Sugar Market Size

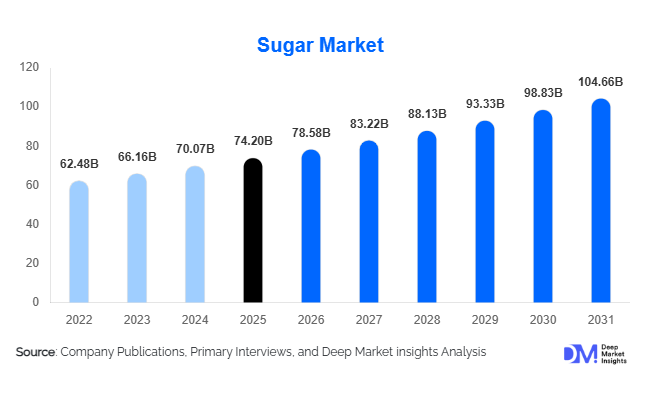

According to Deep Market Insights, the global sugar market size was valued at USD 74.2 billion in 2025 and is projected to grow from USD 78.58 billion in 2026 to reach USD 104.66 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The sugar market growth is primarily driven by rising demand from the processed food and beverage industry, increasing sugarcane-based ethanol production, and expanding industrial applications across pharmaceuticals, fermentation, and bio-based chemicals. Strong population growth in emerging economies, combined with urbanization and increasing packaged food consumption, continues to sustain long-term sugar demand globally.

Key Market Insights

- Sugarcane-based sugar dominates global production, accounting for the majority of market supply due to high cultivation volumes in Brazil, India, and Thailand.

- The food and beverage industry remains the largest consumer of sugar, driven by strong demand from bakery, confectionery, dairy, and soft drink manufacturers.

- Asia-Pacific dominates the global sugar market, supported by high domestic consumption, large-scale production capacity, and expanding food processing industries.

- The Middle East & Africa region is emerging as the fastest-growing market, fueled by increasing imports, population growth, and rising processed food demand.

- Biofuel integration is reshaping the market, particularly in Brazil and India, where ethanol blending mandates are increasing sugarcane utilization.

- Technological modernization in sugar mills, including automation, biomass cogeneration, and AI-driven crop monitoring, is improving production efficiency and sustainability.

Sugar Market Latest Trends

Expansion of Ethanol-Integrated Sugar Production

One of the most important trends shaping the global sugar market is the increasing integration of sugar and ethanol production. Governments worldwide are encouraging biofuel adoption to reduce carbon emissions and dependence on imported crude oil. Brazil continues to maintain a mature flex-fuel ecosystem where sugar mills dynamically shift sugarcane allocation between crystal sugar and ethanol depending on market profitability. India is aggressively expanding ethanol blending programs and investing heavily in distillery infrastructure under national biofuel policies. This trend is transforming sugar mills into integrated energy and biofuel complexes, enabling producers to diversify revenue streams while improving profitability stability during periods of sugar price volatility. Biomass-based power generation using bagasse is also becoming a key operational component within modern sugar manufacturing facilities.

Rising Demand for Organic and Specialty Sugar

Consumer preference for minimally processed and naturally sourced sweeteners is driving demand for specialty sugar categories including organic cane sugar, muscovado sugar, brown sugar, demerara sugar, and low-refined sugar variants. North America and Europe are leading adoption of premium sugar products as consumers increasingly prioritize clean-label ingredients and sustainable sourcing. Food manufacturers are incorporating premium sugar variants into artisanal bakery products, gourmet confectionery, beverages, and premium dairy formulations to improve product differentiation. Sustainability certifications, traceability programs, and ethical sourcing practices are becoming increasingly important purchasing factors for institutional buyers and retail consumers. This trend is enabling sugar producers to improve pricing realization and strengthen profit margins in value-added segments.

Sugar Market Drivers

Growth of Processed Food and Beverage Consumption

The rapid expansion of the global processed food and beverage industry remains one of the primary growth drivers for the sugar market. Sugar continues to play an essential role in bakery products, confectionery, dairy desserts, soft drinks, sauces, flavored beverages, and packaged foods because of its taste-enhancing, preservative, and fermentation properties. Rising urbanization, busy consumer lifestyles, and increasing disposable incomes in emerging economies are accelerating packaged food consumption globally. Countries such as India, Indonesia, Vietnam, China, and Nigeria are witnessing substantial growth in industrial sugar demand from food manufacturers. Large multinational beverage and confectionery companies continue to maintain stable procurement volumes, supporting long-term market expansion.

Increasing Biofuel and Ethanol Demand

Global biofuel initiatives are significantly increasing demand for sugarcane-derived ethanol. Governments are implementing ethanol blending mandates to reduce greenhouse gas emissions and strengthen energy security. Brazil remains the global leader in sugarcane ethanol production, while India is rapidly scaling ethanol capacity through policy incentives, distillery investments, and subsidized financing programs. Ethanol diversification allows sugar producers to optimize production economics by shifting feedstock allocation depending on sugar and crude oil price trends. This dual-demand structure is improving profitability across integrated sugar manufacturing operations and creating stable long-term demand for sugarcane cultivation.

Sugar Market Restraints

Health Concerns and Sugar Reduction Policies

Increasing health awareness related to obesity, diabetes, and excessive sugar consumption remains a major challenge for the global sugar market. Governments and health organizations across North America and Europe are implementing sugar taxes, stricter labeling regulations, and nutritional awareness campaigns targeting carbonated beverages and processed foods. Several multinational food manufacturers are reformulating products with reduced sugar content or alternative sweeteners to align with changing consumer preferences. These developments are slowing per-capita sugar consumption growth in mature economies and creating long-term pressure on traditional refined sugar demand.

Climate Volatility and Agricultural Risks

Sugarcane and sugar beet cultivation are highly vulnerable to climate variability, including droughts, floods, irregular rainfall, and rising temperatures. Major producing nations such as Brazil, India, and Thailand have experienced periodic production disruptions caused by unfavorable weather conditions. Volatility in agricultural yields directly impacts global sugar supply and pricing. In addition, rising fertilizer prices, labor costs, transportation expenses, and energy costs continue to pressure operational profitability for sugar mills and agricultural producers. Supply chain disruptions and export restrictions in producing countries further contribute to market uncertainty.

Sugar Industry Key Opportunities

Expansion of Renewable Energy and Biomass Integration

The growing focus on renewable energy is creating significant opportunities for integrated sugar producers. Sugar mills are increasingly utilizing bagasse, a byproduct of sugarcane processing, for biomass-based electricity generation. Several countries are supporting cogeneration infrastructure to improve renewable power capacity and reduce dependence on fossil fuels. Integrated sugar-energy complexes allow producers to diversify revenues while improving energy efficiency and operational sustainability. Investments in green energy production are expected to become a major competitive differentiator for leading sugar manufacturers globally.

Growth of Premium and Organic Sugar Segments

The premiumization trend within the food and beverage industry is opening new growth opportunities for specialty sugar products. Organic sugar, minimally processed brown sugar, and natural cane sugar variants are witnessing increasing demand from health-conscious and environmentally aware consumers. Food manufacturers are using specialty sugars to position products within premium and artisanal categories. Organic certification programs, traceable sourcing models, and sustainability-focused branding are enabling producers to access higher-margin consumer segments, particularly in North America and Europe.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 74.20 Billion |

| Market Size in 2026 | USD 78.58 Billion |

| Market Size in 2031 | USD 104.66 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Sugarcane sugar dominates the global sugar market, accounting for nearly 79% of total market revenue in 2025 due to favorable tropical cultivation conditions and strong production volumes in Brazil, India, and Thailand. Sugarcane remains the preferred feedstock because of higher extraction efficiency and its ability to support ethanol production alongside sugar refining. Sugar beet sugar maintains significant presence in Europe and North America, where climatic conditions support large-scale beet cultivation. Specialty natural sugars such as coconut sugar and palm sugar represent niche but rapidly growing segments driven by demand for alternative sweeteners and minimally processed products.

Product Type Insights

Refined white sugar remains the leading product category, representing approximately 52% of the global market in 2025 due to its extensive use in food processing, beverage manufacturing, confectionery, and retail consumption. Brown sugar and raw sugar segments are experiencing steady growth due to rising consumer preference for natural and less processed products. Specialty sugars such as muscovado, turbinado, and demerara sugar are gaining traction in premium bakery and gourmet food applications. Liquid sugar is increasingly utilized in beverage manufacturing because of operational convenience and faster dissolution properties.

Application Insights

The food industry remains the largest application segment, accounting for nearly 46% of global sugar demand in 2025. Bakery products, confectionery, dairy formulations, frozen desserts, and processed foods continue to drive substantial industrial sugar procurement volumes. The beverage segment represents approximately 24% market share due to high consumption of soft drinks, flavored beverages, juices, and energy drinks. Industrial applications including ethanol production, fermentation, and bio-based chemicals are emerging as important growth areas, particularly in Brazil and India where biofuel investments are expanding rapidly.

Distribution Channel Insights

Business-to-business (B2B) sales dominate the sugar market with more than 72% share in 2025, as industrial buyers procure sugar through long-term contracts and bulk purchasing agreements. Food manufacturers, beverage producers, pharmaceutical companies, and industrial processors represent the largest institutional buyers. Retail distribution channels including supermarkets, hypermarkets, convenience stores, and online platforms continue to expand, particularly in emerging markets where household sugar consumption remains high. E-commerce platforms are increasingly influencing retail sugar purchases by improving product visibility and direct consumer access.

End-Use Insights

Food and beverage processing remains the dominant end-use industry for sugar globally, accounting for nearly 65% of total market demand in 2025. The sector continues to expand due to rising packaged food consumption and growth in convenience-oriented lifestyles. The biofuel and ethanol industry is among the fastest-growing end-use segments, supported by aggressive ethanol blending mandates in Brazil, India, and Thailand. Pharmaceutical applications are also generating increasing demand for pharmaceutical-grade sugar used in medicinal syrups and fermentation processes. Cosmetics and personal care manufacturers are gradually incorporating sugar-derived ingredients into exfoliants and bio-based formulations.

Explore more data points, trends and opportunities Download Free Sample Report

Sugar Market Segmentations

By Source

- Sugarcane Sugar

- Sugar Beet Sugar

- Specialty and Alternative Natural Sugars

By Product Type

- White Sugar

- Brown Sugar

- Raw Sugar

- Liquid Sugar

- Powdered/Confectioners Sugar

- Specialty Sugars

By Form

- Granulated

- Powdered

- Syrup/Liquid

- Cubes

- Crystalline

By Processing Type

- Refined Sugar

- Unrefined Sugar

- Semi-Refined Sugar

By Nature

- Conventional Sugar

- Organic Sugar

- Non-GMO Sugar

Regional Insights

North America

North America accounted for approximately 17% of the global sugar market in 2025, led primarily by the United States. Strong demand from the food processing and beverage industries continues to support stable industrial sugar consumption despite increasing sugar reduction initiatives. Mexico remains an important regional supplier and exporter, while Canada maintains steady demand from confectionery and packaged food sectors. The region is also witnessing growing interest in organic and specialty sugar products driven by clean-label consumer preferences.

Europe

Europe represented nearly 19% of the global sugar market in 2025, supported by large-scale sugar beet cultivation and advanced food processing industries. Germany, France, the United Kingdom, and Poland remain major consumers and producers of sugar beet-based products. European demand growth is relatively moderate compared to Asia-Pacific due to mature consumption patterns and increasing health-conscious consumer behavior. However, specialty sugars, organic products, and sustainably sourced sugar continue to experience strong demand across premium food categories.

Asia-Pacific

Asia-Pacific dominates the global sugar market with approximately 43% share of total market revenue in 2025. India and China represent the largest regional consumers due to massive populations, expanding food manufacturing sectors, and rising disposable incomes. India is also one of the world’s largest sugar producers and exporters, supported by strong government incentives and ethanol integration policies. Thailand remains a major export-oriented producer, while Indonesia continues to depend heavily on sugar imports to meet domestic industrial demand. Rapid urbanization and increasing packaged food consumption are expected to sustain strong regional growth through 2031.

Latin America

Latin America remains one of the most strategically important sugar-producing regions globally, led overwhelmingly by Brazil. Brazil alone contributes nearly 18% of global sugar market revenue through domestic production and exports. The country benefits from highly efficient sugarcane farming, advanced ethanol infrastructure, and large-scale export competitiveness. Argentina and Colombia are also strengthening investments in sugar processing and ethanol integration. Export-driven production continues to support the region’s importance within global trade flows.

Middle East & Africa

The Middle East & Africa region is emerging as the fastest-growing market with forecast CAGR exceeding 6.5% through 2031. Saudi Arabia, the UAE, Egypt, and Nigeria are witnessing increasing demand for confectionery, packaged foods, and beverages due to population growth and rising urbanization. Most Gulf countries remain heavily dependent on imported sugar, creating stable long-term import demand. Africa is also experiencing gradual expansion in domestic sugar refining capacity as governments focus on improving food security and reducing import dependence.

Key Players in the Sugar Market

- Südzucker AG

- Tereos Group

- Cosan S.A.

- Wilmar International

- Mitr Phol Group

- Raízen S.A.

- Nordzucker AG

- Associated British Foods plc

- Thai Roong Ruang Group

- Shree Renuka Sugars Ltd.

- COFCO Sugar Holdings

- Tongaat Hulett

- Balrampur Chini Mills Ltd.

- American Crystal Sugar Company

- Ragus Sugars Manufacturing Ltd.