Organic Fertilizer Market Size

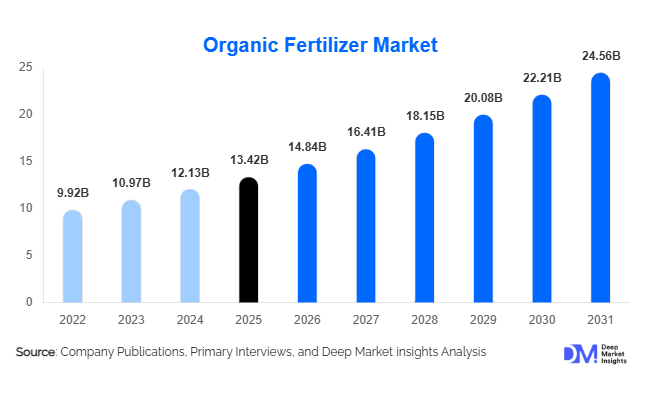

According to Deep Market Insights, the global organic fertilizer market size was valued at USD 13.42 billion in 2025 and is projected to grow from USD 14.85 billion in 2026 to reach USD 24.60 billion by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The organic fertilizer market growth is primarily driven by increasing adoption of sustainable farming practices, rising consumer demand for organic food products, and government initiatives aimed at reducing chemical fertilizer dependency and improving soil health.

Key Market Insights

- Organic fertilizers are increasingly becoming integral to regenerative agriculture practices, driven by global efforts to restore soil fertility, reduce carbon emissions, and improve long-term agricultural productivity.

- Biofertilizers and microbial-based formulations are witnessing strong adoption, particularly in commercial farming and greenhouse cultivation due to their higher nutrient efficiency and eco-friendly profile.

- Asia-Pacific dominates the global market, led by India and China owing to large agricultural economies, expanding organic cultivation acreage, and supportive government subsidies.

- Europe remains one of the fastest-growing markets, supported by strict environmental regulations and rising demand for certified organic produce.

- Liquid organic fertilizers are gaining significant traction, particularly in precision agriculture, hydroponics, and controlled-environment farming systems.

- Technological integration in microbial fermentation and precision nutrient management is improving fertilizer efficiency, crop productivity, and farmer adoption rates globally.

What are the latest trends in the organic fertilizer market?

Regenerative Agriculture Accelerating Organic Fertilizer Adoption

Regenerative agriculture is emerging as one of the most influential trends within the organic fertilizer market. Governments, agricultural cooperatives, and multinational food companies are increasingly promoting farming systems focused on restoring soil biodiversity, reducing synthetic chemical usage, and improving carbon sequestration. Organic fertilizers play a central role in these systems by improving microbial activity, enhancing soil structure, and increasing water retention capacity. Farmers are gradually shifting toward integrated nutrient management practices that combine compost-based fertilizers, microbial inoculants, and crop residue recycling to maintain long-term soil fertility.

Large food manufacturers and retail chains are also encouraging sustainable sourcing practices by partnering with farms using certified organic and regenerative agricultural methods. Carbon-credit programs linked to sustainable farming are further accelerating investment in organic crop nutrition solutions. As global concerns surrounding soil degradation and climate change intensify, regenerative farming models are expected to become a major long-term growth engine for the organic fertilizer market.

Advanced Biofertilizer Technologies Reshaping the Market

Technological innovation in microbial fertilizers and biological nutrient formulations is significantly transforming the organic fertilizer industry. Companies are increasingly developing advanced biofertilizers containing nitrogen-fixing bacteria, phosphate-solubilizing microorganisms, and mycorrhizal fungi capable of improving nutrient uptake efficiency and enhancing crop productivity. Liquid organic fertilizers integrated with precision agriculture systems are also becoming increasingly popular across horticulture and greenhouse cultivation.

Manufacturers are investing heavily in automated microbial fermentation technologies, controlled-release nutrient systems, and AI-driven soil analysis tools that help optimize fertilizer application rates. Precision farming integration is reducing nutrient losses while improving operational efficiency for commercial growers. Additionally, hydroponic and vertical farming operators are increasingly adopting specialized organic nutrient formulations compatible with modern controlled-environment agriculture systems, creating new revenue opportunities for market participants.

What are the key drivers in the organic fertilizer market?

Growing Demand for Organic Food Products

The increasing global preference for organic food products is one of the primary drivers supporting organic fertilizer market expansion. Consumers are becoming increasingly health-conscious and are demanding food products cultivated without synthetic chemicals, pesticides, or genetically modified inputs. This trend has significantly increased global organic farming acreage, thereby boosting demand for certified organic fertilizers across cereals, fruits, vegetables, and plantation crops.

Retailers and food processing companies are also implementing stricter sourcing standards for residue-free produce, encouraging farmers to transition toward organic nutrient management systems. Rising exports of organic agricultural products from countries such as India, Mexico, Peru, and Vietnam are further contributing to market growth, as exporters increasingly require certified organic fertilizers to comply with international quality standards.

Government Support for Sustainable Agriculture

Governments worldwide are implementing policies and subsidy programs aimed at reducing excessive chemical fertilizer consumption and improving environmental sustainability. Initiatives promoting organic farming, regenerative agriculture, and soil restoration are driving fertilizer adoption across both developed and emerging economies. Programs such as India’s Paramparagat Krishi Vikas Yojana (PKVY) and the European Union’s Farm to Fork Strategy are encouraging large-scale adoption of organic farming inputs.

Environmental concerns related to groundwater contamination, greenhouse gas emissions, and declining soil fertility are prompting regulators to strengthen sustainability mandates. Financial incentives, training programs, and infrastructure investments supporting biological crop nutrition are further accelerating market expansion globally.

What are the restraints for the global market?

Lower Nutrient Concentration Compared to Synthetic Fertilizers

One of the major restraints within the organic fertilizer market is the relatively lower nutrient concentration compared to synthetic fertilizers. Organic fertilizers generally release nutrients slowly and often require larger application volumes to achieve similar crop productivity levels. This increases transportation, storage, and handling costs for farmers, particularly in large-scale commercial agriculture operations.

In addition, nutrient variability associated with compost-based fertilizers can create challenges in achieving standardized crop performance. Farmers focused on maximizing short-term yields may continue relying on synthetic fertilizers due to their higher nutrient efficiency and immediate crop response.

Quality Standardization and Supply Chain Challenges

Product quality inconsistency remains a significant challenge within the global organic fertilizer market. Variations in raw material composition, microbial viability, and nutrient release patterns can affect fertilizer performance and reduce farmer confidence. In several developing economies, weak regulatory oversight has resulted in the circulation of low-quality products, slowing broader market penetration.

Supply chain limitations also create operational challenges for manufacturers. Organic fertilizers are highly dependent on agricultural waste, livestock manure, and biological raw materials, making consistent sourcing and processing critical. Rising logistics and processing costs can negatively impact manufacturer profit margins and product affordability.

What are the key opportunities in the organic fertilizer industry?

Expansion of Greenhouse and Urban Farming

The rapid growth of greenhouse cultivation, vertical farming, and urban agriculture is creating substantial opportunities for organic fertilizer manufacturers. Controlled-environment agriculture systems require highly specialized nutrient formulations capable of delivering efficient crop nutrition without compromising sustainability goals. Liquid organic fertilizers and microbial nutrient solutions are increasingly being adopted in hydroponic systems, rooftop farms, and indoor cultivation facilities.

Governments across the Middle East, Asia-Pacific, and Europe are investing heavily in urban farming infrastructure to improve food security and reduce agricultural import dependency. As urban agriculture expands, demand for compact, odor-controlled, and water-efficient organic fertilizers is expected to increase significantly.

Export-Oriented Organic Agriculture

Export-driven agricultural production is emerging as another major opportunity area for the organic fertilizer market. Global demand for certified organic fruits, vegetables, tea, coffee, spices, and cereals continues to rise, particularly in North America and Europe. Farmers producing export-oriented crops are increasingly adopting certified organic fertilizers to comply with international food safety regulations and organic certification standards.

Countries including India, Brazil, Vietnam, and Peru are expanding their organic agricultural exports, creating strong demand for premium biofertilizers, compost-based nutrients, and microbial crop nutrition products. Manufacturers capable of offering traceable, certified, and export-compliant fertilizer solutions are expected to gain a competitive advantage in international markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.42 Billion |

| Market Size in 2026 | USD 14.84 Billion |

| Market Size in 2031 | USD 24.56 Billion |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Type Insights

The global organic fertilizer market is witnessing significant transformation across source categories as agricultural producers increasingly prioritize sustainable soil management, long-term crop productivity, and environmentally responsible farming practices. Among all source types, animal-based organic fertilizers continue to dominate the global market, accounting for nearly 38% of total demand in 2025. The widespread adoption of poultry manure, vermicompost, bone meal, blood meal, and fish emulsion fertilizers is largely attributed to their superior nutrient concentration, cost efficiency, easy availability, and proven effectiveness across large-scale agricultural operations. Poultry manure remains particularly prominent due to its rich nitrogen and phosphorus content, making it highly suitable for cereal cultivation, horticulture, and plantation farming. In Asia-Pacific, especially across India and China, the integration of livestock farming with crop cultivation systems has created a strong supply ecosystem for animal-based fertilizers, supporting continuous market expansion.Plant-based organic fertilizers are emerging as one of the fastest-growing categories due to increasing consumer demand for residue-free food products and environmentally sustainable crop nutrition solutions. Products including compost, green manure, oilseed cakes, seaweed extracts, and crop residue-based fertilizers are witnessing strong adoption across both developed and developing economies. Seaweed extracts in particular are gaining substantial popularity in high-value horticulture and greenhouse cultivation due to their ability to improve root development, stress resistance, and crop quality. Green manure practices are also expanding rapidly as farmers increasingly focus on regenerative agriculture and soil restoration techniques that naturally replenish nutrients while improving soil biodiversity.Mineral and microbial organic fertilizers are witnessing accelerated demand growth due to ongoing technological advancements in agricultural biotechnology. Biofertilizers containing nitrogen-fixing bacteria, phosphate-solubilizing microorganisms, potassium mobilizers, and mycorrhizal fungi are increasingly integrated into modern farming systems to enhance nutrient-use efficiency while reducing dependence on synthetic fertilizers. These products are becoming highly attractive in precision agriculture and sustainable farming systems because they improve nutrient absorption, stimulate root growth, and strengthen soil microbial ecosystems. Growing research investments in biological crop nutrition technologies, coupled with rising demand for climate-resilient farming solutions, are expected to further accelerate adoption of microbial and mineral organic fertilizers over the coming years.

Nutrient Type Insights

Based on nutrient type, multi-nutrient organic fertilizers accounted for approximately 34% of the global market in 2025 and continue to represent the leading product category within the industry. Their dominance is primarily driven by increasing farmer preference for balanced crop nutrition systems capable of simultaneously supplying nitrogen, phosphorus, potassium, and essential micronutrients through a single integrated formulation. Multi-nutrient products significantly improve nutrient management efficiency while reducing operational complexity for commercial farming operations. Their ability to enhance soil fertility, optimize crop yield, and support long-term soil sustainability has made them highly attractive across large-scale agriculture, horticulture, and plantation farming sectors.The leading position of multi-nutrient organic fertilizers is also supported by rising awareness surrounding soil nutrient imbalance caused by excessive use of synthetic fertilizers. Farmers are increasingly seeking comprehensive nutrient solutions that not only improve crop productivity but also restore soil microbial activity and organic matter content. Integrated nutrient formulations containing composted organic matter, biofertilizers, amino acids, and micronutrients are gaining strong traction because they support sustainable crop production while minimizing environmental impact.Nitrogenous organic fertilizers continue to witness substantial demand across cereals, grains, and forage crop cultivation due to the critical role of nitrogen in plant growth and chlorophyll formation. Products such as manure-based nitrogen fertilizers, fish emulsion, and legume-derived biofertilizers are extensively utilized in rice, wheat, and corn farming operations. Meanwhile, phosphatic organic fertilizers are experiencing strong adoption in fruit farming, floriculture, and vegetable cultivation because phosphorus is essential for root development, flowering, and crop maturation. Increasing global horticulture production and export-oriented farming are contributing significantly to segment expansion.Micronutrient-based organic fertilizers are also emerging as an increasingly important category due to growing recognition of trace element deficiencies affecting agricultural productivity. Deficiencies in zinc, boron, iron, magnesium, and sulfur have become widespread across intensively cultivated soils globally. As a result, farmers are increasingly adopting micronutrient-enriched organic fertilizers to improve crop quality, enhance disease resistance, and support balanced plant growth. The growing popularity of specialty crops, precision farming systems, and controlled-environment agriculture is expected to create substantial long-term growth opportunities for micronutrient organic fertilizers worldwide.

Form Insights

Dry organic fertilizers continue to dominate the global market with nearly 62% share in 2025 due to their operational convenience, extended shelf life, lower transportation costs, and compatibility with mechanized farming equipment. Granular and pelletized fertilizers remain highly preferred across commercial agriculture because they allow uniform field application, controlled nutrient release, and improved storage efficiency. Their easy handling and suitability for bulk transportation make them particularly attractive for large-scale farming operations across Asia-Pacific, North America, and Latin America.The leading position of dry organic fertilizers is strongly supported by rising mechanization within modern agriculture. Farmers increasingly favor granular and pelletized products because they can be integrated efficiently into seeding equipment, spreaders, and precision farming systems. Additionally, pelletized organic fertilizers help reduce nutrient volatilization losses while ensuring steady nutrient availability over longer crop cycles. Compost-based powder fertilizers also continue witnessing widespread adoption among smallholder farmers and horticulture growers due to their affordability and easy soil incorporation.Liquid organic fertilizers are emerging as the fastest-growing segment globally due to increasing adoption of precision agriculture technologies, greenhouse farming, hydroponics, and fertigation systems. Liquid formulations provide faster nutrient absorption, higher nutrient-use efficiency, and more accurate dosage management compared to conventional dry fertilizers. Their compatibility with drip irrigation systems and controlled-environment agriculture is significantly accelerating market penetration across developed agricultural economies.Technological advancements in liquid biofertilizer stabilization and microbial nutrient delivery systems are further supporting segment growth. Commercial growers increasingly prefer liquid organic fertilizers because they improve crop response times, enhance nutrient uptake efficiency, and minimize nutrient wastage. The rapid expansion of high-value greenhouse crops, hydroponic vegetables, and protected cultivation systems globally is expected to create substantial opportunities for liquid organic fertilizer manufacturers during the forecast period.

Crop Type Insights

Fruits and vegetables represent the leading crop segment within the global organic fertilizer market, accounting for nearly 29% of total demand in 2025. The dominance of this segment is primarily driven by rapidly growing consumer preference for organic fresh produce, rising awareness regarding food safety, and increasing demand for pesticide-free fruits and vegetables across both domestic and export markets. Organic fertilizers are widely utilized in horticulture production because they improve soil health, enhance crop quality, and support sustainable farming systems capable of producing premium-grade produce.The leading growth driver for the fruits and vegetables segment is the expanding global demand for residue-free horticultural products. Consumers increasingly associate organically grown fruits and vegetables with higher nutritional value, improved taste, and lower chemical contamination risks. This trend has encouraged commercial growers to integrate compost, microbial biofertilizers, seaweed extracts, and vermicompost into crop nutrition programs. Export-oriented horticulture industries across Asia-Pacific, Europe, and Latin America are particularly driving demand for certified organic fertilizers due to strict international food safety regulations.Cereals and grains remain another important application area for organic fertilizers, especially across India, China, Brazil, and other emerging agricultural economies where sustainable farming practices are gaining momentum. Farmers are increasingly utilizing organic fertilizers in rice, wheat, and maize cultivation to improve soil structure, maintain long-term fertility, and reduce dependency on synthetic inputs. Commercial crops such as tea, coffee, sugarcane, cocoa, and cotton are also witnessing rising adoption of microbial fertilizers and compost-based nutrients as global buyers increasingly prioritize sustainability compliance within agricultural supply chains.Plantation crop producers are increasingly adopting biofertilizers and organic soil amendments to improve soil productivity, enhance drought resistance, and support regenerative agricultural practices. Rising sustainability certification requirements within international commodity markets are expected to further strengthen long-term demand across commercial crop cultivation globally.

Application Method Insights

Soil treatment remains the dominant application method in the global organic fertilizer market, accounting for nearly 47% of total demand in 2025. The widespread adoption of soil-based fertilizer application is largely attributed to its effectiveness in restoring soil fertility, improving microbial activity, increasing organic carbon levels, and enhancing water retention capacity. Farmers continue prioritizing direct soil application because it provides long-term agronomic benefits while supporting sustainable crop production systems.Fertigation and foliar application methods are witnessing rapid growth due to rising adoption of precision farming technologies and controlled-environment agriculture systems. Fertigation allows efficient nutrient delivery through irrigation systems while minimizing nutrient losses and optimizing water usage. This method is particularly gaining traction across greenhouse farming, hydroponics, and high-value horticulture cultivation. Foliar spray applications are also becoming increasingly popular because they provide rapid nutrient absorption and help address micronutrient deficiencies during critical crop growth stages.Seed treatment applications involving microbial biofertilizers are emerging as an important growth segment within the market. Farmers are increasingly adopting biological seed coatings containing beneficial microorganisms to improve germination rates, strengthen root development, and enhance early-stage crop health. Growing awareness surrounding sustainable crop establishment techniques and biological farming solutions is expected to drive further expansion within this segment.

Farming Type Insights

Organic farming accounted for approximately 52% of global organic fertilizer demand in 2025 and continues to represent the dominant farming type within the industry. The segment’s leadership is supported by rising certification requirements, increasing consumer demand for chemical-free food products, and expanding government incentives promoting sustainable agriculture practices. Organic fertilizers play a critical role in certified organic farming systems because they improve soil biodiversity, maintain ecological balance, and support long-term agricultural sustainability.The primary growth driver for this segment is the rapid expansion of global organic food consumption. Consumers increasingly prefer organically produced food products due to health concerns associated with synthetic pesticide and chemical fertilizer residues. This trend has encouraged farmers worldwide to transition toward organic farming systems supported by compost, manure-based fertilizers, microbial inoculants, and biofertilizers. Rising export opportunities for certified organic agricultural commodities are also significantly contributing to segment growth.Integrated Nutrient Management practices are witnessing strong adoption as farmers seek balanced approaches combining organic and conventional nutrient systems to maximize productivity while improving sustainability. INM strategies help optimize nutrient efficiency, reduce input costs, and improve long-term soil fertility. Meanwhile, regenerative agriculture is emerging as one of the fastest-growing farming approaches globally due to increasing emphasis on soil carbon sequestration, biodiversity restoration, and climate-resilient agriculture. Regenerative farming systems heavily depend on organic fertilizers, composting practices, and biological soil enhancement technologies to rebuild soil ecosystems and reduce environmental impact.

End-Use Insights

Commercial agriculture remains the largest end-use segment within the global organic fertilizer market, representing nearly 44% of total demand in 2025. Large-scale farming operations are increasingly integrating organic fertilizers into nutrient management programs to improve soil quality, enhance sustainability compliance, and meet export market standards. Commercial growers are also adopting organic fertilizers to improve long-term productivity while addressing environmental concerns associated with intensive chemical fertilizer use.The leading driver supporting commercial agriculture dominance is the growing pressure on agricultural producers to adopt sustainable farming practices capable of meeting evolving environmental regulations and consumer expectations. Export-oriented farming operations increasingly require sustainable crop nutrition systems to comply with international residue standards and environmental certifications. This has accelerated demand for organic manure, compost, biofertilizers, and microbial inoculants across commercial agriculture globally.Horticulture remains one of the fastest-growing end-use sectors due to increasing global demand for premium fruits, vegetables, flowers, ornamental plants, and greenhouse crops. Organic fertilizers are widely utilized within horticulture because they improve crop quality, enhance shelf life, and support sustainable production practices. Home gardening and urban farming are also emerging as attractive demand segments, particularly across North America and Europe where consumers are increasingly adopting rooftop gardening, indoor farming, and sustainable landscaping practices.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Fertilizer Market Segmentations

By Source Type

- Plant-Based Organic Fertilizers

- Animal-Based Organic Fertilizers

- Mineral & Microbial Organic Fertilizers

By Nutrient Type

- Nitrogenous Organic Fertilizers

- Phosphatic Organic Fertilizers

- Potassic Organic Fertilizers

- Micronutrient Organic Fertilizers

- Multi-Nutrient Organic Fertilizers

By Form

- Dry Organic Fertilizers

- Liquid Organic Fertilizers

By Crop Type

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

- Commercial Crops

- Turf & Ornamental Crops

By Application Method

- Soil Treatment

- Seed Treatment

- Fertigation

- Foliar Application

- Root Dipping

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 41% of the global organic fertilizer market in 2025, making it the largest regional market worldwide. China and India continue to dominate regional demand due to vast agricultural land resources, expanding organic farming acreage, and strong government support for sustainable agriculture initiatives. The region’s market growth is heavily supported by rising population pressure, increasing food security concerns, and the need to improve long-term agricultural productivity while minimizing environmental degradation.Southeast Asian economies including Vietnam, Indonesia, and Thailand are witnessing rapid adoption of organic fertilizers due to expanding exports of organic rice, coffee, cocoa, and tropical fruits. Rising awareness regarding soil degradation, increasing climate-related agricultural risks, and growing adoption of regenerative farming practices are further accelerating market expansion across the region. Additionally, the availability of abundant agricultural residues and livestock waste supports large-scale production of cost-effective organic fertilizers throughout Asia-Pacific.

Europe

Europe held nearly 29% of global organic fertilizer market share in 2025, supported by strict environmental regulations, strong sustainability policies, and high consumer demand for organic food products. Germany, France, Italy, Spain, and the Netherlands remain major contributors to regional market growth due to advanced organic farming infrastructure and extensive adoption of sustainable agricultural technologies.Demand for liquid organic fertilizers, microbial inoculants, and precision nutrient delivery systems remains particularly strong across greenhouse cultivation and technologically advanced farming operations. Europe’s highly developed organic food retail sector continues creating strong downstream demand for certified organic agricultural products, further supporting fertilizer consumption across the region.

North America

North America represents one of the most technologically advanced organic fertilizer markets globally, led primarily by the United States and Canada. Rising investments in regenerative agriculture, precision farming technologies, biological crop inputs, and sustainable food production systems continue driving market expansion across the region.Government support for climate-smart agriculture, increasing consumer preference for sustainably produced food, and technological advancements in precision nutrient application are further strengthening market growth across North America. Commercial growers are increasingly integrating organic fertilizers into advanced irrigation and data-driven farming systems to improve nutrient efficiency and reduce environmental impact.

Latin America

Latin America is emerging as a high-potential growth market for organic fertilizers, led by Brazil, Mexico, Argentina, Chile, and Peru. The region’s expanding soybean, sugarcane, coffee, cocoa, and fruit cultivation industries are increasingly adopting organic fertilizers to improve soil productivity and reduce long-term dependence on synthetic chemicals.Government support programs promoting sustainable farming practices, combined with increasing awareness regarding soil degradation and nutrient depletion, are accelerating organic fertilizer penetration across the region. Favorable climatic conditions for organic crop production and growing international trade opportunities are expected to create substantial long-term market potential throughout Latin America.

Middle East & Africa

The Middle East & Africa region is expected to witness one of the fastest growth rates during the forecast period due to increasing investments in food security, controlled-environment agriculture, and sustainable farming infrastructure. Countries including Saudi Arabia, the UAE, South Africa, Kenya, and Egypt are increasingly adopting organic fertilizers to improve agricultural productivity under challenging climatic conditions.In Africa, expanding exports of organic fruits, cocoa, coffee, and horticultural products are supporting strong demand for sustainable crop nutrition solutions. International development programs promoting climate-smart agriculture, combined with rising investments in rural farming infrastructure and soil restoration initiatives, are expected to accelerate long-term market growth across the region.

Key Players in the Organic Fertilizer Market

- Nutrien Ltd.

- Yara International

- ICL Group

- Coromandel International

- The Scotts Miracle-Gro Company

- Tata Chemicals

- Gujarat State Fertilizers & Chemicals (GSFC)

- National Fertilizers Limited

- Rizobacter

- Biolchim S.p.A.

- Symborg

- AgroLiquid

- Suståne Natural Fertilizer

- Midwestern BioAg

- BioStar Renewables