Groundfish Market Size

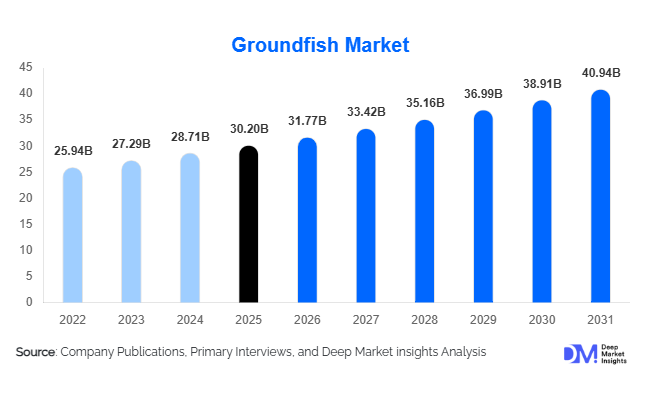

According to Deep Market Insights, the global groundfish market size was valued at approximately USD 30.2 billion in 2025 and is projected to grow from USD 31.77 billion in 2026 to reach USD 40.94 billion by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). The groundfish market growth is primarily driven by increasing global seafood consumption, rising demand for high-protein and low-fat food products, expansion of frozen seafood distribution networks, and growing utilization of cod, pollock, hake, haddock, and other groundfish species in value-added seafood processing applications. The market continues to benefit from evolving consumer preferences toward healthy diets, growing foodservice demand, and technological advancements in seafood harvesting, processing, preservation, and traceability systems.

Key Market Insights

- Cod remains the largest species segment, accounting for approximately 32% of global groundfish market revenue due to strong demand across Europe and North America.

- Frozen groundfish products dominate global trade, representing over 50% of market revenue owing to superior shelf life and export suitability.

- North America leads the global market, supported by large-scale Alaska pollock and Pacific cod fisheries, advanced processing infrastructure, and strong domestic consumption.

- Asia-Pacific is the fastest-growing regional market, driven by rising seafood consumption and expanding seafood processing industries in China, Vietnam, Thailand, and South Korea.

- Value-added seafood products, including fish fingers, breaded fish products, surimi, and ready-to-cook seafood meals, are becoming major growth engines.

- Sustainability certifications and traceability systems are increasingly influencing procurement decisions among retailers, foodservice operators, and institutional buyers worldwide.

Groundfish Market Latest Trends

Expansion of Value-Added Seafood Processing

Groundfish processors are increasingly moving beyond commodity whole-fish sales toward higher-margin value-added products. Frozen fillets, portion-controlled seafood products, breaded fish, fish sticks, ready-to-cook meals, and surimi-based products are experiencing robust demand across developed and emerging markets. Retailers and foodservice operators prefer processed products that simplify preparation while ensuring consistency and food safety. Manufacturers are investing heavily in automated filleting lines, portioning technologies, and advanced packaging systems to meet this demand. The trend is particularly strong in North America, Europe, China, and Japan, where consumers increasingly prioritize convenience-oriented seafood products.

Sustainability and Digital Traceability Becoming Industry Standards

Retail chains, foodservice companies, and institutional buyers are increasingly requiring sustainably sourced groundfish products. Certification programs such as Marine Stewardship Council (MSC) and sustainable fisheries management initiatives are reshaping procurement practices. At the same time, blockchain-based traceability systems, digital catch monitoring, vessel tracking technologies, and electronic reporting platforms are gaining widespread adoption. These technologies improve supply chain transparency, reduce illegal fishing risks, and help companies meet evolving regulatory requirements. Sustainable sourcing and digital traceability are becoming major differentiators among leading global groundfish suppliers.

Groundfish Market Drivers

Growing Consumer Preference for Healthy Protein Sources

Consumers worldwide are increasingly replacing red meat with seafood due to health and wellness considerations. Groundfish species such as cod, pollock, hake, and haddock provide high-quality protein, essential nutrients, and lower fat content compared to many alternative protein sources. Government dietary guidelines promoting seafood consumption, coupled with increasing awareness of healthy eating habits, continue to strengthen market demand. This trend is especially visible across North America, Europe, Japan, South Korea, and urban areas of China.

Rapid Growth of Frozen Seafood Distribution Infrastructure

The expansion of global cold-chain logistics networks has significantly enhanced the accessibility of groundfish products. Investments in refrigerated transportation, cold storage facilities, IQF technologies, and modern distribution systems enable seafood producers to reach geographically distant markets while maintaining product quality. Frozen fillets and processed seafood products have become highly accessible through supermarkets, hypermarkets, online grocery platforms, and foodservice distributors, supporting sustained market expansion.

Increasing Demand from Seafood Processing Industries

Groundfish remains a critical raw material for surimi manufacturing, frozen seafood processing, fish meal production, and ready-meal preparation. Growing demand from quick-service restaurants, institutional catering providers, and packaged food manufacturers is creating significant downstream consumption opportunities. Alaska pollock, in particular, continues to dominate global surimi production, while cod and hake remain preferred species for premium processed seafood products.

Groundfish Market Restraints

Fishing Quota Restrictions and Resource Sustainability Concerns

Several major groundfish fisheries operate under increasingly stringent quota systems designed to prevent overfishing and ensure long-term stock sustainability. While these measures support environmental objectives, they also constrain supply growth and create pricing volatility. Reduced catch allocations for certain cod and hake fisheries have already affected supply availability across key global markets.

Price Volatility and Compliance Costs

Groundfish pricing remains highly sensitive to quota allocations, fuel costs, labor shortages, climatic conditions, and geopolitical trade developments. Furthermore, compliance with food safety regulations, sustainability certifications, and traceability requirements requires substantial investments from seafood companies. These costs can place pressure on profitability, particularly for small and medium-sized operators.

Groundfish Industry Key Opportunities

Premium Sustainable Seafood Segment Expansion

The growing preference for certified sustainable seafood presents significant opportunities for both established participants and new entrants. Retailers and foodservice operators are increasingly willing to pay premium prices for products carrying recognized sustainability certifications. Companies investing in sustainable fishing practices, electronic vessel monitoring systems, and environmentally responsible harvesting methods can secure long-term contracts and premium market positioning. The trend is expected to strengthen as consumers become more environmentally conscious and governments continue tightening fisheries management regulations.

Asia-Pacific Processing and Export Growth

China, Vietnam, Thailand, and South Korea continue expanding their seafood processing industries, creating significant opportunities for groundfish suppliers. Rising seafood consumption across Asia, combined with increasing export-oriented processing activity, is driving demand for imported cod, pollock, and hake. Companies establishing strategic processing partnerships and cold-chain infrastructure investments within Asia-Pacific can capitalize on both domestic consumption growth and export-driven processing demand.

Pet Food and Nutraceutical Applications

Groundfish by-products and lower-grade fish materials are increasingly utilized in premium pet food formulations, fish oils, protein concentrates, and marine nutraceutical ingredients. Growing demand for omega-3 supplements, protein-rich pet foods, and functional nutrition products is opening new revenue streams for seafood processors. These applications improve raw material utilization rates while supporting profitability through value extraction from processing residuals.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 30.20 Billion |

| Market Size in 2026 | USD 31.77 Billion |

| Market Size in 2031 | USD 40.94 Billion |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Species Type Insights

Cod accounted for approximately 32% of the global groundfish market revenue in 2025, making it the leading species segment. The segment’s dominance is supported by strong consumer preference for its mild flavor, versatile culinary applications, high nutritional value, and widespread availability across retail, foodservice, and processed seafood channels. Atlantic cod continues to hold a particularly strong position across European markets, where it remains a staple ingredient in traditional seafood dishes, while Pacific cod enjoys substantial demand throughout North America and Asia-Pacific due to its broad utilization in frozen seafood products and quick-service restaurant offerings. The availability of well-established harvesting and processing infrastructure, coupled with premium pricing compared to several alternative species, further reinforces cod’s market leadership. Pollock represents the second-largest species category and serves as a critical raw material for frozen seafood products, fish sticks, fish sandwiches, and surimi-based products. The species benefits from abundant fish stocks, cost competitiveness, and extensive adoption by large-scale seafood processors. Hake continues to witness increasing demand across Europe and Latin America owing to its favorable price-to-quality ratio, adaptability to various processing formats, and growing acceptance among consumers seeking affordable seafood protein. Flatfish species, including sole, plaice, flounder, and halibut, occupy premium segments of the market and are particularly favored in upscale foodservice establishments and specialty seafood retail channels where quality, texture, and culinary differentiation command higher margins.

Product Form Insights

Fillets represented approximately 41% of total global market revenue in 2025, making them the largest product form segment. The segment's leadership is primarily driven by growing consumer demand for convenience, portion-controlled seafood products, ease of preparation, and reduced processing requirements at the household level. The increasing penetration of modern retail chains, e-commerce seafood platforms, and ready-to-cook meal solutions has further accelerated fillet consumption worldwide. Frozen fillets continue to gain traction among consumers due to their extended shelf life and year-round availability, while fresh fillets remain highly sought after in premium retail and foodservice environments. Whole fish products continue to maintain significant demand across traditional seafood markets, ethnic food segments, and export destinations where consumers prefer minimal processing and freshness attributes. Surimi raw materials remain an essential product category supporting large-scale seafood processing operations, particularly in Asia-Pacific and North America. Meanwhile, value-added processed products such as breaded fish portions, fish fingers, seafood snacks, marinated products, and ready-to-cook meals are among the fastest-growing categories, supported by changing lifestyles, increasing urbanization, rising disposable incomes, and growing demand for convenient protein-rich food solutions.

Preservation Method Insights

Frozen groundfish products accounted for approximately 52% of the global market in 2025, making frozen preservation the dominant segment. The segment's growth is driven by the ability to significantly extend product shelf life, minimize post-harvest losses, maintain product quality during long-distance transportation, and support international seafood trade. Rising investments in cold-chain logistics infrastructure, expanding global seafood exports, and increasing consumer preference for convenient frozen food products continue to strengthen segment performance. Individually Quick Frozen (IQF) technologies are gaining widespread adoption as they help preserve texture, flavor, nutritional value, and product integrity while allowing flexible portion usage for consumers and foodservice operators. Fresh and chilled groundfish products remain important within premium retail and restaurant channels, particularly in Europe and North America where demand for high-quality fresh seafood remains strong. Traditional preservation methods, including smoked, dried, salted, and cured groundfish products, continue to hold substantial cultural and commercial significance across Northern Europe, parts of Asia, and selected Latin American markets, where longstanding culinary traditions and specialty seafood consumption patterns support stable demand.

Application Insights

Human consumption dominated the global groundfish market with approximately 78% market share in 2025. The segment’s leadership is primarily attributed to rising global seafood consumption, growing awareness of the health benefits associated with lean marine protein, and increasing consumer preference for nutrient-rich diets. Retail seafood sales and foodservice consumption collectively account for the majority of demand, supported by expanding supermarket seafood sections, online seafood distribution channels, and increasing seafood menu offerings across restaurants and quick-service establishments. Seafood processing industries represent the second-largest application area, utilizing groundfish extensively for frozen products, prepared meals, surimi manufacturing, and value-added seafood applications. Beyond direct food consumption, fishmeal, fish oil, nutraceuticals, aquaculture feed, and premium pet food applications are emerging as important growth opportunities. These segments are benefiting from growing demand for sustainable protein ingredients, omega-3-rich nutritional supplements, and marine-derived functional ingredients used across animal nutrition and health-focused consumer products.

End-Use Insights

Food processing manufacturers accounted for approximately 29% of global market demand in 2025, making them the largest end-user segment. Segment growth is primarily driven by increasing production of frozen seafood products, ready-to-eat meals, breaded fish products, surimi-based foods, and convenience-oriented seafood offerings that cater to evolving consumer preferences. Large-scale processors benefit from reliable groundfish supply chains, technological advancements in seafood processing, and growing global demand for packaged seafood products. Quick-service restaurants represent one of the fastest-growing end-user categories, supported by expanding consumer demand for fish sandwiches, seafood burgers, wraps, and breaded seafood menu items. Institutional foodservice providers, including schools, hospitals, military organizations, and corporate catering facilities, continue generating stable demand due to the nutritional benefits and cost-effectiveness of groundfish products. In addition, premium pet food manufacturers and marine nutraceutical companies are emerging as increasingly important customer groups as demand rises for protein-rich pet nutrition products and marine-based health supplements, creating additional value-generation opportunities across the supply chain.

Explore more data points, trends and opportunities Download Free Sample Report

Groundfish Market Segmentations

By Species Type

- Cod

- Pollock

- Hake

- Haddock

- Whiting

- Flatfish Groundfish

- Other Groundfish Species

By Product Form

- Whole Fish

- Headed & Gutted (H&G)

- Fillets

- Steaks & Portions

- Surimi Raw Material

- Fish Blocks

- Minced Groundfish Products

- Value-Added Processed Products

By Preservation Method

- Fresh/Chilled

- Frozen

- Individually Quick Frozen (IQF)

- Salted

- Dried

- Smoked

- Canned/Preserved

By Source

- Wild-Caught

- Farmed/Aquaculture-Derived Groundfish

By Distribution Channel

- Direct Sales to Processors

- Seafood Wholesalers

- Foodservice Distributors

- Modern Retail

- Convenience Stores

- Specialty Seafood Stores

- E-Commerce Seafood Platforms

Regional Insights

North America

North America accounted for approximately 38% of global groundfish market revenue in 2025, making it the largest regional market. The United States alone contributes nearly 30% of global demand, supported by extensive Alaska pollock and Pacific cod fisheries, advanced seafood harvesting capabilities, sophisticated processing infrastructure, and strong consumption across retail and foodservice sectors. Canada remains a significant producer and exporter of cod, haddock, and other North Atlantic groundfish species, strengthening the region’s supply position. Regional growth is supported by increasing consumer preference for high-protein and low-fat seafood products, rising demand for sustainable and traceable seafood, growing penetration of frozen and convenience seafood products, and continued investments in processing technologies. Furthermore, well-established fisheries management systems, sustainability certifications, and modernization of cold-chain logistics continue to enhance operational efficiency and strengthen North America's competitive advantage in global seafood trade.

Europe

Europe represented approximately 29% of global market revenue in 2025, making it the second-largest regional market. Major consuming countries include the United Kingdom, Germany, France, Spain, Italy, Norway, Iceland, and the Netherlands. Cod and haddock remain staple seafood products throughout Northern Europe, while hake consumption continues to expand rapidly across Southern European markets. Norway and Iceland play critical roles as leading exporters, supplying premium groundfish products to both regional and international markets. Regional growth is being driven by increasing consumer demand for sustainably sourced seafood, growing health consciousness, strong seafood consumption traditions, and rising preference for certified and traceable fish products. The expansion of premium seafood retail formats, continued development of value-added seafood offerings, and stringent sustainability regulations further support long-term market expansion. Additionally, Europe's well-developed seafood distribution networks and emphasis on responsible fisheries management continue to reinforce market stability and consumer confidence.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR of approximately 6.5% through 2031. China dominates regional demand due to its large seafood-consuming population, extensive seafood processing industry, and growing role as a global seafood trading hub. Japan and South Korea maintain some of the highest per-capita seafood consumption levels globally, while Vietnam and Thailand continue strengthening their export-oriented seafood processing industries. Regional growth is primarily driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, increasing awareness of seafood's nutritional benefits, and growing demand for convenient protein sources. The expansion of organized retail channels, e-commerce food distribution platforms, and cold-chain infrastructure is further supporting seafood accessibility across both developed and emerging economies. Additionally, increasing investments in seafood processing capacity and export-oriented manufacturing continue to position Asia-Pacific as a major growth engine for the global groundfish market.

Latin America

Latin America accounted for approximately 7% of global groundfish market revenue in 2025. Chile, Argentina, Peru, and Mexico represent the region’s largest markets, supported by abundant marine resources and expanding seafood industries. Hake fisheries play a particularly important role in Chile and Argentina, contributing significantly to both domestic consumption and export revenues. Regional growth is being driven by increasing seafood consumption among expanding middle-class populations, rising awareness of the health benefits associated with fish-based diets, and growing investments in seafood processing and export infrastructure. Government initiatives supporting fisheries modernization, improvements in cold-chain logistics, and rising international demand for Latin American seafood products are further strengthening market development. Export-oriented processing activities and favorable resource availability continue to position the region as an important supplier within the global groundfish value chain.

Middle East & Africa

The Middle East and Africa collectively represented approximately 4% of global groundfish market demand in 2025. South Africa remains the region’s most important producer, supported by its well-established hake industry and export-oriented seafood sector. Saudi Arabia, the United Arab Emirates, Egypt, and Qatar are increasingly significant import markets due to rising seafood consumption and expanding foodservice industries. Regional growth is driven by rapid population growth, increasing urbanization, rising disposable incomes, changing dietary preferences toward healthier protein sources, and substantial investments in food distribution infrastructure. The ongoing expansion of cold-chain logistics networks, growth of modern retail formats, and increasing demand from hotels, restaurants, and tourism-related foodservice establishments are further supporting market development. In addition, government-led food security initiatives and growing dependence on imported seafood products continue to create favorable conditions for sustained market growth across the region.

Key Players in the Groundfish Market

- Trident Seafoods

- American Seafoods

- Nissui Corporation

- Maruha Nichiro Corporation

- High Liner Foods

- Royal Greenland

- Lerøy Seafood Group

- Austevoll Seafood

- Pacific Seafood

- Espersen

- Iceland Seafood International

- Brim Seafood

- Pescanova

- Cooke Seafood

- HB Grandi