Fresh Squid Market Size

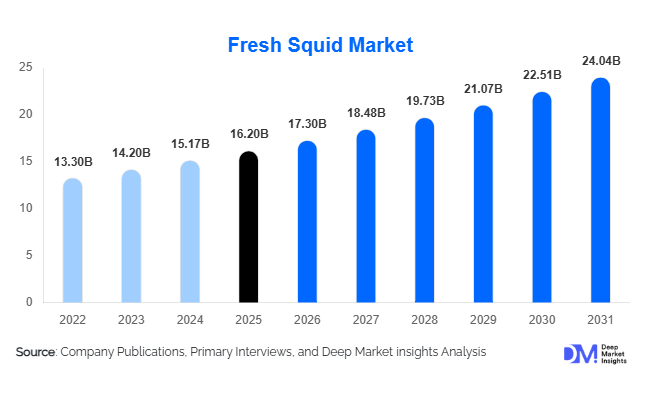

According to Deep Market Insights, the global fresh squid market size was valued at approximately USD 16.2 billion in 2025 and is projected to grow from USD 17.30 billion in 2026 to reach USD 24.04 billion by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The fresh squid market growth is primarily driven by rising global seafood consumption, increasing demand for high-protein marine food products, expansion of international seafood trade, and growing penetration of premium seafood retail and foodservice channels. Fresh squid continues to gain popularity across Asia-Pacific, Europe, and North America due to its nutritional profile, culinary versatility, and strong presence in Mediterranean and Asian cuisines. Improvements in cold-chain logistics, seafood traceability systems, and international distribution networks are further supporting market expansion by ensuring product freshness and quality throughout the supply chain.

Key Market Insights

- Foodservice remains the largest end-use segment, accounting for nearly 48% of global fresh squid demand due to strong consumption in restaurants, hotels, seafood chains, and catering services.

- Asia-Pacific dominates the global market, representing approximately 54% of worldwide consumption, led by China, Japan, South Korea, Thailand, and Vietnam.

- Wild-caught squid accounts for over 90% of global supply, reflecting the limited commercialization of squid aquaculture compared to other seafood categories.

- Premium export-grade squid is gaining market share, supported by increasing demand from Europe, Japan, and North America for high-quality fresh seafood products.

- Seafood e-commerce and direct-to-consumer distribution channels are expanding rapidly, creating new opportunities for exporters and processors to reach premium customers.

- Digital traceability and sustainable sourcing initiatives are becoming competitive differentiators, particularly among exporters targeting developed markets with stringent seafood regulations.

Fresh Squid Market Latest Trends

Sustainable and Traceable Seafood Supply Chains Gaining Momentum

The fresh squid industry is increasingly embracing sustainability and traceability as major competitive advantages. Global retailers, restaurant chains, and seafood distributors are demanding greater visibility into fishing practices, catch locations, and environmental impacts. Governments and fisheries management organizations are implementing stricter regulations regarding vessel monitoring, catch documentation, and sustainable harvesting quotas. Seafood exporters are investing in blockchain-based traceability platforms, digital vessel monitoring systems, and sustainability certifications to strengthen market access. These initiatives are helping suppliers secure premium contracts with international buyers while improving consumer confidence regarding responsible sourcing. As environmental awareness grows globally, sustainably harvested fresh squid is expected to command higher market value and stronger customer loyalty.

Premiumization of Fresh Seafood Consumption

Consumer demand for premium seafood products continues to reshape the fresh squid market. Urban consumers across Asia, Europe, and North America are increasingly willing to pay premium prices for high-quality, freshly landed squid products. Upscale restaurants, seafood specialty stores, gourmet retailers, and premium online seafood platforms are driving demand for export-grade squid with superior freshness and handling standards. Product differentiation through species selection, freshness certification, origin labeling, and premium packaging is becoming increasingly common. This premiumization trend is encouraging seafood processors and exporters to invest in advanced chilling technologies, quality grading systems, and cold-chain infrastructure that enhance product value while reducing spoilage losses.

Fresh Squid Market Drivers

Rising Global Demand for Seafood Protein

Growing consumer awareness regarding healthy diets is significantly increasing seafood consumption worldwide. Fresh squid is recognized as a lean protein source rich in essential amino acids, vitamins, and minerals while remaining relatively low in fat. Consumers are increasingly substituting traditional animal proteins with seafood products as part of healthier eating habits. This trend is particularly evident across Asia-Pacific, Europe, and North America, where seafood consumption continues to rise due to nutritional considerations and evolving dietary preferences. Fresh squid benefits from this transition because of its versatility in multiple cuisines and strong cultural acceptance across key seafood-consuming regions.

Expansion of Global Foodservice and Hospitality Industries

The recovery and expansion of restaurants, hotels, resorts, cruise operators, and catering businesses are driving fresh squid consumption globally. Calamari, grilled squid, seafood platters, sushi preparations, and Mediterranean squid dishes remain popular menu items across international foodservice establishments. Growth in tourism and hospitality infrastructure is supporting higher procurement volumes, particularly in regions with strong seafood cultures. Premium dining concepts and seafood-focused restaurant chains continue introducing squid-based menu innovations that further stimulate demand.

Advancements in Cold-Chain Logistics and Seafood Distribution

Technological advancements in refrigeration, transportation, and seafood handling are significantly improving market accessibility. Modern cold-chain systems enable exporters to maintain freshness during long-distance transportation, expanding access to premium markets. Investments in temperature-controlled logistics, insulated packaging, and rapid chilling technologies are reducing spoilage while increasing shelf life. These developments have strengthened global trade flows and allowed fresh squid suppliers to reach high-value international customers more efficiently.

Fresh Squid Market Restraints

Supply Volatility Due to Overfishing and Fishery Regulations

The fresh squid market remains heavily dependent on wild-caught fisheries, making supply vulnerable to regulatory interventions and resource management policies. Fishing quotas, seasonal closures, and sustainability requirements can constrain harvest volumes and create supply shortages. As governments seek to preserve marine ecosystems, stricter fisheries management measures may limit production growth and contribute to pricing volatility.

Climate Change and Oceanographic Uncertainty

Squid populations are highly sensitive to ocean temperatures, currents, and environmental conditions. Climate variability can alter migration patterns, spawning cycles, and catch volumes, creating uncertainty throughout the supply chain. Unpredictable harvest conditions increase operational risks for fisheries, processors, and exporters while complicating long-term procurement planning for global buyers.

Fresh Squid Industry Key Opportunities

Growth of Premium Seafood Consumption in Emerging Economies

Rapid urbanization and rising disposable incomes across China, India, Southeast Asia, and the Middle East are creating strong demand for premium seafood products. Fresh squid is increasingly positioned as a high-value protein alternative in metropolitan markets where consumers are willing to pay for freshness, quality, and food safety. Seafood companies that establish efficient premium supply chains and strong brand positioning can capitalize on this expanding consumer base.

Expansion of Sustainable Seafood Programs

Demand for responsibly sourced seafood continues to increase among retailers, foodservice operators, and consumers. Companies investing in sustainable harvesting practices, traceability technologies, and environmental certifications can differentiate themselves in competitive export markets. Sustainable sourcing initiatives also improve access to long-term supply agreements with major international buyers seeking compliance with evolving environmental standards.

Development of Direct-to-Consumer Seafood Channels

The rapid growth of seafood e-commerce and online grocery platforms is creating opportunities for fresh squid suppliers to engage directly with consumers. Direct-to-consumer models improve pricing power, enhance brand recognition, and reduce dependence on traditional intermediaries. Investments in cold-chain delivery infrastructure and digital commerce capabilities are expected to generate significant market opportunities throughout the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16.20 Billion |

| Market Size in 2026 | USD 17.30 Billion |

| Market Size in 2031 | USD 24.04 Billion |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

The whole fresh squid segment dominates the global fresh squid market, accounting for approximately 38% of total market value. Its leadership position is primarily attributed to its versatility across wholesale, processing, retail, and foodservice applications. Whole squid provides buyers with greater flexibility for customized processing, portioning, and value-added product development while offering relatively lower procurement costs compared to pre-processed alternatives. Seafood processors, distributors, and large-scale foodservice operators continue to favor whole squid due to its ability to maximize yield and accommodate diverse regional culinary requirements. The segment is further supported by strong international trade flows, particularly across Asia-Pacific and European markets where whole squid serves as a key raw material for downstream seafood processing activities.Fresh squid rings and portioned products continue gaining traction across retail seafood counters, quick-service restaurants, and casual dining chains where convenience and standardized serving sizes are critical. Rising consumer interest in calamari and ready-to-cook seafood products has accelerated demand for these processed formats. Meanwhile, value-added fresh squid products, including marinated, seasoned, and pre-prepared offerings, are emerging as premium categories within developed markets. Growth in these segments is supported by changing consumer lifestyles, increasing demand for convenience-oriented seafood products, and manufacturers' efforts to introduce differentiated products with enhanced flavor profiles and extended shelf-life characteristics.

Species Insights

Japanese Flying Squid remains the leading species segment, accounting for approximately 24% of global market value. Its dominance is supported by strong consumption patterns across Japan, China, and South Korea, where squid represents an integral component of traditional diets and seafood cuisine. The species is widely utilized in fresh consumption, processed seafood products, and foodservice applications, benefiting from established supply chains and extensive regional fishing operations. Consistent consumer familiarity and strong cultural preference for squid-based dishes continue to reinforce demand across East Asian markets.Argentine Shortfin Squid represents another major commercial species and plays a vital role in international squid trade. Large-scale harvesting activities in Argentina and surrounding South Atlantic waters provide substantial export volumes to Europe and Asia. The species is highly valued for its commercial availability, processing suitability, and competitive pricing, making it an important raw material for seafood processors and foodservice operators worldwide.Species diversification has become increasingly important throughout the global fresh squid market as industry participants seek to reduce supply risks associated with environmental variability, changing ocean conditions, fishing quotas, and regulatory restrictions. Processors and exporters are increasingly broadening their sourcing strategies to ensure supply continuity and maintain operational resilience amid evolving market conditions.

Distribution Channel Insights

Seafood wholesalers remain the dominant distribution channel, accounting for nearly 36% of global market value. Their leadership is driven by their central role in facilitating the movement of fresh squid from harvesting fleets and processors to retailers, foodservice operators, and industrial buyers. Wholesalers provide critical cold-chain infrastructure, inventory management capabilities, and logistical expertise that enable efficient distribution across domestic and international markets. The fragmented nature of seafood supply chains further reinforces the importance of wholesalers in ensuring consistent product availability and quality.Direct business-to-business sales continue gaining momentum as large exporters, integrated seafood companies, and major processors increasingly establish direct supply relationships with restaurants, hospitality groups, and food manufacturing companies. This distribution model offers greater pricing transparency, improved supply reliability, and stronger quality control while reducing intermediary costs. The growing adoption of digital procurement platforms is further supporting the expansion of direct sales channels across global seafood markets.Online seafood platforms represent one of the fastest-growing distribution channels, supported by rapid advancements in cold-chain logistics, last-mile delivery infrastructure, and e-commerce penetration. Growing consumer confidence in online food purchasing, combined with increasing demand for home-delivered fresh seafood products, continues to create significant opportunities for digital seafood retailers and direct-to-consumer suppliers.

End-Use Insights

The foodservice segment remains the largest end-use category, representing approximately 48% of total global demand. The segment's dominance is driven by the extensive use of fresh squid across restaurants, hotels, catering services, seafood chains, and quick-service establishments. Squid's versatility, affordability relative to several premium seafood species, and strong consumer acceptance across diverse cuisines make it a preferred ingredient for foodservice operators worldwide. The continued expansion of seafood-focused dining concepts, Asian cuisine restaurants, and calamari-based menu offerings further supports segment growth.The seafood processing industry represents another important end-use segment, utilizing fresh squid in chilled seafood products, frozen preparations, ready-to-cook meals, and value-added seafood applications. Processors benefit from squid's adaptability across multiple product formats, enabling manufacturers to meet evolving consumer preferences for convenience-oriented seafood products. Demand from this segment is expected to remain strong as seafood companies continue investing in product innovation and value-added processing capabilities.Institutional buyers, including cruise operators, corporate catering providers, educational institutions, healthcare facilities, and hospitality groups, also contribute significantly to market demand. Growing tourism activity, expansion of large-scale catering operations, and increasing incorporation of seafood into institutional meal programs are expected to support sustained demand from this segment over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Fresh Squid Market Segmentations

By Product Form

- Whole Fresh Squid

- Cleaned Fresh Squid

- Fresh Squid Tubes

- Fresh Squid Rings & Portions

- Value-Added Fresh Squid

By Species

- Japanese Flying Squid

- Argentine Shortfin Squid

- European Squid

- Humboldt Squid

- Market Squid

- Other Commercial Squid Species

By Catch Source

- Wild-Caught Fresh Squid

- Aquaculture/Farmed Fresh Squid

By Quality Grade

- Premium Export Grade

- Standard Commercial Grade

- Economy Grade

By Distribution Channel

- Direct B2B Sales

- Seafood Wholesalers

- Modern Retail & Supermarkets

- Traditional Fish Markets

- Online Seafood Platforms

By End User

- Foodservice/HoReCa

- Household Retail Consumption

- Seafood Processing Industry

- Institutional Buyers (Hotels, Catering Services & Cruise Operators)

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global fresh squid market with approximately 54% market share, making it both the largest consumption and production hub worldwide. China represents the largest consuming and processing market globally, supported by strong seafood consumption patterns, extensive seafood processing infrastructure, and significant domestic distribution networks. Japan remains one of the highest-value importers and consumers of premium squid products, while South Korea records among the highest per-capita squid consumption rates globally. Thailand, Vietnam, Indonesia, and India continue strengthening their positions as important seafood processing and export centers, supported by growing investments in seafood processing facilities and export-oriented production capabilities.Regional growth is being driven by rising seafood consumption across densely populated economies, increasing disposable incomes, rapid urbanization, expanding middle-class populations, and strong cultural preferences for squid-based cuisine. The region also benefits from extensive fishing activities, well-established seafood supply chains, expanding cold-storage infrastructure, growing foodservice industries, and increasing exports to North America and Europe. Continuous investments in aquaculture-related infrastructure, seafood processing modernization, and cross-border seafood trade are expected to further reinforce Asia-Pacific's leadership position throughout the forecast period.

Europe

Europe accounts for approximately 22% of global market demand, led by Spain, Italy, Portugal, and France. Squid remains deeply embedded within Mediterranean culinary traditions, supporting consistently high levels of consumption across both household and foodservice sectors. Spain serves as one of the region's largest consumers, importers, and processors of squid products, benefiting from a well-developed seafood industry and strong domestic demand.Market growth across Europe is supported by increasing consumer preference for seafood-based diets, rising demand for high-quality and sustainably sourced seafood products, and continued expansion of premium foodservice establishments. Strong import dependence among several European countries creates substantial opportunities for international suppliers, while increasing emphasis on traceability, sustainability certifications, and responsible fishing practices encourages investment in quality assurance and supply chain transparency. Growth in tourism-related foodservice demand and the popularity of Mediterranean cuisine further contribute to market expansion across the region.

North America

North America contributes approximately 13% of global market value, with the United States representing the largest regional market. Demand is primarily driven by seafood restaurants, sushi chains, casual dining establishments, and premium retail seafood counters. Calamari remains one of the most widely consumed squid-based menu items across the region, contributing significantly to foodservice demand.Regional growth is being supported by increasing consumer awareness of seafood's nutritional benefits, growing popularity of international cuisines, rising demand for high-protein food products, and expanding seafood consumption among health-conscious consumers. The proliferation of Asian and Mediterranean restaurants, improvements in seafood distribution networks, and increasing availability of fresh seafood products through modern retail channels are further supporting market growth. Canada and Mexico continue contributing to regional demand through rising seafood imports, growing foodservice activity, and increasing consumer acceptance of premium seafood products.

Latin America

Latin America represents approximately 8% of the global fresh squid market. Argentina and Peru rank among the world's leading squid harvesting nations and serve as important suppliers to international markets, particularly Europe and Asia. The region plays a strategic role within global squid supply chains due to its abundant marine resources and export-oriented fishing industry.Regional market growth is driven by expanding seafood exports, increasing investments in fisheries modernization, rising processing capacity, and growing participation in international seafood trade. Domestic seafood consumption is also increasing across several Latin American countries as urbanization, income growth, and changing dietary preferences encourage greater seafood intake. Improvements in cold-chain infrastructure and government support for fisheries development are expected to further strengthen the region's contribution to global market growth.

Middle East & Africa

The Middle East & Africa accounts for approximately 3% of global market share but continues to present attractive growth opportunities. Morocco remains a major harvesting and export hub, supplying squid products to key international markets. Meanwhile, countries such as the United Arab Emirates and Saudi Arabia are experiencing rising seafood consumption driven by demographic growth, increasing disposable incomes, and evolving dietary preferences.Regional growth is supported by rapid expansion of the hospitality and tourism sectors, increasing demand for premium seafood products, rising seafood imports, and ongoing investments in modern retail infrastructure. The development of luxury hotels, resorts, restaurants, and foodservice establishments across Gulf Cooperation Council countries continues to stimulate demand for fresh squid. Additionally, government initiatives aimed at strengthening food security, improving seafood distribution networks, and diversifying food supply sources are expected to support long-term market expansion throughout the Middle East and Africa.

Key Players in the Fresh Squid Market

- Thai Union Group

- Nueva Pescanova

- Maruha Nichiro Corporation

- Nissui Corporation

- Royal Greenland

- Qingdao Seaflying Food

- Lee Fishing Company

- Seafood Pride International

- Xiamen Taiseng Seafoods

- Bigsams

- Freshkatch

- Seaquest Fisheries

- Holmes Seafood

- Minh Khue Seafood

- Holt Seafood