Strawberry Syrups Market Size

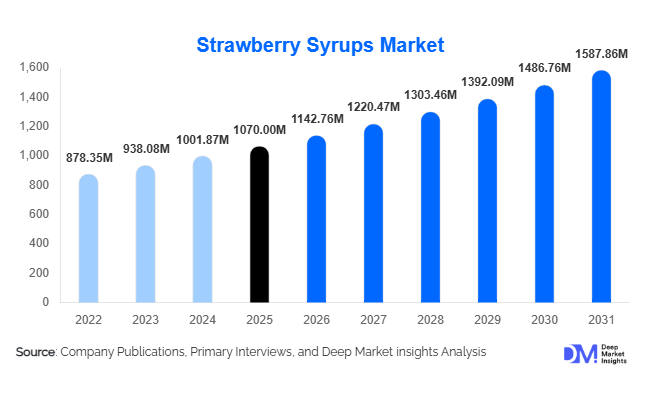

According to Deep Market Insights, the global strawberry syrups market size was valued at USD 1,070 million in 2025 and is projected to grow from USD 1,142.76 million in 2026 to reach USD 1,587.86 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The strawberry syrups market growth is primarily driven by increasing consumption of flavored beverages, rising demand for dessert toppings and bakery ingredients, the expansion of specialty café chains, and growing consumer preference for fruit-based flavoring solutions across food and beverage applications.

Key Market Insights

- Natural and clean-label strawberry syrups are gaining significant traction, driven by consumers seeking products made with real fruit extracts, natural colors, and fewer artificial ingredients.

- The beverage industry remains the largest application segment, with strawberry syrups increasingly used in milkshakes, smoothies, specialty coffees, cocktails, and ready-to-drink beverages.

- North America dominates the global market, supported by mature foodservice industries, strong café culture, and high household consumption of flavored syrups.

- Asia-Pacific is the fastest-growing regional market, led by rising middle-class populations, expanding quick-service restaurant chains, and increasing westernization of food consumption patterns.

- Premium and organic strawberry syrups are becoming important value-added segments, benefiting from growing consumer willingness to pay for healthier and artisanal products.

- Technological advancements in fruit extraction and sugar-reduction formulations are enabling manufacturers to launch innovative, low-calorie, and functional strawberry syrup products.

Strawberry Syrups Market Latest Trends

Shift Toward Natural and Clean-Label Formulations

Consumers are increasingly scrutinizing ingredient labels and seeking products with natural fruit ingredients, minimal preservatives, and clean-label formulations. This trend has significantly increased demand for strawberry syrups made with real fruit puree, natural colors, and reduced artificial additives. Manufacturers are reformulating products to eliminate synthetic preservatives and are increasingly promoting non-GMO, organic, and sustainably sourced ingredients. Premium foodservice operators and specialty cafés are also preferring natural syrups to meet consumer demand for healthier and more authentic flavors. The clean-label movement is particularly strong in North America and Europe, where regulatory frameworks and consumer awareness have accelerated product innovation.

Sugar-Free and Functional Syrups Emerging as High-Growth Categories

The increasing prevalence of obesity and diabetes, combined with rising health awareness, has encouraged consumers to shift toward reduced-sugar and sugar-free syrup products. Manufacturers are introducing strawberry syrups sweetened with stevia, monk fruit, and other natural alternatives while maintaining taste profiles comparable to traditional products. Functional formulations enriched with vitamins, antioxidants, and immunity-support ingredients are also emerging. These innovations are creating premium pricing opportunities and enabling manufacturers to target health-conscious consumers across retail and foodservice channels.

Strawberry Syrups Market Drivers

Expansion of Specialty Coffee and Beverage Culture

The rapid growth of cafés, juice bars, and specialty beverage chains has significantly increased the use of flavored syrups globally. Strawberry syrup remains one of the most versatile and widely accepted fruit flavors used in milkshakes, smoothies, flavored milk, iced beverages, and cocktails. The proliferation of premium beverage outlets in Asia-Pacific and the Middle East is generating substantial incremental demand for fruit-based syrups.

Growing Demand for Premium Bakery and Dessert Products

Consumer preferences are increasingly shifting toward premium desserts, artisanal bakery products, and indulgent frozen treats. Strawberry syrup serves as a key ingredient in cake toppings, pastry fillings, ice cream, yogurt, and confectionery products. The expansion of the global bakery and confectionery industry is therefore creating sustained demand for strawberry syrup formulations.

Increasing Preference for Fruit-Based Flavor Ingredients

Consumers increasingly perceive fruit-derived ingredients as healthier alternatives to artificial flavorings. Strawberry syrup manufacturers are capitalizing on this trend by introducing products with higher fruit content and natural ingredient claims. The demand for fruit-flavored dairy products and beverages is also supporting long-term market expansion.

Strawberry Syrups Market Restraints

Volatility in Raw Material Prices

The market remains vulnerable to fluctuations in the prices of strawberries, fruit concentrates, and sugar. Adverse weather conditions, supply-chain disruptions, and agricultural uncertainties can significantly impact manufacturing costs and profit margins. Price volatility often forces manufacturers to increase retail prices, potentially affecting demand.

Regulatory Pressure on Sugar Consumption

Governments worldwide are implementing sugar taxes and stricter nutritional labeling requirements to combat obesity and related health conditions. These regulations may reduce consumption of conventional high-sugar strawberry syrups and require manufacturers to invest heavily in reformulation and product innovation.

Strawberry Syrups Industry Key Opportunities

Expansion of Premium and Organic Product Portfolios

Organic and premium strawberry syrups represent one of the most attractive opportunities in the market. Consumer willingness to pay higher prices for natural, sustainably sourced, and artisanal products is increasing globally. Manufacturers that invest in organic certifications, premium packaging, and real fruit formulations are expected to achieve higher margins and improved brand differentiation. Premiumization trends are particularly pronounced in North America, Western Europe, and developed Asia-Pacific markets.

Growth of Foodservice and Café Chains in Emerging Markets

The rapid expansion of specialty coffee shops, bubble tea chains, dessert cafés, and quick-service restaurants in India, Southeast Asia, and the Middle East presents substantial opportunities for syrup manufacturers. These businesses rely heavily on flavored syrups to create differentiated beverage offerings. Establishing local manufacturing capabilities and strategic partnerships with foodservice operators can help suppliers capture significant market share in high-growth economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1070.00 Million |

| Market Size in 2026 | USD 1142.76 Million |

| Market Size in 2031 | USD 1587.86 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The conventional strawberry syrup segment accounted for nearly 47% of global market revenues in 2025 and continues to maintain its leading position owing to its cost-effectiveness, longer shelf life, and extensive application across industrial food processing, foodservice, and household consumption. The segment's growth is primarily driven by increasing demand from beverage manufacturers, bakery producers, and quick-service restaurant chains that require economical flavoring ingredients for large-scale production. Conventional syrups also benefit from widespread retail availability and strong consumer familiarity, particularly in emerging economies where price sensitivity remains high.Organic strawberry syrups represent one of the fastest-growing product categories, supported by the global clean-label movement and increasing awareness regarding ingredient transparency and sustainable food production. Growing demand for certified organic products, particularly in North America and Europe, continues to encourage manufacturers to expand their organic product portfolios. Similarly, sugar-free and reduced-sugar strawberry syrups are gaining substantial traction due to rising health consciousness, increasing diabetes prevalence, and consumer preference for low-calorie food and beverage alternatives.Functional strawberry syrups enriched with vitamins, minerals, probiotics, and immunity-support ingredients are emerging as an attractive niche category. The increasing convergence of indulgence and wellness trends is encouraging manufacturers to develop value-added products that deliver both flavor and nutritional benefits. These products are particularly gaining acceptance in developed markets where consumers increasingly seek functional ingredients in everyday food and beverage products.

Application Insights

Beverage preparation remains the largest application segment, accounting for approximately 34% of global strawberry syrup demand in 2025. The segment's leadership is primarily driven by the rapid expansion of specialty cafés, coffee chains, bubble tea outlets, and premium beverage establishments worldwide. Strawberry syrup is extensively utilized in milkshakes, smoothies, flavored coffees, mocktails, cocktails, sparkling beverages, and frozen drinks because of its ability to provide consistent flavor, color, and sweetness. Rising consumer preference for customized and visually appealing beverages continues to accelerate demand across both commercial and household applications.Bakery and confectionery applications constitute another significant segment, supported by growing consumption of premium cakes, pastries, doughnuts, fillings, and dessert toppings. The increasing popularity of indulgent desserts and seasonal flavored bakery products has encouraged manufacturers to incorporate fruit-based syrups into product formulations. In addition, strawberry syrup serves as a versatile ingredient in confectionery manufacturing due to its ability to enhance flavor profiles and improve product differentiation.The dairy application segment continues to generate substantial demand, particularly in North America and Europe, where strawberry-flavored yogurts, ice creams, frozen desserts, and flavored milk products enjoy strong consumer acceptance. Increasing demand for fruit-flavored dairy products and the expansion of premium dairy offerings are supporting market growth across this segment.Industrial food processing and household consumption are also expanding steadily. Food manufacturers increasingly utilize strawberry syrup in ready-to-eat products, sauces, and dessert preparations, while rising retail penetration, e-commerce growth, and increasing experimentation with home-based beverage and dessert preparation are driving household consumption globally.

Distribution Channel Insights

Supermarkets and hypermarkets accounted for approximately 38% of global strawberry syrup sales in 2025, making them the leading distribution channel. The segment's dominance is driven by extensive product assortments, attractive promotional strategies, strong consumer trust, and the convenience of one-stop grocery shopping. Large retail chains also provide manufacturers with significant visibility and shelf presence, enabling both established and emerging brands to reach broader consumer bases.Online retail channels are expected to witness the fastest growth during the forecast period, supported by increasing internet penetration, expanding e-commerce infrastructure, and changing purchasing behaviors. Consumers are increasingly using digital platforms to access premium, organic, imported, and specialty strawberry syrup products that may not be readily available through traditional retail channels. Subscription models, direct-to-consumer platforms, and rapid delivery services are further strengthening online sales growth.Foodservice distributors continue to play a critical role in market development by supplying cafés, restaurants, hotels, bakeries, and beverage chains. The expansion of organized foodservice establishments and specialty beverage outlets globally has significantly increased procurement volumes through distribution networks. Direct-to-business channels are also gaining momentum as manufacturers increasingly establish long-term supply agreements with industrial food processors, quick-service restaurants, and beverage companies to ensure stable demand and supply chain efficiency.

End-Use Industry Insights

The food and beverage manufacturing industry represented approximately 42% of global strawberry syrup consumption in 2025 and remains the largest end-use segment. The segment's dominance is primarily driven by the widespread incorporation of strawberry syrup in dairy products, bakery items, confectionery products, ready-to-drink beverages, and dessert preparations. Growing demand for flavored food products and continuous product innovation within the processed food industry continue to support substantial consumption of strawberry syrup across manufacturing applications.The HoReCa sector is emerging as the fastest-growing end-use segment, benefiting from the rapid expansion of cafés, restaurants, premium dessert outlets, and specialty beverage chains worldwide. Increasing consumer spending on out-of-home dining experiences and rising demand for customized beverages and desserts have significantly increased syrup utilization across foodservice establishments.Institutional catering and household consumption are also witnessing steady growth, particularly in emerging economies where rising disposable incomes, changing lifestyles, and increasing urbanization are encouraging greater consumption of value-added food products. The growing popularity of home baking, café-style beverages, and dessert preparation further supports demand from household consumers.

Packaging Insights

PET bottles accounted for approximately 43% of total market revenues in 2025 and continue to dominate the global strawberry syrups market. The segment's leadership is driven by the cost efficiency, lightweight nature, durability, and ease of transportation offered by PET packaging. Manufacturers also prefer PET bottles because they support large-scale production, minimize logistics costs, and provide convenient dispensing solutions for both retail and foodservice consumers.Glass bottles remain highly preferred in premium, artisanal, and organic product categories due to their superior shelf appeal, premium appearance, and strong consumer perception regarding product quality and ingredient preservation. Premium brands increasingly utilize glass packaging to enhance product positioning and appeal to health-conscious and environmentally aware consumers.Foodservice bulk containers continue to witness stable demand from cafés, restaurants, hotels, and industrial food processors that require larger packaging formats to support high-volume consumption. Flexible pouches and sachets are also gaining popularity, particularly in developing economies, due to their affordability, lower packaging costs, ease of storage, and suitability for smaller serving sizes and price-sensitive consumer segments.

Explore more data points, trends and opportunities Download Free Sample Report

Strawberry Syrups Market Segmentations

By Product Formulation

- Conventional Strawberry Syrup

- Premium Strawberry Syrup

- Concentrated Strawberry Syrup

- Ready-to-Use (RTU) Strawberry Syrup

- Sugar-Free/Reduced-Sugar Strawberry Syrup

- Functional/Fortified Strawberry Syrup

- Organic Strawberry Syrup

By Ingredient Profile

- Natural Strawberry Syrup

- Artificially Flavored Strawberry Syrup

- Clean-Label Strawberry Syrup

By Sweetener Type

- Sucrose-Based Syrup

- High-Fructose Corn Syrup (HFCS)-Based Syrup

- Stevia-Sweetened Syrup

- Monk Fruit Sweetened Syrup

- Mixed Sweetener Formulations

By Packaging Type

- Glass Bottles

- PET Bottles

- Squeezable Plastic Bottles

- Pouches and Sachets

- Foodservice Bulk Containers

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Food Stores

- Foodservice Distributors

- Online Retail and E-commerce

- Direct-to-Business (B2B) Sales

Regional Insights

North America

North America accounted for approximately 31% of the global strawberry syrups market in 2025, making it the largest regional market. The United States contributes nearly 24% of global demand owing to its mature foodservice industry, extensive café culture, and high consumption of flavored beverages and desserts. Canada also represents a significant market, driven by increasing demand for premium and organic syrups. Consumer preference for natural ingredients and innovative beverage formulations continues to support market expansion across the region.Regional growth is further supported by the strong presence of multinational food and beverage manufacturers, increasing consumption of specialty coffees and ready-to-drink beverages, rising demand for clean-label and low-sugar products, and continued expansion of premium café chains and quick-service restaurants. The region's advanced retail infrastructure and high consumer spending on premium food products further contribute to sustained market growth.

Europe

Europe represented approximately 28% of global revenues in 2025. Germany, the United Kingdom, France, and Italy are among the largest consumers of strawberry syrups in the region. Demand is increasingly shifting toward natural and organic formulations due to stringent food regulations and growing consumer awareness regarding health and sustainability. The region also benefits from strong bakery and confectionery industries, which extensively utilize fruit-based flavor ingredients.Market growth in Europe is driven by increasing demand for clean-label and naturally flavored products, expanding premium dessert and artisanal bakery segments, rising consumption of specialty beverages, and growing preference for sustainably sourced ingredients. Continuous product innovation and increasing adoption of organic food products across Western European countries are expected to further strengthen regional demand.

Asia-Pacific

Asia-Pacific accounted for approximately 27% of global demand and is projected to be the fastest-growing regional market, with a CAGR exceeding 8.5% through 2031. China, India, Japan, South Korea, and Indonesia are major markets. India is expected to record the highest growth rate globally, supported by rapid urbanization, increasing café penetration, and expanding processed food industries. Rising disposable incomes and changing dietary preferences continue to drive demand for flavored beverages and premium dessert products across the region.The region's growth is additionally supported by a rapidly expanding middle-class population, increasing westernization of food consumption patterns, strong growth in foodservice and quick-service restaurant chains, rising penetration of modern retail and e-commerce platforms, and increasing investment in processed food manufacturing. The growing popularity of bubble tea, specialty beverages, and premium café experiences is also creating significant demand opportunities for strawberry syrup manufacturers across Asia-Pacific.

Latin America

Latin America is gradually emerging as an important market for strawberry syrups, led by Brazil and Mexico. The growth of quick-service restaurants, increasing consumption of dairy desserts, and rising urbanization are supporting regional demand. Premium and fruit-based products are also gaining traction among middle-income consumers in major metropolitan areas.Additional growth drivers include expanding organized retail networks, increasing demand for flavored beverages among younger consumers, rising disposable incomes, and growing investment in the region's food processing industry. The increasing popularity of café culture and dessert-based foodservice concepts is expected to create further opportunities for market expansion over the forecast period.

Middle East & Africa

The Middle East and Africa market is witnessing steady growth, supported by expanding foodservice sectors and rising demand for premium beverages and desserts. The UAE and Saudi Arabia represent the largest markets in the Middle East due to strong café culture and high per capita spending on premium food products. South Africa remains the largest consumer in Sub-Saharan Africa, supported by the development of modern retail infrastructure and growing processed food industries.Regional growth is further driven by increasing tourism activity, rising investments in hospitality and foodservice infrastructure, expanding international café and restaurant chains, growing urbanization, and increasing consumer preference for premium and flavored beverage experiences. The gradual modernization of retail channels and increasing availability of imported and premium food products are also contributing to market development across the region.

Key Players in the Strawberry Syrups Market

- Monin

- Torani

- The Hershey Company

- DaVinci Gourmet

- Tate & Lyle

- Sensient Technologies

- Sicoly

- R. Torre & Company

- Concord Foods

- Kerry Group

- 1883 Maison Routin

- SIS Natural

- Giffard

- Fabbri 1905

- Kraft Heinz