B2B Food for Foodservice Market Size

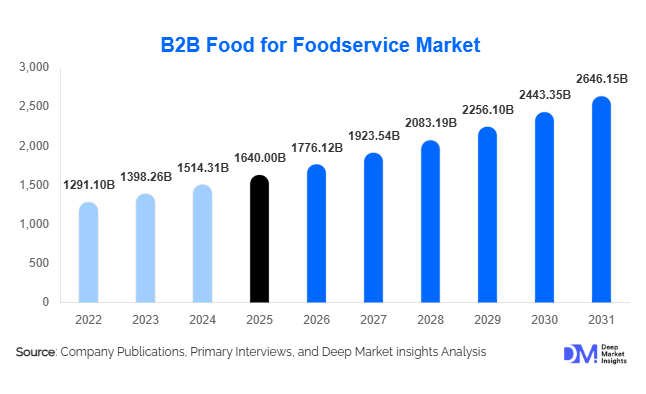

According to Deep Market Insights, the global B2B food for foodservice market size was valued at USD 1,640.0 billion in 2025 and is projected to grow from USD 1,776.12 billion in 2026 to reach USD 2,646.15 billion by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of organized foodservice chains, increasing penetration of cloud kitchens and delivery-first brands, and the ongoing digital transformation of procurement systems across the hospitality and institutional catering industries.

Key Market Insights

- Processed and semi-prepared food products dominate procurement, driven by demand for consistency, scalability, and reduced preparation time across QSR and cloud kitchen operations.

- Asia-Pacific leads the global market, supported by rapid urbanization, expansion of organized foodservice, and strong growth in digital food delivery ecosystems.

- Online B2B procurement platforms are the fastest-growing distribution channel, improving pricing transparency, inventory management, and supplier access.

- Cold chain infrastructure expansion is transforming supply capabilities, enabling efficient distribution of perishable food products across long distances.

- Contract-based procurement dominates purchasing models, ensuring price stability and long-term supplier relationships for large foodservice operators.

- Sustainability and traceability are becoming key differentiators, with increasing demand for organic, plant-based, and ethically sourced ingredients.

What are the latest trends in the B2B food for foodservice market?

Digitalization of Procurement and Supply Chains

The adoption of digital platforms is revolutionizing the B2B food procurement landscape. Foodservice operators are increasingly leveraging online marketplaces, ERP-integrated ordering systems, and AI-driven demand forecasting tools to streamline procurement processes. These platforms provide real-time visibility into pricing, inventory levels, and delivery schedules, significantly improving operational efficiency. Suppliers are also integrating predictive analytics to optimize supply chains, reduce wastage, and enhance fulfillment rates. This shift toward digital procurement is particularly beneficial for small and mid-sized foodservice businesses, enabling them to access a broader supplier base and competitive pricing structures.

Rising Demand for Ready-to-Cook and Processed Ingredients

Foodservice operators are increasingly adopting ready-to-cook (RTC) and ready-to-eat (RTE) ingredients to reduce preparation time, minimize labor costs, and ensure consistency across outlets. This trend is especially prominent among quick service restaurants and cloud kitchens, which rely on standardized recipes and high operational efficiency. Suppliers are responding by offering customized, semi-processed food solutions tailored to specific cuisines and menu requirements. The demand for value-added processed food products is expected to continue growing as foodservice operators prioritize speed, scalability, and cost efficiency.

What are the key drivers in the B2B food for foodservice market?

Expansion of Organized Foodservice Chains

The rapid growth of global QSR and FSR chains is a major driver of the B2B food for foodservice market. These chains require standardized, high-volume procurement of ingredients to maintain consistency across locations. Their expansion into emerging markets is further driving demand for structured B2B supply networks. Centralized procurement strategies adopted by these chains are increasing reliance on professional suppliers, boosting overall market growth.

Growth of Cloud Kitchens and Delivery Platforms

The proliferation of cloud kitchens and food delivery platforms is significantly influencing procurement patterns. These models depend heavily on centralized sourcing and frequent replenishment, creating strong demand for reliable B2B suppliers. The scalability of cloud kitchen operations is directly linked to efficient supply chains, making B2B food sourcing a critical component of their business models. This segment is among the fastest-growing contributors to market demand.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in the prices of key commodities such as grains, dairy, and meat pose significant challenges for B2B food suppliers. Price volatility impacts profit margins and creates uncertainty in long-term contracts, making it difficult for suppliers to maintain stable pricing structures. This challenge is particularly pronounced in regions with limited domestic production and high reliance on imports.

Fragmentation in Emerging Markets

In many developing regions, the presence of unorganized suppliers and inconsistent supply chains acts as a barrier to market growth. Lack of standardization, quality control issues, and logistical inefficiencies hinder the adoption of organized B2B procurement systems. Overcoming these challenges requires investment in infrastructure, regulatory frameworks, and supplier consolidation.

What are the key opportunities in the B2B food for foodservice industry?

Growth of Cloud Kitchen Ecosystems

The rapid expansion of cloud kitchens presents a significant opportunity for B2B food suppliers. These businesses rely on centralized procurement and standardized inputs, creating strong demand for bulk, consistent, and semi-processed ingredients. Suppliers that can offer customized product solutions, efficient logistics, and reliable delivery schedules are well-positioned to capitalize on this trend. The scalability of cloud kitchens further amplifies long-term demand potential.

Adoption of Sustainable and Clean-Label Products

Sustainability is becoming a key focus area for foodservice operators. Increasing demand for organic, plant-based, and ethically sourced ingredients is creating new growth avenues for suppliers. Regulatory support in regions such as Europe is further accelerating this trend. Suppliers investing in sustainable sourcing, eco-friendly packaging, and transparent supply chains can gain a competitive advantage in this evolving market landscape.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1640 Billion |

| Market Size in 2026 | USD 1776.12 Billion |

| Market Size in 2031 | USD 2646.15 Billion |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Category Insights

The global foodservice sourcing and procurement market is strongly anchored by processed food products, which account for approximately 34% of the total market share in 2025. This dominance reflects a structural shift in how foodservice operators prioritize efficiency, consistency, and scalability in an increasingly competitive landscape. Processed food products offer standardized quality, extended shelf life, and reduced preparation time, making them indispensable for high-volume operations such as Quick Service Restaurants (QSRs), cloud kitchens, and institutional catering. The ability to maintain uniform taste profiles across multiple locations is particularly critical for franchise-based models, where brand consistency directly impacts customer loyalty and repeat purchases. In addition, processed foods significantly reduce dependency on skilled labor, addressing workforce shortages that are becoming more prevalent across both developed and emerging economies.The leading driver behind the processed food segment is the growing need for operational efficiency and cost optimization within foodservice establishments. Rising labor costs, increasing demand volatility, and the need for faster service turnaround have collectively pushed operators toward pre-prepared and semi-processed inputs. Furthermore, advancements in food processing technologies, including freezing, vacuum sealing, and modified atmosphere packaging, have enhanced product quality while preserving nutritional value, making processed options more appealing even to premium segments.Specialty and functional food categories, including plant-based proteins, organic ingredients, gluten-free options, and fortified foods, are emerging as high-growth segments. This growth is fueled by evolving consumer preferences toward healthier, sustainable, and ethically sourced products. Foodservice operators are increasingly incorporating such offerings into their menus to cater to health-conscious consumers, thereby expanding their addressable market and enhancing brand differentiation.

Buyer Type Insights

Quick Service Restaurants (QSRs) dominate the buyer landscape, contributing nearly 28% of total demand in 2025. Their leadership position is driven by their standardized operating models, centralized procurement systems, and continuous expansion across urban and semi-urban markets. QSR chains rely heavily on bulk purchasing agreements and long-term supplier partnerships to ensure consistent quality and cost efficiency. The leading driver for this segment is the rapid global expansion of organized fast-food chains, coupled with increasing consumer preference for convenience dining and on-the-go consumption patterns.Full-service restaurants represent the next significant buyer category, characterized by a more diverse sourcing strategy that balances quality, variety, and cost. These establishments often procure a mix of fresh, processed, and specialty ingredients to deliver differentiated dining experiences. Their demand patterns are influenced by evolving culinary trends, seasonal menus, and the growing emphasis on premiumization.Institutional foodservice, including hospitals, educational institutions, corporate cafeterias, and government facilities, provides a stable and recurring demand base. This segment is driven by long-term contracts, predictable consumption patterns, and a focus on cost control and nutritional compliance. The expansion of corporate campuses and healthcare infrastructure globally continues to support sustained growth in this category.

Distribution Channel Insights

Wholesale distributors remain the dominant distribution channel, accounting for approximately 36% of the market. Their stronghold is attributed to their ability to aggregate products from multiple suppliers, offer extensive product portfolios, and provide value-added services such as logistics management, credit facilities, and inventory support. The leading driver for this segment is the need for supply chain consolidation and reliability, particularly for small and medium-sized foodservice operators that lack the scale to procure directly from manufacturers.At the same time, online B2B marketplaces are experiencing rapid growth, reshaping traditional procurement models. These platforms offer enhanced transparency, competitive pricing, and real-time inventory visibility, enabling foodservice operators to make data-driven purchasing decisions. The increasing adoption of digital technologies, coupled with improved internet penetration and mobile accessibility, is a key driver accelerating the growth of this channel.Direct manufacturer-to-foodservice supply is also gaining traction, particularly among large restaurant chains and institutional buyers. This model allows for better cost control, improved quality assurance, and stronger supplier relationships. As supply chains become more integrated and technologically advanced, direct sourcing is expected to expand further, especially in mature markets.

Supply Chain Insights

The supply chain landscape is increasingly defined by the prominence of cold chain logistics, which account for around 42% of the market. This reflects the growing demand for perishable products such as meat, seafood, dairy, and frozen foods. The leading driver for this segment is the rising consumption of protein-rich and convenience food products, which require strict temperature control to maintain quality and safety standards.Significant investments in cold storage infrastructure, refrigerated transportation, and last-mile delivery solutions are enabling suppliers to expand their geographic reach and reduce wastage. Emerging markets, in particular, are witnessing rapid development in cold chain capabilities, supported by government initiatives and private sector investments.Hybrid supply chain models are also gaining importance, combining ambient and cold storage solutions to optimize operational efficiency. These models allow suppliers to handle a diverse range of products while minimizing costs and improving responsiveness. The integration of advanced technologies such as IoT-enabled tracking, real-time monitoring, and predictive analytics is further enhancing supply chain visibility and reliability.

Pricing Model Insights

Volume-based pricing continues to dominate the market, accounting for approximately 48% share. This model aligns well with the bulk purchasing practices of foodservice operators, enabling them to achieve economies of scale and reduce per-unit costs. The primary driver for this segment is the inherent need for cost optimization in a highly competitive industry where margins are often tight.Contract-based pricing models are widely adopted by large-scale operators, providing price stability and supply assurance over extended periods. These agreements help mitigate risks associated with price volatility and supply disruptions, particularly for essential commodities.Dynamic pricing models are gaining relevance in response to fluctuating commodity prices and market uncertainties. By linking prices to real-time market conditions, suppliers and buyers can achieve greater flexibility and responsiveness. The increasing use of data analytics and digital procurement platforms is facilitating the adoption of such models, enabling more accurate forecasting and pricing strategies.

Explore more data points, trends and opportunities Download Free Sample Report

B2B Food for Foodservice Market Segmentations

By Product Category

- Fresh Food Products

- Processed Food Products

- Dry & Ambient Food Products

- Beverages )

- Specialty & Functional Foods

By Foodservice Buyer Type

- Quick Service Restaurants (QSRs)

- Full-Service Restaurants (FSRs)

- Cloud Kitchens & Delivery-Only Brands

- Institutional Foodservice

- Hotels & Catering Services

- Travel & Leisure Foodservice

By Distribution Channel

- Direct Manufacturer-to-Foodservice

- Wholesale Distributors

- Cash & Carry Stores

- Online B2B Marketplaces

- Integrated Supply Chain Platforms

By Supply Chain Type

- Cold Chain Supply

- Ambient Supply

- Hybrid Supply Chain

By Pricing Model

- Volume-Based Pricing

- Contract-Based Pricing

- Dynamic Pricing

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with approximately 38% share in 2025, making it the most dynamic and rapidly evolving region. China dominates the regional landscape due to its vast and highly fragmented restaurant industry, which continues to expand alongside rising urbanization and income levels. India represents the fastest-growing market within the region, driven by a combination of demographic advantages, increasing disposable incomes, and the rapid proliferation of digital food delivery platforms. The growth of organized foodservice chains and the expansion of cloud kitchen models are further accelerating demand for standardized and scalable sourcing solutions.Key growth drivers in Asia-Pacific include rapid urbanization, changing dietary habits, and the increasing penetration of smartphones and internet connectivity, which have transformed how consumers interact with foodservice providers. The rising middle-class population is also contributing to higher spending on dining out and convenience foods. In addition, government initiatives aimed at improving supply chain infrastructure, particularly cold storage and logistics, are supporting market expansion. Countries such as Japan and those in Southeast Asia continue to play a significant role, driven by strong demand for convenience foods, innovation in food processing, and a well-established culture of dining out.

North America

North America accounts for around 27% of the market, with the United States serving as the primary growth engine. The region benefits from a highly developed and technologically advanced supply chain ecosystem, enabling efficient sourcing, storage, and distribution of food products. The high penetration of QSR chains, coupled with strong consumer demand for convenience and quick-service dining, continues to drive market growth.Key drivers in North America include the widespread adoption of digital procurement systems, which enhance efficiency and transparency in sourcing processes. The region is also characterized by a high level of innovation, with foodservice operators increasingly incorporating automation, data analytics, and AI-driven solutions into their operations. Additionally, the growing emphasis on sustainability, traceability, and clean-label products is influencing sourcing strategies, encouraging suppliers to adopt more transparent and environmentally friendly practices. Canada complements regional growth with steady demand from institutional foodservice and a growing focus on health-oriented menu offerings.

Europe

Europe holds approximately 22% share of the global market, with key countries such as Germany, France, and the United Kingdom leading demand. The region is characterized by a mature foodservice industry, strong regulatory frameworks, and a high level of consumer awareness regarding food quality and sustainability.The primary growth drivers in Europe include increasing demand for organic, locally sourced, and sustainably produced food products. Stringent regulations related to food safety and environmental impact are shaping procurement practices, encouraging the adoption of traceable and ethically sourced ingredients. Additionally, the growing popularity of plant-based diets and alternative proteins is influencing product offerings across the foodservice sector. Technological advancements in supply chain management and the integration of digital platforms are further enhancing efficiency and supporting market growth.

Middle East & Africa

The Middle East & Africa region is experiencing rapid growth, driven by significant investments in tourism, hospitality, and infrastructure development. Countries such as the United Arab Emirates and Saudi Arabia are at the forefront of this expansion, supported by government-led initiatives aimed at diversifying their economies and boosting the hospitality sector.Key drivers in this region include rising disposable incomes, increasing urbanization, and a growing expatriate population, all of which contribute to higher demand for diverse dining options. The expansion of international restaurant chains and the development of large-scale hospitality projects are further fueling demand for reliable and efficient foodservice supply chains. In Africa, improving infrastructure and the gradual formalization of the foodservice sector are creating new growth opportunities, although challenges related to logistics and supply chain efficiency remain.

Latin America

Latin America accounts for nearly 8% of the global market, with Brazil and Mexico serving as key contributors. The region is characterized by a growing urban population, increasing consumer spending on dining out, and the gradual expansion of organized foodservice formats.The main growth drivers in Latin America include the rising adoption of QSR and fast-casual dining concepts, supported by changing lifestyles and increasing time constraints among urban consumers. Economic development and improving infrastructure are also contributing to market growth, enabling better distribution and supply chain management. Additionally, the growing influence of international cuisines and the expansion of global restaurant chains are shaping demand patterns, encouraging the adoption of standardized sourcing practices and processed food products.

Key Players in the B2B Food for Foodservice Market

- Sysco Corporation

- US Foods Holding Corp.

- Performance Food Group

- Nestlé S.A.

- Unilever Food Solutions

- Cargill Incorporated

- Archer Daniels Midland (ADM)

- JBS S.A.

- Tyson Foods Inc.

- Bidcorp Ltd.

- Metro AG

- Gordon Food Service

- Olam Group

- CJ CheilJedang

- Maruha Nichiro Corporation