Nutrition Wine Market Size

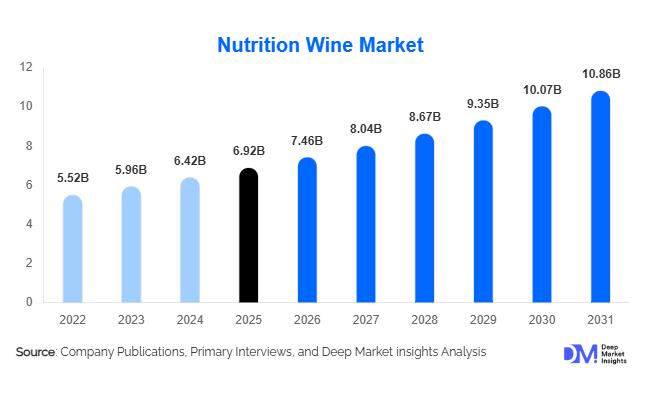

According to Deep Market Insights, the global nutrition wine market size was valued at approximately USD 6.92 billion in 2025 and is projected to grow from USD 7.46 billion in 2026 to reach USD 10.86 billion by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The nutrition wine market growth is being driven by rising consumer demand for functional beverages, increasing awareness of preventive healthcare, growing adoption of antioxidant-rich alcoholic products, and expanding innovation in herbal and botanical wine formulations. The convergence of wellness trends and premium alcoholic beverage consumption has positioned nutrition wine as one of the fastest-growing niche categories within the global functional beverage industry.

Key Market Insights

- Herbal and botanical nutrition wines account for nearly 50% of global market revenue, supported by strong consumer acceptance across Asia-Pacific markets.

- Red nutrition wine remains the leading wine base segment, benefiting from consumer perception regarding natural antioxidant and polyphenol content.

- Asia-Pacific dominates the global nutrition wine market, accounting for approximately 47% of global demand, led by China, Japan, and South Korea.

- North America represents the fastest-growing regional market, driven by premiumization and growing interest in functional alcoholic beverages.

- Online retail and direct-to-consumer sales channels are expanding rapidly, enabling manufacturers to educate consumers on nutritional benefits and ingredient functionality.

- Low-alcohol and alcohol-free nutrition wine products are gaining traction, supported by health-conscious consumers seeking moderation without sacrificing wellness attributes.

- Functional ingredients such as ginseng, goji berry, probiotics, collagen, amino acids, and adaptogens are increasingly being incorporated into premium nutrition wine formulations.

Nutrition Wine Market Latest Trends

Functional and Wellness-Oriented Alcohol Beverages Gaining Mainstream Acceptance

The global alcoholic beverage industry is undergoing a significant transformation as consumers increasingly seek products that offer perceived health and wellness benefits. Nutrition wine has emerged as a prominent beneficiary of this trend by combining traditional wine consumption with functional ingredients such as botanical extracts, vitamins, antioxidants, probiotics, and nutraceutical compounds. Manufacturers are launching specialized formulations targeting immunity support, digestive health, cardiovascular wellness, stress management, and healthy aging. Premium consumers increasingly view nutrition wine as a lifestyle product that complements broader wellness goals rather than merely serving as a recreational alcoholic beverage. This trend is particularly evident among urban professionals, affluent consumers, and aging populations seeking healthier consumption alternatives.

Rise of Low-Alcohol and Alcohol-Free Nutrition Wine Products

Alcohol moderation trends are creating substantial opportunities within the nutrition wine market. Consumers are increasingly adopting balanced lifestyles and reducing alcohol intake while continuing to seek sophisticated beverage experiences. In response, manufacturers are introducing low-alcohol and alcohol-free nutrition wines fortified with functional ingredients such as antioxidants, adaptogens, collagen, and probiotics. These products are attracting younger consumers, wellness-focused individuals, and health-conscious women who prioritize nutritional benefits without excessive alcohol consumption. Technological advancements in dealcoholization and flavor preservation are further supporting product quality improvements and broader market adoption.

Nutrition Wine Market Drivers

Growing Consumer Demand for Functional Beverages

The rapid expansion of the global functional beverage sector is serving as a major growth catalyst for nutrition wine. Consumers increasingly prioritize products that contribute to overall well-being, disease prevention, and healthy lifestyles. Nutrition wine addresses this demand by offering ingredients associated with antioxidant activity, cardiovascular support, and immune health. The category benefits from increasing awareness surrounding nutraceuticals, plant-based wellness ingredients, and preventive healthcare solutions. As consumers become more informed regarding functional food and beverage products, demand for nutrition wine continues to strengthen across both developed and emerging economies.

Rising Healthcare Awareness and Preventive Wellness Spending

Preventive healthcare has become a central component of consumer spending patterns worldwide. Aging populations, rising healthcare costs, and increasing prevalence of lifestyle-related diseases are encouraging consumers to adopt wellness-focused purchasing behaviors. Nutrition wines enriched with resveratrol, polyphenols, vitamins, minerals, and herbal extracts are increasingly positioned as products supporting healthy aging and overall wellness. This shift is particularly evident in Asia-Pacific, Europe, and North America, where consumers are actively seeking products that complement long-term health objectives.

Innovation in Herbal and Botanical Formulations

Continuous innovation in botanical ingredient incorporation is creating new growth opportunities for nutrition wine manufacturers. Traditional medicinal ingredients such as ginseng, cordyceps, wolfberry, and various adaptogenic herbs are being integrated into modern wine formulations. These innovations appeal to consumers seeking natural ingredients and traditional wellness concepts. Product differentiation through proprietary botanical blends, scientifically supported health claims, and premium ingredient sourcing is enabling companies to command higher margins while expanding consumer adoption.

Nutrition Wine Market Restraints

Regulatory Complexity Across Multiple Jurisdictions

Nutrition wine manufacturers face significant regulatory challenges due to the dual nature of the product category, which combines alcoholic beverages with functional food ingredients. Health claims, ingredient approvals, labeling requirements, advertising restrictions, and alcohol taxation frameworks vary substantially across countries. Compliance costs can be particularly burdensome for smaller manufacturers seeking international expansion. Regulatory scrutiny surrounding functional claims may also limit marketing flexibility and delay product launches.

Consumer Skepticism Regarding Functional Health Claims

Despite growing interest in wellness products, some consumers remain skeptical regarding the health benefits associated with nutrition wine. Concerns regarding the compatibility of alcohol consumption and wellness objectives continue to create challenges for category expansion. Manufacturers must invest significantly in consumer education, scientific validation, and transparent labeling practices to establish credibility and improve long-term consumer trust.

Nutrition Wine Industry Key Opportunities

Expansion into Preventive Healthcare and Wellness Ecosystems

The growing global focus on preventive healthcare presents substantial opportunities for nutrition wine manufacturers. Products targeting healthy aging, cardiovascular wellness, stress management, and immunity support can be integrated into broader wellness ecosystems. Collaborations with nutraceutical companies, wellness retailers, healthcare practitioners, and lifestyle brands may further strengthen category positioning. Companies that successfully combine scientific validation with premium consumer experiences are expected to capture significant market share in the coming years.

Premiumization and Luxury Functional Beverage Positioning

Premium alcoholic beverages continue to outperform mass-market categories across many regions. Nutrition wine manufacturers are capitalizing on this trend by introducing super-premium formulations featuring rare botanical ingredients, organic certifications, sustainable production methods, and luxury packaging. Affluent consumers increasingly seek unique products that combine indulgence, exclusivity, and wellness benefits. Premium nutrition wines command significantly higher profit margins and offer attractive opportunities for both established producers and new market entrants.

Digital Commerce and Cross-Border E-Commerce Expansion

Digital sales channels are becoming increasingly important for nutrition wine manufacturers seeking global expansion. Online retail platforms allow companies to communicate product benefits, educate consumers regarding ingredients, and develop direct relationships with customers. Cross-border e-commerce is particularly beneficial for Asian producers targeting North American and European wellness consumers. Subscription-based sales models, personalized nutrition recommendations, and digital wellness communities are expected to create additional growth opportunities over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.92 Billion |

| Market Size in 2026 | USD 7.46 Billion |

| Market Size in 2031 | USD 10.86 Billion |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Herbal and botanical nutrition wine remains the dominant product category, accounting for approximately 49.9% of the global market in 2025. This leadership is primarily driven by deep-rooted consumer familiarity with traditional medicinal ingredients and the long-standing integration of herbal formulations into wellness culture, particularly across China, Japan, and South Korea. The segment benefits from strong cultural trust in botanical remedies, ongoing product innovation by manufacturers, and the expansion of modern functional beverage positioning that blends traditional medicine with contemporary lifestyle consumption. Increasing scientific validation of certain botanical extracts is further strengthening consumer confidence and accelerating premiumization within this category.Antioxidant-enriched nutrition wines represent the second-largest category, supported by rising global awareness of polyphenols, resveratrol, and their perceived role in supporting cellular health and anti-aging benefits. Functional wellness wines designed for digestive health, immune support, and healthy aging are among the fastest-growing segments, driven by the broader shift toward preventive healthcare and functional nutrition. Vitamin- and mineral-fortified wines are steadily gaining traction in developed markets where consumers seek structured nutritional supplementation through convenient formats. Alcohol-free nutrition wines are emerging as a high-growth niche, propelled by moderation trends, sober-curious lifestyles, and increasing demand for inclusive wellness beverages that cater to health-conscious and non-alcohol-consuming demographics.

Wine Base Insights

Red nutrition wine dominates the global market with an estimated 43.7% share in 2025. Its leadership is primarily supported by strong consumer perception of red wine as a naturally rich source of antioxidants, particularly polyphenols and resveratrol, which are widely associated with cardiovascular and anti-aging benefits. The segment is further strengthened by extensive historical consumption patterns, established production infrastructure, and premium positioning in both Western and Asian markets.White nutrition wines continue to gain popularity due to their lighter flavor profiles, lower perceived intensity, and increasing appeal among younger consumers and first-time wine drinkers. Rosé and sparkling nutrition wines are expanding rapidly within premium lifestyle and social consumption segments, benefiting from their association with celebratory occasions and modern, image-driven consumption behavior. Fortified nutrition wines remain concentrated in niche wellness markets where higher functional ingredient concentrations are preferred. Across all wine base categories, innovation in flavor profiling, functional ingredient blending, and sensory enhancement continues to be a key driver of differentiation and consumer expansion.

Distribution Channel Insights

Specialty health stores, wellness retailers, and pharmacies collectively account for approximately 41.1% of global nutrition wine sales, with leadership driven by consumer trust in expert guidance, product education, and the perceived credibility of health-focused retail environments. These channels play a critical role in influencing first-time adoption, particularly for functional and fortified beverage categories where ingredient understanding is essential for purchase decisions.Supermarkets and hypermarkets continue to provide mass-market accessibility and high-volume sales due to their extensive geographic penetration and convenience-driven purchasing behavior. Online retail and direct-to-consumer platforms represent the fastest-growing distribution channels, supported by accelerating digital adoption, personalized marketing capabilities, and the ability to communicate functional benefits through targeted content and influencer-driven engagement. Hospitality channels, including premium hotels, wellness resorts, and fine-dining establishments, are increasingly integrating nutrition wines into curated beverage programs, driven by the rise of experiential luxury consumption and wellness tourism.

Consumer Group Insights

Health-conscious consumers represent the largest customer segment, accounting for approximately 35% of global demand in 2025. Growth in this segment is primarily driven by increasing awareness of preventive healthcare, rising incidence of lifestyle-related health concerns, and a strong preference for functional products that align with long-term wellness goals. Fitness-oriented consumers are increasingly adopting low-alcohol and functional wine alternatives as part of active lifestyle routines, particularly in urban markets where wellness integration into daily consumption is accelerating.Aging populations represent a structurally important growth segment, especially in developed economies, where healthy aging, cognitive wellness, and cardiovascular health are key purchasing drivers. Female consumers are contributing significantly to demand growth, particularly for premium, low-calorie, and aesthetically positioned wellness wines that align with lifestyle and dietary preferences. Traditional herbal beverage consumers continue to underpin strong baseline demand in Asia-Pacific markets, where cultural familiarity with medicinal drinks reinforces adoption of nutrition-based wine formulations.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for nearly 58% of global nutrition wine demand. This dominance is supported by increasing consumer interest in at-home wellness routines, premium self-care experiences, and convenient functional beverage consumption integrated into daily lifestyles. The shift toward home-based wellness solutions has been further accelerated by digital commerce expansion and direct delivery models.Wellness and preventive healthcare applications represent the fastest-growing end-use category, driven by rising consumer focus on long-term health management and the integration of functional beverages into broader nutrition strategies. Hospitality establishments, including luxury hotels, wellness retreats, and premium restaurants, are expanding their offerings of nutrition wines as part of curated wellness and experiential dining programs. Corporate gifting applications are also gaining momentum, particularly in Asia-Pacific markets where premium health-oriented gifting aligns with cultural and business practices. Export-driven demand continues to expand rapidly as manufacturers leverage cross-border e-commerce platforms and global wellness trends to reach international consumers.

Explore more data points, trends and opportunities Download Free Sample Report

Nutrition Wine Market Segmentations

By Product Type

- Herbal & Botanical Nutrition Wine

- Vitamin & Mineral Fortified Wine

- Antioxidant-Enriched Wine

- Functional Wellness Wine

- Low-Alcohol Functional Wine

- Alcohol-Free Functional Wine

By Wine Base

- Red Nutrition Wine

- White Nutrition Wine

- Rosé Nutrition Wine

- Sparkling Nutrition Wine

- Fortified Nutrition Wine

By Ingredient Category

- Herbal Extracts

- Antioxidants (Resveratrol, Polyphenols)

- Vitamins & Minerals

- Amino Acids & Peptides

- Probiotics & Fermentation Cultures

- Fruit-Based Nutraceutical Ingredients

By Distribution Channel

- Specialty Health Stores & Pharmacies

- Supermarkets & Hypermarkets

- Online Retail & E-Commerce

- Direct-to-Consumer (D2C)

- Hospitality & Premium On-Premise Sales

By End Use

- Household Consumption

- Wellness & Preventive Healthcare

- Hospitality Industry

- Corporate Gifting

- Premium Retail Consumption

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global nutrition wine market with approximately 47% market share in 2025, and its leadership is reinforced by strong cultural integration of herbal medicine, expanding middle-class income levels, and increasing health awareness among urban populations. China remains the largest market, accounting for nearly one-third of global demand, driven by deep-rooted acceptance of herbal medicinal wines, strong domestic production ecosystems, and continuous product innovation in functional beverages. Japan and South Korea contribute significantly through demand for premium wellness-oriented beverages, supported by aging populations and high consumer sophistication. India is emerging as a high-potential growth market, fueled by rapid urbanization, rising disposable incomes, and increasing adoption of preventive healthcare lifestyles.

Europe

Europe accounts for approximately 24% of global nutrition wine demand, with growth driven by strong consumer preference for premium wines, organic formulations, and functional beverages aligned with clean-label expectations. Key markets such as Germany, France, Italy, Spain, and the United Kingdom benefit from mature wine cultures that are increasingly integrating wellness-oriented innovations. The primary growth driver in the region is the accelerating shift toward low-sugar, antioxidant-rich, and naturally derived beverage formulations, supported by stringent regulatory frameworks that emphasize ingredient transparency, product safety, and quality assurance. This regulatory environment is encouraging premiumization and fostering innovation in functional wine categories.

North America

North America holds approximately 18% of global market share and represents the fastest-growing regional market, with a projected CAGR of approximately 9.2% through 2031. Growth in the region is primarily driven by increasing consumer adoption of wellness-oriented lifestyles, strong demand for functional beverages, and rising interest in premium alcoholic innovations that combine health benefits with experiential consumption. The United States dominates regional demand, accounting for nearly three-quarters of consumption, supported by robust wellness industry infrastructure, advanced retail ecosystems, and high consumer willingness to adopt functional nutrition products. Canada is witnessing steady growth in low-alcohol and health-focused wine categories, supported by rising health consciousness and expanding premium beverage consumption trends.

Latin America

Latin America accounts for approximately 7% of global demand, with growth driven by rising middle-class incomes, increasing urbanization, and growing awareness of functional and health-enhancing beverages. Brazil, Mexico, Argentina, and Chile are the leading markets, supported by expanding wine consumption cultures and increasing openness to product innovation. A key driver in the region is the premiumization of beverage consumption patterns, where consumers are increasingly willing to pay for higher-value functional and wellness-oriented products. Local wine producers are also incorporating botanical and herbal ingredients into traditional wine offerings, blending regional agricultural strengths with global wellness trends.

Middle East & Africa

The Middle East & Africa region accounts for approximately 4% of global demand, with growth concentrated in select high-income and tourism-driven markets. South Africa leads both production and consumption due to its established wine industry and export capabilities. The United Arab Emirates is emerging as a key premium import market, driven by strong expatriate populations, luxury hospitality expansion, and rising demand for high-end wellness beverages. Regional growth is primarily supported by increasing investment in premium retail channels, expansion of tourism infrastructure, and growing interest in functional non-traditional beverages within urban consumer segments.

Key Players in the Nutrition Wine Market

- Zhizhonghe Health Wine

- Yedao Group

- Jinpai Health Industry

- Wandongyaoye

- Changyu Pioneer Wine

- Tongrentang Health Wine

- Guilin Sanjin Pharmaceutical Health Wine

- COFCO Great Wall Wine

- Treasury Wine Estates

- Constellation Brands

- The Wine Group

- Pernod Ricard Winemakers

- E. & J. Gallo Winery

- Accolade Wines

- Vina Concha y Toro