Soybean Paste Market Size

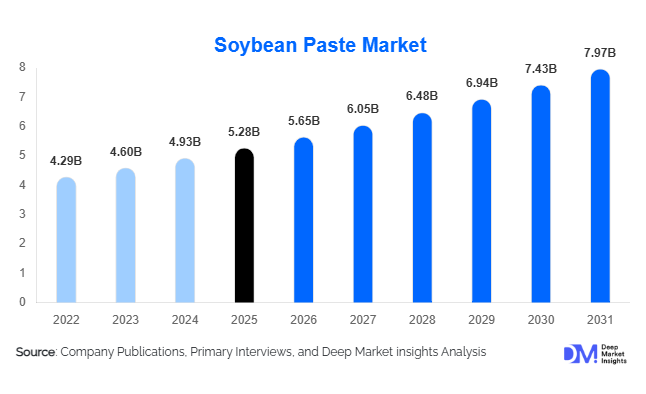

According to Deep Market Insights, the global soybean paste market size was valued at USD 5.28 billion in 2025 and is projected to grow from USD 5.65 billion in 2026 to reach USD 7.97 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The soybean paste market growth is primarily driven by rising global consumption of fermented foods, increasing demand for plant-based and clean-label ingredients, and the growing popularity of Asian cuisine across North America and Europe. Soybean paste products, including miso, doenjang, and Chinese fermented bean pastes, are increasingly being incorporated into processed foods, ready-to-eat meals, sauces, and plant-based meat applications. Growing consumer awareness regarding gut health and the functional benefits of fermented foods is further supporting market expansion.

Key Market Insights

- Fermented and functional foods are becoming mainstream globally, significantly increasing demand for soybean paste as a natural source of probiotics and bioactive compounds.

- Asia-Pacific dominates the global soybean paste market, accounting for nearly 64% of global revenues due to high consumption in China, Japan, and South Korea.

- North America and Europe are emerging as high-growth regions, supported by the expansion of Asian cuisine and increasing plant-based food consumption.

- Organic and low-sodium soybean paste products are witnessing robust demand, driven by health-conscious consumers seeking clean-label alternatives.

- The food processing industry is becoming a major demand generator, with soybean paste increasingly used in sauces, seasonings, ready meals, and meat substitutes.

- E-commerce channels are rapidly transforming product distribution, enabling premium and artisanal soybean paste brands to reach international consumers.

Soybean Paste Market Latest Trends

Premium and Organic Soybean Paste Gaining Popularity

Consumer demand for natural, organic, and minimally processed foods is reshaping the soybean paste industry. Premium soybean paste products made using traditional fermentation techniques and non-GMO soybeans are experiencing strong growth, particularly in North America and Europe. Manufacturers are increasingly launching organic and artisanal product lines that command premium pricing and cater to health-conscious consumers. The trend is also encouraging investment in sustainable soybean sourcing and environmentally friendly packaging solutions. Premium soybean paste products are increasingly being marketed based on their probiotic content, fermentation duration, and nutritional benefits, further supporting category premiumization.

Integration of Soybean Paste into Plant-Based Foods

The rapid expansion of the plant-based food industry is creating new applications for soybean paste. Food manufacturers are increasingly utilizing soybean paste as a natural umami enhancer and fermentation-derived flavor ingredient in meat alternatives, vegan sauces, and ready meals. The ingredient's ability to deliver depth of flavor without artificial additives has positioned it as an attractive solution for clean-label product formulations. The trend is expected to accelerate as plant-based food manufacturers continue seeking authentic, naturally fermented ingredients that improve taste profiles and nutritional value.

Soybean Paste Market Drivers

Growing Demand for Fermented Functional Foods

Consumers worldwide are increasingly associating fermented foods with digestive health, immunity enhancement, and overall wellness. Soybean paste contains bioactive compounds, amino acids, and beneficial microorganisms that align with the growing functional food movement. The increasing prevalence of lifestyle-related health concerns and consumer preference for preventive nutrition continue to support demand for fermented soybean products.

Global Expansion of Asian Cuisine

The international popularity of Korean, Japanese, and Chinese cuisine has significantly increased consumption of soybean paste products. The rapid expansion of Asian restaurant chains, food delivery services, and international food retailing has introduced soybean paste to new consumer groups. Cultural influences from social media, streaming platforms, and food tourism are also contributing to the globalization of traditional Asian condiments.

Increasing Demand for Natural Flavor Enhancers

Food manufacturers are increasingly replacing synthetic flavoring ingredients with naturally fermented alternatives. Soybean paste's rich umami profile enables food processors to improve product flavor while maintaining clean-label positioning. The ingredient is finding growing applications in soups, sauces, seasonings, and plant-based products, supporting long-term market growth.

Soybean Paste Market Restraints

Volatility in Soybean Prices

Raw material costs remain one of the major challenges facing soybean paste manufacturers. Global soybean prices are influenced by weather conditions, trade policies, and supply chain disruptions, creating uncertainty in production costs and profit margins. Smaller producers often face difficulties in absorbing these cost fluctuations, leading to pricing pressures throughout the value chain.

Health Concerns Regarding Sodium Content

Traditional soybean paste products generally contain high sodium levels, creating concerns among health-conscious consumers and regulatory authorities. Increasing demand for low-sodium diets is compelling manufacturers to invest in product reformulation and sodium-reduction technologies. Balancing flavor retention with sodium reduction remains a significant technical challenge for producers.

Soybean Paste Industry Key Opportunities

Expansion in Functional Nutrition and Gut Health Products

The growing global market for digestive health and functional nutrition products presents substantial opportunities for soybean paste manufacturers. The ingredient's fermentation-derived probiotics and bioactive compounds make it suitable for positioning as a functional food ingredient. Manufacturers can capitalize on this trend by introducing fortified and low-sodium formulations targeting health-conscious consumers and premium retail channels.

Growing Demand from Plant-Based Food Manufacturers

The global plant-based food industry is expanding rapidly and increasingly requires natural ingredients that improve flavor and nutritional profiles. Soybean paste is becoming an important ingredient in plant-based meat alternatives, vegan ready meals, and meat-free sauces. Strategic partnerships between soybean paste manufacturers and plant-based food producers are expected to generate significant revenue opportunities over the forecast period.

International Expansion of Asian Cuisine

Asian cuisine continues to gain popularity across North America, Europe, and Latin America. Governments in Japan and South Korea are actively promoting traditional food products through export development initiatives and culinary diplomacy programs. This increasing international exposure is creating significant export opportunities for soybean paste manufacturers, particularly premium and artisanal producers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.28 Billion |

| Market Size in 2026 | USD 5.65 Billion |

| Market Size in 2031 | USD 7.97 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Miso paste remains the dominant product segment in the global soybean paste market, accounting for approximately 31% of total market share in 2025. Its leadership is primarily driven by its deep integration into traditional Japanese cuisine, strong cultural consumption patterns, and increasing international popularity as global consumers adopt Asian flavors in everyday cooking. The expansion of Japanese restaurant chains worldwide, along with rising retail availability of authentic imported products, continues to reinforce demand across both developed and emerging markets. Growing consumer preference for fermented, umami-rich, and natural flavoring ingredients further strengthens its position as the leading product type within the category.Traditional fermented soybean pastes, including Korean doenjang and Chinese yellow bean pastes, maintain strong market relevance due to their longstanding culinary heritage and widespread household usage across Asia. These segments benefit from stable domestic demand supported by daily cooking traditions and increasing export penetration into Western markets. The rising awareness of gut health and fermentation benefits has also elevated consumer interest in these traditional variants.Organic and low-sodium soybean paste products represent the fastest-growing product categories, driven by increasing health consciousness, demand for clean-label foods, and dietary concerns related to sodium intake. Premiumization trends, especially in North America and Europe, are accelerating adoption as consumers seek high-quality, minimally processed, and functional food ingredients that align with wellness-oriented lifestyles.

Application Insights

Household consumption continues to be the largest application segment, accounting for nearly 47% of global demand. This dominance is driven by the essential role of soybean paste in everyday cooking across Asian households, particularly in Japan, Korea, and China. The increasing globalization of Asian cuisine, combined with improved retail accessibility in Western markets, is expanding household penetration beyond traditional geographies. Rising interest in home cooking, influenced by health, cost efficiency, and culinary exploration trends, further supports sustained demand growth in this segment.The food processing industry is emerging as the fastest-growing application segment, fueled by the incorporation of soybean paste into a wide range of packaged and convenience foods such as ready-to-eat meals, sauces, instant soups, frozen foods, and plant-based meat alternatives. The segment’s growth is strongly supported by the global shift toward convenience foods and the increasing demand for natural flavor enhancers in processed formulations. Manufacturers are leveraging soybean paste for its umami profile, clean-label positioning, and functional fermentation benefits, making it a key ingredient in product innovation pipelines.Foodservice applications are also expanding rapidly, driven by the global proliferation of Asian restaurants, fusion cuisine trends, and increasing consumer dining-out frequency. Institutional adoption in hotels, catering services, and quick-service restaurants is further reinforcing demand. Additionally, emerging applications in nutraceuticals and functional foods are broadening the market scope, as fermented soybean ingredients gain recognition for their potential digestive and metabolic health benefits.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel, accounting for approximately 38% of global sales. Their dominance is driven by wide product assortment, strong consumer trust, and the convenience of one-stop shopping experiences. These retail formats play a particularly important role in urban markets where consumers prefer immediate product availability and brand comparison options, further reinforcing mainstream adoption of soybean paste products.Specialty Asian grocery stores continue to hold significant importance, particularly in North America and Europe, where they serve as key access points for authentic imported products. These outlets benefit from strong diaspora demand and consumer preference for traditional and region-specific food products that are not always widely available in conventional retail channels.E-commerce is the fastest-growing distribution channel, driven by increasing digital adoption, expanding online grocery ecosystems, and growing consumer preference for convenience. Online platforms enable global access to niche, artisanal, organic, and premium soybean paste brands, significantly broadening market reach for producers. Direct-to-consumer strategies and subscription-based food delivery models are further enhancing brand engagement and customer retention, particularly among younger and urban populations.

End-User Insights

Retail consumers represent the largest end-user segment, accounting for approximately 52% of global demand. This dominance is supported by strong household usage patterns in Asia and growing adoption in Western markets due to increased exposure to Asian cuisine and health-driven dietary changes. The segment’s growth is further reinforced by rising interest in home cooking, culinary experimentation, and natural fermented food products.Food manufacturers are the fastest-growing end-user segment, driven by the increasing integration of soybean paste into processed foods, seasonings, marinades, and plant-based formulations. The demand is strongly influenced by the food industry’s shift toward natural flavor enhancers and clean-label ingredients. Innovation in plant-based protein products and ready-to-eat meals is significantly accelerating consumption within this segment.Foodservice operators, including restaurants, catering services, and institutional kitchens, are also contributing significantly to demand growth as Asian cuisine continues to gain global popularity. The expansion of international restaurant chains and fusion dining concepts is increasing the utilization of soybean paste in professional culinary applications. Institutional buyers, such as hotels, schools, and healthcare facilities, provide a stable baseline demand, particularly in developed markets where standardized meal programs incorporate ethnic and functional ingredients.

Packaging Type Insights

Plastic containers and tubs dominate the packaging segment with nearly 44% market share due to their cost-effectiveness, durability, lightweight nature, and ability to preserve product freshness over extended shelf life. Their versatility across both retail and foodservice applications makes them the most widely adopted packaging format globally.Glass jars continue to perform strongly in the premium segment, where packaging aesthetics, perceived quality, and product authenticity play a critical role in consumer purchasing decisions. These formats are particularly favored in organic and artisanal product lines, where brand positioning emphasizes traditional preparation methods and superior quality standards.Flexible pouches and single-serve packaging formats are experiencing rapid growth, driven by urbanization, on-the-go consumption trends, and increasing demand for convenience-oriented packaging solutions. These formats are especially popular among younger consumers and in modern retail environments. Bulk industrial packaging continues to expand steadily, supported by rising demand from food manufacturers and large-scale foodservice operators requiring cost-efficient and high-volume supply solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Soybean Paste Market Segmentations

By Product Type

- Traditional Fermented Soybean Paste

- Chinese Fermented Soybean Paste

- Indonesian and Southeast Asian Soybean Paste

- Instant Soybean Paste Preparations

- Organic Soybean Paste

- Low-Sodium Soybean Paste

- Premium and Artisanal Soybean Paste

By Fermentation Method

- Naturally Fermented

- Controlled Industrial Fermentation

- Enzyme-Assisted Fermentation

By Ingredient Source

- Conventional Soybean Paste

- Non-GMO Soybean Paste

- Organic Soybean Paste

By Packaging Type

- Glass Jars

- Plastic Containers and Tubs

- Flexible Pouches

- Sachets and Single-Serve Packs

- Bulk Industrial Packaging

By Application

- Household Consumption

- Foodservice Industry

- Food Processing Industry

- Nutraceutical and Functional Food Applications

Regional Insights

Asia-Pacific

Asia-Pacific remains the dominant regional market, accounting for approximately 64% of global revenues in 2025. This leadership is primarily driven by deeply rooted culinary traditions, high per-capita consumption, and strong domestic production capabilities. China, Japan, and South Korea collectively form the core demand base, supported by established fermentation cultures and daily dietary reliance on soybean paste products.Growth in the region is further reinforced by rising disposable incomes, rapid urbanization, and increasing demand for premium and organic variants. The expansion of modern retail infrastructure and the globalization of Asian cuisine are also supporting export growth and cross-border product adoption. Additionally, innovation in health-oriented fermented foods is contributing to sustained long-term market expansion.

North America

North America accounts for approximately 15% of the global market and is one of the fastest-growing regions. Growth is primarily driven by increasing consumer interest in Asian cuisine, expanding multicultural demographics, and rising awareness of fermented and functional foods. The United States leads regional demand due to strong penetration of Japanese, Korean, and pan-Asian restaurant chains, alongside increasing retail availability of authentic imported products.The region’s growth is further supported by the rapid expansion of plant-based diets and clean-label food trends, which have increased the use of soybean paste as a natural flavor enhancer in processed and home-prepared foods. Canada is also witnessing steady growth driven by urbanization, immigration-driven food diversity, and increasing health-conscious consumption patterns.

Europe

Europe represents nearly 12% of global demand, with key markets including Germany, the United Kingdom, France, and the Netherlands. Growth in the region is primarily driven by rising awareness of fermented foods, increasing vegan and vegetarian populations, and expanding interest in global culinary experiences.The proliferation of Asian restaurants and specialty food retailers has significantly improved product accessibility, while health and wellness trends are encouraging adoption of fermented and plant-based ingredients. Regulatory emphasis on clean-label and natural food products is also supporting market expansion across both retail and foodservice sectors.

Latin America

Latin America accounts for approximately 5% of global revenues and is projected to be the fastest-growing regional market, expanding at over 8% CAGR. Growth is driven by increasing exposure to international cuisines, rising urban middle-class populations, and expanding retail modernization. Countries such as Brazil, Mexico, and Argentina are witnessing growing demand for Asian condiments and plant-based food ingredients.The expansion of modern supermarkets and e-commerce platforms is improving product availability, while rising health awareness is encouraging the adoption of fermented and functional foods. Foodservice sector growth, particularly in urban centers, is also contributing to increasing consumption of soybean-based products.

Middle East & Africa

The Middle East & Africa region accounts for approximately 4% of global demand, with growth primarily driven by urbanization, tourism, and a large expatriate population familiar with Asian cuisine. Key markets such as the United Arab Emirates, Saudi Arabia, and South Africa are witnessing rising demand due to expanding international foodservice infrastructure and increasing diversification of dietary preferences.Growth is further supported by investments in premium retail formats and hospitality expansion, particularly in metropolitan areas. The increasing presence of global food brands and rising disposable incomes are also contributing to gradual but steady market penetration across the region.

Key Players in the Soybean Paste Market

- Marukome Co., Ltd.

- Kikkoman Corporation

- CJ CheilJedang Corporation

- Sempio Foods Company

- Daesang Corporation

- Mizkan Holdings Co., Ltd.

- Hikari Miso Co., Ltd.

- Yamasa Corporation

- Shinho Food Industries Co., Ltd.

- Pulmuone Corporation

- Morinaga Nutritional Foods, Inc.

- Eden Foods, Inc.

- Hain Celestial Group, Inc.

- Muso Co., Ltd.

- Yeo Hiap Seng Limited