Strawberry Preparations Market Size

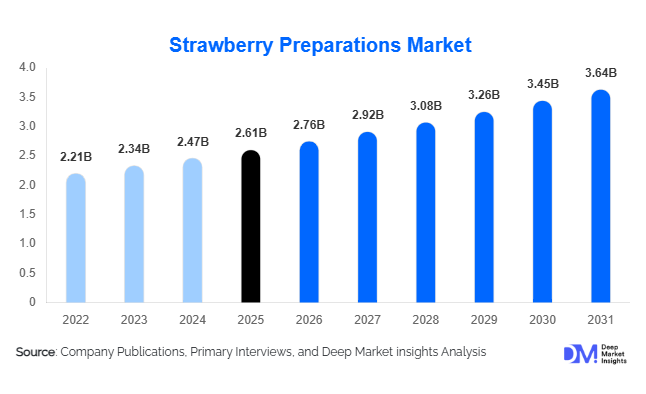

According to Deep Market Insights, the global strawberry preparations market size was valued at USD 2.61 billion in 2025 and is projected to grow from USD 2.76 billion in 2026 to reach USD 3.64 billion by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The strawberry preparations market growth is primarily driven by rising consumption of fruit-based dairy products, increasing demand for clean-label ingredients, expansion of premium bakery and confectionery applications, and growing utilization of fruit preparations in plant-based food formulations. Strawberry remains one of the most widely accepted fruit flavors globally, making it a preferred ingredient across yogurt, desserts, bakery fillings, beverages, and frozen food products.

Key Market Insights

- Dairy applications account for the largest share of global demand, representing nearly 35% of total strawberry preparation consumption due to extensive use in yogurt, dairy desserts, and flavored milk products.

- Europe dominates the global strawberry preparations market, supported by strong dairy manufacturing, premium bakery consumption, and established fruit processing infrastructure.

- Asia-Pacific is the fastest-growing regional market, driven by rapid expansion of food processing industries in China, India, Indonesia, and Southeast Asia.

- Reduced-sugar and clean-label formulations are gaining significant traction, encouraging manufacturers to invest in innovative sweetening technologies and natural ingredient systems.

- Industrial B2B sales remain the primary distribution channel, accounting for more than 70% of total market revenues through long-term supply agreements with food manufacturers.

- Plant-based dairy alternatives are creating new opportunities, as producers increasingly utilize strawberry preparations to improve flavor, texture, and consumer acceptance.

Strawberry Preparations Market Latest Trends

Clean-Label and Natural Fruit Ingredient Adoption Accelerating

Food manufacturers worldwide are increasingly replacing artificial flavors, synthetic colors, and chemical additives with fruit-derived ingredients. Strawberry preparations provide natural flavor, color, texture, and nutritional appeal while supporting clean-label product positioning. Consumers are showing greater preference for products containing recognizable ingredients, leading manufacturers to launch formulations featuring high-fruit-content strawberry preparations. This trend is particularly evident across yogurt, premium desserts, fruit snacks, and bakery products. Ingredient suppliers are responding by developing minimally processed fruit systems, transparent sourcing programs, and formulations that preserve fruit authenticity while meeting industrial shelf-life requirements.

Growth of Reduced-Sugar and Functional Formulations

Health-conscious consumers are increasingly seeking products with lower sugar content without compromising taste. Strawberry preparation manufacturers are investing in technologies that reduce sugar while maintaining texture stability, fruit integrity, and sensory performance. Formulations utilizing natural sweeteners, fruit concentrates, and fiber enrichment are becoming more common. Functional food manufacturers are also incorporating strawberry preparations into protein-rich snacks, meal replacements, fortified dairy products, and wellness-oriented food applications. This trend is expected to significantly influence product innovation over the coming decade as regulatory scrutiny around sugar consumption continues to intensify globally.

Strawberry Preparations Market Drivers

Strong Growth in Global Dairy Consumption

Dairy remains the largest end-use sector for strawberry preparations, with yogurt, drinking yogurt, dairy desserts, and cultured products accounting for a substantial share of demand. Strawberry continues to be the most popular fruit flavor used in yogurt formulations globally due to broad consumer acceptance across all age groups. Expansion of premium dairy products, functional yogurts, probiotic beverages, and high-protein dairy snacks continues to create substantial opportunities for strawberry preparation suppliers. Rapid dairy sector growth in Asia-Pacific is further strengthening long-term market prospects.

Expansion of Premium Bakery and Dessert Categories

Consumers are increasingly willing to spend on premium bakery products, pastries, cakes, donuts, cheesecakes, and desserts featuring fruit-based fillings and toppings. Strawberry fillings and fruit preparations are extensively utilized in these applications due to their flavor versatility and premium appeal. Product innovation in artisanal bakery segments, café chains, and foodservice channels is contributing to sustained demand growth. The increasing popularity of indulgent desserts and premium confectionery products further supports market expansion.

Growing Demand for Plant-Based and Alternative Foods

The rapid growth of plant-based dairy alternatives is creating a significant new demand channel for strawberry preparations. Oat-based yogurts, almond-based desserts, coconut-based dairy alternatives, and plant-derived beverages increasingly rely on fruit preparations to enhance taste and improve consumer acceptance. Strawberry remains one of the most preferred flavors within plant-based product launches, enabling ingredient manufacturers to diversify beyond traditional dairy applications.

Strawberry Preparations Market Restraints

Volatility in Strawberry Raw Material Prices

Strawberry cultivation is highly susceptible to climate fluctuations, labor shortages, disease outbreaks, and changing agricultural conditions. Weather-related disruptions can significantly impact fruit availability and processing costs. These fluctuations create challenges for manufacturers operating under long-term contracts, particularly when raw material costs rise sharply. Price instability can compress margins and complicate procurement planning throughout the value chain.

Perishability and Supply Chain Complexities

Strawberries are among the most perishable fruits used in food processing. Maintaining quality during harvesting, transportation, storage, freezing, and processing requires sophisticated cold-chain infrastructure and rigorous quality control measures. In emerging economies, inadequate logistics infrastructure and fragmented agricultural supply chains can increase wastage and operational costs. These challenges remain a key restraint for market participants seeking expansion in developing regions.

Strawberry Preparations Industry Key Opportunities

Expansion of Plant-Based Dairy and Alternative Foods

The global plant-based food industry is expanding rapidly, creating significant opportunities for strawberry preparation manufacturers. Plant-based yogurt, dairy-free desserts, and alternative beverages increasingly utilize fruit preparations to improve taste, texture, and visual appeal. Suppliers that develop customized formulations for vegan and dairy-free applications can secure long-term growth opportunities as consumer adoption of alternative proteins accelerates globally.

Premium Reduced-Sugar Product Innovation

Consumers are actively seeking healthier food options without sacrificing flavor quality. Reduced-sugar and no-added-sugar strawberry preparations represent a high-margin growth opportunity for manufacturers. Advances in natural sweetening technologies, fruit concentration methods, and formulation science are enabling suppliers to develop premium offerings that meet evolving regulatory requirements and consumer preferences. Premium health-focused products are expected to generate above-average profitability throughout the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.61 Billion |

| Market Size in 2026 | USD 2.76 Billion |

| Market Size in 2031 | USD 3.64 Billion |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The strawberry preparations market is segmented into dairy fruit preparations, strawberry fillings, jams and preserves, purees and concentrates, and freeze-dried or powdered strawberry preparations. Dairy fruit preparations remain the largest product segment, accounting for approximately 32% of global market revenue. The segment’s leadership is primarily driven by the expanding global yogurt industry, increasing consumption of flavored dairy products, and growing demand for fruit-inclusive functional dairy offerings. Manufacturers continue to incorporate strawberry preparations into yogurt, drinking yogurt, cultured dairy products, dairy desserts, and protein-enriched dairy snacks due to their ability to enhance flavor, texture, visual appeal, and nutritional positioning. The continued expansion of probiotic and premium dairy categories further strengthens demand for customized strawberry preparations.Strawberry jams and preserves maintain a significant market presence across both retail and foodservice channels. Strong household consumption, widespread use as breakfast spreads, and growing demand for premium fruit-based condiments support sustained demand, particularly across Europe and North America where fruit preserves remain deeply embedded within consumer food habits.Purees and concentrates represent an increasingly important category due to their broad functionality within industrial food and beverage manufacturing. These ingredients are widely utilized in smoothies, fruit beverages, flavored waters, dairy drinks, frozen desserts, confectionery products, and food processing applications. Growing demand for natural fruit ingredients and clean-label formulations is accelerating adoption among beverage and food manufacturers seeking authentic fruit profiles.Freeze-dried and powdered strawberry preparations are emerging as one of the fastest-growing product categories. Growth is being driven by increasing demand for shelf-stable fruit ingredients, functional foods, sports nutrition products, nutritional supplements, meal replacement products, and convenience formulations. Their extended shelf life, ease of transportation, concentrated nutritional profile, and suitability for health-oriented product development continue to create new opportunities across global food and nutraceutical industries.

Nature Insights

Based on nature, the market is categorized into conventional and organic strawberry preparations. Conventional strawberry preparations dominate the global market, accounting for approximately 84% of total revenue. The segment’s leadership is primarily attributed to its cost competitiveness, widespread availability of raw materials, established agricultural supply chains, and greater production scalability for large-volume industrial applications. Food manufacturers across dairy, bakery, confectionery, and beverage sectors continue to favor conventional preparations due to their ability to ensure consistent quality, supply reliability, and operational efficiency while maintaining competitive product pricing.Organic strawberry preparations represent a comparatively smaller but rapidly expanding segment. Growth is being driven by rising consumer awareness regarding food safety, sustainability, environmental responsibility, and clean-label consumption. Increasing preference for minimally processed and naturally sourced ingredients is encouraging food manufacturers to expand organic product portfolios. Premium dairy brands, organic bakery manufacturers, and health-focused food companies are increasingly incorporating certified organic strawberry preparations to strengthen product differentiation and enhance brand value.The ongoing expansion of organic food retail networks, stricter transparency requirements across food labeling, and rising consumer willingness to pay premium prices for organic products are expected to support long-term growth within the segment. As sustainability initiatives continue to gain importance throughout the food value chain, demand for organic fruit preparations is anticipated to strengthen across both developed and emerging markets.

Sugar Profile Insights

The market is segmented into regular sugar, reduced-sugar, and no-added-sugar strawberry preparations. Regular sugar formulations remain the dominant category, representing nearly 69% of global demand. The segment’s leading position is driven by superior preservation performance, formulation stability, enhanced texture characteristics, cost efficiency, and broad compatibility across dairy, bakery, confectionery, and foodservice applications. Manufacturers continue to prefer traditional sugar formulations for large-scale production due to their proven ability to maintain product quality, shelf life, and consumer acceptance.Reduced-sugar strawberry preparations are experiencing steady growth as food manufacturers respond to increasing consumer awareness regarding sugar intake and the growing prevalence of obesity, diabetes, and lifestyle-related health conditions. Regulatory initiatives aimed at reducing sugar consumption across multiple regions are also encouraging product reformulation efforts. As a result, reduced-sugar offerings are becoming increasingly common within dairy products, fruit spreads, beverages, and snack applications.No-added-sugar formulations represent a rapidly developing niche segment supported by demand for healthier food choices and specialized nutrition products. These preparations are increasingly incorporated into diabetic-friendly foods, wellness-oriented products, functional nutrition applications, and premium health-focused product lines. To meet evolving consumer expectations, manufacturers continue investing in advanced sweetening technologies and formulation innovations that enable sugar reduction while preserving fruit flavor, texture, visual appeal, and shelf stability.

Distribution Channel Insights

Based on distribution channel, the market is divided into business-to-business (B2B) industrial sales, foodservice and HoReCa, and retail sales. Business-to-business industrial sales account for approximately 71% of global market revenue, making it the largest distribution channel. The segment’s dominance is driven by the extensive use of strawberry preparations as ingredients within large-scale food manufacturing operations. Dairy processors, bakery manufacturers, dessert producers, beverage companies, confectionery manufacturers, and functional food producers typically procure customized fruit preparations through long-term contractual agreements to ensure supply consistency, product standardization, and operational efficiency.The foodservice and HoReCa segment continues to gain momentum as restaurants, cafés, bakeries, quick-service outlets, and dessert chains increasingly utilize premium fruit ingredients to enhance menu offerings. Rising consumer spending on out-of-home dining experiences, premium desserts, specialty beverages, and artisanal bakery products is contributing to growing demand for customized strawberry preparations within commercial foodservice operations.Retail sales represent a smaller but steadily expanding channel supported by increasing consumer demand for premium jams, preserves, fruit toppings, spreads, dessert ingredients, and home-baking solutions. The continued growth of organized retail, specialty food stores, and e-commerce distribution channels is further improving product accessibility and supporting market penetration among household consumers.

End-Use Industry Insights

The dairy industry remains the largest end-use segment, accounting for approximately 35% of global market demand. The segment’s leadership is primarily driven by strong global consumption of yogurt, flavored milk products, cultured dairy beverages, dairy desserts, and protein-enriched dairy snacks. Strawberry remains one of the most preferred fruit flavors within dairy applications due to its broad consumer acceptance, attractive sensory profile, and compatibility with a wide range of dairy formulations. Continued innovation within probiotic, high-protein, and functional dairy categories is expected to sustain segment growth.Bakery and confectionery applications represent one of the fastest-growing end-use sectors. Increasing demand for premium pastries, fruit-filled cakes, donuts, croissants, muffins, confectionery products, and indulgent desserts continues to support rising consumption of strawberry fillings, inclusions, and fruit preparations. Product innovation and premiumization trends across bakery categories are further strengthening demand globally.Nutraceutical and functional food applications are emerging as an important growth area within the market. Strawberry preparations are increasingly utilized in protein snacks, meal replacement products, nutritional supplements, sports nutrition formulations, and wellness-focused foods. Rising consumer interest in health, immunity, nutrition, and convenient functional food solutions is expected to generate significant long-term growth opportunities within this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Strawberry Preparations Market Segmentations

By Product Type

- Strawberry Fruit Preparations for Dairy Applications

- Strawberry Fillings

- Strawberry Jam & Preserves

- Strawberry Purees

- Strawberry Toppings & Sauces

- Strawberry Syrups & Concentrates

- Freeze-Dried & Powdered Strawberry Preparations

By Nature

- Conventional

- Organic

By Sugar Profile

- Regular Sugar Formulations

- Reduced Sugar Formulations

- No Added Sugar Formulations

By Form

- Liquid

- Semi-Solid

- Frozen

- Powder

By Distribution Channel

- Business-to-Business (Industrial Sales)

- Foodservice & HoReCa

- Retail

Regional Insights

North America

North America accounts for approximately 26% of the global strawberry preparations market, led primarily by the United States, followed by Canada. The region benefits from a highly developed food processing industry, strong yogurt consumption, extensive bakery manufacturing capabilities, and widespread adoption of fruit-based ingredients across packaged food applications. Growing demand for clean-label products, premium dairy offerings, functional foods, and reduced-sugar formulations continues to support market expansion.Key regional growth drivers include increasing consumption of Greek yogurt and high-protein dairy products, rising demand for premium bakery and dessert products, growing consumer preference for natural fruit ingredients over artificial flavors, expanding functional beverage markets, and continued product innovation by major food manufacturers. The strong presence of advanced food processing infrastructure and established retail distribution networks further supports sustained demand for customized strawberry preparations throughout the region.

Europe

Europe remains the largest regional market, accounting for approximately 38% of global demand. Germany, France, the United Kingdom, Italy, Spain, Poland, and the Netherlands represent the primary consuming countries, with Germany alone contributing nearly 10% of global demand due to its highly developed dairy and bakery industries. The region benefits from mature food manufacturing sectors, established consumer preference for fruit-based products, and a well-developed fruit processing ecosystem.Regional growth is being driven by strong demand for fruit-based yogurt and dairy desserts, increasing consumption of premium bakery and confectionery products, rising adoption of organic and clean-label food ingredients, growing demand for reduced-sugar formulations, and continuous product innovation across premium food categories. In addition, Europe's well-established strawberry cultivation and processing infrastructure enhances supply chain efficiency, raw material availability, and production consistency, supporting long-term market growth.

Asia-Pacific

Asia-Pacific accounts for nearly 24% of global market demand and represents the fastest-growing regional market, with forecast growth exceeding 7% annually. China, India, Japan, South Korea, Indonesia, and Thailand are the principal growth engines. Rapid urbanization, expanding middle-class populations, rising disposable incomes, and changing dietary preferences are transforming food consumption patterns throughout the region.Major growth drivers include accelerating dairy consumption, rapid expansion of organized food processing industries, increasing penetration of Western-style bakery and confectionery products, rising demand for convenience foods, growing investments in beverage manufacturing, and expanding modern retail infrastructure. China continues to emerge as a major consumer of fruit preparations due to large-scale food manufacturing expansion, while India is witnessing strong growth supported by investments in dairy processing, cold-chain infrastructure, and organized packaged food production. Increasing health awareness and demand for premium food products are further supporting regional market expansion.

Latin America

Latin America represents approximately 7% of global market demand, with Brazil and Mexico serving as the largest markets. The region is experiencing gradual modernization of its food manufacturing sector, accompanied by increasing demand for processed foods and value-added fruit ingredients. Strawberry preparations are increasingly being incorporated into dairy products, bakery goods, beverages, and dessert applications across the region.Key growth drivers include rising urbanization, growing disposable incomes, increasing consumption of packaged and convenience foods, expansion of organized retail channels, modernization of bakery and dairy manufacturing facilities, and growing consumer demand for premium and fruit-based food products. The continued development of foodservice industries and improvements in regional food processing capabilities are expected to create additional growth opportunities for strawberry preparation suppliers over the forecast period.

Middle East & Africa

The Middle East & Africa accounts for approximately 5% of global market demand, with Saudi Arabia, the United Arab Emirates, South Africa, and Egypt representing the leading markets. Demand is being supported by rising consumption of premium dairy products, bakery items, desserts, and imported food products across both retail and foodservice channels.Regional growth is driven by increasing investments in food manufacturing facilities, expansion of modern retail and supermarket networks, growing tourism and hospitality sectors, rising demand for premium packaged foods, increasing adoption of Western-style bakery and dessert products, and ongoing diversification of food industries across Gulf Cooperation Council countries. South Africa continues to lead Sub-Saharan Africa due to its relatively advanced food processing infrastructure, while Gulf countries are benefiting from strong investments in food security initiatives, value-added food production, and premium food consumption trends.

Key Players in the Strawberry Preparations Market

- AGRANA Beteiligungs AG

- Frulact

- Zentis GmbH

- Hero Group

- Zuegg Group

- SVZ International

- Puratos Group

- Tree Top Inc.

- Döhler Group

- Valio Food Solutions

- Fourayes

- Andros Group

- Fresh Food Industries

- Darbo AG

- Ingredion Incorporated