractive.Pyrolysis and gasification technologies are experiencing rapid growth as industries seek advanced solutions for producing biochar, syngas, and liquid biofuels with higher energy efficiency. The growth driver here is the increasing need for high-value energy recovery systems that can convert diverse agricultural waste streams into multiple output products. These technologies are also gaining traction due to their ability to support carbon sequestration through biochar production, which is being integrated into climate mitigation strategies and carbon credit markets.Pelletization and briquetting technologies are expanding significantly due to rising global demand for standardized biomass fuels used in industrial boilers, residential heating, and power generation facilities. The main driver is the substitution of coal with renewable biomass fuels in energy-intensive industries. Europe and parts of Asia are leading adoption due to strict emissions regulations and renewable energy mandates. Improved supply chain logistics and export-oriented biomass pellet industries are also supporting global market expansion.

Application Insights

Bioenergy generation remains the largest application segment, accounting for nearly 39% of the agricultural waste market in 2025. This includes biomass power plants, compressed biogas facilities, ethanol production units, and industrial biofuel refineries. The dominant growth driver is the global energy transition toward low-carbon and renewable energy sources, supported by national energy security policies and climate change commitments. Increasing volatility in fossil fuel markets is also accelerating investments in decentralized bioenergy systems that rely on agricultural waste as a stable feedstock source.Organic fertilizers and soil conditioners represent another major application segment, driven by the global expansion of organic farming and regenerative agriculture practices. The key growth driver is the increasing awareness of soil degradation caused by excessive chemical fertilizer usage, prompting farmers to adopt sustainable alternatives. Government subsidies for organic agriculture and certification programs are also supporting this shift. Agricultural waste-derived compost and biofertilizers are becoming essential inputs in improving crop yield sustainability and soil microbial health.Beyond traditional applications, agricultural waste is increasingly utilized in bioplastics, pulp and paper manufacturing, animal feed production, and sustainable construction materials. The primary driver for these diversified applications is the global circular economy movement, which encourages waste valorization across industrial value chains. Biochar applications are emerging rapidly due to increasing focus on carbon sequestration, soil enhancement, and climate-smart agriculture. Additionally, industries are actively exploring agricultural residues as cost-effective raw materials to reduce dependence on virgin resources.

End-Use Industry Insights

The energy and utilities sector accounts for the largest share of agricultural waste consumption globally, driven by the expansion of biomass-based power generation, renewable gas production, and distributed energy systems. The main driver is the increasing integration of renewable energy into national grids and the need for sustainable baseload power sources. Utility companies are investing heavily in biomass co-firing and waste-to-energy infrastructure to meet emission reduction targets.The chemicals and biorefining industries are rapidly expanding their use of agricultural residues for producing bio-based chemicals, ethanol, and renewable polymers. The key driver is the shift away from fossil fuel-based chemical production toward bio-based alternatives. This transition is supported by strong research and development investments in green chemistry and industrial biotechnology.The construction sector is emerging as a high-growth application area, with increasing use of rice husk ash, bagasse fibers, straw composites, and bio-based insulation materials. The main driver is the growing demand for sustainable and low-carbon building materials, especially in urbanizing economies. Green building certifications and environmental regulations are further supporting this trend. Additionally, the pulp and paper industry is increasingly substituting wood-based raw materials with agricultural residues to reduce deforestation pressures and improve supply chain sustainability.

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Waste Market Segmentations

By Waste Type

- Crop Residue Waste

- Animal-Based Agricultural Waste

- Forestry & Agro-Forestry Residue

- Plantation Waste

- Food Processing Agricultural Waste

By Processing Technology

- Composting

- Anaerobic Digestion

- Gasification

- Pyrolysis

- Pelletization & Briquetting

- Waste-to-Energy Conversion

By Application

- Bioenergy Generation

- Organic Fertilizers & Soil Conditioners

- Animal Feed

- Bioplastics & Biochemicals

- Pulp & Paper Production

- Construction Materials

- Activated Carbon & Biochar

By End-Use Industry

- Energy & Utilities

- Agriculture

- Chemicals & Biorefining

- Pulp & Paper

- Construction Materials

- Animal Nutrition Industry

By Distribution & Collection Model

- Direct Farm Collection

- Cooperative Collection Systems

- Third-Party Waste Aggregation

- Integrated Agro-Industrial Collection

Regional Insights

North America

North America accounted for approximately 22% of the global agricultural waste market in 2025, led by the United States and Canada. The United States dominates regional demand due to its advanced agricultural mechanization, large-scale corn and livestock production, and well-established biomass energy infrastructure. The primary growth driver in this region is strong policy support for renewable energy, including renewable natural gas incentives, carbon credit trading systems, and federal decarbonization targets. The expansion of biogas facilities utilizing livestock manure is particularly significant, driven by environmental compliance requirements and methane reduction initiatives. Canada is also experiencing strong growth in biomass pellet production and export-oriented biofuel industries, supported by its abundant forestry and agricultural residues and its strategic focus on clean energy exports.

Europe

Europe remains one of the most technologically advanced regions in the agricultural waste market, accounting for nearly 24% of global market share in 2025. Germany leads the region due to its mature biogas infrastructure and strong implementation of circular economy policies. The key driver across Europe is stringent environmental regulation, including landfill diversion targets, carbon neutrality commitments, and renewable energy directives under the European Green Deal. France, the Netherlands, and the United Kingdom are heavily investing in anaerobic digestion, biomass heating systems, and waste recycling technologies. The region is also witnessing strong growth in bioeconomy initiatives, where agricultural waste is increasingly viewed as a strategic raw material for energy independence and industrial decarbonization.

Asia-Pacific

Asia-Pacific dominates the global agricultural waste market with nearly 41% share in 2025, making it the largest and fastest-growing regional market. China leads global production and utilization due to its vast agricultural base and aggressive investment in biomass energy infrastructure. The key growth driver in China is government-led policies aimed at reducing crop residue burning and promoting large-scale biomass utilization. India is emerging as the fastest-growing market, driven by strong policy initiatives supporting compressed biogas production, ethanol blending programs, and large-scale crop residue management schemes. Japan and South Korea are heavily dependent on biomass pellet imports to meet renewable energy targets, while Southeast Asian countries are rapidly expanding palm residue and rice husk utilization for energy and industrial applications, supported by strong agro-industrial growth.

Latin America

Latin America is emerging as a high-potential growth region, led by Brazil and Argentina. Brazil’s sugarcane industry plays a central role in regional biomass utilization, with bagasse widely used for cogeneration and ethanol production. The key driver in this region is the strong integration of agricultural production with bioenergy systems, particularly in sugar, soybean, and livestock sectors. Government support for renewable energy expansion and rural economic development is further accelerating market growth. Argentina is also expanding its use of agricultural residues for energy and fertilizer production, driven by increasing investments in sustainable agriculture and export-oriented agribusiness models.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but steady growth in agricultural waste utilization. South Africa leads regional adoption due to increasing investments in biomass energy projects and sustainable agricultural practices. The primary growth driver is the need to improve waste management efficiency while supporting renewable energy diversification. Gulf countries are increasingly exploring agricultural waste processing technologies as part of broader food security and sustainability initiatives. Across Africa, rising agricultural output combined with international investment in renewable energy infrastructure is expected to significantly expand long-term opportunities for biomass utilization, organic fertilizer production, and decentralized energy systems.