Unsweetened Coconut Milk Market Size

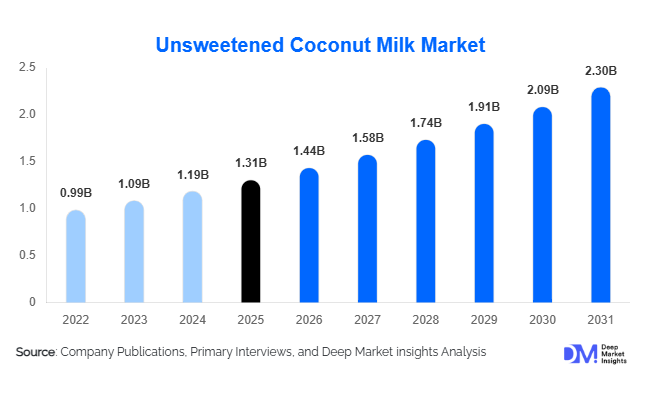

According to Deep Market Insights, the global unsweetened coconut milk market size was valued at USD 1.31 billion in 2025 and is projected to grow from USD 1.44 billion in 2026 to reach USD 2.30 billion by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The unsweetened coconut milk market growth is primarily driven by increasing consumer preference for plant-based nutrition, rising demand for sugar-free dairy alternatives, growing lactose intolerance awareness, and the expansion of vegan and flexitarian lifestyles worldwide. Food manufacturers are increasingly incorporating unsweetened coconut milk into dairy-free beverages, yogurts, frozen desserts, bakery products, and functional nutrition applications, further supporting market expansion.

Key Market Insights

- Unsweetened coconut milk is increasingly preferred over sweetened variants due to growing consumer focus on sugar reduction, weight management, and metabolic health.

- Food and beverage processing remains the largest application segment, accounting for nearly 47% of global market demand as manufacturers expand dairy-free product portfolios.

- Asia-Pacific dominates the global market, supported by abundant coconut production, established consumption patterns, and strong export-oriented manufacturing capabilities.

- North America remains a high-value consumption market, driven by strong adoption of plant-based diets and premium health-focused food products.

- Organic and fortified coconut milk products are gaining traction, as consumers increasingly seek clean-label, nutrient-enhanced, and sustainably sourced alternatives.

- Advancements in aseptic packaging and processing technologies are improving product shelf life, distribution efficiency, and global market accessibility.

Unsweetened Coconut Milk Market Latest Trends

Growth of Functional and Fortified Plant-Based Beverages

One of the most prominent trends in the unsweetened coconut milk market is the increasing development of functional and fortified formulations. Manufacturers are introducing products enriched with calcium, vitamin D, vitamin B12, probiotics, protein, and omega fatty acids to address growing consumer demand for nutrient-dense plant-based beverages. Health-conscious consumers are increasingly viewing coconut milk not only as a dairy alternative but also as a functional wellness product. This trend is particularly visible across North America and Europe, where consumers actively seek products supporting immunity, digestive health, and overall well-being. Functional coconut milk beverages are also gaining traction among athletes, fitness enthusiasts, and aging populations looking for healthier beverage alternatives.

Sustainable Packaging and Organic Product Expansion

Sustainability has become a major purchasing criterion across global food and beverage markets. Manufacturers are increasingly adopting recyclable cartons, lightweight packaging materials, and environmentally responsible sourcing programs to strengthen brand positioning. Organic-certified unsweetened coconut milk products are experiencing robust demand growth as consumers seek clean-label products free from synthetic additives and pesticides. Retailers are expanding shelf space dedicated to organic and plant-based products, while e-commerce platforms provide greater visibility for premium coconut milk brands. Sustainability certifications and transparent sourcing practices are becoming important competitive differentiators among leading manufacturers.

Unsweetened Coconut Milk Market Drivers

Rising Adoption of Plant-Based Diets

The global transition toward vegan, vegetarian, and flexitarian lifestyles continues to drive substantial demand for unsweetened coconut milk. Consumers are increasingly reducing dairy consumption due to health, environmental, and ethical concerns. Unsweetened coconut milk offers a naturally dairy-free, lactose-free, and vegan-friendly alternative that aligns with evolving dietary preferences. The rapid expansion of plant-based food categories across supermarkets, restaurants, and foodservice establishments is creating favorable conditions for long-term market growth. Growing consumer awareness regarding sustainable food choices further reinforces the adoption of coconut-based alternatives.

Increasing Focus on Sugar Reduction and Clean Labels

Consumers worldwide are actively reducing sugar intake in response to rising concerns regarding obesity, diabetes, and cardiovascular health. Unsweetened coconut milk directly benefits from this trend, as it offers a natural, low-sugar alternative to conventional flavored beverages and sweetened dairy substitutes. Public health initiatives encouraging sugar reduction and transparent nutritional labeling are accelerating demand for unsweetened formulations across both developed and emerging economies. The clean-label movement has also encouraged manufacturers to simplify ingredient lists and eliminate artificial additives, further supporting market adoption.

Unsweetened Coconut Milk Market Restraints

Volatility in Coconut Supply and Raw Material Pricing

The market remains highly dependent on coconut cultivation concentrated across Southeast Asia. Weather-related disruptions such as typhoons, droughts, flooding, and pest infestations can significantly impact coconut yields and increase raw material costs. Since coconut procurement accounts for a substantial portion of production expenses, fluctuations in agricultural output can directly affect manufacturer margins and retail pricing. Supply chain vulnerabilities continue to represent a key challenge for market participants seeking long-term pricing stability.

Intense Competition from Alternative Plant-Based Milks

Unsweetened coconut milk faces strong competition from other plant-based alternatives, including oat milk, almond milk, soy milk, rice milk, and pea protein beverages. Many competing products offer higher protein content or stronger sustainability perceptions among consumers. Continuous innovation across the broader plant-based beverage category increases competitive pressure and requires coconut milk manufacturers to invest heavily in product differentiation, branding, and functional ingredient development.

Unsweetened Coconut Milk Industry Key Opportunities

Expansion into Emerging Consumer Markets

Emerging economies such as India, Brazil, Vietnam, Indonesia, Saudi Arabia, and the UAE represent significant untapped opportunities for unsweetened coconut milk manufacturers. Rising disposable income, urbanization, growing health awareness, and expansion of organized retail are creating favorable conditions for plant-based product adoption. Early market entrants can establish strong brand recognition and distribution networks before competitive intensity increases. As modern retail channels expand across these regions, premium and health-oriented food products are becoming more accessible to middle-income consumers.

Industrial Ingredient Applications Across Food Manufacturing

Food manufacturers are increasingly incorporating unsweetened coconut milk into dairy-free yogurts, frozen desserts, ready meals, bakery products, sauces, and functional beverages. Industrial ingredient demand is expected to grow faster than retail household consumption in several developed markets. Standardized formulations with consistent fat content, texture, and flavor profiles are attracting food processors seeking reliable plant-based ingredients. Long-term supply contracts with food manufacturers provide opportunities for stable revenue growth and margin improvement among coconut milk suppliers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.31 Billion |

| Market Size in 2026 | USD 1.44 Billion |

| Market Size in 2031 | USD 2.30 Billion |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

The liquid unsweetened coconut milk segment continues to dominate the global market, accounting for approximately 68% of total demand in 2025. Its leadership is primarily driven by consumer preference for convenient, ready-to-use products that can be seamlessly incorporated into daily diets across multiple applications, including beverages, cooking, baking, and food preparation. The growing popularity of plant-based lifestyles, coupled with increasing demand for dairy alternatives, has further strengthened the position of liquid coconut milk in both retail and foodservice channels. Shelf-stable liquid products packaged in aseptic cartons remain particularly attractive due to their extended shelf life, reduced refrigeration requirements, and efficient distribution capabilities, enabling manufacturers to expand market reach while minimizing logistical costs.Coconut milk powder is emerging as a rapidly growing product category, particularly among industrial processors, food manufacturers, and export-oriented businesses. The segment benefits from lower transportation expenses, improved storage stability, reduced packaging requirements, and greater formulation flexibility. Powdered variants are increasingly utilized in bakery products, confectionery applications, nutritional supplements, instant beverages, and foodservice preparations where long shelf life and ease of handling are critical. Meanwhile, coconut milk concentrates and frozen formulations continue to serve specialized market niches, primarily catering to food manufacturers, commercial kitchens, and institutional buyers that require customized ingredient solutions, higher solids content, or bulk-volume procurement.

Application Insights

Food and beverage processing remains the largest application segment, contributing approximately 47% of global market revenue in 2025. The segment's dominance is driven by the increasing incorporation of unsweetened coconut milk into a broad range of plant-based and clean-label food products. Manufacturers are utilizing coconut milk as a functional dairy substitute in yogurts, frozen desserts, bakery products, soups, sauces, confectionery products, and ready-to-eat meals. The growing consumer shift toward vegan, lactose-free, and allergen-friendly foods continues to create significant opportunities for coconut milk integration across mainstream product categories.Beverage applications represent one of the most dynamic growth areas within the market. Rising demand for dairy-free beverages, specialty coffee drinks, smoothies, meal replacement products, and functional wellness beverages is accelerating the use of unsweetened coconut milk across both retail and foodservice environments. The segment is benefiting from evolving consumer preferences for naturally derived ingredients, lower sugar formulations, and products that support digestive health and overall wellness.Nutraceutical applications are expanding rapidly as manufacturers increasingly incorporate coconut milk into protein-enriched beverages, nutritional supplements, meal replacement products, and functional health formulations. Growing awareness regarding preventive healthcare, immunity support, and holistic nutrition is encouraging greater utilization of coconut-derived ingredients within the wellness sector. Additionally, personal care and cosmetic applications continue to gain traction as coconut-based ingredients are increasingly used in natural skincare, haircare, and beauty formulations due to their moisturizing properties, natural origin, and alignment with clean beauty trends.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel, accounting for nearly 39% of global market sales in 2025. The segment's leadership is supported by extensive product assortments, strong brand visibility, competitive pricing strategies, and the convenience of one-stop shopping experiences. These retail formats enable consumers to compare multiple brands and product variants while providing manufacturers with broad market exposure and high-volume sales opportunities.Specialty health food stores continue to play a significant role in the distribution of premium, organic, and clean-label coconut milk products. Consumers seeking certified organic, non-GMO, and sustainably sourced products frequently rely on these outlets for differentiated offerings. The channel remains particularly important in developed markets where health-conscious consumers demonstrate a willingness to pay premium prices for high-quality plant-based products.Online retail channels are among the fastest-growing distribution segments, driven by expanding digital grocery adoption, increasing internet penetration, subscription-based purchasing models, and direct-to-consumer sales strategies. E-commerce platforms provide consumers with greater product accessibility, convenience, and access to niche brands that may have limited physical retail presence. At the same time, foodservice distributors and industrial ingredient suppliers are strengthening their market position as restaurants, cafés, bakeries, and food manufacturers continue to increase the use of coconut-based ingredients across commercial applications.

End User Insights

Household consumers represent the largest end-user segment, accounting for approximately 42% of global demand in 2025. The segment's growth is being driven by rising consumer awareness of plant-based nutrition, increasing prevalence of lactose intolerance and dairy sensitivities, growing interest in sugar reduction, and expanding adoption of healthier dietary lifestyles. Consumers are increasingly utilizing unsweetened coconut milk as a substitute for conventional dairy products in cooking, baking, beverages, and everyday meal preparation.Food and beverage manufacturers constitute the second-largest end-user category and continue to play a pivotal role in market expansion. Growing product innovation initiatives, reformulation strategies focused on clean-label ingredients, and increasing demand for dairy-free alternatives are encouraging manufacturers to integrate coconut milk into a diverse range of consumer products. The segment is further supported by strong investment in plant-based product development across global food industries.Foodservice operators, including coffee chains, quick-service restaurants, bakeries, hotels, and full-service restaurants, represent one of the fastest-growing end-user groups. Rising consumer demand for vegan and dairy-free menu options has encouraged operators to expand plant-based offerings, driving greater utilization of coconut milk in beverages, desserts, and culinary applications. Nutraceutical companies and personal care manufacturers are also increasing coconut milk adoption as consumers continue to seek natural, multifunctional, and sustainably sourced ingredients across wellness and beauty products.

Source Type Insights

Conventional unsweetened coconut milk dominates the global market, accounting for approximately 74% of total revenue in 2025. The segment maintains its leadership position due to widespread availability, lower production and certification costs, established supply chains, and stronger penetration across mass-market retail channels. Conventional products remain highly attractive to both consumers and manufacturers seeking cost-effective plant-based ingredient solutions while maintaining broad accessibility across developed and emerging markets.Organic unsweetened coconut milk represents a smaller yet rapidly expanding segment within the industry. Growth is being fueled by increasing consumer preference for pesticide-free, minimally processed, clean-label, and sustainably sourced food products. Rising awareness regarding environmental sustainability, ethical sourcing practices, and overall food quality continues to strengthen demand for certified organic products. Organic coconut milk commands premium pricing and enjoys particularly strong demand across North America and Western Europe, where organic food consumption and health-conscious purchasing behavior continue to accelerate across multiple consumer categories.

Explore more data points, trends and opportunities Download Free Sample Report

Unsweetened Coconut Milk Market Segmentations

By Product Form

- Liquid Unsweetened Coconut Milk

- Unsweetened Coconut Milk Powder

- Unsweetened Coconut Milk Concentrate

- Frozen Unsweetened Coconut Milk

By Fat Content

- Full-Fat Unsweetened Coconut Milk

- Reduced-Fat / Light Unsweetened Coconut Milk

- Low-Fat Unsweetened Coconut Milk

By Source Type

- Conventional Unsweetened Coconut Milk

- Organic Unsweetened Coconut Milk

By Application

- Beverage Consumption

- Food Processing

- Nutraceutical & Functional Foods

- Personal Care & Cosmetic Formulations

- Foodservice & Hospitality

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health Stores

- Online Retail / E-commerce

- Foodservice Distribution

- B2B Industrial Supply

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 46% of global market revenue in 2025, making it the largest regional market for unsweetened coconut milk. Thailand, Indonesia, the Philippines, Vietnam, China, India, and Australia represent the primary contributors to regional production and consumption. Southeast Asian countries dominate global coconut cultivation, processing, and export activities, providing the region with a strong competitive advantage in raw material availability and manufacturing capacity.Regional growth is being driven by abundant coconut production, expanding processing infrastructure, rising urbanization, increasing disposable incomes, and growing consumer awareness of plant-based nutrition. China and India are emerging as major consumption centers due to rapidly expanding middle-class populations, changing dietary preferences, and increasing demand for dairy alternatives. Furthermore, significant investments in export-oriented manufacturing facilities, value-added coconut processing, and food innovation are strengthening the region's position as both the largest producer and consumer market globally.

North America

North America represented approximately 24% of global market demand in 2025. The United States accounted for nearly 19% of global consumption, supported by strong consumer interest in dairy alternatives, functional beverages, and clean-label food products. Canada continues to witness growing demand for premium and organic coconut milk products as consumers increasingly prioritize health and sustainability considerations in purchasing decisions.The region's growth is primarily driven by the rapid expansion of plant-based diets, rising prevalence of lactose intolerance, increasing vegan and flexitarian populations, and strong demand for low-sugar beverage alternatives. Continuous product innovation, widespread retail availability, advanced distribution networks, and growing consumer interest in wellness-focused foods continue to support sustained market expansion. The presence of major plant-based food manufacturers and strong investment in alternative dairy product development further enhances market growth prospects.

Europe

Europe accounted for approximately 22% of global market revenue in 2025, with Germany, the United Kingdom, France, Italy, Spain, and the Netherlands serving as major consumption hubs. The region has emerged as one of the most mature markets for plant-based food and beverage products, supported by evolving consumer preferences and favorable regulatory developments.Key growth drivers include increasing adoption of vegan and flexitarian lifestyles, government initiatives encouraging healthier dietary habits, growing efforts to reduce sugar consumption, and strong demand for sustainable food products. Consumers across Europe demonstrate a high preference for organic, environmentally responsible, and ethically sourced products, creating favorable conditions for premium coconut milk offerings. Additionally, sustainability-focused purchasing decisions and expanding availability of plant-based alternatives across retail and foodservice channels continue to support long-term market growth.

Latin America

Latin America is experiencing steady growth in demand for unsweetened coconut milk, led primarily by Brazil, Mexico, Argentina, and Chile. Increasing consumer awareness of health and wellness, expanding urban populations, and improving access to modern retail channels are contributing to greater adoption of plant-based beverages across the region.Regional growth is being driven by rising disposable incomes, growing demand for functional and natural food products, increasing influence of global health trends, and expanding availability of dairy-free alternatives. Brazil remains the largest market within the region due to strong cultural familiarity with coconut-based products, a well-established food processing industry, and increasing consumer interest in healthier dietary choices. The expansion of organized retail and e-commerce channels is further improving product accessibility and market penetration.

Middle East & Africa

The Middle East and Africa currently represent a smaller share of global demand but rank among the fastest-growing regional markets. The United Arab Emirates and Saudi Arabia are emerging as key growth centers due to rising premium food consumption, increasing expatriate populations, and growing awareness of plant-based nutrition. South Africa remains the largest market within Africa, supported by expanding retail infrastructure and increasing consumer exposure to dairy alternatives.Regional growth is being supported by rising health consciousness, increasing demand for premium imported food products, rapid urbanization, growing modern retail penetration, and expanding foodservice industries. The increasing prevalence of lifestyle-related health concerns, coupled with greater consumer interest in clean-label and plant-based products, is creating new opportunities for coconut milk manufacturers. Additionally, the continued expansion of supermarkets, hypermarkets, and online grocery platforms is improving product availability and accelerating market development across the region.