Bovine and Capra Colostrum Market Size

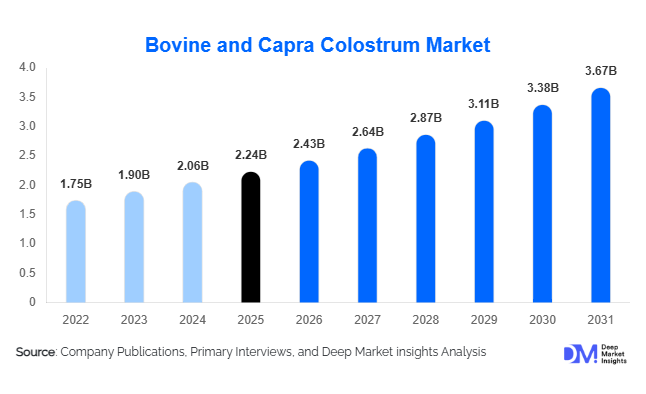

According to Deep Market Insights, the global bovine and capra colostrum market size was valued at USD 2.24 billion in 2025 and is projected to grow from USD 2.43 billion in 2026 to reach USD 3.67 billion by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The bovine and capra colostrum market growth is primarily driven by increasing consumer awareness regarding immune health, rising demand for natural bioactive ingredients in dietary supplements, growing adoption of premium infant nutrition products, and expanding applications in sports nutrition, medical nutrition, and animal health. Colostrum-derived ingredients are gaining significant traction due to their rich concentration of immunoglobulins, lactoferrin, growth factors, peptides, and other functional compounds that support immunity, gut health, recovery, and overall wellness.

Key Market Insights

- Bovine colostrum dominates the global market, accounting for approximately 86% of total revenue due to widespread dairy infrastructure and scalable production capabilities.

- Dietary supplements represent the largest application segment, contributing nearly 34% of global demand as consumers increasingly seek natural immune-support solutions.

- Powdered colostrum remains the preferred product form, representing over 55% of market revenue owing to superior shelf stability and formulation flexibility.

- North America leads the global market, supported by strong nutraceutical consumption and advanced dairy ingredient processing infrastructure.

- Asia-Pacific is the fastest-growing regional market, driven by rising demand for premium nutrition products in China, India, Japan, and South Korea.

- Goat-derived (capra) colostrum is emerging as a premium growth category, particularly within infant nutrition and digestive health formulations.

- Technological advancements in freeze-drying and low-temperature processing are improving bioactive retention and product efficacy.

- Veterinary nutrition and premium pet health applications are creating new growth opportunities for colostrum manufacturers globally.

Bovine and Capra Colostrum Market Latest Trends

Growing Demand for Immune Health and Preventive Nutrition

The global shift toward preventive healthcare continues to reshape demand patterns across the bovine and capra colostrum market. Consumers increasingly seek nutritional ingredients that provide immunity support while addressing digestive wellness, healthy aging, and overall health maintenance. Colostrum products are benefiting from growing scientific evidence surrounding immunoglobulins, lactoferrin, and growth factors. Manufacturers are responding by launching clinically supported formulations targeting immunity enhancement, gut microbiome support, and recovery nutrition. This trend is particularly evident in North America, Europe, China, Japan, and Australia, where preventive healthcare spending continues to increase. Premium supplement brands are also emphasizing traceability, bioactive preservation, and clean-label positioning to attract health-conscious consumers.

Expansion of Goat Colostrum-Based Premium Products

Capra colostrum is increasingly being positioned as a premium alternative to bovine colostrum due to perceived digestibility advantages and nutritional benefits. Demand is particularly strong across Asia-Pacific, where consumers often associate goat-derived nutrition with enhanced gastrointestinal tolerance and superior absorption. Manufacturers are introducing goat colostrum powders, capsules, infant nutrition ingredients, and specialty functional foods targeted at sensitive consumer groups. The trend is encouraging investment in specialized goat dairy operations and dedicated capra colostrum processing facilities. Premium pricing and growing consumer awareness are expected to support above-average growth rates for goat-derived colostrum products throughout the forecast period.

Bovine and Capra Colostrum Market Drivers

Rising Adoption of Dietary Supplements

The global dietary supplement industry continues to expand as consumers prioritize immunity, digestive health, and wellness. Colostrum ingredients align strongly with these consumer preferences due to their natural bioactive composition. Supplement manufacturers are increasingly incorporating bovine and capra colostrum into capsules, powders, chewables, and functional beverages. Growing health awareness among aging populations and increased preventive healthcare spending are further accelerating demand. The trend is particularly strong in developed markets where consumers are willing to pay premium prices for clinically supported nutritional ingredients.

Growth of Premium Infant Nutrition

Infant nutrition manufacturers are actively seeking bioactive ingredients that closely mimic the functional characteristics of human milk. Colostrum-derived proteins, growth factors, and immune-support compounds are increasingly being incorporated into premium infant formulations. Rising birth rates in selected emerging economies, combined with increasing disposable incomes and premiumization trends, are supporting adoption. Demand remains particularly strong in China, Southeast Asia, and parts of the Middle East where parents increasingly prioritize advanced nutritional products for infant development.

Expanding Sports and Recovery Nutrition Applications

Sports nutrition companies are increasingly leveraging colostrum's role in recovery, muscle support, gut health, and immune maintenance. Professional athletes, fitness enthusiasts, and active lifestyle consumers are adopting colostrum-based supplements as part of broader performance and recovery regimens. This trend is encouraging product innovation across protein blends, recovery beverages, endurance nutrition products, and specialized sports supplements. The increasing popularity of fitness culture worldwide continues to create sustained demand within this segment.

Bovine and Capra Colostrum Market Restraints

Limited Raw Material Availability

Colostrum collection occurs only during a short postpartum period, creating inherent supply limitations. Maintaining adequate supplies while ensuring animal welfare and neonatal nutrition requirements presents ongoing challenges for producers. Seasonal fluctuations, dairy herd productivity, and collection protocols can directly impact raw material availability and pricing stability. These supply constraints often limit large-scale expansion opportunities and contribute to premium pricing structures.

Regulatory and Health Claim Challenges

Manufacturers face increasingly stringent regulations regarding health claims associated with immune support and disease prevention. Regulatory agencies across North America, Europe, and Asia require extensive scientific substantiation before approving product claims. Compliance costs, registration requirements, and varying regional regulations can delay product commercialization and increase operational complexity. These factors may slow adoption in highly regulated applications such as pharmaceuticals and infant nutrition.

Bovine and Capra Colostrum Industry Key Opportunities

Medical Nutrition and Clinical Healthcare Applications

The growing medical nutrition sector presents significant opportunities for colostrum manufacturers. Research supporting gut health, immune modulation, gastrointestinal recovery, and elderly nutrition continues to expand the clinical relevance of colostrum-based ingredients. Hospitals, healthcare providers, and medical nutrition companies increasingly seek scientifically validated bioactive ingredients that support patient recovery and long-term health outcomes. Companies investing in clinical trials, proprietary formulations, and healthcare partnerships are expected to capture premium market opportunities over the coming decade.

Premium Animal Health and Pet Nutrition

Animal health applications are emerging as one of the fastest-growing opportunities within the global market. Livestock producers increasingly utilize colostrum-based supplements to improve neonatal survival rates, immune development, and overall productivity. Simultaneously, pet owners are driving demand for premium pet supplements focused on immunity, digestive health, and healthy aging. The ongoing humanization of pets is encouraging manufacturers to develop high-value companion animal nutrition products incorporating bovine and capra colostrum ingredients. This segment offers attractive margins and growing global demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.24 Billion |

| Market Size in 2026 | USD 2.43 Billion |

| Market Size in 2031 | USD 3.67 Billion |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Type Insights

The bovine colostrum segment dominated the global colostrum market in 2025, accounting for approximately 86% of total revenue. The segment’s leadership is primarily driven by the widespread availability of raw materials from large-scale dairy farming operations, established collection and processing infrastructure, and extensive scientific research validating the health benefits of bovine-derived bioactive compounds. Bovine colostrum contains a rich concentration of immunoglobulins, growth factors, lactoferrin, and other bioactive nutrients that support immune health, gut integrity, and overall wellness, making it highly attractive across nutraceutical, infant nutrition, sports nutrition, and animal health applications. The strong dairy industries in countries such as the United States, New Zealand, Australia, Germany, and the Netherlands provide a reliable supply chain, enabling manufacturers to achieve economies of scale and maintain consistent product quality. Furthermore, increasing incorporation of bovine colostrum into functional foods, dietary supplements, and clinical nutrition products continues to strengthen its market position.The capra (goat-derived) colostrum segment, while accounting for a smaller market share, is anticipated to witness robust growth throughout the forecast period. Growth is supported by rising consumer preference for specialty and premium nutritional ingredients, particularly among individuals seeking alternatives to conventional bovine-derived products. Goat colostrum is increasingly recognized for its favorable digestibility profile, smaller fat globules, and unique nutritional composition, which appeal to consumers with sensitive digestive systems. Demand is particularly increasing across Asia-Pacific and premium healthcare markets, where consumers are willing to pay higher prices for differentiated wellness products. Growing innovation in high-value nutraceutical formulations and increasing awareness regarding specialized immune-support products are expected to further accelerate adoption of capra colostrum globally.

Product Form Insights

The powdered colostrum segment accounted for approximately 55% of global market revenue in 2025, making it the leading product form category. The segment’s dominance is primarily attributed to its extended shelf life, superior product stability, ease of storage and transportation, and compatibility with a broad range of end-use applications. Powdered colostrum can be efficiently incorporated into dietary supplements, functional foods, sports nutrition products, infant nutrition formulations, and pharmaceutical preparations, making it highly versatile for manufacturers. In particular, freeze-dried powder formats have gained substantial popularity due to their ability to preserve sensitive bioactive compounds, including immunoglobulins and growth factors, while maintaining nutritional integrity. These advantages significantly reduce logistics costs and support wider global distribution, further reinforcing market demand.Capsules, tablets, and sachets are also experiencing notable growth as consumers increasingly seek convenient and standardized dosage formats that align with busy lifestyles. The growing popularity of preventive healthcare and personalized nutrition solutions has contributed to rising demand for portable supplement formats that offer ease of consumption and dosage accuracy. Meanwhile, liquid colostrum products continue to serve niche applications, particularly within infant nutrition and specialty healthcare products. However, challenges associated with shorter shelf life, cold-chain requirements, and higher transportation costs continue to limit large-scale adoption compared with powdered alternatives.

Application Insights

The dietary supplements segment emerged as the largest application category in 2025, accounting for nearly 34% of global market demand. The segment's leadership is primarily driven by growing consumer awareness regarding immune system support, digestive health, healthy aging, and preventive healthcare. Increasing interest in natural bioactive ingredients with clinically supported health benefits has encouraged manufacturers to expand colostrum-based supplement portfolios across both developed and emerging markets. Rising healthcare costs and a proactive approach toward wellness management are further contributing to sustained demand for colostrum supplements globally.Sports nutrition represents one of the fastest-growing application areas as athletes, fitness enthusiasts, and active consumers increasingly adopt colostrum-based products to support muscle recovery, performance enhancement, and immune resilience. The infant nutrition segment continues to offer substantial growth opportunities owing to increasing demand for advanced nutritional ingredients that closely mimic the functional properties of human breast milk. Functional foods and beverages are also witnessing expanding adoption as manufacturers seek scientifically validated ingredients capable of supporting wellness, immunity, and digestive health claims. In addition, animal nutrition applications are gaining momentum due to the growing use of colostrum in livestock health management, neonatal animal care, and premium companion animal nutrition, where immune support and gastrointestinal health remain key priorities.

Distribution Channel Insights

The B2B distribution channel accounted for approximately 62% of total market revenue in 2025, making it the dominant distribution segment globally. The primary driver of this leadership is the ingredient-centric nature of the colostrum industry, where manufacturers supply bulk colostrum ingredients directly to nutraceutical companies, pharmaceutical manufacturers, infant nutrition producers, food and beverage companies, and animal feed formulators. Large-scale procurement by industrial customers ensures stable demand while supporting long-term supply agreements and strategic partnerships across the value chain. The growing incorporation of colostrum into diversified product formulations further strengthens the importance of direct ingredient sales and industrial distribution networks.Within the B2C segment, online retail channels are projected to experience the fastest growth during the forecast period. Increasing internet penetration, growing consumer confidence in e-commerce platforms, and expanding direct-to-consumer supplement brands are driving online sales globally. Digital channels enable manufacturers to reach wider consumer bases while offering educational content regarding the health benefits of colostrum products. Pharmacies, specialty nutrition retailers, health stores, and wellness-focused retail chains continue to play a critical role in enhancing product visibility, consumer trust, and accessibility, particularly for premium and clinically positioned formulations.

End-Use Industry Insights

The nutraceutical industry remained the largest end-use sector in 2025, accounting for approximately 31% of total market revenue. The leading driver for this segment is the growing global demand for preventive healthcare solutions that support immune health, digestive wellness, and overall well-being. Consumers are increasingly shifting toward functional and natural health products, creating significant opportunities for colostrum-based ingredients that offer multiple clinically recognized benefits. Expanding product innovation and increasing investment in evidence-based nutritional formulations continue to support strong market penetration across the nutraceutical industry.The sports nutrition sector is increasingly integrating colostrum into performance enhancement and post-exercise recovery products, supported by growing participation in fitness activities and rising demand for functional protein-based nutrition. Infant nutrition remains a highly attractive segment due to increasing demand for premium formulations containing bioactive ingredients capable of supporting healthy growth and immune development. Animal nutrition is emerging as one of the fastest-growing end-use industries, particularly in neonatal livestock management, veterinary nutrition, and premium pet food formulations. Additionally, cosmetics and personal care manufacturers are exploring colostrum-derived bioactive compounds for applications related to skin rejuvenation, anti-aging, and cellular repair, creating new avenues for market expansion beyond traditional nutritional applications.

Explore more data points, trends and opportunities Download Free Sample Report

Bovine and Capra Colostrum Market Segmentations

By Source Type

- Bovine Colostrum

- Capra Colostrum

By Product Standardization

- Whole Colostrum

- Immunoglobulin-Enriched Colostrum

- Lactoferrin-Enriched Colostrum

- Growth Factor-Enriched Colostrum

- Defatted/Low-Fat Colostrum

- Specialty Formulated Colostrum Blends

By Form

- Powder

- Liquid

- Capsules

- Tablets

- Softgels

- Sachets/Stick Packs

By Nature

- Conventional

- Organic

By Application

- Dietary Supplements

- Functional Foods

- Functional Beverages

- Sports Nutrition

- Medical Nutrition

- Infant Nutrition

- Healthy Aging/Geriatric Nutrition

- Cosmetics & Dermaceuticals

- Animal Nutrition

Regional Insights

North America

North America accounted for approximately 34% of global market revenue in 2025, maintaining its position as the largest regional market. The United States represents the overwhelming majority of regional demand due to its highly developed nutraceutical industry, strong dietary supplement consumption patterns, advanced dairy processing capabilities, and extensive commercialization of functional health products. Market growth is further supported by increasing consumer awareness regarding preventive healthcare, rising demand for immunity-enhancing supplements, and growing adoption of sports nutrition products. The region also benefits from significant investments in nutritional research, strong regulatory oversight supporting product quality, and a well-established distribution network encompassing pharmacies, specialty retailers, and e-commerce platforms. Canada contributes to regional growth through increasing demand for premium wellness products, functional foods, and clinically supported nutritional supplements.

Europe

Europe represented approximately 27% of global market demand in 2025. Germany, the United Kingdom, France, Italy, and the Netherlands remain key contributors to regional revenue generation. Growth across Europe is driven by strong consumer preference for functional nutrition, medical nutrition products, and clean-label ingredients with transparent sourcing and scientifically validated health benefits. The region's mature healthcare infrastructure and growing aging population are encouraging greater adoption of immune-support and digestive health supplements. Additionally, stringent quality standards, increasing emphasis on product traceability, and rising demand for premium natural ingredients continue to create favorable conditions for colostrum manufacturers. Ongoing innovation in nutraceutical formulations and expanding consumer interest in preventive health management are expected to further support market expansion across European countries.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of global market revenue in 2025 and is projected to be the fastest-growing regional market throughout the forecast period. Regional growth is primarily driven by rising disposable incomes, rapid urbanization, expanding middle-class populations, increasing health consciousness, and strong growth in infant nutrition and dietary supplement consumption. China remains the largest regional market owing to substantial demand for premium infant formula products, immune-health supplements, and functional nutrition solutions. India is emerging as a major growth engine due to expanding e-commerce penetration, increasing healthcare awareness, a growing nutraceutical industry, and rising consumer spending on wellness products. Japan and South Korea continue to contribute significantly through demand for premium nutrition products, healthy aging solutions, and scientifically backed functional ingredients. Meanwhile, Southeast Asian countries are witnessing increasing adoption of functional foods and dietary supplements, supported by evolving consumer lifestyles and expanding retail infrastructure.

Latin America

Latin America accounted for approximately 8% of global market revenue in 2025. Brazil leads regional demand due to its expanding nutraceutical sector, growing health-conscious consumer base, and increasing acceptance of preventive healthcare products. The region is benefiting from rising disposable incomes, urban population growth, and improving consumer access to premium dietary supplements and wellness products. Mexico and Argentina are also experiencing increased adoption of colostrum-based nutritional products, supported by growing awareness of immune health, digestive wellness, and sports nutrition. Furthermore, expanding livestock industries and increasing investments in animal health management are creating additional growth opportunities for colostrum applications in veterinary and animal nutrition sectors throughout the region.

Middle East & Africa

The Middle East & Africa region represented approximately 7% of global market demand in 2025. Market growth is being driven by rising healthcare expenditure, increasing awareness regarding preventive health management, expanding demand for premium nutritional supplements, and growing consumption of imported specialty dairy ingredients. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa remain the leading regional markets due to higher consumer purchasing power and expanding wellness-focused retail sectors. The region is also witnessing increasing demand for premium infant nutrition products supported by favorable demographic trends and growing investments in healthcare infrastructure. Additionally, rising prevalence of lifestyle-related health concerns, growing interest in immunity-support products, and increasing penetration of international nutraceutical brands are expected to sustain long-term market growth across the Middle East and Africa.

Key Players in the Bovine and Capra Colostrum Market

- PanTheryx

- Sterling Technology

- Ingredia

- Biostrum Nutraceutical

- Good Health New Zealand

- Deep Blue Health

- APS BioGroup

- Anagenix

- The Saskatoon Colostrum Company

- Synertek Industries

- Bionatin

- Colostrum BioTec

- Farmlands Industries

- Now Foods

- Melrose Health