Sweet Paprika Powder Market Size

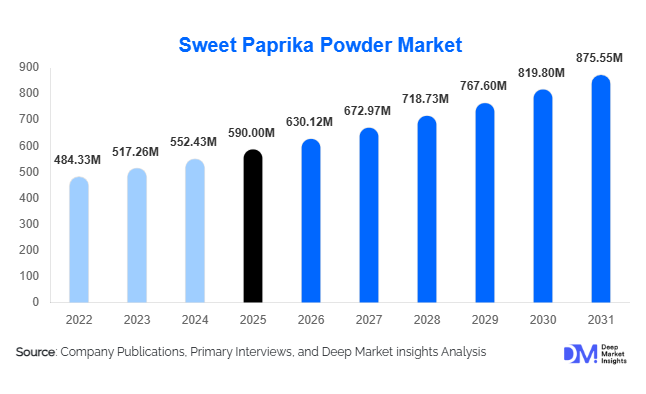

According to Deep Market Insights, the global sweet paprika powder market size was valued at USD 590 million in 2025 and is projected to grow from USD 630.12 million in 2026 to reach USD 875.55 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The sweet paprika powder market growth is primarily driven by increasing demand for natural food colorants, growing consumption of processed foods, expansion of clean-label product formulations, and rising adoption of paprika-based ingredients across food manufacturing, foodservice, nutraceutical, and specialty seasoning applications. Sweet paprika powder continues to gain traction as food processors seek multifunctional ingredients capable of providing both flavor enhancement and natural coloration while complying with evolving consumer preferences for minimally processed and naturally sourced ingredients.

Key Market Insights

- Natural food colorant substitution is accelerating globally, creating strong demand for sweet paprika powder as an alternative to synthetic dyes in processed foods and beverages.

- Processed meat, poultry, and seafood applications remain the largest consumption segment, accounting for nearly one-third of global demand.

- Europe dominates the global market, supported by strong culinary traditions, advanced food processing industries, and major paprika-producing countries such as Spain and Hungary.

- Asia-Pacific is the fastest-growing regional market, driven by expanding packaged food production and increasing consumer spending on convenience foods.

- Organic sweet paprika powder is emerging as a premium category, benefiting from rising consumer interest in traceable and sustainably sourced spices.

- Advanced processing technologies and ASTA-standard color grading systems are improving product consistency and enabling suppliers to secure premium contracts with multinational food manufacturers.

Sweet Paprika Powder Market Latest Trends

Growing Adoption of Natural Color Ingredients

The global food industry is witnessing a significant shift away from artificial food additives, creating strong demand for naturally derived color solutions. Sweet paprika powder has emerged as one of the most widely used natural red-orange coloring ingredients due to its ability to provide both visual appeal and flavor enhancement. Food manufacturers are increasingly incorporating paprika powder into processed meats, snacks, sauces, dressings, and ready meals to satisfy clean-label requirements. Regulatory scrutiny of synthetic food colors across Europe and North America has accelerated this trend. Manufacturers are investing in high-ASTA paprika varieties and standardized extraction processes to improve color consistency and support large-scale industrial adoption.

Premiumization and Organic Spice Expansion

Consumer preferences are increasingly shifting toward premium and organic food ingredients. Organic sweet paprika powder is experiencing rapid growth as food brands seek differentiated offerings supported by sustainable farming practices and traceable supply chains. Premium paprika products featuring geographic indications, origin certifications, and enhanced color specifications are gaining popularity among specialty food manufacturers and foodservice operators. Organic paprika commands significant price premiums compared with conventional products, encouraging growers and processors to expand certified production acreage. This trend is expected to continue as consumers increasingly prioritize ingredient transparency and environmental sustainability.

Sweet Paprika Powder Market Drivers

Rising Demand for Clean-Label Food Products

Consumer demand for clean-label products continues to reshape ingredient procurement strategies across the global food industry. Sweet paprika powder serves as a multifunctional ingredient that provides natural flavor and color while supporting ingredient simplification initiatives. Major food manufacturers are reformulating products to eliminate synthetic additives, creating new opportunities for paprika suppliers. Growth in premium packaged foods, organic products, and health-conscious consumer segments is further supporting market expansion. Food processors increasingly view paprika as a strategic ingredient that enhances product appeal while aligning with evolving regulatory and consumer expectations.

Expansion of Global Processed Food Production

The continued growth of processed food manufacturing remains a major driver of sweet paprika powder consumption. The ingredient is extensively used in meat processing, snack manufacturing, seasoning blends, sauces, frozen foods, and convenience meals. Rapid urbanization, changing lifestyles, and growing demand for ready-to-eat products are increasing industrial demand across both developed and emerging markets. Countries including China, India, Brazil, Indonesia, and Mexico are experiencing strong growth in food processing capacity, creating substantial opportunities for paprika suppliers serving industrial customers.

Increasing Popularity of Ethnic and International Cuisines

Consumer interest in Mediterranean, Spanish, Hungarian, Mexican, and Middle Eastern cuisines continues to expand globally. Sweet paprika powder is a core ingredient in many traditional recipes and seasoning systems associated with these cuisines. Restaurants, foodservice operators, and packaged food manufacturers are increasingly incorporating paprika-based flavors into new product launches. This trend is helping expand paprika consumption beyond traditional markets and creating broader global demand.

Sweet Paprika Powder Market Restraints

Raw Material Supply Volatility

Sweet paprika production remains highly dependent on agricultural conditions in key producing countries including Spain, Hungary, China, India, and Peru. Weather variability, drought conditions, crop diseases, and changing climatic patterns can significantly impact paprika yields and quality. Such disruptions create pricing volatility throughout the supply chain and challenge procurement planning for industrial buyers. Maintaining supply stability remains a critical concern for market participants.

Quality Standardization and Adulteration Concerns

The industry faces ongoing challenges related to product consistency, color intensity variation, and adulteration risks. Industrial buyers increasingly require strict compliance with ASTA color standards, food safety certifications, and traceability requirements. Meeting these specifications requires significant investments in quality control systems, laboratory testing, and supplier verification programs. Smaller producers may struggle to meet evolving customer expectations, limiting market participation and increasing compliance costs.

Sweet Paprika Powder Industry Key Opportunities

Natural Colorant Replacement Programs

The ongoing replacement of synthetic food colorants represents one of the most significant opportunities within the sweet paprika powder market. Global food manufacturers are actively seeking plant-based alternatives that provide consistent coloring performance while supporting clean-label claims. Sweet paprika powder offers an attractive solution due to its dual functionality as both a flavoring and coloring ingredient. Suppliers capable of delivering standardized color specifications and reliable supply chains are expected to benefit from long-term growth opportunities in this segment.

Emerging Market Food Processing Expansion

Rapid growth in food manufacturing industries across Asia-Pacific, Latin America, and the Middle East is creating new demand centers for sweet paprika powder. Rising disposable incomes, urbanization, and increasing consumption of packaged foods are driving investment in food processing facilities throughout these regions. New entrants can capitalize on these opportunities by developing localized production, sourcing, and distribution networks that support regional food manufacturers. As processed food consumption continues to rise, paprika demand is expected to increase proportionately across multiple application categories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 590.00 Million |

| Market Size in 2026 | USD 630.12 Million |

| Market Size in 2031 | USD 875.55 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Grade Insights

Food-grade sweet paprika powder continues to dominate the global market, contributing approximately 46% of global revenue in 2025. Its leadership is primarily driven by its extensive functional versatility in processed food manufacturing, where it is widely used in seasoning blends, snack coatings, sauces, and ready-to-eat formulations. The leading growth driver for this segment is the accelerating shift toward natural colorants and clean-label reformulation across global food processing industries, as manufacturers actively replace synthetic additives with plant-derived ingredients that meet evolving regulatory and consumer expectations.Premium culinary-grade paprika is witnessing steady expansion, supported by rising demand from specialty food producers and foodservice operators seeking enhanced color vibrancy, flavor depth, and product differentiation. This segment benefits from the broader premiumization trend in global cuisine, where authenticity and sensory appeal are increasingly prioritized. Industrial-grade paprika continues to play a critical role in large-scale manufacturing environments where cost optimization, supply consistency, and functional performance are the primary procurement criteria, particularly in mass-produced seasoning systems and processed protein applications. Organic-certified paprika represents the fastest-growing product category, driven by sustainability-focused sourcing mandates, increasing consumer preference for traceable ingredients, and the rapid expansion of organic food product portfolios across retail and foodservice channels.

Application Insights

Meat, poultry, and seafood processing remains the dominant application segment, accounting for approximately 28% of the global sweet paprika powder market. The leading driver of growth within this segment is the increasing demand for naturally enhanced coloration and flavor standardization in processed protein products, particularly in sausages, cured meats, marinades, and value-added seafood formulations. Paprika’s functional role as both a natural coloring agent and flavor enhancer has positioned it as an essential ingredient in reformulated meat systems targeting clean-label compliance.Snacks and savory foods represent a rapidly expanding application area, fueled by rising global consumption of flavored chips, extruded snacks, and ready-to-eat convenience foods. The primary growth driver in this category is the strong consumer preference for bold, natural flavor profiles and ethnic-inspired seasoning blends. Sauce, dressing, and condiment applications continue to grow steadily, supported by increasing demand for visually appealing, naturally colored formulations in both retail and foodservice segments. Nutraceutical and functional food applications are emerging as a high-growth frontier, driven by scientific interest in paprika-derived antioxidants and carotenoid compounds, which are increasingly incorporated into wellness-oriented formulations and functional dietary products.

Distribution Channel Insights

Direct B2B sales remain the dominant distribution channel, accounting for approximately 57% of total global revenue. The leading growth driver for this channel is the increasing reliance of large-scale food manufacturers on long-term procurement contracts that ensure consistent quality standards, supply chain stability, and cost predictability in volatile raw material markets. These agreements are particularly critical for multinational food processors operating across multiple production facilities.Ingredient distributors continue to play a vital intermediary role, especially in serving mid-sized manufacturers and regional food processors that require flexible order quantities and diversified sourcing options. Retail distribution channels are expanding steadily, driven by rising consumer interest in gourmet cooking, home experimentation with global cuisines, and increased availability of premium spice assortments in supermarkets and specialty stores. E-commerce has emerged as a structurally important growth channel, particularly for organic and specialty paprika products, as digital platforms enable producers to directly reach niche consumer segments, culinary enthusiasts, and health-conscious buyers seeking high-quality ingredients.

End-User Insights

Food manufacturers represent the largest end-user segment, accounting for approximately 51% of global market demand. The leading driver for this segment is the widespread reformulation of processed food products toward natural ingredient systems, particularly in snacks, ready meals, sauces, and protein-based foods. Manufacturers are increasingly integrating paprika powder as a multifunctional ingredient that delivers both color and flavor enhancement while aligning with clean-label requirements.Foodservice operators constitute a significant secondary end-user segment, supported by the expansion of global restaurant chains, ethnic cuisine popularity, and increasing demand for standardized seasoning profiles across commercial kitchens. Nutraceutical manufacturers represent a high-growth segment, driven by rising incorporation of natural antioxidants and plant-based compounds into dietary supplements and functional health products. Cosmetic and personal care manufacturers are also exploring paprika-derived natural colorants for use in formulations such as lip products, skincare enhancements, and herbal-based cosmetic lines, further broadening the industrial application landscape.

Explore more data points, trends and opportunities Download Free Sample Report

Sweet Paprika Powder Market Segmentations

By Product Grade

- Food Grade Sweet Paprika Powder

- Premium Culinary Grade Sweet Paprika Powder

- Industrial Processing Grade Sweet Paprika Powder

- Organic Certified Sweet Paprika Powder

By Cultivation Type

- Conventional Sweet Paprika Powder

- Organic Sweet Paprika Powder

By Color Intensity

- Low Color Intensity

- Medium Color Intensity

- High Color Intensity

By Application

- Meat, Poultry & Seafood Processing

- Snacks & Savory Foods

- Sauces, Dressings & Condiments

- Ready Meals & Processed Foods

- Bakery & Savory Confectionery

- Spice Blends & Seasonings

- Foodservice & Catering

- Nutraceuticals & Functional Foods

- Cosmetics & Personal Care

- Pharmaceutical Preparations

By Distribution Channel

- Direct/B2B Sales

- Ingredient Distributors

- Retail Stores

- Supermarkets & Hypermarkets

- Specialty Food Stores

- E-commerce Platforms

Regional Insights

North America

North America accounted for approximately 21% of the global sweet paprika powder market in 2025. The leading growth driver in this region is the accelerating shift toward clean-label and natural ingredient adoption across a highly developed processed food industry. The United States remains the dominant consumer market, where manufacturers are increasingly replacing synthetic colorants with paprika in snacks, sauces, and processed meat products in response to regulatory pressures and evolving consumer preferences. Canada contributes to steady growth through rising demand for premium seasoning products and expanding packaged food consumption, while Mexico benefits from a growing food processing base and increasing export-oriented meat production activities.

Europe

Europe remains the largest regional market, representing approximately 39% of global demand in 2025. The primary growth driver is the combination of strong culinary heritage and stringent regulatory frameworks promoting natural and clean-label ingredients. Countries such as Spain, Germany, France, Italy, Hungary, and the United Kingdom serve as both major consumption and production hubs. Spain and Hungary, in particular, play a strategic role in global supply due to favorable agro-climatic conditions and established paprika cultivation expertise. Demand is further reinforced by the rapid expansion of premium food categories and the increasing preference for authentic, natural spice profiles in both household and industrial applications.

Asia-Pacific

Asia-Pacific accounted for approximately 28% of the global market in 2025 and is projected to remain the fastest-growing regional segment with a forecast CAGR exceeding 8.2%. The leading driver of growth in this region is rapid urbanization combined with the expansion of modern food processing industries and rising exposure to international cuisines. China, India, Japan, South Korea, Indonesia, and Thailand are key demand centers, with increasing consumption of packaged foods, convenience meals, and flavored snack products. India is expected to emerge as the fastest-growing country market globally, supported by strong domestic food manufacturing expansion, evolving retail infrastructure, and rising consumer demand for spice-rich processed foods aligned with both traditional and modern dietary preferences.

Latin America

Latin America represented approximately 7% of global market demand in 2025. The primary growth driver is the expansion of processed food and meat export industries, particularly in Brazil and Mexico. These countries benefit from strong agricultural bases and growing investments in food manufacturing infrastructure. Regional growth is also supported by increasing adoption of paprika in locally developed seasoning blends and packaged snack products, as manufacturers respond to rising urbanization and shifting dietary patterns toward convenience foods and value-added processed products.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5% of global demand in 2025. The leading driver of growth is the rapid expansion of foodservice sectors, supported by increasing tourism activity, urban population growth, and rising penetration of international restaurant chains. Saudi Arabia, the UAE, South Africa, and Egypt are key markets where demand for processed foods and imported food ingredients continues to rise. Additionally, ongoing investments in domestic food manufacturing infrastructure and supply chain modernization are expected to enhance long-term market penetration of paprika-based seasoning products across the region.

Key Players in the Sweet Paprika Powder Market

- McCormick & Company

- Synthite Industries

- Plant Lipids

- Chr. Hansen

- Olam Food Ingredients

- Paprimur S.L.

- Kalsec

- Foodchem International

- EVESA

- Naturex

- Döhler

- Givaudan

- Universal Oleoresins

- Lay Gewürze

- Ingredients Network Paprika Producers Group