Plant Based Food Market Size

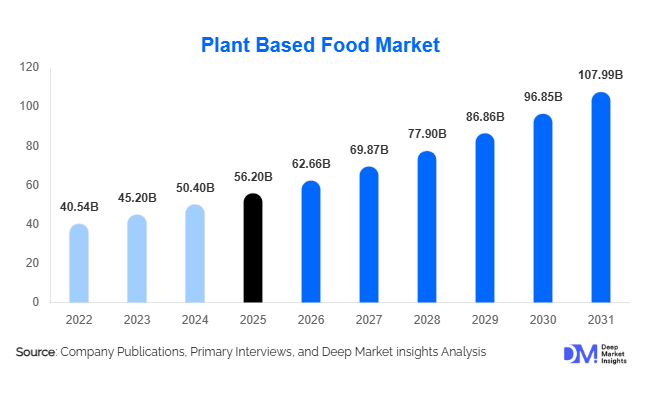

According to Deep Market Insights, the global plant based food market size was valued at USD 56.2 billion in 2025 and is projected to grow from USD 62.66 billion in 2026 to reach USD 107.99 billion by 2031, expanding at a CAGR of 11.5% during the forecast period (2026–2031). The plant based food market growth is primarily driven by rising consumer preference for sustainable nutrition, growing flexitarian and vegan populations, increasing lactose intolerance prevalence, and continuous innovation in dairy and meat alternative products. Expanding retail penetration, foodservice adoption, and advancements in protein formulation technologies are also accelerating global market expansion.

Key Market Insights

- Plant-based dairy alternatives remain the largest product category, led by oat milk, almond milk, and soy-based beverages with strong household penetration globally.

- Flexitarian consumption trends are reshaping mainstream food demand, with consumers increasingly reducing animal protein intake without fully adopting vegan diets.

- North America dominates the global market, supported by advanced retail infrastructure, innovation-led competition, and high consumer awareness.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable incomes, and expanding demand for sustainable nutrition in China and India.

- Foodservice and quick-service restaurant adoption is accelerating, with global chains expanding plant-based menu offerings across burgers, beverages, and ready meals.

- Technological innovation in extrusion, fermentation, and protein processing is significantly improving taste, texture, and nutritional functionality.

Plant Based Food Market Latest Trends

Clean-Label and Functional Nutrition Products Gaining Momentum

Consumers are increasingly prioritizing clean-label and nutritionally enhanced plant-based foods. Manufacturers are reformulating products with shorter ingredient lists, reduced additives, and improved protein quality to address consumer concerns regarding ultra-processed foods. Functional ingredients such as probiotics, omega fatty acids, adaptogens, vitamins, and high-protein blends are becoming central to product differentiation. Plant-based beverages fortified with calcium, B12, and digestive health ingredients are witnessing strong retail demand. Sports nutrition and active lifestyle consumers are also driving growth for protein-rich plant-based shakes and recovery beverages. This trend is encouraging manufacturers to integrate wellness positioning into mainstream product portfolios while strengthening premium pricing opportunities.

Expansion of Alternative Protein Technologies

Technological innovation is transforming the plant based food industry. Precision fermentation, AI-assisted formulation, extrusion processing, and advanced ingredient blending technologies are improving flavor replication, texture consistency, and shelf stability. Manufacturers are increasingly diversifying beyond soy into pea protein, fava bean protein, chickpea protein, and mycoprotein ingredients to improve allergen profiles and nutritional functionality. Hybrid formulations combining fermentation-derived ingredients with plant proteins are also emerging across dairy and meat substitute categories. These innovations are helping companies expand into mainstream retail and foodservice channels while improving repeat consumer purchases and product affordability.

Plant Based Food Market Drivers

Rising Global Demand for Sustainable Nutrition

Growing environmental awareness is significantly accelerating adoption of plant-based foods globally. Consumers are increasingly recognizing the environmental impact associated with livestock farming, including greenhouse gas emissions, land degradation, and water consumption. Governments, retailers, and foodservice chains are incorporating sustainability goals into procurement strategies, creating favorable conditions for plant-based food adoption. Major restaurant chains and supermarkets are expanding sustainable product portfolios to meet changing consumer preferences. Younger demographics, particularly millennials and Gen Z consumers, are strongly influencing this transition toward low-carbon food systems and ethical consumption patterns.

Rapid Growth of Flexitarian and Health-Conscious Consumers

The rise of flexitarian diets has expanded the addressable market far beyond traditional vegan consumers. Consumers are increasingly reducing meat and dairy intake due to health concerns related to cholesterol, obesity, and digestive issues while still maintaining occasional animal protein consumption. Plant-based foods are benefiting from strong health positioning linked to heart health, weight management, and digestive wellness. Rising lactose intolerance prevalence globally is also driving demand for dairy alternatives such as oat milk, almond milk, and coconut milk. Improved taste profiles and broader retail availability are further encouraging mainstream adoption across multiple demographics.

Plant Based Food Market Restraints

Premium Product Pricing and Affordability Challenges

Plant-based food products continue to face pricing disadvantages compared to conventional meat and dairy products. High ingredient processing costs, specialized manufacturing requirements, and premium brand positioning contribute to elevated retail prices. This remains a significant challenge in price-sensitive emerging markets where conventional protein sources remain more affordable. Inflationary pressure and agricultural commodity volatility are also increasing operational costs for manufacturers. Achieving large-scale manufacturing efficiencies and stronger supply chain integration will remain essential for improving affordability and expanding mass-market penetration.

Consumer Concerns Regarding Ultra-Processed Foods

Some consumers remain skeptical regarding heavily processed plant-based meat products containing stabilizers, additives, and artificial flavoring agents. This perception has slowed growth in certain mature markets where consumers increasingly prefer minimally processed foods and transparent ingredient sourcing. Regulatory debates surrounding labeling standards and nutritional claims are also creating market complexity. Manufacturers are therefore focusing heavily on cleaner formulations, simplified ingredient lists, and improved nutritional transparency to address evolving consumer expectations and strengthen long-term market credibility.

Plant Based Food Industry Key Opportunities

Expansion in Emerging Economies

Emerging markets across Asia-Pacific, Latin America, and the Middle East present substantial growth opportunities for plant-based food manufacturers. Urbanization, rising middle-class incomes, and expanding organized retail infrastructure are increasing demand for affordable alternative proteins. Countries such as China, India, Brazil, and the UAE are witnessing stronger consumer awareness regarding health and sustainability while governments are increasingly supporting food security and sustainable agriculture initiatives. Companies localizing flavors, leveraging regional crop sources, and introducing value-oriented product lines are expected to gain significant competitive advantages in these high-growth markets.

Foodservice and Institutional Adoption

Foodservice, institutional catering, and quick-service restaurant channels are creating major expansion opportunities for plant-based foods. Restaurants, cafés, schools, hospitals, and corporate cafeterias are incorporating plant-based menu options to align with sustainability targets and evolving dietary preferences. Large foodservice operators are increasingly partnering with alternative protein brands to diversify menus and attract younger consumers. Institutional adoption also supports long-term volume growth through stable procurement contracts. The integration of plant-based foods into school meal programs and corporate wellness initiatives is expected to strengthen mainstream consumption globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 56.20 Billion |

| Market Size in 2026 | USD 62.66 Billion |

| Market Size in 2031 | USD 107.99 Billion |

| CAGR | 11.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Plant-based dairy alternatives dominate the global market, accounting for nearly 38% of total industry revenues in 2025. Oat milk and almond milk remain particularly popular due to strong café adoption, broad retail availability, and favorable taste profiles. Plant-based meat alternatives represent the second-largest category, led by burgers, patties, nuggets, and poultry substitutes. Manufacturers are increasingly focusing on seafood alternatives and hybrid protein formulations to expand category diversity. Plant-based snacks, frozen meals, and ready-to-drink functional beverages are also witnessing rapid growth as consumers seek convenient and health-oriented food solutions. Premium and fortified products continue to command higher margins due to strong consumer willingness to pay for sustainability, nutrition, and clean-label positioning.

Source Insights

Soy remains the dominant protein source within the global plant based food market, accounting for approximately 31% of total market demand due to its strong protein functionality, cost efficiency, and established supply chain infrastructure. However, pea protein is emerging as the fastest-growing ingredient category because of its allergen-friendly positioning and clean-label appeal. Oat-based ingredients are expanding rapidly in dairy alternatives, particularly across North America and Europe. Emerging ingredients such as chickpea protein, fava bean protein, and mycoprotein are gaining traction among manufacturers seeking differentiated formulations with improved texture and nutritional performance. Ingredient diversification is also helping companies reduce dependence on soy while addressing sustainability and supply chain resilience objectives.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channels, contributing nearly 44% of global sales due to extensive shelf visibility, promotional campaigns, and strong consumer accessibility. Retailers are increasingly introducing private-label plant-based products to improve affordability and category penetration. Online retail and direct-to-consumer platforms are witnessing strong growth, particularly for premium nutrition products, subscription-based meal kits, and functional beverages. Foodservice distribution channels are also expanding rapidly as restaurants, cafés, and institutional catering providers broaden plant-based menu offerings. Digital marketing, influencer campaigns, and social media engagement are playing an increasingly important role in shaping consumer purchasing decisions across younger demographics.

End-Use Insights

Household retail consumption remains the dominant end-use segment, accounting for more than 52% of total global demand in 2025. Consumers are increasingly incorporating plant-based dairy, snacks, beverages, and frozen meals into everyday diets. Foodservice and HoReCa applications are among the fastest-growing segments, supported by growing restaurant adoption and consumer demand for plant-forward dining experiences. Institutional consumption across schools, hospitals, and corporate cafeterias is also increasing due to sustainability-focused procurement strategies and dietary diversification initiatives. Sports nutrition and clinical nutrition applications are emerging as high-growth end-use areas, particularly for fortified beverages and protein supplements targeting active lifestyle consumers.

Price Positioning Insights

Premium plant-based products currently dominate the market, accounting for approximately 46% of global revenues due to strong demand for clean-label, organic, and functional nutrition products. Consumers in developed markets are willing to pay premium prices for sustainability-focused and nutritionally enhanced offerings. Mid-range products are expected to witness the fastest growth over the forecast period as manufacturers increasingly focus on affordability and mass-market expansion. Economy-positioned products are gradually expanding in emerging economies through private-label retail offerings and localized manufacturing strategies aimed at improving accessibility among price-sensitive consumers.

Explore more data points, trends and opportunities Download Free Sample Report

Plant Based Food Market Segmentations

By Product Type

- Plant-Based Dairy Alternatives

- Plant-Based Meat Alternatives

- Plant-Based Egg Alternatives

- Plant-Based Bakery & Confectionery

- Plant-Based Snacks & Convenience Foods

- Plant-Based Beverages

- Plant-Based Nutritional Ingredients

By Source

- Soy

- Pea

- Wheat

- Oat

- Almond

- Coconut

- Rice

- Chickpea

- Fava Bean

- Mycoprotein

- Mixed Plant Proteins

By Nature

- Conventional

- Organic

- Non-GMO Certified

- Clean-Label Formulations

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health Stores

- Online Retail & Direct-to-Consumer

- Foodservice Distribution

- Institutional Sales

- Club Stores & Wholesale Retail

By End Use

- Household Retail Consumption

- Foodservice & HoReCa

- Institutional Consumption

- Food Manufacturing & Ingredient Processing

- Sports & Clinical Nutrition

Regional Insights

North America

North America remains the largest regional market, accounting for nearly 35% of global market share in 2025. The United States dominates regional demand due to strong consumer awareness, large flexitarian populations, extensive supermarket penetration, and high levels of innovation in dairy and meat alternatives. Canada is also emerging as a major producer of plant proteins and sustainable food ingredients supported by government investments in agricultural processing and alternative protein manufacturing infrastructure.

Europe

Europe represents approximately 29% of global market share and remains one of the most mature plant-based food markets globally. Germany, the United Kingdom, and the Netherlands are key growth centers due to strong sustainability awareness, vegan product adoption, and supportive environmental regulations. Oat milk, vegan bakery products, and plant-based ready meals are experiencing particularly strong demand across the region. European consumers are also highly receptive to organic, non-GMO, and clean-label formulations.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, forecast to expand at nearly 14% CAGR during 2026–2031. China is emerging as a major demand center due to increasing health awareness, food security initiatives, and government interest in sustainable protein systems. India benefits from a large vegetarian population and rising urban incomes, while Japan and South Korea are witnessing growing demand for functional nutrition and premium plant-based beverages. Singapore continues to position itself as a leading innovation hub for alternative proteins and food technology development.

Latin America

Latin America is witnessing steady growth led by Brazil and Mexico. Strong agricultural resources, rising environmental awareness, and increasing retail penetration are supporting market development across the region. Brazilian manufacturers are increasingly leveraging soy and pea proteins to produce cost-efficient alternatives targeted at domestic and export markets. Growing middle-class demand for healthier food options is further strengthening long-term growth potential.

Middle East & Africa

The Middle East and Africa region currently represents a smaller share of the global market but is showing accelerating adoption in premium urban centers such as Dubai, Riyadh, and Tel Aviv. The UAE is witnessing increasing demand for imported premium vegan products driven by affluent consumers and hospitality sector expansion. Israel remains a leading innovation ecosystem for food technology and alternative protein startups, while South Africa is emerging as a regional growth center for plant-based retail products.

Key Players in the Plant Based Food Market

- Nestlé S.A.

- Danone S.A.

- Beyond Meat Inc.

- Impossible Foods Inc.

- Oatly Group AB

- Unilever PLC

- The Hain Celestial Group

- Conagra Brands Inc.

- Maple Leaf Foods Inc.

- Tyson Foods Inc.

- Kerry Group plc

- SunOpta Inc.

- Amy’s Kitchen Inc.

- Eat Just Inc.

- Kellogg Company