Tiger Prawn Market Size

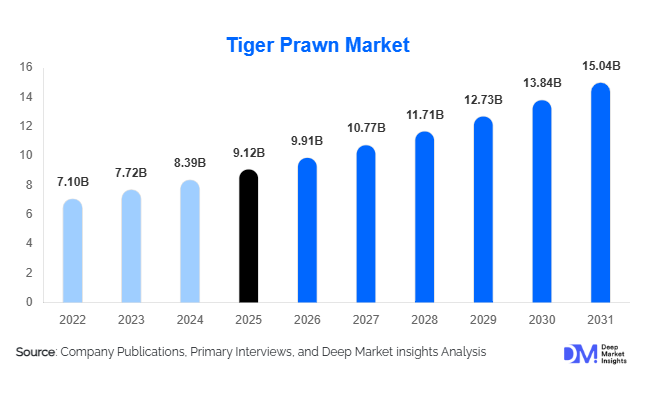

According to Deep Market Insights, the global tiger prawn market size was valued at USD 9.12 billion in 2025 and is projected to grow from USD 9.91 billion in 2026 to reach USD 15.04 billion by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The tiger prawn market growth is primarily driven by increasing global seafood consumption, rising demand for premium protein products, expansion of sustainable aquaculture practices, and growing adoption of frozen and ready-to-cook seafood products across retail and foodservice industries.

Key Market Insights

- Black tiger prawns continue to dominate global seafood trade, supported by strong export demand from the United States, China, Japan, and Europe.

- Asia-Pacific remains the leading production and export hub, with India, Vietnam, Indonesia, and Thailand accounting for a major share of global aquaculture output.

- Frozen and value-added tiger prawn products are witnessing rapid growth, driven by expansion of organized retail and convenience-focused consumer behavior.

- Sustainable and antibiotic-free aquaculture practices are becoming critical purchasing factors, especially among institutional buyers and premium retailers.

- Foodservice and hospitality industries remain major demand generators, particularly across tourism-driven economies and premium restaurant chains.

- Technological adoption in aquaculture farming, including AI-based water quality monitoring, biofloc systems, and automated feeding technologies, is improving productivity and survival rates.

Tiger Prawn Market Latest Trends

Growth of Sustainable and Certified Aquaculture

Sustainability has become one of the most influential trends shaping the global tiger prawn market. International seafood buyers, retailers, and foodservice chains are increasingly demanding sustainably farmed and traceable seafood products. This trend has accelerated the adoption of certifications such as ASC, BAP, and antibiotic-free production standards among aquaculture operators. Producers are investing in biosecure hatcheries, eco-friendly farming systems, and responsible feed management practices to improve export competitiveness. Sustainable aquaculture is also gaining government support across Asia-Pacific countries, where authorities are promoting environmentally compliant shrimp farming to strengthen long-term export opportunities and reduce ecological damage from intensive aquaculture activities.

Rapid Expansion of Value-Added Frozen Seafood Products

The market is witnessing substantial growth in processed and value-added tiger prawn products including breaded prawns, marinated prawns, ready-to-cook frozen seafood meals, and individually quick frozen (IQF) products. Urban consumers increasingly prefer convenient seafood options with longer shelf life and easier preparation. Retailers and quick-service restaurant chains are expanding frozen seafood offerings to meet rising demand from working consumers and younger demographics. E-commerce seafood retail platforms are also contributing to higher penetration of frozen tiger prawn products globally. Manufacturers are increasingly focusing on premium packaging, cold-chain optimization, and private-label seafood products to capture higher margins in developed markets.

Tiger Prawn Market Drivers

Rising Global Demand for Premium Seafood Protein

Growing health consciousness and increasing preference for lean protein diets are significantly boosting demand for tiger prawns globally. Consumers are increasingly shifting toward seafood products rich in protein and omega-3 fatty acids, particularly in developed economies. Tiger prawns are considered premium seafood products due to their larger size, superior texture, and high meat yield, making them highly preferred across restaurants, hospitality chains, and premium retail outlets. Rising disposable incomes in Asia-Pacific and Middle Eastern countries are further accelerating seafood consumption and premium dining expenditure, supporting sustained market growth.

Expansion of Aquaculture Infrastructure Across Asia-Pacific

Asia-Pacific countries including India, Vietnam, Indonesia, and Thailand continue to invest heavily in aquaculture infrastructure, hatchery modernization, feed optimization, and processing facilities. Intensive and semi-intensive shrimp farming systems are enabling producers to maximize production efficiency and export capacity. Government subsidies, export incentives, and technological advancements in water quality monitoring and disease management are strengthening regional production competitiveness. The adoption of biofloc systems and recirculating aquaculture systems (RAS) is also helping producers improve sustainability while reducing mortality risks and operational losses.

Global Market Restraints

Disease Outbreaks and Aquaculture Risks

The tiger prawn industry remains highly vulnerable to viral disease outbreaks such as White Spot Syndrome Virus (WSSV) and Early Mortality Syndrome (EMS). Disease-related production losses can significantly impact profitability and export volumes, particularly for small and medium-scale producers. Climatic changes, water contamination, and poor biosecurity management further increase operational risks within shrimp farming operations. These challenges continue to create uncertainty in supply consistency and long-term production planning.

Volatility in Feed and Operational Costs

Feed ingredients such as fishmeal and soybean meal account for a substantial portion of aquaculture production costs. Fluctuations in global commodity prices, transportation expenses, fuel costs, and energy prices directly influence producer profitability. Rising labor costs and inflationary pressures in key producing countries are also impacting operational efficiency. Additionally, export-oriented producers face currency fluctuations and changing international trade regulations, which may further pressure margins across the tiger prawn supply chain.

Tiger Prawn Industry Key Opportunities

Growth of Premium Ready-to-Cook Seafood Products

The increasing popularity of convenience foods presents major opportunities for tiger prawn processors and exporters. Consumers are increasingly purchasing marinated, breaded, seasoned, and ready-to-cook seafood products through supermarkets and online platforms. Premium frozen seafood categories are expanding rapidly in North America, Europe, China, Japan, and Gulf countries. Companies investing in value-added processing facilities and cold-chain logistics are expected to achieve higher margins and stronger retail partnerships. This opportunity is particularly attractive for exporters seeking to diversify away from low-margin raw seafood trade.

Technology-Driven Smart Aquaculture

The adoption of advanced aquaculture technologies is creating significant opportunities for productivity improvement and risk reduction. AI-enabled water quality monitoring, automated feeding systems, predictive disease analytics, and genetic breeding programs are helping producers optimize farming efficiency. Smart aquaculture solutions reduce feed wastage, improve survival rates, and increase production consistency. Governments and private investors are increasingly funding digital aquaculture projects to strengthen long-term seafood security and export competitiveness. Technology-driven farming practices are expected to become a major differentiator among leading global tiger prawn producers over the coming decade.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.12 Billion |

| Market Size in 2026 | USD 9.91 Billion |

| Market Size in 2031 | USD 15.04 Billion |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Species Type Insights

Black tiger prawns dominate the global tiger prawn market, accounting for approximately 63% of the total market share in 2025. Their dominance is supported by strong export demand, superior size characteristics, premium meat quality, and high acceptance within hospitality and foodservice industries. Giant tiger prawns are also witnessing increasing popularity across luxury seafood restaurants due to their larger size and premium pricing potential. Organic and antibiotic-free tiger prawns are emerging as rapidly growing niche categories, particularly in Europe and North America where sustainability and traceability have become critical purchasing considerations. Producers are increasingly investing in disease-resistant broodstock and sustainable farming certifications to improve international market access and pricing realization.

Product Form Insights

Raw frozen tiger prawns remain the leading product form segment, contributing nearly 38% of global market revenue. Frozen products dominate due to their extended shelf life, export efficiency, and strong retail demand. Individually quick frozen (IQF) tiger prawns are witnessing accelerated growth across supermarkets and e-commerce seafood retail channels. Value-added products such as peeled, deveined, marinated, and breaded prawns are increasingly preferred by urban consumers seeking convenience-oriented seafood options. Premium hospitality and restaurant sectors continue favoring head-on shell-on tiger prawns due to their visual appeal and culinary versatility in gourmet seafood preparations.

Farming Method Insights

Intensive aquaculture systems account for nearly 46% of the global tiger prawn market due to their higher production efficiency and scalability. Producers are increasingly adopting advanced aeration systems, automated feeding technologies, and biosecure farming methods to maximize output and minimize disease-related losses. Semi-intensive farming remains widely used across emerging aquaculture regions because of lower capital requirements and operational flexibility. Biofloc farming and recirculating aquaculture systems (RAS) are gaining traction as sustainable alternatives that reduce water usage, improve feed conversion ratios, and support environmentally responsible production practices.

Distribution Channel Insights

Direct B2B sales and seafood wholesalers collectively dominate tiger prawn distribution channels, accounting for approximately 44% of the global market. Restaurants, seafood processors, hotels, and catering operators remain major procurement customers within this channel. Organized retail chains and supermarkets are rapidly expanding frozen seafood shelf space to meet rising urban demand for premium seafood products. Online seafood retail platforms are emerging as one of the fastest-growing distribution channels globally, supported by improvements in cold-chain logistics, direct-to-consumer delivery models, and digital seafood marketplaces. Subscription seafood delivery services are also gaining popularity in developed economies.

End-Use Insights

Hotels and restaurants remain the largest end-use segment in the global tiger prawn market, accounting for nearly 35% of total demand in 2025. Premium seafood dining, tourism growth, and expansion of Asian cuisine globally continue supporting foodservice demand. Quick-service restaurants and ready-meal manufacturers are among the fastest-growing end-use segments due to increasing consumer preference for convenient seafood-based meals. Household consumption is also expanding steadily as frozen and ready-to-cook seafood products become more accessible through retail and e-commerce channels. Export trading companies remain highly important within producing countries, facilitating large-scale international seafood shipments to major importing markets.

Explore more data points, trends and opportunities Download Free Sample Report

Tiger Prawn Market Segmentations

By Species Type

- Black Tiger Prawn

- Giant Tiger Prawn

- Green Tiger Prawn

- Brown Tiger Prawn

- Organic Tiger Prawn

- SPF (Specific Pathogen Free) Tiger Prawn

By Product Form

- Whole Tiger Prawn

- Peeled Tiger Prawn

- Deveined Tiger Prawn

- Tail-on Tiger Prawn

- Cooked Tiger Prawn

- Raw Frozen Tiger Prawn

- Breaded & Processed Tiger Prawn

- Marinated Tiger Prawn

- Value-Added Ready-to-Cook Tiger Prawn

By Farming Method

- Intensive Aquaculture

- Semi-Intensive Aquaculture

- Extensive Aquaculture

- Biofloc Farming

- Recirculating Aquaculture Systems

- Organic & Sustainable Aquaculture

By Processing Type

- Fresh

- Chilled

- Frozen

- Individually Quick Frozen

- Smoked

- Dried

By Distribution Channel

- Direct/B2B Sales

- Seafood Distributors

- Hypermarkets & Supermarkets

- Specialty Seafood Stores

- Convenience Stores

- Online Retail & E-Commerce

- Foodservice Wholesalers

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global tiger prawn market with approximately 54% market share in 2025. India, Vietnam, Indonesia, Thailand, and China serve as the leading production and export hubs due to favorable climatic conditions, extensive coastlines, and established aquaculture infrastructure. India remains one of the largest exporters globally, benefiting from large-scale shrimp farming expansion and competitive processing costs. Vietnam continues strengthening its position in value-added seafood exports, particularly across Europe and North America. China represents both a major producer and importer, supported by rising seafood consumption among middle-class consumers. Japan and South Korea maintain strong import demand for premium frozen seafood products.

North America

North America accounts for nearly 18% of the global tiger prawn market, led primarily by the United States. The region remains heavily dependent on seafood imports due to limited domestic shrimp farming capacity. Rising demand for sustainably certified seafood, premium restaurant dining, and frozen ready-to-cook products is driving market growth. Retail chains and foodservice operators continue expanding seafood product portfolios, particularly within premium and convenience-focused categories. Canada also contributes to regional demand growth through rising frozen seafood consumption and hospitality industry expansion.

Europe

Europe represents approximately 16% of the global tiger prawn market, with Spain, France, Italy, Germany, and the United Kingdom emerging as key importing countries. European consumers increasingly prefer sustainably sourced and traceable seafood products, encouraging exporters to adopt certification standards and transparent supply chains. Frozen seafood retail sales continue growing steadily across Western Europe, supported by urban lifestyles and rising seafood consumption. Premium restaurants and Mediterranean cuisine trends also contribute significantly to regional tiger prawn demand.

Latin America

Latin America is emerging as a growing aquaculture and seafood consumption region. Ecuador and Brazil are investing substantially in shrimp farming infrastructure, processing technologies, and export capacity expansion. Brazil’s domestic seafood market is also benefiting from increasing protein consumption and changing dietary preferences. Regional governments are encouraging seafood exports and sustainable aquaculture development to strengthen international trade competitiveness.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand for premium seafood products, particularly across the UAE, Saudi Arabia, and South Africa. Tourism expansion, luxury hospitality growth, and rising disposable incomes are driving tiger prawn consumption within hotels and fine dining establishments. Saudi Arabia is aggressively investing in aquaculture projects under national food security initiatives. In Africa, coastal aquaculture development and export-oriented seafood processing are gradually expanding, particularly in East African nations.

Key Players in the Tiger Prawn Market

- Charoen Pokphand Foods

- Thai Union Group

- Minh Phu Seafood Corporation

- Avanti Feeds

- Devi Sea Foods

- Apex Frozen Foods

- Surapon Foods

- PT Central Proteina Prima

- Vinh Hoan Corporation

- Japfa Comfeed

- Omarsa

- Seajoy Group

- Blue Star Foods

- Nekkanti Sea Foods

- BMR Group