Soyasaponin Market Size

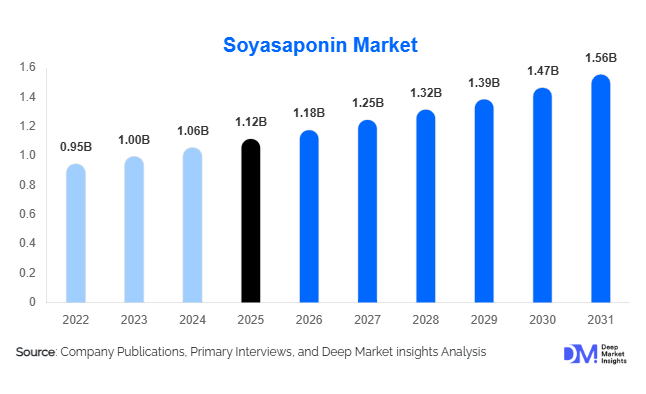

According to Deep Market Insights, the global soyasaponin market size was valued at USD 1.12 billion in 2025 and is projected to grow from USD 1.18 billion in 2026 to reach USD 1.56 billion by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The soyasaponin market growth is primarily driven by rising demand for plant-derived bioactive ingredients, increasing adoption of functional foods and dietary supplements, expanding pharmaceutical research on natural compounds, and growing utilization of soy processing by-products for value-added ingredient production. Soyasaponins have gained significant commercial importance owing to their antioxidant, anti-inflammatory, cholesterol-lowering, immune-modulating, and emulsification properties. As consumers increasingly seek natural, clean-label, and scientifically validated ingredients, manufacturers across food, nutraceutical, pharmaceutical, cosmetic, and animal nutrition industries are integrating soyasaponins into product formulations. Technological advancements in extraction and purification processes are further improving product quality and expanding the commercial viability of high-purity soyasaponin products globally.

Key Market Insights

- Nutraceutical applications account for approximately 34% of global soyasaponin demand, making dietary supplements the largest end-use segment worldwide.

- Group B soyasaponins represent nearly 38% of the market, supported by extensive scientific research and superior commercial adoption.

- North America dominates the global soyasaponin market, accounting for approximately 36% of global demand, led by the United States.

- Asia-Pacific is the fastest-growing regional market, driven by expanding nutraceutical industries in China, India, Japan, and South Korea.

- Growing utilization of soybean processing by-products is improving production economics and supporting circular economy initiatives.

- High-purity soyasaponins above 90% purity are witnessing strong demand growth, particularly in pharmaceutical and premium nutraceutical applications.

- Plant-based wellness trends and clean-label formulations continue to accelerate adoption across food, cosmetics, and healthcare industries.

Soyasaponin Market Latest Trends

Growing Adoption of Functional and Preventive Nutrition

The global shift toward preventive healthcare is significantly increasing demand for bioactive plant compounds such as soyasaponins. Consumers are actively seeking ingredients that support cardiovascular health, immune function, metabolic wellness, and anti-aging benefits. Functional foods, fortified beverages, protein supplements, and wellness-focused dietary products increasingly incorporate soyasaponins due to their scientifically supported health benefits. Manufacturers are launching premium formulations targeted at cholesterol management, inflammation reduction, and antioxidant support, further strengthening demand. This trend is particularly evident in North America, Europe, Japan, and South Korea, where aging populations and health-conscious consumers continue to drive innovation in functional nutrition products.

Sustainable Recovery from Soy Processing By-products

Sustainability has emerged as a key trend shaping the soyasaponin industry. Manufacturers are increasingly recovering soyasaponins from soy molasses, defatted soy meal, and soy protein processing residues, transforming low-value waste streams into high-margin functional ingredients. The trend aligns with global circular economy objectives and sustainability mandates adopted by food and ingredient producers. Advanced extraction technologies such as membrane filtration, enzymatic extraction, and supercritical fluid extraction are improving recovery efficiency while reducing environmental impact. Large soybean processing countries including China, Brazil, the United States, and Argentina are investing heavily in integrated extraction facilities that maximize resource utilization and improve overall production economics.

Soyasaponin Market Drivers

Rising Demand for Natural and Clean-Label Ingredients

Consumers increasingly prefer plant-derived ingredients over synthetic additives in food, supplements, cosmetics, and healthcare products. Clean-label product development has become a major focus area for manufacturers worldwide, creating substantial opportunities for soyasaponin suppliers. Regulatory scrutiny of artificial ingredients and growing awareness of ingredient transparency continue to support demand for natural bioactive compounds. Soyasaponins fit well within this trend due to their natural origin and multifunctional health benefits.

Expansion of the Global Nutraceutical Industry

The rapid growth of dietary supplements and functional nutrition products remains one of the strongest growth drivers for the soyasaponin market. Global consumers are increasingly investing in preventive healthcare solutions that address immunity, cardiovascular health, and healthy aging. Soyasaponins have demonstrated strong potential in supporting cholesterol reduction, anti-inflammatory activity, and antioxidant protection, making them attractive ingredients for supplement manufacturers. The expanding middle-class population in Asia-Pacific and increasing wellness spending in developed economies are further accelerating nutraceutical demand.

Advancements in Extraction and Purification Technologies

Continuous technological innovation is improving the commercial feasibility of soyasaponin production. Modern extraction techniques enable higher yields, better purity levels, and improved product consistency while reducing manufacturing costs. Enhanced purification technologies have also expanded the use of pharmaceutical-grade soyasaponins in clinical and therapeutic applications. These advancements are allowing manufacturers to enter premium markets where regulatory requirements and product performance standards are significantly higher.

Soyasaponin Market Restraints

High Production and Purification Costs

Despite increasing demand, soyasaponin extraction remains relatively capital-intensive. High-purity formulations require sophisticated purification systems and quality control measures, resulting in elevated production costs. Smaller manufacturers often face challenges in achieving economies of scale, limiting their ability to compete with established suppliers.

Regulatory and Allergen Labeling Challenges

As soyasaponins are derived from soybean sources, manufacturers must comply with stringent allergen labeling regulations across multiple jurisdictions. Regulatory approvals for health claims and functional ingredient applications can also vary significantly by region, creating additional compliance costs and market entry barriers for producers.

Soyasaponin Industry Key Opportunities

Expansion into Natural Cosmetic Formulations

The global beauty and personal care industry is rapidly shifting toward botanical and naturally derived ingredients. Soyasaponins serve as effective natural surfactants, foaming agents, and anti-aging bioactives, making them attractive alternatives to synthetic ingredients. Premium skincare and haircare manufacturers are increasingly incorporating soyasaponins into sulfate-free and clean-label formulations. This opportunity is expected to generate above-average growth compared with traditional applications over the next decade.

High-Value Pharmaceutical Applications

Ongoing research into anti-inflammatory, immune-supportive, and cardioprotective properties of soyasaponins is creating opportunities in pharmaceutical development. As clinical evidence expands, pharmaceutical-grade soyasaponins could become important components of advanced therapeutic formulations. Manufacturers investing in high-purity extraction technologies and regulatory approvals are expected to benefit from higher margins and stronger long-term demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.12 Billion |

| Market Size in 2026 | USD 1.18 Billion |

| Market Size in 2031 | USD 1.56 Billion |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The soyasaponin market is segmented into Group A, Group B, DDMP (2,3-dihydro-2,5-dihydroxy-6-methyl-4H-pyran-4-one), Group E, and purified soyasaponin blends. Among these, Group B soyasaponins dominate the global market, accounting for approximately 38% of total revenue in 2025. Their market leadership is primarily attributed to extensive scientific validation of their bioactive properties, broad therapeutic potential, and widespread incorporation into pharmaceutical, nutraceutical, and functional health formulations. Growing research highlighting their anti-inflammatory, antioxidant, cholesterol-lowering, and immune-supporting effects continues to strengthen demand across multiple industries. The segment also benefits from established extraction technologies and favorable commercial scalability, making Group B soyasaponins the preferred choice among ingredient manufacturers.Group A soyasaponins maintain a significant market presence due to their widespread use in food, beverage, and dietary supplement applications. Increasing consumer demand for plant-based bioactive ingredients and functional nutrition products supports continued adoption. DDMP soyasaponins are attracting growing commercial and scientific interest owing to their strong antioxidant activity and potential role in chronic disease prevention. Rising investments in nutraceutical innovation and preventive healthcare research are expected to accelerate demand for DDMP variants during the forecast period. Group E soyasaponins continue to serve specialized applications, particularly in advanced health formulations and research-driven product development. Meanwhile, purified soyasaponin blends are witnessing increasing adoption as manufacturers seek standardized ingredients that provide consistent efficacy, regulatory compliance, and formulation flexibility across pharmaceutical, food, cosmetic, and animal nutrition applications.

Source Material Insights

Based on source material, the market is categorized into soybean seeds, soy molasses, defatted soy flour, soy meal, and soy protein processing residues. Soybean seed-derived soyasaponins represent approximately 63% of global market revenue, making them the leading source segment. The dominance of soybean seeds is supported by abundant global availability, well-established agricultural supply chains, mature extraction infrastructure, and consistent raw material quality. The high concentration of recoverable soyasaponins in soybean seeds enables efficient large-scale production, supporting their extensive use across nutraceutical, pharmaceutical, and food applications.Soy molasses-derived soyasaponins are emerging as one of the fastest-growing source categories due to increasing emphasis on sustainable manufacturing practices and waste valorization initiatives. As industries seek to improve resource efficiency and support circular economy objectives, the utilization of soy processing by-products has gained considerable momentum. Defatted soy flour and soy meal-derived soyasaponins are also experiencing increasing adoption as manufacturers aim to maximize extraction economics while utilizing readily available secondary processing streams. Additionally, soy protein processing residues are gaining attention as promising alternative feedstocks due to their substantial concentration of bioactive compounds and growing availability from expanding soy protein production activities worldwide. Increasing focus on sustainable sourcing and cost-effective extraction technologies is expected to support diversification of raw material utilization over the forecast period.

Purity Level Insights

The market is segmented into below 40% purity, 40–70% purity, 70–90% purity, and above 90% purity categories. The 70–90% purity segment holds the largest market share, accounting for approximately 35% of global revenue in 2025. This segment benefits from its optimal balance between manufacturing cost, product performance, and commercial scalability. The purity range provides sufficient bioactive concentration for most nutraceutical, food, cosmetic, and pharmaceutical applications while maintaining competitive production economics. As a result, it remains the preferred specification among ingredient suppliers and formulation companies.The above 90% purity segment is projected to register the fastest growth throughout the forecast period, driven by rising pharmaceutical research, increasing demand for standardized active ingredients, and growing regulatory emphasis on product consistency and efficacy. High-purity soyasaponins are increasingly utilized in premium nutraceutical products, clinical research programs, and advanced therapeutic formulations where precise bioactive concentrations are essential. The 40–70% purity category continues to maintain substantial demand across food processing, functional beverages, and animal nutrition applications where ultra-high purity is not a critical requirement. Products below 40% purity remain relevant for industrial and cost-sensitive applications; however, their market share is gradually declining as customers increasingly prioritize premium formulations, enhanced functionality, and quality assurance.

Application Insights

Pharmaceutical applications account for approximately 41% of global soyasaponin demand, making them the largest application segment in 2025. The segment's leadership is driven by growing interest in naturally derived therapeutic compounds, expanding clinical investigations into soyasaponin bioactivity, and increasing demand for plant-based pharmaceutical ingredients. Research exploring the anti-inflammatory, antioxidant, immunomodulatory, cholesterol-lowering, and anticancer potential of soyasaponins continues to create new opportunities for pharmaceutical manufacturers. Rising investments in drug development and preventive healthcare further strengthen demand across this segment.Functional foods and dietary supplements represent the second-largest application category, supported by increasing consumer awareness of preventive healthcare, healthy aging, and wellness-focused lifestyles. Demand for naturally sourced ingredients with scientifically supported health benefits continues to encourage incorporation of soyasaponins into nutritional products. Cosmetic and personal care applications are among the fastest-growing segments, benefiting from increasing preference for natural active ingredients, clean-label beauty products, and plant-based surfactants. Soyasaponins are increasingly utilized in anti-aging, skin protection, and formulation stabilization applications. Animal nutrition applications are also expanding steadily as feed manufacturers investigate the potential of soyasaponins to improve gut health, nutrient absorption, immune performance, and overall feed efficiency in livestock production systems.

Distribution Channel Insights

The distribution landscape is dominated by direct business-to-business supply agreements, which account for approximately 52% of global sales. The leading position of this segment is supported by long-term procurement contracts, stringent quality requirements, and the need for reliable supply continuity among pharmaceutical, nutraceutical, and food ingredient manufacturers. Direct sourcing allows buyers to maintain greater control over ingredient specifications, traceability, regulatory compliance, and pricing stability, making it the preferred distribution channel across large-scale industrial applications.Ingredient distributors continue to play a vital role in market expansion by providing regional accessibility, technical support, and inventory management services for small and medium-sized manufacturers. Contract formulation partnerships are gaining increasing importance as companies seek customized ingredient solutions, product development expertise, and accelerated commercialization timelines. Meanwhile, online specialty ingredient platforms are emerging as a rapidly evolving distribution channel, particularly among research institutions, start-up nutraceutical brands, specialty cosmetic manufacturers, and smaller formulation companies seeking flexible procurement options and broader supplier access.

End-Use Industry Insights

The nutraceutical industry represents the largest end-use segment, accounting for approximately 34% of global soyasaponin demand in 2025. The segment's leadership is primarily driven by rising global consumption of dietary supplements, increasing focus on preventive healthcare, growing aging populations, and expanding consumer demand for natural bioactive ingredients with scientifically supported health benefits. As wellness and self-care trends continue to influence purchasing behavior, nutraceutical manufacturers are increasingly incorporating soyasaponins into formulations targeting cardiovascular health, immune support, metabolic wellness, and healthy aging.Pharmaceutical companies remain major consumers of soyasaponins due to ongoing therapeutic research, expanding interest in plant-derived active compounds, and increasing development of evidence-based natural health products. The food and beverage industry is witnessing growing adoption as manufacturers incorporate soyasaponins into functional foods, fortified products, and health-oriented formulations designed to deliver additional nutritional value. Cosmetic and personal care manufacturers are increasingly utilizing soyasaponins as multifunctional ingredients offering emulsification, antioxidant protection, and skin-conditioning benefits. Animal feed applications continue to emerge as a promising growth area, particularly in Asia-Pacific and Latin America, where improving livestock productivity, feed efficiency, and animal health remains a strategic priority for agricultural producers.

Explore more data points, trends and opportunities Download Free Sample Report

Soyasaponin Market Segmentations

By Product Type

- Group A Soyasaponins

- Group B Soyasaponins

- DDMP Soyasaponins

- Group E Soyasaponins

- Purified Soyasaponin Blends

By Source Material

- Soybean Seed-Derived Soyasaponins

- Soy Molasses-Derived Soyasaponins

- Defatted Soy Flour/Meal-Derived Soyasaponins

- Soy Protein Processing By-product Derived Soyasaponins

- Other Soy Processing Residue-Derived Soyasaponins

By Purity Level

- Below 40% Purity

- 40–70% Purity

- 70–90% Purity

- Above 90% Purity

By Form

- Powder

- Liquid

- Granules

- Encapsulated/Standardized Formulations

By Application

- Functional Foods

- Dietary Supplements & Nutraceuticals

- Pharmaceuticals

- Cosmetics & Personal Care

- Animal Nutrition & Feed Additives

- Food Ingredient Processing Aids

- Research & Specialty Applications

Regional Insights

North America

North America accounted for approximately 36% of the global soyasaponin market in 2025, making it the largest regional market. The United States alone represented nearly 29% of worldwide demand, supported by a mature nutraceutical industry, high consumer spending on wellness products, advanced pharmaceutical research infrastructure, and strong adoption of preventive healthcare practices. The region benefits from widespread consumer acceptance of dietary supplements, increasing demand for clean-label ingredients, and a highly developed functional food market. Growing investments in botanical ingredient research and expanding clinical validation of plant-based bioactives continue to support market growth. Canada contributes significantly through its expanding natural health products sector, favorable regulatory framework for nutraceuticals, and increasing utilization of plant-derived ingredients across food, pharmaceutical, and personal care applications. Rising demand for evidence-based wellness products remains the primary driver supporting regional expansion.

Europe

Europe accounts for approximately 25% of global demand and remains one of the most established markets for soyasaponin-based products. Germany leads regional consumption owing to its advanced nutraceutical manufacturing sector, strong pharmaceutical industry presence, and growing preference for natural health solutions. The United Kingdom, France, Italy, and Spain also contribute significantly through rising demand for botanical ingredients, functional nutrition products, and clean-label consumer goods. Stringent European regulations emphasizing ingredient quality, safety, traceability, and scientific substantiation continue to encourage adoption of standardized and high-purity soyasaponin formulations. Increasing consumer focus on preventive healthcare, healthy aging, and sustainable plant-based ingredients serves as a major growth catalyst. Additionally, expanding demand for natural cosmetic ingredients and functional foods further supports market development across the region.

Asia-Pacific

Asia-Pacific accounted for approximately 25% of global demand in 2025 and represents the fastest-growing regional market, with growth exceeding 6.2% annually. China serves as both the largest producer and one of the largest consumers due to its extensive soybean cultivation, processing infrastructure, and rapidly expanding nutraceutical industry. Japan remains a global leader in functional food innovation and continues to drive demand through advanced research into bioactive ingredients and health-promoting food products. India is emerging as one of the fastest-growing markets, supported by rising disposable incomes, increasing health awareness, expanding dietary supplement consumption, and growing investments in domestic nutraceutical manufacturing. South Korea and Australia contribute through strong demand for premium wellness products, advanced food technology sectors, and increasing adoption of plant-based health ingredients. The region's growth is primarily driven by expanding middle-class populations, rising healthcare expenditures, growing preventive health awareness, and the presence of a large soybean processing ecosystem.

Latin America

Latin America occupies a strategically important position within the global soyasaponin value chain due to its substantial soybean production capacity. Brazil dominates regional production and export activity, while Argentina maintains a significant role through large-scale soybean cultivation and processing operations. The region benefits from abundant raw material availability, competitive agricultural economics, and increasing investments in value-added ingredient manufacturing. Growing efforts to diversify beyond commodity exports and develop higher-margin bioactive ingredient industries are expected to strengthen regional market growth. Rising demand for animal nutrition products, expanding functional food consumption, and increasing participation in global nutraceutical supply chains further support long-term development. Continued modernization of agricultural processing infrastructure is expected to enhance the region's competitiveness in soyasaponin extraction and commercialization.

Middle East & Africa

The Middle East & Africa region currently accounts for approximately 5% of global demand but offers considerable long-term growth potential. Saudi Arabia and the United Arab Emirates are leading regional demand growth through expanding dietary supplement markets, increasing consumer spending on premium wellness products, and rising adoption of natural personal care ingredients. Growing government initiatives aimed at healthcare diversification and wellness promotion are further supporting market development. South Africa remains the largest sub-Saharan market due to increasing consumer awareness of preventive healthcare, expanding pharmaceutical manufacturing activities, and rising demand for functional nutrition products. Across the broader region, improving healthcare infrastructure, increasing urbanization, expanding retail availability of nutraceutical products, and growing interest in plant-based health solutions are expected to create favorable conditions for future soyasaponin market expansion.

Key Players in the Soyasaponin Market

- Merck KGaA

- Thermo Fisher Scientific

- FUJIFILM Wako Pure Chemical Corporation

- Cayman Chemical Company

- Sigma-Aldrich

- TCI Chemicals

- Chengdu Biopurify Phytochemicals Ltd.

- Xi'an Lyphar Biotech Co., Ltd.

- Shaanxi Undersun Biomedtech Co., Ltd.

- Nanjing Zelang Medical Technology Co., Ltd.

- Sabinsa Corporation

- Martin Bauer Group

- Avestia Pharma

- Phyto Life Sciences

- Naturalin Bio-Resources Co., Ltd.