Mealworm Protein Powder Market Size

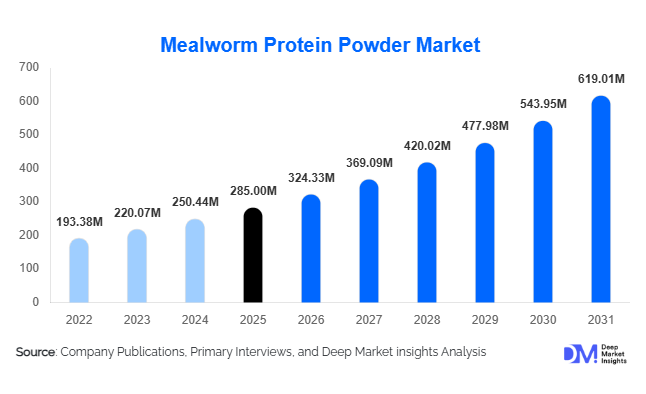

According to Deep Market Insights, the global mealworm protein powder market size was valued at USD 285 million in 2025 and is projected to grow from USD 324.33 million in 2026 to reach USD 619.01 million by 2031, expanding at a CAGR of 13.8% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for sustainable alternative proteins, increasing regulatory approvals for insect-based ingredients, and expanding adoption across aquaculture feed, pet nutrition, and functional food industries.

Key Market Insights

- Animal nutrition dominates the market, accounting for nearly 45% of 2025 revenue, driven by aquaculture feed demand.

- Europe leads globally, contributing approximately 35% of the total market share in 2025 due to early regulatory approvals and sustainability mandates.

- Asia-Pacific is the fastest-growing region, projected to expand at nearly 16% CAGR through 2031, supported by aquaculture expansion.

- Automated vertical farming systems account for over 55% of global production capacity, improving cost efficiency.

- Protein concentrates (70–80% protein) represent around 60% of product demand due to cost-effectiveness in feed and food applications.

- The top five companies control nearly 55% of global revenue, reflecting moderate industry concentration.

What are the latest trends in the mealworm protein powder market?

Industrial Automation in Insect Farming

Automation is rapidly transforming mealworm protein production. Leading producers are investing in AI-driven climate control systems, robotic larvae harvesting, and automated feeding mechanisms to scale production and reduce labor dependency. These innovations have reduced operational costs by an estimated 20–30% over recent years. Vertical farming models are enabling high-density production in controlled environments, ensuring biosecurity and consistent protein yield. Automation also supports standardized output quality, which is critical for feed manufacturers and nutraceutical companies requiring uniform protein specifications.

Hybrid Protein Formulations in Functional Foods

Food manufacturers are increasingly blending mealworm protein with plant-based proteins such as pea and soy to enhance amino acid balance and improve texture in meat alternatives and protein bars. This hybrid formulation strategy reduces sensory barriers for consumers while delivering nutritional benefits. Sports nutrition brands are also introducing insect-protein-based powders as sustainable alternatives to whey, targeting environmentally conscious consumers. The growing demand for clean-label and high-digestibility proteins is reinforcing this trend.

What are the key drivers in the mealworm protein powder market?

Sustainability and Carbon Reduction Initiatives

Mealworm protein production requires significantly less land, water, and feed compared to conventional livestock proteins. With corporations committing to ESG targets and carbon reduction goals, insect protein has emerged as a low-emission alternative. Lifecycle assessments indicate substantially lower greenhouse gas emissions compared to beef and dairy proteins, making it attractive for environmentally focused brands and feed producers.

Aquaculture Industry Expansion

Global aquaculture production continues to grow to meet rising seafood consumption. Fishmeal supply constraints and price volatility are pushing feed manufacturers to adopt alternative protein sources. Mealworm protein offers high digestibility and an optimal amino acid profile, making it a viable partial replacement for fishmeal. Even modest penetration rates into aquafeed formulations represent significant revenue expansion potential.

What are the restraints for the global market?

High Production Costs and Scaling Barriers

Despite automation improvements, insect farming remains capital-intensive. Facility construction costs range between USD 20–60 million per industrial plant. Scaling operations while maintaining biosecurity standards poses operational challenges, impacting profit margins.

Consumer Acceptance in Western Markets

While B2B adoption is rising, direct consumer acceptance of insect-based protein products remains gradual in North America and parts of Europe. Psychological resistance and labeling sensitivities limit mainstream retail adoption.

What are the key opportunities in the mealworm protein powder industry?

Pet Food Premiumization

The global pet food industry is experiencing premiumization, with consumers seeking sustainable and hypoallergenic protein sources. Mealworm protein aligns with these preferences, offering digestibility and sustainability benefits. North American and European premium pet food brands are increasingly incorporating insect protein as a differentiation strategy.

Regulatory Expansion in Emerging Markets

As regulatory approvals expand across Asia-Pacific and Latin America, new growth corridors are opening. Government-backed food security initiatives are encouraging alternative protein investments, particularly in countries aiming to reduce reliance on imported soybean meal and fishmeal.

Product Type Insights

Protein concentrates (70–80% protein) remain the leading product segment, accounting for nearly 60% of total market revenue in 2025. The dominance of concentrates is primarily driven by their cost-to-protein efficiency ratio, making them highly attractive for bulk feed applications and functional food fortification. Feed manufacturers prefer concentrates due to balanced amino acid composition, high digestibility, and comparatively lower processing costs than isolates. Additionally, concentrates integrate easily into aquafeed pellets and poultry mash formulations without requiring extensive reformulation. As aquaculture and pet food sectors expand globally, this segment is expected to maintain leadership over the forecast period.

Protein isolates (>80% protein) are the fastest-growing premium segment, particularly within sports nutrition, nutraceuticals, and specialized dietary supplements. Although they command higher pricing due to additional purification processes, isolates offer superior protein density, reduced fat content, and enhanced solubility, making them suitable for high-performance formulations. Meanwhile, blended protein formulations combining mealworm protein with plant-based proteins are emerging in hybrid meat products and functional snacks, helping improve amino acid balance while addressing consumer sensory preferences.

Application Insights

Animal nutrition leads the application segment, representing approximately 45% of global market share in 2025. The key driver behind this leadership is the rapid expansion of aquaculture production worldwide, coupled with volatility in fishmeal prices. Mealworm protein serves as a sustainable partial replacement for traditional marine-based proteins, offering strong feed conversion ratios and digestibility. Poultry feed is also contributing to segment growth, particularly in regions seeking sustainable feed alternatives.

Food & beverage applications account for nearly 35% of revenue, driven by growing demand for sustainable protein ingredients in sports nutrition, protein bars, baked goods, and meat alternatives. The increasing popularity of hybrid protein products, combining insect and plant proteins, is reducing consumer resistance while enhancing nutritional profiles. Pet food remains a rapidly growing sub-segment within animal nutrition, supported by premiumization trends and demand for hypoallergenic formulations. Cosmetics and nutraceutical applications collectively hold a smaller share but are gaining attention due to bioactive peptides and micronutrient content present in mealworm protein.

Distribution Channel Insights

Direct B2B sales dominate distribution channels, accounting for nearly 70% of total market revenue in 2025. Long-term supply agreements between insect protein producers and feed or food processors ensure price stability and consistent volume procurement. The dominance of B2B channels is driven by bulk purchasing patterns and the ingredient-based nature of mealworm protein applications.

Online B2C channels are expanding steadily, particularly in North America and Europe, where branded insect protein powders target athletes, fitness enthusiasts, and environmentally conscious consumers. E-commerce platforms provide education, transparency, and direct consumer engagement, helping overcome perception barriers. Specialty health stores and modern retail chains continue to represent a smaller but gradually expanding share as awareness improves and regulatory approvals broaden retail accessibility.

End-Use Industry Insights

Feed manufacturers represent the largest end-use industry, contributing approximately 40% of total market demand. This dominance is driven by aquaculture feed expansion in Asia-Pacific and Europe, where fishmeal substitution is becoming strategically important for cost management and sustainability compliance. Bulk procurement contracts and recurring demand cycles reinforce feed manufacturers’ leadership position.

Food processing companies account for around 30% of market demand, fueled by growth in protein-enriched snacks, sports supplements, and fortified foods. Nutraceutical manufacturers are witnessing consistent growth as research supports the digestibility and micronutrient density of insect protein. Export-driven demand remains strongest in Asia-Pacific, where expanding shrimp and fish farming industries rely on imported insect-based feed ingredients to support production growth and reduce marine ecosystem dependence.

| By Product Type | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Europe

Europe leads the global mealworm protein powder market with approximately 35% share in 2025. Growth in the region is primarily driven by progressive regulatory frameworks, including novel food approvals that have accelerated commercialization. Countries such as France and the Netherlands function as production hubs, supported by advanced insect farming technologies and strong venture capital investments. Germany and Denmark are major consumption markets, particularly within functional foods and sustainable feed applications. The European Union’s sustainability mandates and carbon reduction targets further drive adoption among food manufacturers seeking low-emission protein sources.

Asia-Pacific

Asia-Pacific accounts for roughly 30% of global market share and is the fastest-growing region, expanding at nearly 16% CAGR. China alone represents about 15% of global demand, supported by its massive aquaculture industry and rising feed protein requirements. Thailand and Vietnam are emerging as high-growth aquafeed markets due to expanding shrimp and fish exports. Regional growth is fueled by increasing seafood consumption, government-backed food security initiatives, and efforts to reduce reliance on imported soybean meal and fishmeal.

North America

North America contributes approximately 20% of global revenue, led by the United States. Growth drivers include premium pet food innovation, increasing demand for sustainable sports nutrition products, and expanding consumer awareness of alternative proteins. Venture capital investment in insect agriculture and supportive research initiatives is strengthening domestic production capacity.

Latin America

Latin America represents nearly 8% of the global market, with Brazil and Chile leading regional demand. Growth is largely tied to aquaculture development and export-oriented seafood production. Rising feed costs and the need for sustainable protein inputs are encouraging gradual adoption of insect-derived feed ingredients.

Middle East & Africa

The Middle East & Africa region accounts for around 7% of global revenue. Growth is supported by increasing sustainability initiatives, feed imports for poultry production, and food security diversification strategies in countries such as the UAE and South Africa. Additionally, the region’s proximity to aquaculture hubs in Africa creates opportunities for insect protein integration within local feed supply chains.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Mealworm Protein Powder Market

- Ÿnsect

- Protix

- InnovaFeed

- Entomo Farms

- Beta Hatch

- MealFood Europe

- NextProtein

- EnviroFlight

- Hexafly

- Aspire Food Group

- Jimini’s

- Protenga

- Entobel

- Insectta

- Kreca Ento-Food