Soy Chunks Market Size

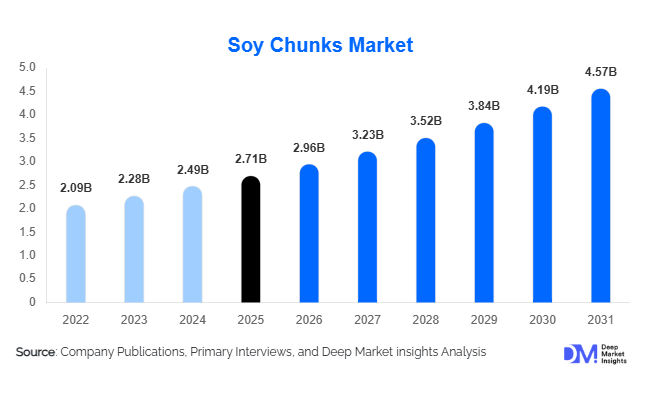

According to Deep Market Insights, the global soy chunks market size was valued at USD 2.71 billion in 2025 and is projected to grow from USD 2.96 billion in 2026 to reach USD 4.57 billion by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The soy chunks market growth is primarily driven by rising global demand for affordable plant-based proteins, increasing vegan and flexitarian dietary adoption, and the growing use of textured soy protein in processed food and meat alternative applications.

Key Market Insights

- Soy chunks are increasingly positioned as a cost-effective meat alternative, particularly in emerging economies where protein affordability remains critical.

- Plant-based food manufacturers are rapidly expanding soy protein usage, driven by rising consumer demand for vegan and flexitarian food products.

- Asia-Pacific dominates the global soy chunks market, led by strong consumption across India and China due to large vegetarian populations and expanding food processing sectors.

- North America represents one of the fastest-growing regions, supported by increasing investments in alternative proteins and sustainable food innovation.

- Organic and non-GMO soy chunks are gaining significant traction, particularly in Europe and North America where clean-label demand is accelerating.

- Advanced extrusion and flavor enhancement technologies are improving texture, taste, and product versatility, strengthening consumer acceptance globally.

Soy Chunks Market Latest Trends

Rising Adoption of Plant-Based Protein Diets

The global shift toward plant-based nutrition is significantly reshaping the soy chunks market. Consumers are increasingly reducing animal protein intake due to concerns surrounding health, sustainability, and animal welfare. Soy chunks are emerging as one of the most economical and protein-rich alternatives to meat, making them highly attractive across both developed and emerging markets. Vegan, vegetarian, and flexitarian diets are rapidly expanding, especially among younger consumers who prioritize sustainable food consumption. Foodservice providers and packaged food manufacturers are incorporating soy chunks into ready-to-eat meals, frozen products, protein snacks, and meat substitute formulations. This trend is particularly strong in Asia-Pacific and North America, where plant-based product launches continue to rise substantially.

Premiumization Through Organic and Fortified Products

Manufacturers are increasingly focusing on premium soy chunk offerings including organic, non-GMO, flavored, and fortified variants. Consumers are demanding clean-label products with higher nutritional value and improved functionality. Iron-fortified, calcium-enriched, and high-protein soy chunks are gaining popularity among health-conscious consumers, athletes, and elderly populations seeking nutritional support. Organic soy chunks are particularly witnessing robust demand growth in Europe and North America where regulatory standards and consumer awareness surrounding food transparency are high. Companies are also introducing innovative flavors and convenience-focused instant products to expand their consumer base beyond traditional vegetarian households.

Soy Chunks Market Drivers

Growing Demand for Affordable Protein Sources

The increasing global demand for affordable and nutritionally dense protein sources is one of the major drivers supporting soy chunks market expansion. Soy chunks offer significantly higher protein content at lower prices compared to animal proteins such as chicken, beef, and fish. In emerging economies including India, Indonesia, Nigeria, and parts of Latin America, soy chunks are widely consumed due to their affordability and long shelf life. Government nutritional programs and institutional meal schemes are also increasing the incorporation of soy protein products into food distribution systems. Rising inflation in meat prices and volatility in livestock supply chains have further accelerated demand for soy-based protein alternatives globally.

Expansion of Plant-Based Food Manufacturing

The rapid growth of the global plant-based food industry is substantially driving soy chunks consumption. Food manufacturers are increasingly utilizing textured soy protein due to its ability to mimic meat texture and absorb flavors efficiently. Soy chunks are widely used in burgers, sausages, curries, noodles, frozen meals, and protein snacks. Major food brands are investing heavily in plant-based product portfolios to meet changing consumer preferences. Advancements in extrusion technology and flavor engineering are improving product quality, making soy chunks more appealing to mainstream consumers. The growing popularity of flexitarian diets across North America and Europe is further accelerating industrial demand for soy protein ingredients.

Soy Chunks Market Restraints

Concerns Regarding GMO Soybeans

One of the key restraints affecting the soy chunks market is the growing consumer concern surrounding genetically modified soybeans. Several consumers, particularly in Europe and North America, prefer non-GMO and organic products due to health and environmental considerations. Compliance with GMO labeling regulations and certification requirements increases operational complexity and sourcing costs for manufacturers. Non-GMO soybean procurement also creates supply chain challenges in regions heavily dependent on genetically modified crop cultivation. These factors can impact pricing competitiveness and profit margins for soy chunk producers operating in premium markets.

Competition from Alternative Plant Proteins

The soy chunks market is facing increasing competition from alternative plant proteins such as pea protein, chickpea protein, fava bean protein, and mycoprotein. Many consumers are seeking diversified protein sources due to allergen concerns or perceptions regarding excessive soy consumption. The rapid commercialization of alternative protein technologies is creating competitive pressure, especially within premium plant-based food categories. Companies operating in the soy chunks market must therefore continue investing in innovation, nutritional education, and clean-label positioning to maintain long-term competitiveness and consumer loyalty.

Soy Chunks Industry Key Opportunities

Expansion into Emerging Export Markets

Rising protein demand across the Middle East, Africa, and Southeast Asia presents major export opportunities for soy chunk manufacturers. Countries with limited domestic protein production are increasingly importing affordable plant-based proteins to address food security concerns. India, China, Brazil, and the United States are strengthening soybean processing capabilities and export-oriented soy protein manufacturing infrastructure. Governments are also supporting value-added agricultural exports through food processing incentives and industrial development programs. Companies establishing integrated export supply chains and region-specific product formulations are expected to gain substantial long-term advantages.

Growth of Functional and Sports Nutrition Foods

The increasing popularity of protein-enriched diets and functional foods is creating strong opportunities for soy chunk manufacturers. High-protein soy chunks are increasingly being incorporated into sports nutrition products, weight management diets, and clinical nutrition applications. Functional food manufacturers are introducing fortified soy protein products targeting immunity support, heart health, and muscle recovery. Rising awareness regarding preventive healthcare and active lifestyles is encouraging consumers to seek convenient protein-rich food options. This trend is expected to accelerate premium product demand and improve profitability within the soy chunks industry over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.71 Billion |

| Market Size in 2026 | USD 2.96 Billion |

| Market Size in 2031 | USD 4.57 Billion |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Textured soy protein (TSP) chunks dominate the market, accounting for a significant share of global demand due to their high protein concentration, superior texture retention, and extensive usage in plant-based meat applications. These products are widely utilized in frozen foods, processed meals, institutional catering, and vegan meat alternatives because of their ability to replicate meat-like consistency at low cost. Organic and non-GMO soy chunks are witnessing the fastest growth, particularly in developed markets where consumers increasingly prioritize clean-label and sustainably sourced food products. Flavored soy chunks, including masala and barbecue variants, are also gaining popularity among younger consumers seeking convenience and enhanced taste profiles. Instant soy chunks designed for rapid cooking applications are expanding in urban markets driven by busy lifestyles and rising convenience food consumption.

Application Insights

Household cooking remains the leading application segment in the soy chunks market, particularly across Asia-Pacific where soy chunks are widely incorporated into traditional vegetarian meals and protein-rich curries. Meat substitute applications are emerging as the fastest-growing segment globally due to increasing demand for plant-based burgers, nuggets, sausages, and ready-to-eat meals. Food processing companies are extensively utilizing soy chunks in frozen foods, noodles, snacks, soups, and convenience foods because of their cost efficiency and high nutritional value. Sports nutrition and functional food applications are also expanding steadily as consumers seek protein-rich dietary options that support fitness and wellness goals. Institutional catering, including school meal programs and healthcare nutrition services, is becoming an important demand contributor in developing economies.

Distribution Channel Insights

Supermarkets and hypermarkets dominate soy chunk distribution globally due to their extensive product variety, organized retail infrastructure, and growing penetration in urban markets. Consumers prefer organized retail channels because they provide access to branded, packaged, and certified soy products. Online retail is emerging as the fastest-growing distribution channel, supported by expanding e-commerce grocery adoption and direct-to-consumer sales strategies. Health-focused specialty stores continue to maintain strong demand for premium organic and fortified soy chunk products. Wholesale and foodservice distribution channels are also witnessing substantial growth as restaurants, institutional kitchens, and processed food manufacturers increase bulk procurement of soy protein ingredients.

End-Use Insights

Residential consumers account for the largest share of soy chunk demand globally due to widespread household adoption of soy-based protein products in vegetarian and flexitarian diets. The food processing industry represents one of the fastest-growing end-use segments as manufacturers increasingly integrate textured soy proteins into convenience foods and meat substitute products. Restaurants and foodservice providers are rapidly incorporating soy chunks into menu offerings to cater to rising vegan and health-conscious consumer demand. Institutional buyers including schools, hospitals, and military organizations are also increasing soy chunk procurement due to affordability and nutritional benefits. The sports nutrition industry is emerging as a high-growth niche segment supported by increasing demand for protein-rich plant-based foods among fitness-oriented consumers.

Explore more data points, trends and opportunities Download Free Sample Report

Soy Chunks Market Segmentations

By Product Type

- Defatted Soy Chunks

- Textured Soy Protein (TSP) Chunks

- Organic Soy Chunks

- Non-GMO Soy Chunks

- Flavored Soy Chunks

- Instant Soy Chunks

- High-Protein Soy Chunks

By Nature

- Conventional

- Organic

By Form

- Granules

- Mini Chunks

- Regular Chunks

- Large Chunks

- Nuggets

By Application

- Household Cooking

- Meat Substitute Products

- Ready-to-Eat Meals

- Frozen Foods

- Protein Supplements

- Functional Foods

- Institutional Catering

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health Stores

- Online Retail

- Direct-to-Consumer (D2C)

- Foodservice Distribution

Regional Insights

North America

North America accounts for a significant share of the global soy chunks market, led primarily by the United States and Canada. Rising vegan and flexitarian dietary adoption, coupled with strong investments in plant-based food innovation, are driving regional demand growth. Consumers increasingly prefer non-GMO and organic soy products, encouraging manufacturers to expand premium product portfolios. The region also benefits from advanced food processing infrastructure and strong retail penetration of alternative protein products.

Europe

Europe represents a major growth market for soy chunks, supported by increasing demand for sustainable and clean-label foods. Germany, the United Kingdom, France, and the Netherlands are among the leading markets due to high vegan population growth and favorable regulatory support for plant-based foods. Organic soy chunks are witnessing particularly strong demand across European markets where consumers prioritize traceability, food transparency, and environmental sustainability. Retailers are significantly expanding shelf space dedicated to plant-based protein products.

Asia-Pacific

Asia-Pacific dominates the global soy chunks market with nearly 48% market share in 2025. India remains the largest consumer globally due to its large vegetarian population and widespread household usage of soy chunks as an affordable protein source. China represents another major market supported by large-scale soybean processing capabilities and expanding plant-based food manufacturing industries. Southeast Asian countries including Indonesia, Thailand, and Vietnam are witnessing increasing soy protein consumption due to urbanization, rising disposable incomes, and growing awareness regarding protein-rich diets.

Latin America

Latin America is experiencing steady market growth, particularly in Brazil, Argentina, and Mexico. Brazil benefits from extensive soybean cultivation infrastructure and increasing investments in value-added soy protein manufacturing. Demand for soy chunks is rising due to increasing processed food production and growing interest in affordable protein alternatives. Regional export opportunities are also strengthening as Latin American producers expand international trade partnerships.

Middle East & Africa

The Middle East & Africa region represents one of the fastest-growing markets for soy chunks due to rising urbanization, food security concerns, and increasing demand for affordable protein products. Countries including the UAE, Saudi Arabia, and South Africa are witnessing growing imports of soy-based protein foods. Institutional feeding programs and rising health awareness are further supporting market growth across African economies. Expanding foodservice sectors and increasing demand for processed convenience foods are expected to accelerate regional consumption over the forecast period.

Key Players in the Soy Chunks Market

- Archer Daniels Midland Company

- Cargill Incorporated

- International Flavors & Fragrances Inc.

- Wilmar International Ltd.

- CHS Inc.

- Sonic Biochem Extractions Ltd.

- Nutrela (Ruchi Soya Industries)

- The Scoular Company

- Devansoy Inc.

- Victoria Group

- Shandong Yuxin Bio-Tech Co., Ltd.

- Fuji Oil Holdings Inc.

- Bremil Group

- Crown Soya Protein Group

- Soya Food South Africa