Insect Protein Market Size

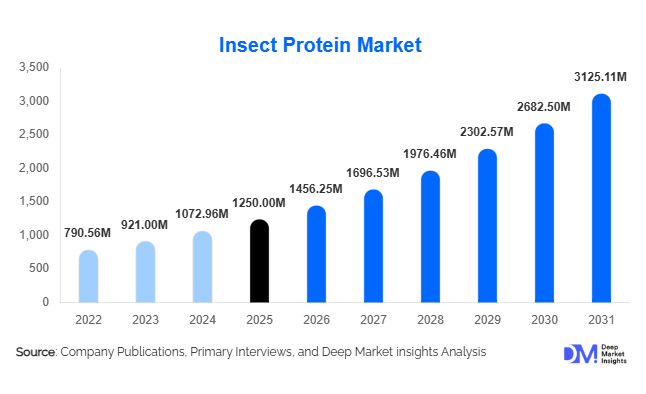

According to Deep Market Insights, the global insect protein market size was valued at USD 1,250 million in 2025 and is projected to grow from USD 1,456.25 million in 2026 to reach approximately USD 3,125.11 million by 2031, expanding at a CAGR of 16.5% during the forecast period (2026–2031). The insect protein market growth is primarily driven by rising demand for sustainable alternative proteins, increasing substitution of fishmeal and soybean meal in aquaculture and livestock feed, and expanding applications in premium pet food and functional nutrition.

Insect protein, particularly from Black Soldier Fly (BSF) and mealworms, is gaining traction as a low-carbon, resource-efficient protein source. Growing regulatory approvals across the European Union and commercialization efforts in the United States and China are accelerating large-scale production capacity. Strong investor interest, automation in insect farming, and integration with circular economy waste management models are further strengthening long-term market prospects.

Key Market Insights

- Animal feed accounts for nearly 68% of total demand in 2025, led by aquaculture and poultry feed substitution.

- Black Soldier Fly dominates with approximately 48% market share, driven by scalability and high feed conversion efficiency.

- Europe holds around 35% of the global market share, supported by progressive feed regulations and sustainability mandates.

- Asia-Pacific is the fastest-growing region, expanding at nearly 19% CAGR due to aquaculture expansion in China, Vietnam, and Thailand.

- The top five companies collectively account for about 52% of global revenue, reflecting moderate consolidation.

- Controlled-environment industrial farms represent over 55% of global production, driven by automation and yield optimization.

What are the latest trends in the insect protein market?

Fishmeal Replacement in Aquaculture

One of the most significant trends in the insect protein market is the accelerated replacement of fishmeal in aquaculture feed. Rising volatility in fishmeal supply due to climate events and overfishing has pushed feed manufacturers to diversify protein sources. Black Soldier Fly meal provides comparable amino acid profiles and digestibility levels, making it a strong alternative. Long-term supply agreements between insect protein producers and global aquafeed manufacturers are increasing revenue visibility and supporting industrial-scale expansion.

Automation and AI-Driven Farming

Industrial insect farming is rapidly adopting robotics, AI-based monitoring systems, and climate-controlled vertical farming models. Automated larval harvesting, feed optimization algorithms, and real-time biomass monitoring are improving yield efficiency and reducing mortality rates. These advancements are helping reduce production costs, improve consistency, and scale output to meet rising demand from the feed and pet food industries.

What are the key drivers in the insect protein market?

Rising Demand for Sustainable Protein

Global pressure to reduce greenhouse gas emissions and land usage in agriculture is accelerating the adoption of low-impact protein alternatives. Insect protein requires significantly less water, land, and feed compared to soy and livestock-based protein, aligning with ESG investment frameworks and corporate sustainability commitments.

Growth of Premium Pet Food Industry

The global pet food industry, valued at over USD 120 billion, is increasingly incorporating insect-based formulations due to hypoallergenic benefits and sustainability branding. Pet humanization trends in North America and Europe are fueling the rapid expansion of insect-based premium and specialty pet diets.

What are the restraints for the global market?

High Production and Energy Costs

Despite technological progress, insect protein production remains capital-intensive. Climate-controlled facilities, automated systems, and biosecurity protocols increase operational expenditure. Current pricing ranges between USD 2,000 and USD 4,500 per metric ton, higher than conventional soybean meal in many regions.

Consumer Perception Barriers

While acceptance in animal feed is strong, direct human consumption of insect protein faces cultural resistance in Western markets. Marketing strategies and regulatory clarity are required to normalize edible insect products for mainstream consumers.

What are the key opportunities in the insect protein industry?

Circular Economy Integration

Insect farming can convert food waste and agricultural by-products into high-value protein and organic fertilizer (frass). Governments promoting zero-waste policies are supporting insect farming through grants and policy incentives. Industrial symbiosis models between food processors and insect farms present strong cost and ESG advantages.

Emerging Human Nutrition Applications

Functional foods, protein bars, and meat alternatives incorporating insect protein are gaining traction. As regulatory approvals expand and consumer education improves, the human food segment is expected to grow at over 20% CAGR, albeit from a smaller base.

Product Type Insights

Insect meal remains the leading product type, accounting for approximately 42% of total revenue in 2025, primarily due to its direct compatibility with existing aquaculture and poultry feed formulations. The dominance of insect meal is driven by its high protein content (45–65%), balanced amino acid profile, and ease of integration into compound feed without significant formulation changes. Aquafeed manufacturers prefer insect meal, especially Black Soldier Fly (BSF) meal, because it provides a viable substitute for fishmeal while maintaining growth performance and feed conversion ratios. Additionally, regulatory approvals in Europe and North America for insect meal inclusion in poultry and swine feed have strengthened demand visibility and supported long-term procurement contracts.

Protein powders and concentrates are gaining momentum in premium pet food and functional nutrition applications, particularly in hypoallergenic and limited-ingredient diets. Insect oil and lipids represent an emerging high-margin segment, particularly in aquafeed, where lauric acid-rich BSF oil enhances gut health and disease resistance. Frass, the nutrient-rich by-product, is expanding within organic agriculture markets due to rising demand for bio-based fertilizers and soil conditioners aligned with regenerative farming practices.

Application Insights

Animal feed continues to dominate the market with nearly 68% share of total demand in 2025, supported primarily by aquaculture, which alone accounts for approximately 40% of overall insect protein consumption. The leading driver for this segment is the structural shortage and price volatility of fishmeal, coupled with sustainability mandates among global seafood producers. Insect protein offers traceability, lower environmental footprint, and consistent supply, making it attractive to integrated aquaculture operators.

Poultry feed is the second-largest contributor to animal feed, benefiting from increasing protein requirements in intensive farming systems. Human food applications, while still under 15% of total market share, are expanding at over 20% CAGR due to rising interest in alternative proteins, sports nutrition, and sustainable snack formulations. Agricultural biofertilizers derived from insect frass are witnessing strong uptake in organic farming systems, where growers seek natural soil amendments that enhance microbial activity and nutrient absorption.

Production Technology Insights

Controlled-environment industrial farms account for roughly 55% of global production capacity, making them the leading production model. Their dominance is driven by scalability, biosecurity control, and yield optimization through automation and AI-enabled monitoring systems. These facilities ensure consistent temperature, humidity, and feedstock management, reducing mortality rates and improving protein output per square meter.

Modular and substrate-based rearing systems are particularly prominent in the Asia-Pacific due to lower capital expenditure requirements and access to abundant agricultural by-products. These decentralized systems enable cost-efficient production while supporting circular economy initiatives. However, industrial-scale vertical farming remains the preferred model in Europe and North America, where regulatory compliance and quality consistency are critical for feed certification.

End-Use Industry Insights

The aquaculture industry remains the largest end-use segment, underpinned by global fish production exceeding 90 million metric tons annually. Demand for insect protein in aquaculture is expanding at nearly 18% CAGR as producers aim to reduce reliance on marine-derived feed inputs. Salmon, trout, and shrimp farming operations are leading adopters due to export-driven sustainability requirements and retailer pressure for environmentally responsible sourcing.

The pet food industry represents the fastest-growing end-use segment, driven by premiumization and pet humanization trends. Insect-based formulations are positioned as sustainable, hypoallergenic alternatives in high-end dog and cat food categories. Emerging end-use applications include sports nutrition powders, nutraceutical capsules, and meat analogue products, particularly in European markets where regulatory pathways for novel foods are clearer. Export-driven demand remains strong in Europe, where insect meal is increasingly incorporated into salmonid feed destined for global seafood markets.

| By Species Type | By Product Type | By Application | By Production Technology | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Europe

Europe accounts for approximately 35% of the global market share in 2025, making it the largest regional market. Growth is primarily driven by progressive feed legislation permitting insect protein inclusion in aquaculture, poultry, and swine diets. France, the Netherlands, and Germany lead both production and consumption due to strong regulatory frameworks, sustainability mandates, and significant investment in automated insect farming facilities. The region’s advanced aquaculture sector, particularly salmon farming in Northern Europe, creates a stable demand for fishmeal substitutes. Additionally, ESG-focused investors and government grants supporting circular economy initiatives further stimulate regional expansion.

North America

North America holds nearly 28% of the global market share, led by the United States, which dominates regional consumption due to rapid growth in premium pet food and expanding aquaculture operations. The primary driver in this region is strong consumer acceptance of sustainable pet nutrition and increasing venture capital investment in alternative proteins. Canada is emerging as a production hub, supported by government-backed agri-tech funding and proximity to major aquaculture markets. Regulatory clarity from feed authorities is also accelerating commercialization.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at approximately 19% CAGR, driven by its vast aquaculture and shrimp farming industries. China dominates regional demand due to its large-scale fish and shrimp production, while Vietnam and Thailand are integrating insect meal into export-oriented aquafeed formulations. The key growth driver is the region’s need for feed cost optimization and protein security amid fluctuating soybean and fishmeal imports. Additionally, abundant agricultural waste availability supports cost-efficient insect farming models.

Latin America

Brazil and Mexico represent emerging growth markets, primarily driven by poultry and aquaculture exports. The main driver in this region is feed cost volatility and dependency on imported soybean meal. As exporters face sustainability compliance requirements from North American and European buyers, insect protein adoption is gradually increasing as a differentiation strategy.

Middle East & Africa

Growth in the Middle East & Africa is moderate but rising, particularly in aquaculture-intensive economies such as South Africa and the UAE. The primary driver is feed self-sufficiency and food security initiatives aimed at reducing import dependency. Governments in arid regions are exploring insect farming as a water-efficient protein source. In Africa, the availability of organic waste streams and increasing investment in agri-tech solutions are expected to support long-term capacity development.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Insect Protein Market

- Ÿnsect

- Protix

- InnovaFeed

- Enterra Feed Corporation

- AgriProtein

- Entobel

- Beta Hatch

- Hexafly

- EnviroFlight

- NextProtein

- Chapul Farms

- Aspire Food Group

- Protenga

- Insectta

- Entomo Farms