Lactobacillus Acidophilus Market Size

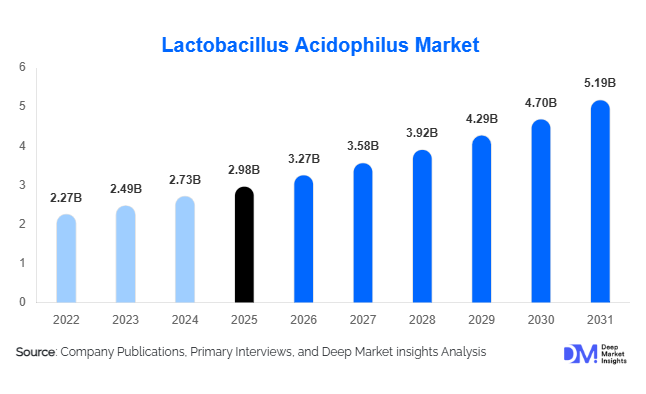

According to Deep Market Insights, the global Lactobacillus Acidophilus market size was valued at USD 2.98 billion in 2025 and is projected to grow from USD 3.27 billion in 2026 to reach USD 5.19 billion by 2031, expanding at a CAGR of 9.5% during the forecast period (2026–2031). Market growth is being driven by increasing consumer awareness of gut health, rising adoption of preventive healthcare practices, expanding demand for probiotic supplements, and growing incorporation of probiotic strains into functional foods, beverages, pharmaceuticals, and animal nutrition products. Lactobacillus acidophilus remains one of the most commercially established probiotic strains globally due to its strong scientific validation, broad regulatory acceptance, and effectiveness in supporting digestive health, immune function, and microbiome balance.

Key Market Insights

- Dietary supplements remain the largest application segment, accounting for nearly 46% of global market revenue owing to strong consumer demand for digestive and immune health products.

- Multi-strain probiotic formulations dominate the market, representing approximately 61% of global demand as consumers increasingly prefer broader-spectrum microbiome support.

- North America leads the global market, contributing approximately 34% of total revenue, supported by high healthcare spending and mature nutraceutical industries.

- Asia-Pacific is the fastest-growing region, led by China and India, where rising healthcare awareness and nutraceutical consumption are accelerating demand.

- Pharmaceutical applications are emerging rapidly, supported by growing clinical evidence for probiotic use in gastrointestinal and immune-related health conditions.

- Technological innovations in microencapsulation and strain stabilization are improving shelf life, viability, and efficacy across probiotic products.

Lactobacillus Acidophilus Market Latest Trends

Personalized Probiotics and Microbiome-Based Nutrition

The increasing adoption of personalized nutrition is transforming the Lactobacillus Acidophilus market. Consumers are increasingly seeking probiotic products tailored to their individual microbiome composition, health goals, age groups, and lifestyle factors. Companies are partnering with microbiome testing providers to develop customized probiotic regimens that incorporate Lactobacillus acidophilus as a core strain. The integration of artificial intelligence, genetic testing, and microbiome analytics is helping manufacturers create targeted products that improve customer engagement and retention. Personalized probiotic subscriptions and digital health platforms are expected to become major growth channels during the forecast period.

Expansion of Functional Food and Beverage Applications

Food and beverage manufacturers are increasingly incorporating Lactobacillus acidophilus into yogurts, fermented dairy products, plant-based beverages, nutrition bars, and fortified foods. Consumers are preferring convenient health solutions that can be integrated into daily diets without requiring separate supplement consumption. Product innovations in probiotic snacks, ready-to-drink beverages, and dairy alternatives are expanding addressable markets globally. The growing popularity of clean-label products and natural health ingredients is further supporting the incorporation of Lactobacillus acidophilus across functional food categories.

Lactobacillus Acidophilus Market Drivers

Growing Consumer Focus on Digestive and Immune Health

Consumers worldwide are increasingly recognizing the connection between gut health, immunity, metabolism, and overall well-being. Scientific research demonstrating the role of probiotics in supporting digestive health and microbiome balance has significantly increased consumer adoption. As healthcare systems shift toward preventive health management, demand for clinically supported probiotic strains such as Lactobacillus acidophilus continues to expand. Growing prevalence of digestive disorders and antibiotic-associated gut health issues is further contributing to market growth.

Expansion of Preventive Healthcare and Nutraceutical Spending

Preventive healthcare has become a major focus for consumers, healthcare providers, and governments globally. Individuals are increasingly investing in dietary supplements and wellness products to reduce long-term healthcare risks. The nutraceutical industry continues to experience strong growth across developed and emerging economies, driving demand for probiotic ingredients. Lactobacillus acidophilus is benefiting from this trend due to its established reputation and extensive use in premium digestive health formulations.

Lactobacillus Acidophilus Market Restraints

Challenges in Maintaining Strain Stability

Lactobacillus acidophilus is a living microorganism that requires careful handling throughout manufacturing, storage, transportation, and retail distribution. Maintaining adequate viability levels until consumption remains a significant challenge for manufacturers. Temperature fluctuations, moisture exposure, and extended storage periods can reduce product effectiveness and increase production costs. Companies must continue investing in advanced encapsulation and stabilization technologies to address these challenges.

Regulatory Complexity Across Global Markets

Regulatory requirements governing probiotics vary significantly across countries and regions. Manufacturers face challenges in obtaining approval for health claims, clinical substantiation requirements, labeling regulations, and product registration processes. Regulatory inconsistencies increase product development costs and can delay commercialization timelines, particularly for companies seeking global expansion.

Lactobacillus Acidophilus Industry Key Opportunities

Expansion into Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East represent substantial growth opportunities for probiotic manufacturers. Rising disposable incomes, urbanization, improving healthcare awareness, and growing middle-class populations are increasing demand for preventive health products. Countries such as India, China, Brazil, Indonesia, and Saudi Arabia are witnessing rapid expansion of nutraceutical and functional food markets. Establishing local manufacturing facilities and regional distribution networks can help companies capture these growing opportunities while reducing supply chain costs.

Clinical and Pharmaceutical Product Development

The pharmaceutical sector presents significant growth potential for Lactobacillus acidophilus manufacturers. Growing clinical evidence supporting probiotic applications in gastrointestinal disorders, antibiotic-associated diarrhea management, women's health, and immune support is encouraging pharmaceutical companies to incorporate probiotics into therapeutic formulations. Clinical-grade probiotic products often command higher pricing and stronger physician acceptance compared with conventional dietary supplements. Strategic collaborations between probiotic manufacturers and pharmaceutical companies are expected to accelerate innovation and market penetration.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.98 Billion |

| Market Size in 2026 | USD 3.27 Billion |

| Market Size in 2031 | USD 5.19 Billion |

| CAGR | 9.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Format Insights

Freeze-dried powder remains the leading product format in the global Lactobacillus Acidophilus market, accounting for approximately 38% of total revenue. The segment’s dominance is primarily driven by its superior strain stability, extended shelf life, high bacterial viability during storage, lower transportation and handling costs, and adaptability across a broad range of end-use applications. Manufacturers increasingly prefer freeze-dried powder for incorporation into dietary supplements, pharmaceutical formulations, functional foods, and customized probiotic blends because it enables efficient large-scale production while preserving probiotic potency. Continuous advancements in freeze-drying technologies and strain preservation methods are further strengthening the commercial appeal of this format.Capsules represent the second-largest product category, benefiting from growing consumer preference for convenient, easy-to-consume probiotic supplements with precise dosage control. Capsule-based formulations also provide enhanced protection against environmental factors and gastric conditions, supporting improved probiotic delivery. Tablet formulations continue to maintain strong demand, particularly in developed markets where consumers value portability, affordability, and familiarity. Meanwhile, liquid formulations, sachets, gummies, chewables, and other innovative delivery systems are witnessing robust growth as manufacturers target pediatric, geriatric, and lifestyle-oriented consumers seeking convenient wellness solutions. The growing adoption of microencapsulation and controlled-release technologies is improving probiotic survivability and expanding the range of commercially viable product formats across the market.

Strain Composition Insights

Multi-strain probiotic formulations dominate the Lactobacillus Acidophilus market, accounting for approximately 61% of global revenue. The segment’s leadership is driven by increasing consumer preference for comprehensive microbiome support and the perception that combinations of probiotic strains provide broader health benefits than single-strain products. Manufacturers are increasingly incorporating Lactobacillus acidophilus alongside Bifidobacterium species, Lactobacillus rhamnosus, Lactobacillus casei, and other clinically researched strains to address digestive health, immune function, metabolic wellness, and overall gut microbiota balance. Growing scientific evidence supporting synergistic interactions among probiotic strains is further encouraging product innovation and market adoption.Single-strain formulations continue to maintain an important position within the market, particularly in pharmaceutical, clinical nutrition, and research-based applications where targeted therapeutic outcomes and scientific validation are critical purchasing factors. Healthcare professionals often prefer single-strain products when specific health benefits are supported by clinical studies and regulatory approvals. As microbiome research continues to evolve, manufacturers are expected to invest heavily in both advanced multi-strain formulations and precision-targeted probiotic solutions, creating opportunities across multiple consumer and healthcare segments.

Application Insights

Dietary supplements account for approximately 46% of global Lactobacillus Acidophilus market revenue, making them the largest application segment. The segment’s dominance is driven by increasing consumer awareness regarding digestive health, immune system support, preventive healthcare, and microbiome wellness. Rising demand for self-care solutions, growing health-conscious populations, and expanding availability of probiotic supplements through both offline and online channels continue to support strong segment growth. Furthermore, consumers increasingly view probiotics as a daily wellness product rather than a treatment-specific supplement, contributing to sustained demand across developed and emerging markets.Functional foods represent the second-largest application area, supported by widespread incorporation of Lactobacillus acidophilus into yogurt, fermented dairy products, nutritional snacks, and fortified food products. Functional beverages are emerging as one of the fastest-growing categories as consumers seek convenient formats that integrate wellness benefits into everyday consumption habits. Pharmaceutical applications are expanding steadily due to increasing clinical evidence supporting probiotic interventions for gastrointestinal disorders, antibiotic-associated complications, and immune-related conditions. Additional growth opportunities are emerging in animal nutrition and personal care applications as manufacturers increasingly diversify probiotic utilization beyond traditional human dietary supplement markets.

Distribution Channel Insights

Pharmacies and drug stores account for approximately 32% of global sales, making them the leading distribution channel in the Lactobacillus Acidophilus market. The segment’s leadership is primarily driven by strong consumer trust in healthcare-oriented retail environments, access to professional guidance from pharmacists, and the growing preference for clinically supported probiotic products. Consumers frequently rely on pharmacist recommendations when selecting probiotic supplements, particularly for digestive and immune health concerns, reinforcing the channel’s continued importance.E-commerce represents the fastest-growing distribution channel, supported by rapid growth in online health product sales, subscription-based wellness programs, digital health awareness campaigns, and direct-to-consumer business models. Online platforms provide consumers with access to extensive product selections, educational content, customer reviews, and personalized purchasing experiences. Health and nutrition stores continue to play a critical role in premium and specialty probiotic product distribution, while supermarkets and hypermarkets maintain broad accessibility for mainstream probiotic brands. Institutional sales through hospitals, clinics, and healthcare facilities are also expanding as probiotic usage becomes increasingly integrated into preventive and therapeutic healthcare strategies.

Consumer Group Insights

Adults represent the largest consumer group, accounting for approximately 49% of total market demand. The segment’s dominance is driven by increasing awareness regarding digestive wellness, immune health, stress-related gut disorders, preventive healthcare practices, and overall lifestyle management. Growing incidences of digestive discomfort, changing dietary habits, and rising interest in microbiome optimization continue to encourage probiotic consumption among adult consumers globally.The geriatric population is emerging as one of the fastest-growing consumer categories due to increasing focus on healthy aging, gastrointestinal health maintenance, immune system support, and management of age-related digestive challenges. Women’s health formulations containing Lactobacillus acidophilus are experiencing strong growth as awareness increases regarding reproductive, vaginal, urinary tract, and hormonal health benefits. Pediatric probiotic products continue to witness robust demand as parents prioritize digestive and immune support for children from an early age. In addition, sports nutrition consumers are increasingly incorporating probiotics into wellness regimens to support nutrient absorption, recovery, gastrointestinal comfort, and overall athletic performance.

End-Use Industry Insights

The nutraceutical industry remains the largest end-use sector, contributing approximately 44% of global Lactobacillus Acidophilus demand. The segment’s leadership is driven by growing consumer preference for preventive healthcare solutions, rising demand for scientifically supported wellness products, continuous product innovation, and favorable premium pricing opportunities. Increasing investment in microbiome research and personalized nutrition solutions is further supporting the expansion of probiotic-based nutraceutical offerings.The food and beverage industry represents the second-largest end-use category, benefiting from strong demand for functional, fortified, and health-oriented food products. Pharmaceutical applications are among the fastest-growing sectors due to increasing clinical validation, physician recommendations, and growing integration of probiotics into evidence-based healthcare approaches. Animal health applications continue to expand as livestock producers seek sustainable alternatives to antibiotic growth promoters and focus on improving animal gut health and productivity. Furthermore, personal care manufacturers are increasingly exploring probiotic-based skincare, beauty, and wellness formulations, creating new opportunities for market diversification and long-term growth.

Explore more data points, trends and opportunities Download Free Sample Report

Lactobacillus Acidophilus Market Segmentations

By Product Format

- Freeze-Dried Powder

- Capsules

- Tablets

- Liquid Formulations

- Sachets & Stick Packs

- Other Delivery Formats

By Strain Composition

- Single-Strain Lactobacillus Acidophilus

- Multi-Strain Probiotic Formulations

By Potency (CFU Concentration)

- Below 1 Billion CFU

- 1–10 Billion CFU

- 10–50 Billion CFU

- Above 50 Billion CFU

By Application

- Dietary Supplements

- Functional Foods

- Functional Beverages

- Pharmaceutical Preparations

- Animal Nutrition & Feed

- Personal Care & Cosmetic Applications

By Distribution Channel

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Health & Nutrition Stores

- E-commerce Platforms

- Direct-to-Consumer Sales

- Institutional Sales

Regional Insights

North America

North America accounted for approximately 34% of the global Lactobacillus Acidophilus market in 2025, making it the largest regional market. The United States alone contributes nearly 28% of global demand, supported by strong consumer awareness, high healthcare expenditures, mature nutraceutical industries, and extensive supplement distribution networks. Canada continues to experience steady growth driven by increasing adoption of preventive healthcare products and functional foods. Demand across North America is increasingly shifting toward premium, clinically validated probiotic formulations supported by scientific evidence and healthcare professional recommendations.Regional growth is being driven by rising prevalence of digestive disorders, increasing consumer focus on gut microbiome health, strong penetration of dietary supplements, expanding personalized nutrition trends, and continuous innovation in probiotic product development. The presence of leading probiotic manufacturers, favorable consumer spending on health and wellness products, widespread e-commerce adoption, and growing physician acceptance of probiotic supplementation continue to reinforce North America's leadership position in the global market.

Europe

Europe represents approximately 29% of global market revenue, making it the second-largest regional market. Germany, the United Kingdom, France, Italy, and the Netherlands are among the region’s leading markets. Germany contributes nearly 7% of global demand due to its strong functional food industry, advanced healthcare infrastructure, and high probiotic acceptance rates. European consumers place significant emphasis on product quality, clinical evidence, regulatory compliance, and transparency, encouraging manufacturers to invest heavily in research-driven product development and scientifically substantiated health claims.The region’s growth is supported by increasing demand for natural and clean-label health products, growing consumer preference for preventive healthcare, expanding adoption of functional foods and beverages, and rising awareness regarding digestive and immune health. Sustainability initiatives, strong regulatory frameworks promoting product quality, and continuous innovation in microbiome-based nutrition are further accelerating market development across both Western and Eastern European countries.

Asia-Pacific

Asia-Pacific accounted for approximately 26% of global market revenue in 2025 and represents the fastest-growing regional market. China contributes nearly 10% of global demand and remains a major manufacturing and consumption hub for probiotic products. India is emerging as one of the fastest-growing country markets globally, supported by expanding healthcare awareness, rising disposable incomes, and rapid growth of the nutraceutical sector. Japan and South Korea maintain strong demand due to established probiotic consumption habits, aging populations, and highly developed functional food industries.Growth across Asia-Pacific is being driven by rapid urbanization, increasing middle-class populations, rising healthcare expenditures, expanding awareness of gut health, and growing demand for preventive nutrition solutions. The region is also benefiting from strong functional food consumption traditions, increasing investments in biotechnology and microbiome research, expansion of digital retail channels, and favorable demographic trends. Rising consumer interest in immunity enhancement, digestive wellness, and daily nutritional supplementation is expected to sustain robust market growth throughout the forecast period.

Latin America

Latin America contributes approximately 7% of global market revenue, with Brazil accounting for more than half of regional demand. Rising awareness regarding digestive health, increasing supplement consumption, and expanding retail distribution channels continue to support market growth. Argentina, Chile, and Mexico are also witnessing growing adoption of probiotic products as preventive healthcare trends strengthen and consumers become more proactive in managing overall wellness.Regional expansion is being driven by improving healthcare access, rising disposable incomes, increasing urbanization, growing penetration of dietary supplements, and expanding availability of functional foods and beverages. The rapid development of e-commerce platforms, growing investment in health and wellness industries, and increasing consumer awareness regarding the benefits of probiotics for digestive and immune health are expected to support continued market growth across Latin America.

Middle East & Africa

The Middle East & Africa region accounts for approximately 4% of global market revenue but offers significant long-term growth potential. Saudi Arabia, the United Arab Emirates, South Africa, and Egypt are among the leading markets. Rising healthcare investments, growing wellness awareness, and increasing demand for premium nutritional products are contributing to regional expansion. Governments across several countries are actively promoting healthcare modernization, biotechnology development, and preventive healthcare initiatives, creating favorable conditions for probiotic market growth.Key growth drivers include expanding healthcare infrastructure, increasing prevalence of lifestyle-related health conditions, rising consumer spending on nutritional supplements, growing awareness of digestive health benefits, and increasing availability of international probiotic brands. Furthermore, economic diversification programs, investments in pharmaceutical manufacturing capabilities, and expanding retail and e-commerce networks are expected to accelerate probiotic adoption and support long-term market development across the region.

Key Players in the Lactobacillus Acidophilus Market

- IFF Health (Danisco)

- Chr. Hansen

- Lallemand Health Solutions

- Probi AB

- BioGaia

- Kerry Group

- ADM Biopolis

- Morinaga Milk Industry

- Yakult Honsha

- Novonesis

- Biosearch Life

- Winclove Probiotics

- Protexin

- Deerland Probiotics & Enzymes

- Probiotical S.p.A.