Vegan Vanilla Milk Market Size

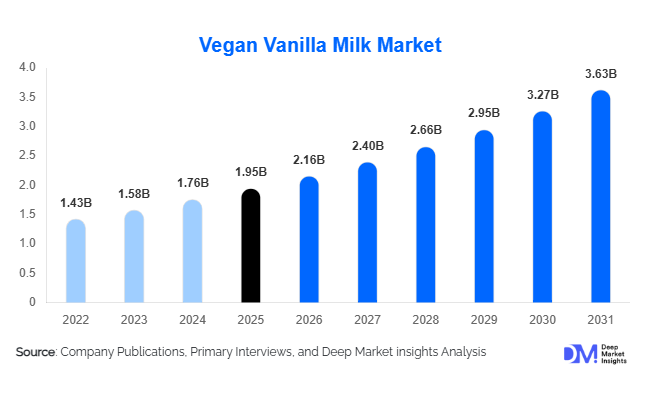

According to Deep Market Insights, the global vegan vanilla milk market size was valued at USD 1.95 billion in 2025 and is projected to grow from USD 2.16 billion in 2026 to reach USD 3.63 billion by 2031, expanding at a CAGR of 10.9% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer preference for plant-based nutrition, increasing prevalence of lactose intolerance and dairy allergies, and growing demand for flavored dairy alternatives that align with sustainability and clean-label consumption trends. Vegan vanilla milk has evolved from a niche offering for vegan consumers into a mainstream beverage category adopted by flexitarians, health-conscious consumers, and environmentally aware millennials and Gen Z populations. Product innovation in oat, almond, pea, and blended plant-based formulations, coupled with increasing penetration across retail and foodservice channels, is expected to sustain robust market growth during the forecast period.

Key Market Insights

- Almond-based vegan vanilla milk remains the leading product category, accounting for nearly 34% of global market revenue due to its established consumer acceptance and wide retail availability.

- Functional and fortified vegan vanilla milk products are rapidly gaining traction, supported by demand for high-protein, calcium-enriched, and probiotic formulations.

- North America dominates the global market, accounting for approximately 33% of global revenues, driven by high plant-based food penetration and strong consumer awareness.

- Asia-Pacific is the fastest-growing regional market, fueled by increasing disposable incomes, urbanization, and rising lactose intolerance rates across China and India.

- Foodservice and coffee chains are becoming major demand generators, with vegan vanilla milk increasingly incorporated into specialty coffee beverages and smoothies.

- Technological innovation in flavor systems and plant protein processing is improving taste, texture, and nutritional profiles, broadening mainstream consumer adoption.

Vegan Vanilla Milk Market Latest Trends

Functional and Fortified Plant-Based Milk Gaining Popularity

Consumers increasingly expect beverages to deliver functional health benefits beyond basic nutrition. As a result, manufacturers are introducing vegan vanilla milk products enriched with calcium, vitamin D, omega-3 fatty acids, probiotics, and plant proteins. High-protein variants targeting sports nutrition and healthy aging segments are witnessing particularly strong growth. Premium fortified products are commanding higher price points and creating opportunities for product differentiation in an increasingly competitive marketplace. Functional claims related to digestive health, immunity enhancement, and bone health are becoming major purchasing factors, particularly among millennials and older consumers.

Premiumization and Clean-Label Innovation

Premium vegan vanilla milk products featuring organic ingredients, natural vanilla bean extracts, and minimal ingredient lists are becoming increasingly popular globally. Consumers are scrutinizing ingredient labels more closely and actively seeking products that avoid artificial additives, preservatives, and excessive sugar content. Manufacturers are responding by introducing clean-label and organic formulations that offer superior taste and nutritional positioning. Sustainability claims, recyclable packaging, and carbon footprint reduction initiatives are also emerging as important product differentiators within premium segments.

Vegan Vanilla Milk Market Drivers

Increasing Prevalence of Lactose Intolerance and Dairy Allergies

Rising rates of lactose intolerance worldwide are significantly supporting demand for plant-based dairy alternatives. More than half of the global adult population experiences some level of lactose malabsorption, making dairy-free beverages increasingly attractive. Vegan vanilla milk provides a flavorful alternative that replicates many of the sensory characteristics of traditional flavored dairy milk while avoiding digestive concerns associated with lactose consumption.

Growing Consumer Preference for Sustainable and Ethical Foods

Environmental concerns surrounding conventional dairy production are accelerating consumer migration toward plant-based products. Vegan vanilla milk generally requires lower water consumption and generates lower greenhouse gas emissions compared with dairy milk production. Younger consumers, particularly millennials and Gen Z, increasingly consider sustainability and ethical sourcing when making purchasing decisions, driving long-term demand for plant-based beverages.

Rapid Expansion of Plant-Based Product Innovation

Advancements in processing technologies and ingredient formulations have significantly improved the taste and texture of vegan vanilla milk. Manufacturers are investing heavily in enzyme technologies, emulsification systems, and protein extraction techniques to produce products with creamier textures and superior nutritional profiles. Product innovation is also extending into barista formulations, sugar-reduced offerings, and premium vanilla bean varieties, supporting broader market adoption.

Vegan Vanilla Milk Market Restraints

Premium Product Pricing

Despite strong growth prospects, vegan vanilla milk products remain substantially more expensive than conventional dairy milk in many markets. Higher raw material costs, smaller production scales, and premium ingredient sourcing contribute to elevated retail pricing, limiting accessibility among price-sensitive consumers and emerging market populations.

Regulatory and Labeling Challenges

Several countries have implemented or proposed regulations restricting the use of dairy-related terminology for plant-based products. Such regulations create marketing complexities and increase compliance costs for manufacturers. Regulatory uncertainty may also hinder product positioning strategies and create barriers to market expansion in certain jurisdictions.

Vegan Vanilla Milk Industry Key Opportunities

Expansion in Emerging Economies

Asia-Pacific, the Middle East, and Latin America remain significantly underpenetrated markets for vegan vanilla milk. Rising disposable incomes, increasing health awareness, and rapid urbanization are creating favorable conditions for plant-based beverage consumption. Countries including China, India, Indonesia, Brazil, and the UAE are witnessing double-digit growth in plant-based food categories, creating substantial opportunities for both multinational companies and local manufacturers. Establishing regional manufacturing facilities and localized product offerings will likely become a key strategy for market participants.

Foodservice and Café Integration

Coffee shops and quick-service restaurants are increasingly incorporating vegan vanilla milk into specialty beverages, smoothies, and desserts. The global café industry continues to expand rapidly, creating significant opportunities for long-term supply partnerships. Barista-grade formulations designed specifically for frothing and coffee applications are becoming a major premium segment, enabling manufacturers to establish recurring demand streams and improve economies of scale.

Functional Nutrition and Personalized Wellness Products

The growing functional nutrition industry presents substantial opportunities for manufacturers to introduce customized vegan vanilla milk products targeting specific health needs. Products designed for sports nutrition, digestive health, pediatric nutrition, and healthy aging can command premium pricing and achieve higher profit margins. Personalized nutrition trends and increasing demand for clean-label fortified products are expected to create new avenues for innovation and category expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.95 Billion |

| Market Size in 2026 | USD 2.16 Billion |

| Market Size in 2031 | USD 3.63 Billion |

| CAGR | 10.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Type Insights

The almond-based segment dominated the global vegan vanilla milk market in 2025 and accounted for approximately 34% of total revenue. The segment's leadership is primarily attributed to strong consumer familiarity, mild flavor characteristics, broad retail availability, and its established position within the plant-based dairy category. Almond milk has benefited significantly from early market penetration and extensive product innovation by leading manufacturers, resulting in high brand recognition and consumer trust. Furthermore, its versatility across multiple applications, including direct consumption, coffee beverages, cereals, smoothies, and desserts, continues to reinforce its dominant market position.Soy-based vegan vanilla milk continues to maintain a significant share of the global market owing to its superior protein profile, nutritional value, and affordability. The segment remains highly attractive among consumers seeking functional dairy alternatives that provide enhanced protein intake without compromising taste or cost competitiveness. Soy milk also enjoys strong consumer acceptance in Asian markets where soy-based beverages have long-standing cultural and dietary significance.Pea protein-based vegan vanilla milk is emerging as a premium and high-growth category due to its excellent nutritional profile, allergen-friendly positioning, and suitability for sports nutrition and functional beverage applications. Manufacturers are increasingly incorporating pea protein into premium formulations to address consumer demand for higher protein content and clean-label ingredients. Meanwhile, blended plant-based formulations combining almonds, oats, soy, coconut, and pea proteins are gaining traction as companies seek to optimize taste, texture, nutritional performance, and cost efficiency while differentiating their product portfolios.

Product Formulation Insights

Sweetened vegan vanilla milk represented nearly 46% of global revenues in 2025, making it the leading formulation segment. The segment's dominance is largely supported by strong consumer preference for indulgent flavors and enhanced palatability, particularly among younger demographics and first-time plant-based beverage consumers. Sweetened formulations are widely utilized in flavored beverages, coffee preparations, desserts, and ready-to-drink applications, further contributing to their substantial market share. The increasing availability of naturally sweetened products using ingredients such as agave, dates, and stevia is also supporting continued demand.However, unsweetened and reduced-sugar formulations are expected to witness accelerated growth throughout the forecast period as consumers increasingly prioritize healthier lifestyles, calorie management, and reduced sugar consumption. Rising awareness regarding obesity, diabetes, and metabolic health is encouraging consumers to shift toward products with cleaner nutritional profiles and minimal additives. The growing popularity of ketogenic, low-carbohydrate, and wellness-oriented diets is also contributing to increasing demand for sugar-free and low-sugar plant-based beverages.Functional and fortified vegan vanilla milk products are rapidly gaining market share as consumers increasingly seek value-added nutrition and products that deliver specific health benefits. Fortification with calcium, vitamin D, vitamin B12, omega fatty acids, probiotics, and additional protein content is becoming a major product differentiation strategy among manufacturers. The rising demand for preventive healthcare, immunity support, digestive wellness, and personalized nutrition is expected to significantly boost the adoption of premium fortified formulations over the coming years.

Packaging Insights

Carton packaging remained the dominant packaging format in 2025 and accounted for approximately 68% of global market revenues. The segment's leadership is primarily attributable to its ability to extend product shelf life without requiring refrigeration, thereby reducing transportation and storage costs across supply chains. Carton packaging also aligns with increasing consumer and regulatory emphasis on sustainability due to its lower environmental impact and high recyclability. In addition, its lightweight nature and suitability for large-scale retail distribution continue to make it the preferred packaging solution for manufacturers.PET bottles are gaining popularity, particularly within single-serve and on-the-go consumption categories. Increasing demand for convenience beverages, growing urban lifestyles, and the expansion of ready-to-drink product offerings are supporting the adoption of bottle packaging formats. Glass packaging continues to occupy a niche but important position within premium organic and artisanal product categories, where consumers often associate glass containers with superior product quality and environmental responsibility.Bulk packaging solutions are also witnessing increasing adoption across foodservice and industrial applications. Cafés, restaurants, bakeries, and beverage manufacturers are increasingly incorporating vegan vanilla milk into their operations, creating sustained demand for larger packaging formats that improve operational efficiency and reduce packaging costs.

Distribution Channel Insights

Supermarkets and hypermarkets remained the largest distribution channel in 2025, accounting for approximately 39% of global sales. The segment's leadership is driven by extensive product assortments, widespread geographical presence, and strong promotional capabilities that enable consumers to access a broad range of plant-based beverage offerings. The increasing allocation of shelf space for dairy alternatives and the expansion of private-label vegan products are further strengthening the position of modern retail channels.Online retail and direct-to-consumer distribution channels are experiencing rapid growth as digital grocery adoption continues to accelerate worldwide. Consumers increasingly value the convenience of home delivery, subscription-based purchasing models, and access to a wider variety of premium and niche products that may not be readily available in traditional retail outlets. The growing influence of e-commerce platforms and digital marketing strategies is expected to significantly enhance product accessibility and consumer engagement.Specialty health food stores continue to play a crucial role in the premium and organic segments of the market, particularly among health-conscious consumers seeking clean-label, fortified, and sustainably produced products. Meanwhile, foodservice distribution channels are expanding rapidly due to increasing demand from coffee chains, restaurants, hotels, and quick-service establishments that are introducing dairy-free menu options to cater to evolving consumer preferences.

End-Use Insights

Household consumption remained the largest end-use segment and accounted for approximately 58% of global market revenues in 2025. The segment's dominance is supported by the increasing incorporation of vegan vanilla milk into everyday dietary routines, including breakfast cereals, smoothies, coffee preparations, baking, and direct consumption. Rising health awareness, growing lactose intolerance prevalence, and increasing adoption of flexitarian dietary patterns continue to support strong household demand across both developed and emerging markets.Foodservice applications represent the fastest-growing end-use category, driven by the rapid expansion of cafés, specialty coffee chains, and restaurants that increasingly offer plant-based alternatives to conventional dairy products. The growing popularity of vegan beverages, specialty coffee preparations, and dairy-free desserts is creating significant opportunities for vegan vanilla milk suppliers within commercial foodservice operations.Ready-to-drink beverage manufacturers, bakery companies, and frozen dessert producers are also emerging as important consumers of vegan vanilla milk. The expanding use of plant-based ingredients across multiple food and beverage categories is contributing to demand diversification and strengthening the long-term growth outlook of the market.

Explore more data points, trends and opportunities Download Free Sample Report

Vegan Vanilla Milk Market Segmentations

By Source Type

- Almond Vanilla Milk

- Oat Vanilla Milk

- Soy Vanilla Milk

- Coconut Vanilla Milk

- Cashew Vanilla Milk

- Rice Vanilla Milk

- Pea Protein Vanilla Milk

- Blended Plant-Based Vanilla Milk

By Product Formulation

- Sweetened Vegan Vanilla Milk

- Unsweetened Vegan Vanilla Milk

- Reduced-Sugar Vegan Vanilla Milk

- Functional/Fortified Vegan Vanilla Milk

- Organic Vegan Vanilla Milk

- Conventional Vegan Vanilla Milk

By Packaging Type

- Carton Packaging

- PET Bottles

- Glass Bottles

- Pouches/Sachets

- Bulk Packaging

By Shelf Stability

- Ambient/Shelf-Stable Products

- Refrigerated Products

- Frozen Concentrates

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Health Food Stores

- Pharmacies and Wellness Stores

- Online Retail/E-commerce

- Direct-to-Consumer (DTC)

- Foodservice Distribution

Regional Insights

North America

North America accounted for approximately 33% of global vegan vanilla milk market revenues in 2025 and remained the largest regional market. The United States contributed nearly 27% of global demand due to its highly developed plant-based food industry, increasing vegan population, and strong consumer awareness regarding health and sustainability. Canada is also witnessing robust growth supported by favorable consumer preferences toward organic and clean-label products. High retail penetration and strong foodservice adoption continue to support regional demand expansion.Regional growth is further being driven by increasing incidences of lactose intolerance, rising consumer expenditure on premium health and wellness products, extensive product innovation by leading plant-based beverage manufacturers, and the strong presence of organized retail and e-commerce channels. The growing popularity of plant-based diets among millennials and Generation Z consumers, coupled with expanding investments in alternative protein production and supportive environmental sustainability initiatives, is expected to sustain long-term market growth across North America.

Europe

Europe represented nearly 30% of global market revenues in 2025 and remains one of the most mature plant-based beverage markets globally. The United Kingdom, Germany, France, and the Netherlands are leading consumers of vegan vanilla milk products. Sustainability initiatives, high vegan and flexitarian populations, and strong regulatory support for plant-based foods continue to drive market growth across the region. Oat-based vanilla milk products are particularly popular among European consumers due to environmental considerations and local sourcing advantages.The region's growth is further supported by stringent environmental regulations, increasing consumer preference for sustainable and ethically sourced products, rising demand for clean-label and organic food products, and continuous product innovation by major food and beverage companies. The expansion of plant-based product offerings in supermarkets and foodservice establishments, combined with growing awareness regarding the environmental impact of dairy production, continues to strengthen market prospects throughout Europe.

Asia-Pacific

Asia-Pacific accounted for approximately 25% of global revenues and is projected to register the fastest growth throughout the forecast period. China and India are emerging as key demand centers due to increasing disposable incomes, urbanization, and growing awareness regarding lactose intolerance. Australia and Japan represent relatively mature markets with strong consumer acceptance of premium plant-based beverages. Expanding retail infrastructure and increasing investments in plant-based food manufacturing are expected to accelerate regional market growth.Additional growth drivers include rapidly changing dietary habits, increasing health consciousness among younger consumers, rising middle-class populations with higher purchasing power, and the growing influence of Western dietary trends. Government initiatives supporting food innovation, the expansion of organized retail networks, and increasing investments by domestic and international companies in alternative protein production are expected to further accelerate market penetration across the region.

Latin America

Brazil and Mexico dominate vegan vanilla milk consumption in Latin America, supported by rising health consciousness and increasing penetration of premium food products. Although market development remains at an early stage compared with North America and Europe, improving retail infrastructure and growing vegan populations are expected to support future growth opportunities.The regional market is also benefiting from increasing urbanization, rising disposable incomes, growing awareness regarding lactose intolerance and dietary wellness, and the gradual expansion of international plant-based food brands. E-commerce growth and increasing investments in modern retail channels are improving product accessibility, while the younger consumer demographic is accelerating the adoption of plant-based beverage alternatives throughout the region.

Middle East & Africa

The Middle East and Africa region remains comparatively smaller but is witnessing strong growth momentum. The UAE and Saudi Arabia are emerging as important markets due to premium food consumption patterns and increasing health awareness. South Africa represents the largest African market, benefiting from a relatively developed retail sector and increasing adoption of plant-based nutrition products among younger consumers.Regional growth is being supported by increasing prevalence of lifestyle-related health conditions, rising demand for premium imported food products, growing expatriate populations with strong preference for plant-based diets, and expanding investments in modern retail and foodservice infrastructure. Increasing awareness regarding sustainable nutrition and the gradual introduction of plant-based product portfolios by international brands are expected to create significant growth opportunities across the Middle East and Africa during the forecast period.

Key Players in the Vegan Vanilla Milk Market

- Danone

- Oatly Group AB

- Califia Farms LLC

- Blue Diamond Growers

- SunOpta Inc.

- The Hain Celestial Group Inc.

- Elmhurst 1925

- Pacific Foods

- Ripple Foods

- Vitasoy International Holdings Ltd.

- Minor Figures

- Earth's Own Food Company

- Naturli' Foods

- Alpro

- Oatside