Coco Peat Market Size

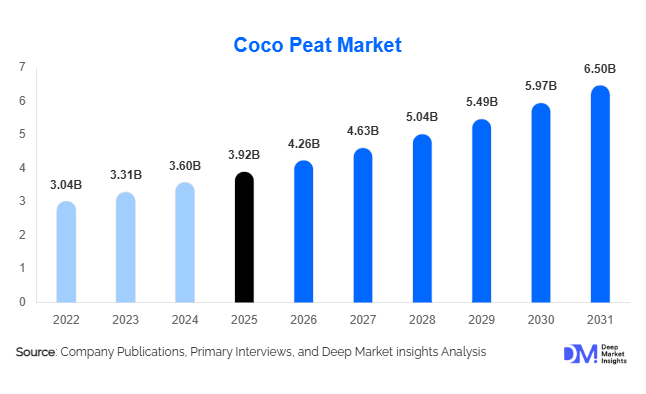

According to Deep Market Insights, the global coco peat market size was valued at USD 3.92 billion in 2025 and is projected to grow from USD 4.26 billion in 2026 to reach USD 6.50 billion by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The coco peat market growth is primarily driven by increasing adoption of sustainable horticulture practices, rapid expansion of greenhouse cultivation, and rising demand for hydroponic and peat-free growing substrates across commercial agriculture and controlled-environment farming systems.

Key Market Insights

- Coco peat is increasingly replacing peat moss in commercial horticulture, driven by sustainability regulations and environmental concerns regarding peatland degradation.

- Hydroponics and controlled-environment agriculture are becoming major demand centers, particularly in North America, Europe, and the Middle East.

- Asia-Pacific dominates global production and exports, led by India and Sri Lanka due to abundant coconut cultivation and established coir processing industries.

- Europe remains one of the fastest-growing consumption regions, supported by peat-free cultivation initiatives and greenhouse expansion.

- Commercial greenhouse operators increasingly prefer buffered and low-EC coco peat, improving demand for premium-grade substrates.

- Technological advancements in washing, buffering, sterilization, and compression are improving product quality and export competitiveness globally.

coco peat market latest trends

Rapid Shift Toward Peat-Free Cultivation

The global horticulture industry is rapidly transitioning toward peat-free growing media, creating substantial demand for coco peat products. Environmental concerns associated with peat extraction, including carbon emissions and peatland ecosystem destruction, are encouraging governments and horticultural companies to adopt sustainable alternatives. Coco peat has emerged as one of the most preferred substitutes due to its biodegradability, water retention capacity, and renewability. European retailers and greenhouse operators are increasingly launching peat-free product lines for both commercial and retail gardening applications. Commercial nurseries are integrating coco peat into professional growing mixes to meet sustainability targets and regulatory expectations. This trend is expected to significantly strengthen long-term demand for premium-grade washed and buffered coco peat products.

Expansion of Hydroponics and Vertical Farming

The rapid growth of hydroponics, indoor farming, and vertical agriculture is significantly reshaping the coco peat market. Modern hydroponic cultivation systems require substrates that provide stable moisture management, efficient root aeration, and low pathogen risks. Coco peat’s ability to maintain nutrient stability while supporting high crop yields makes it highly suitable for hydroponic vegetables, herbs, berries, and cannabis cultivation. Indoor farming companies are increasingly investing in customized coco peat blends designed specifically for controlled-environment agriculture. Advanced substrate formulations combining coco peat with perlite and coco chips are becoming increasingly common across commercial greenhouse projects. Automation in greenhouse agriculture and precision irrigation systems are further increasing demand for consistent and high-performance growing media globally.

coco peat market drivers

Growing Adoption of Sustainable Agriculture

Global agricultural systems are increasingly shifting toward environmentally sustainable cultivation practices, driving strong demand for natural and biodegradable growing media such as coco peat. Governments, agricultural cooperatives, and food producers are prioritizing water-efficient and eco-friendly farming techniques to reduce environmental impact while maintaining productivity. Coco peat improves water retention and soil aeration while reducing dependency on synthetic soil conditioners. Organic farming acreage continues to expand globally, particularly in Europe and North America, further supporting market growth. The increasing use of coco peat in landscaping, reforestation, and soil rehabilitation projects is also contributing to wider adoption across multiple agricultural applications.

Expansion of Commercial Greenhouse Cultivation

Commercial greenhouse farming is expanding rapidly across Europe, North America, China, and the Middle East due to growing food security concerns and rising demand for year-round crop production. Greenhouse growers require reliable growing substrates that improve root-zone stability, nutrient absorption, and crop consistency. Coco peat has become one of the preferred growing media for tomatoes, cucumbers, peppers, strawberries, herbs, and leafy greens cultivated under controlled conditions. Large-scale greenhouse investments in arid regions such as the UAE and Saudi Arabia are particularly supporting premium coco peat demand due to the substrate’s superior water retention characteristics.

coco peat market restraints

Supply Chain Dependence on Coconut-Producing Regions

The global coco peat industry remains heavily dependent on coconut-producing countries such as India, Sri Lanka, Indonesia, and the Philippines. Climatic fluctuations, monsoon disruptions, labor shortages, export policy changes, and logistics bottlenecks can significantly impact global supply consistency and pricing. Rising freight costs and container shortages have also created challenges for exporters serving Europe and North America. Since a major portion of the market depends on international trade, transportation disruptions can affect lead times and inventory management for greenhouse operators and distributors.

Quality Inconsistency and Salinity Concerns

Quality inconsistency remains a key challenge within the coco peat market, particularly among low-cost suppliers lacking advanced processing infrastructure. Improper washing and buffering processes can result in high sodium and potassium levels, negatively affecting crop productivity in hydroponic systems. Commercial growers increasingly demand low-electrical-conductivity (EC), pathogen-free, and sterilized substrates, forcing suppliers to invest in advanced processing technologies and quality certifications. Smaller manufacturers often face difficulties competing in premium export markets due to limited technological capabilities and inconsistent product standards.

coco peat industry key opportunities

Growth of Controlled-Environment Agriculture

The expansion of controlled-environment agriculture (CEA), including hydroponics, greenhouse farming, and vertical farming, presents one of the largest opportunities for the coco peat market. Governments and private investors are increasing investments in indoor agriculture systems to improve food security, reduce water usage, and ensure year-round crop production. Coco peat’s superior aeration and moisture retention capabilities make it highly suitable for precision farming systems. Increasing commercial cultivation of leafy greens, berries, herbs, and tomatoes in climate-controlled environments is expected to drive long-term demand for premium-grade coco peat products.

Rising Demand for Premium Hydroponic Substrates

Hydroponic cultivation and cannabis farming are generating strong demand for high-quality buffered coco peat substrates with low EC levels and customized nutrient compatibility. Growers increasingly prefer specialized substrate blends designed for specific crops and controlled cultivation systems. Manufacturers capable of supplying pathogen-free, UV-treated, and professionally buffered products are expected to gain strong competitive advantages. The rise of urban farming, commercial indoor agriculture, and export-oriented horticulture further creates opportunities for value-added substrate solutions with higher profit margins.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.92 Billion |

| Market Size in 2026 | USD 4.26 Billion |

| Market Size in 2031 | USD 6.50 Billion |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Coco peat blocks dominate the market, accounting for nearly 36% of global demand due to their superior compression efficiency, lower transportation costs, and suitability for export logistics. Commercial greenhouse operators and distributors prefer compressed blocks because they expand significantly after hydration while minimizing storage expenses. Coco peat briquettes are increasingly popular among home gardeners and small-scale growers because of their ease of handling and compact packaging. Grow bags are witnessing strong demand from greenhouse tomato, cucumber, and berry cultivation projects, particularly across Europe and the Middle East. Loose coco peat products remain important in landscaping and retail gardening applications where immediate usability is preferred over compression efficiency. Buffered and washed coco peat products are rapidly gaining share in premium hydroponic applications due to increasing demand for low-salinity growing media.

Application Insights

Horticulture remains the leading application segment, accounting for nearly 39% of global market demand in 2025. Commercial nurseries, greenhouse farming, floriculture, and landscaping activities continue to drive large-scale adoption of coco peat substrates. Hydroponics and controlled-environment agriculture represent the fastest-growing application segment, supported by increasing investments in vertical farming and indoor crop production. Organic farming applications are also expanding steadily as growers seek sustainable soil conditioning solutions. Mushroom cultivation, erosion control, and reforestation projects are emerging niche applications supporting additional market diversification. Increasing adoption of coco peat within cannabis cultivation is further strengthening premium-grade substrate demand globally.

Distribution Channel Insights

Direct B2B sales dominate the coco peat market with nearly 47% market share, driven by bulk procurement from greenhouse operators, hydroponic farms, nurseries, and agricultural cooperatives. Agricultural input distributors continue to play a major role in emerging economies where localized supply chains remain important for commercial growers. Garden centers and retail stores are increasingly offering branded coco peat products targeted at urban gardeners and landscaping customers. E-commerce platforms are emerging as one of the fastest-growing distribution channels due to rising DIY gardening and home cultivation trends. Manufacturers are also strengthening OEM and private-label supply agreements with global gardening brands and hydroponic equipment suppliers to expand international market penetration.

End-User Insights

Commercial greenhouses remain the largest end-user segment, accounting for approximately 31% of global market consumption in 2025. Greenhouse vegetable production requires stable and water-efficient growing substrates capable of supporting high crop productivity under controlled conditions. Hydroponic farms are experiencing the fastest growth due to increasing investments in indoor farming and vertical agriculture. Commercial nurseries continue to represent a significant demand center because coco peat improves seed germination and root development. Home gardening is witnessing strong expansion globally due to urban gardening trends and increasing interest in organic food cultivation. Cannabis growers are also emerging as high-value end users requiring premium buffered coco peat products for controlled cultivation systems.

Crop Type Insights

Fruits and vegetables account for approximately 44% of global coco peat consumption due to extensive greenhouse cultivation of tomatoes, cucumbers, peppers, lettuce, and berries. Floriculture remains another important crop segment, particularly in export-oriented flower-producing countries such as Kenya, the Netherlands, and Colombia. Herbs and spices cultivated in hydroponic systems are increasingly utilizing coco peat substrates due to superior moisture control. Cannabis cultivation represents one of the fastest-growing specialty crop applications globally, particularly in North America and Europe where legal cultivation infrastructure continues to expand. Forestry nurseries and plantation crops also contribute to market demand through large-scale propagation activities.

Explore more data points, trends and opportunities Download Free Sample Report

Coco Peat Market Segmentations

By Product Form

- Coco Peat Blocks

- Coco Peat Briquettes

- Loose Coco Peat

- Coco Peat Grow Bags

- Coco Peat Discs & Pellets

- Buffered Coco Peat

- Washed Coco Peat

By Material Composition

- 100% Coco Peat

- Coco Peat + Coco Chips Blends

- Coco Peat + Perlite Blends

- Coco Peat + Vermiculite Blends

- Customized Hydroponic Substrate Blends

By Application

- Horticulture

- Agriculture

- Hydroponics & Controlled Environment Agriculture

- Home Gardening

- Landscaping

- Mushroom Cultivation

- Animal Bedding

- Soil Conditioning

By Crop Type

- Fruits & Vegetables

- Flowers & Floriculture Crops

- Ornamental Plants

- Cannabis Cultivation

- Herbs & Spices

- Forestry & Nursery Crops

By Distribution Channel

- Direct B2B Sales

- Agricultural Input Dealers

- Garden Centers & Retail Stores

- E-commerce Platforms

- Bulk Export Traders

- OEM & Private Label Supply

Regional Insights

North America

North America accounts for nearly 18% of the global coco peat market, driven primarily by hydroponics, greenhouse cultivation, and cannabis farming. The United States dominates regional demand due to increasing investments in indoor farming and controlled-environment agriculture. Commercial greenhouse operators increasingly prefer low-EC and buffered coco peat products for high-value crop cultivation. Canada is among the fastest-growing markets owing to legal cannabis cultivation and expanding greenhouse vegetable production. The region also benefits from strong retail gardening demand and rising adoption of sustainable growing media.

Europe

Europe represents approximately 27% of global market demand and remains one of the fastest-growing consumption regions. The Netherlands leads regional demand due to its highly advanced greenhouse horticulture industry and export-oriented vegetable production systems. Germany, the United Kingdom, Spain, France, and Italy are major consumers of peat-free growing substrates. Regulatory pressure against peat extraction and increasing environmental awareness are accelerating adoption of coco peat products across commercial horticulture and retail gardening sectors. Hydroponics and vertical farming investments are also contributing to premium substrate demand throughout the region.

Asia-Pacific

Asia-Pacific dominates the global coco peat market with approximately 46% market share, supported by abundant coconut production and established coir processing infrastructure. India remains the world’s largest producer and exporter of coco peat, particularly through processing hubs in Tamil Nadu and Kerala. Sri Lanka is recognized for premium buffered substrate exports serving hydroponic and greenhouse applications. China is witnessing rising demand from greenhouse vegetable production and indoor farming initiatives. Southeast Asian countries including Indonesia, Vietnam, and the Philippines are expanding processing capacity to strengthen export competitiveness and capture rising international demand.

Latin America

Latin America is gradually emerging as a growing market for coco peat products, led by Mexico, Brazil, Chile, and Colombia. Mexico is witnessing increasing demand from greenhouse vegetable exports to North America, while Brazil’s expanding horticulture and landscaping sectors are contributing to broader market growth. Commercial berry cultivation and floriculture projects across the region are also supporting substrate demand. Although the market remains smaller than Europe and North America, increasing adoption of greenhouse cultivation technologies is expected to support long-term growth.

Middle East & Africa

The Middle East & Africa region is expected to register one of the highest growth rates globally during the forecast period. Countries such as the UAE and Saudi Arabia are heavily investing in greenhouse agriculture and hydroponics to improve food security and reduce dependence on imports. Water scarcity concerns are encouraging adoption of moisture-efficient substrates such as coco peat. Kenya and Morocco remain important horticulture hubs supporting export-oriented flower and vegetable cultivation. South Africa also contributes significantly to regional demand through commercial greenhouse farming and landscaping applications.

Key Players in the Coco Peat Market

- Dutch Plantin

- Cocogreen

- Pelemix

- Jiffy Group

- FibreDust LLC

- Sri Ram Coir Mills

- Sai Cocopeat Exports

- Kumaran Fibres

- SMS Exports

- Coco Coir Global

- Growell Products

- Vaighai Agro Products

- Riococo

- Benlion Coir Industry

- Ceilan Coir Products