Sesame Seeds Market Size

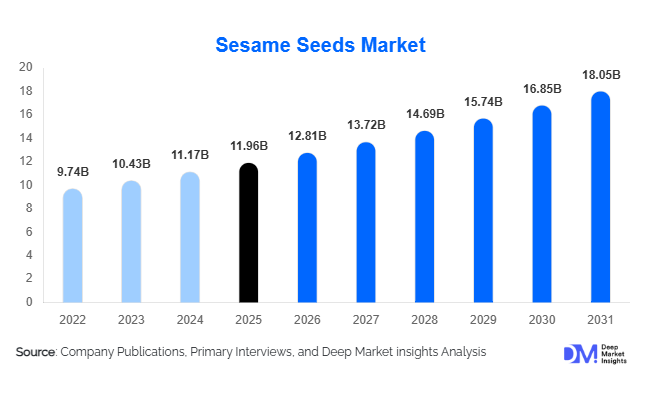

According to Deep Market Insights, the global sesame seeds market size was valued at USD 11.96 billion in 2025 and is projected to grow from USD 12.81 billion in 2026 to reach USD 18.05 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The sesame seeds market growth is primarily driven by rising global demand for functional food ingredients, increasing adoption of plant-based nutrition, expanding bakery and confectionery industries, and growing consumption of healthy edible oils across both developed and emerging economies.

Key Market Insights

- Food and beverage applications dominate global sesame demand, accounting for the majority of consumption across bakery, snacks, confectionery, sauces, and edible oils.

- White sesame seeds remain the leading product category, supported by strong demand from bakery manufacturers, tahini processors, and packaged food companies.

- Asia-Pacific dominates the global sesame seeds market, led by China, India, Japan, and South Korea due to high consumption and strong processing industries.

- Organic and traceable sesame products are witnessing accelerated growth, particularly across Europe and North America due to clean-label food trends.

- African producing nations are becoming strategically important suppliers, with Sudan, Ethiopia, Nigeria, and Tanzania expanding export-oriented sesame cultivation.

- Advanced processing technologies, including steam sterilization, AI-enabled optical sorting, and blockchain traceability, are reshaping global sesame trade and food safety standards.

Sesame Seeds Market Latest Trends

Growing Demand for Plant-Based and Functional Foods

The rapid expansion of plant-based nutrition and functional food categories is significantly increasing the use of sesame seeds across global food manufacturing. Consumers are increasingly seeking natural ingredients rich in protein, healthy fats, calcium, antioxidants, and dietary fiber, positioning sesame as a highly attractive ingredient in vegan and wellness-oriented food products. Sesame-based ingredients such as tahini, sesame milk, sesame butter, cold-pressed oils, and protein-rich snack coatings are becoming mainstream in developed economies. Food companies are integrating sesame into fortified snacks, energy bars, dairy alternatives, and plant-based meat formulations to improve nutritional profiles and enhance texture. The growing popularity of Mediterranean, Middle Eastern, Korean, and Japanese cuisines is also increasing sesame consumption globally, particularly among younger consumers seeking authentic international food experiences.

Technology-Led Modernization of Sesame Processing

The sesame industry is increasingly adopting advanced processing technologies to improve food safety, export quality, and operational efficiency. Steam sterilization systems, optical sorting technologies, AI-enabled grading platforms, and automated packaging systems are becoming essential investments for exporters targeting premium markets such as Europe, Japan, and North America. Blockchain-based traceability systems are also gaining traction, allowing buyers to track product origin, farming practices, and contamination controls throughout the supply chain. This modernization trend is particularly important as regulatory authorities continue to tighten standards related to pesticide residues, salmonella contamination, and microbial safety. Digital procurement systems and direct farmer sourcing models are further improving supply consistency while reducing quality risks across fragmented agricultural networks.

Sesame Seeds Market Drivers

Expansion of the Global Bakery and Processed Food Industry

The continued growth of the global bakery and processed food industries remains a major driver for the sesame seeds market. Sesame seeds are extensively used in burger buns, artisan breads, crackers, cookies, confectionery items, and snack coatings due to their flavor profile, texture enhancement, and nutritional value. Rising urbanization, increasing disposable income, and growing demand for convenient packaged foods are accelerating bakery consumption across Asia-Pacific, Latin America, and the Middle East. Premium bakery chains and foodservice operators are also increasing the use of sesame toppings and sesame-based spreads to cater to evolving consumer preferences for gourmet and health-oriented products. The rapid expansion of organized retail and quick-service restaurant chains further supports demand growth.

Rising Consumer Preference for Healthy Oils and Natural Ingredients

Consumers globally are increasingly prioritizing healthier cooking oils and minimally processed food ingredients. Sesame oil, known for its antioxidant properties and heart-health benefits, is witnessing growing popularity in both household cooking and industrial food applications. Simultaneously, sesame seeds are gaining traction as natural ingredients in functional foods due to their high mineral content and clean-label appeal. Manufacturers are reformulating products to eliminate artificial additives while incorporating nutrient-dense seeds and grains. This trend is particularly strong across North America and Europe, where clean-label food purchasing has become a major consumer behavior driver.

Sesame Seeds Market Restraints

Price Volatility and Climate Dependency

The sesame seeds market remains highly vulnerable to climatic fluctuations and agricultural instability. Sesame cultivation is concentrated in regions that are often exposed to droughts, irregular rainfall, pest outbreaks, and geopolitical uncertainty. African producing countries such as Sudan and Ethiopia, which contribute substantially to global exports, frequently face production disruptions due to environmental and political factors. Since sesame farming is largely dominated by smallholder agriculture, supply consistency remains challenging for large international buyers. These supply uncertainties contribute to raw material price volatility, affecting profitability across the value chain.

Stringent Food Safety and Regulatory Compliance Challenges

Increasing food safety scrutiny from international regulatory agencies remains a major challenge for market participants. Sesame products have faced multiple recalls globally due to contamination issues involving salmonella and pesticide residues. Importing regions such as the European Union, the United States, and Japan continue to enforce stricter food safety standards, increasing compliance costs for exporters and processors. Smaller suppliers lacking advanced sterilization systems, laboratory testing infrastructure, and traceability capabilities may struggle to access premium international markets. Compliance with certifications such as HACCP, ISO 22000, BRC, organic standards, and non-GMO verification is becoming increasingly critical for competitive participation.

Sesame Seeds Industry Key Opportunities

Growth of Organic and Premium Sesame Products

The increasing consumer preference for organic, traceable, and sustainably sourced food ingredients presents a significant growth opportunity within the sesame seeds market. Organic sesame products are witnessing particularly strong demand across Europe and North America as consumers prioritize pesticide-free and clean-label foods. Premium black sesame varieties are also gaining popularity due to their perceived antioxidant benefits and increasing use in nutraceutical products. Food manufacturers are actively seeking suppliers capable of offering certified organic sesame ingredients with stable quality standards and traceable sourcing networks. This trend is creating opportunities for vertically integrated suppliers and export-oriented processors to secure higher profit margins through premium product positioning.

Expansion of Export-Oriented Processing Infrastructure

Major sesame-producing countries are increasingly investing in export-focused processing capabilities to improve competitiveness within global trade markets. Governments and private companies across Ethiopia, India, Nigeria, and Sudan are expanding investments in cleaning facilities, steam sterilization plants, warehouse infrastructure, and automated sorting technologies. These investments enable suppliers to meet increasingly stringent food safety requirements in developed markets while moving up the value chain from raw commodity exports toward value-added ingredient processing. The expansion of direct sourcing programs and contract farming models is also improving supply consistency and helping processors secure long-term partnerships with multinational food manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.96 Billion |

| Market Size in 2026 | USD 12.81 Billion |

| Market Size in 2031 | USD 18.05 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Raw sesame seeds continue to dominate the global market, accounting for nearly 46% of overall market value due to extensive demand from edible oil extraction, bakery manufacturing, and industrial food processing applications. Their lower processing costs and broad usability make them the preferred product category among large-scale food manufacturers. Processed sesame seeds, including roasted and toasted variants, are witnessing rapid growth as demand increases for ready-to-use ingredients in premium snacks, packaged foods, and restaurant applications. Sesame-based ingredient products such as tahini paste and sesame powders are also gaining traction within plant-based and functional food categories. Increasing use of flavored sesame toppings and premium bakery-grade sesame varieties is further supporting product diversification across global food industries.

Application Insights

The food and beverage industry represents the largest application segment, accounting for approximately 72% of global sesame seeds demand. Bakery and confectionery products remain the dominant consumption category due to widespread use of sesame toppings, fillings, coatings, and flavoring ingredients. Edible oil processing is another major application area, particularly across Asia-Pacific and Middle Eastern markets where sesame oil is widely used in cooking and traditional foods. Nutraceutical and dietary supplement applications are expanding rapidly as sesame-derived oils, powders, and antioxidant-rich black sesame ingredients gain popularity within wellness-focused products. Cosmetics and personal care applications are emerging as a niche but fast-growing segment, driven by increasing use of sesame oil in skincare, haircare, soaps, and massage formulations.

Distribution Channel Insights

Business-to-business (B2B) distribution channels dominate the sesame seeds market, accounting for nearly 67% of total global sales. Large food manufacturers, bakery companies, edible oil processors, and ingredient suppliers rely heavily on long-term procurement contracts to stabilize sourcing and maintain quality consistency. Industrial ingredient distributors continue to play a major role in supplying bulk sesame products to multinational food companies. Meanwhile, retail and direct-to-consumer channels are growing steadily, particularly for organic, premium, and packaged sesame products sold through supermarkets, specialty health stores, and e-commerce platforms. Online retail channels are increasingly important for premium sesame oils, black sesame products, and value-added health-focused consumer offerings.

End-Use Industry Insights

The food processing industry remains the largest end-use segment, accounting for approximately 49% of global market revenue in 2025. Rising consumption of packaged foods, convenience snacks, bakery products, and ready-to-eat meals continues to support strong demand for sesame ingredients globally. The bakery industry remains highly dependent on sesame for premium bread products, burger buns, crackers, and confectionery applications. The nutraceutical industry is emerging as one of the fastest-growing end-use sectors due to increasing incorporation of sesame proteins, oils, and antioxidant-rich black sesame ingredients into functional foods and dietary supplements. The cosmetics and personal care sector is also witnessing growing adoption of sesame oil in organic skincare and wellness products, creating additional long-term demand opportunities beyond traditional food applications.

Explore more data points, trends and opportunities Download Free Sample Report

Sesame Seeds Market Segmentations

By Product Type

- Raw Sesame Seeds

- Processed Sesame Seeds

- Sesame-Based Ingredient Products

By Seed Color

- White Sesame Seeds

- Black Sesame Seeds

- Brown Sesame Seeds

- Golden Sesame Seeds

- Mixed & Specialty Sesame Seeds

By Nature

- Conventional Sesame Seeds

- Organic Sesame Seeds

- Non-GMO Sesame Seeds

- Fair-Trade Certified Sesame Seeds

By Application

- Food & Beverage

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

- Pharmaceutical Applications

- Animal Feed & Pet Nutrition

By Distribution Channel

- Business-to-Business (B2B)

- Supermarkets & Hypermarkets

- Specialty Organic Stores

- Convenience Stores

- Online Retail Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global sesame seeds market, accounting for nearly 43% of total market share in 2025. China remains the largest consumer globally due to extensive demand from edible oil processing, bakery products, snacks, and traditional food industries. The country also imports large volumes of sesame seeds from African nations to support domestic processing demand. India represents another major market due to strong domestic consumption of sesame-based sweets, oils, snacks, and export-oriented processing industries. Japan and South Korea continue to import high-quality sterilized sesame products for premium packaged foods, restaurant chains, and health-oriented applications. Rapid urbanization and rising packaged food consumption across Southeast Asia further strengthen regional demand growth.

Europe

Europe accounted for approximately 24% of the global sesame seeds market in 2025, supported by rising demand for clean-label bakery products, vegan foods, and ethnic cuisines. Germany remains the leading European market due to its large bakery industry and strong consumer preference for healthy and natural ingredients. The Netherlands serves as a major import and redistribution hub for sesame products across the European Union. France, the United Kingdom, and Poland are also witnessing growing demand for sesame-based snacks, organic spreads, and plant-based foods. Europe continues to experience strong growth in organic and traceable sesame products due to stringent food safety regulations and sustainability-focused consumer preferences.

North America

North America represented nearly 16% of global sesame seeds market revenue in 2025, led primarily by the United States. Strong demand for bakery products, healthy snacks, tahini spreads, hummus, and plant-based foods continues to support regional market growth. Consumers increasingly prefer organic, non-GMO, and clean-label sesame products, driving higher adoption of premium and specialty varieties. Canada is also witnessing growing demand for sesame ingredients in natural and wellness-focused packaged food categories. Expanding Asian and Middle Eastern cuisine consumption further contributes to increasing regional demand.

Latin America

Latin America is emerging as a developing market for sesame products, with Brazil and Argentina leading regional demand growth. Increasing urbanization, expansion of modern retail channels, and growing awareness of healthy food ingredients are supporting market expansion. Demand is particularly strong for bakery applications, healthy snacks, and vegetable oil alternatives. Several countries are also increasing sesame cultivation to support export opportunities and diversify agricultural revenues.

Middle East & Africa

The Middle East and Africa region remains strategically important due to its dual role as both a major producer and consumer of sesame products. Sudan and Ethiopia continue to rank among the world’s leading sesame exporters due to favorable climatic conditions and increasing cultivation acreage. Turkey remains one of the largest consumption markets in the region due to strong use of sesame in tahini, bakery products, confectionery, and traditional cuisine. Gulf countries including the UAE and Saudi Arabia continue to import significant volumes of sesame for food processing and hospitality industries. Africa is expected to remain one of the fastest-growing supplier regions globally due to increasing export infrastructure investments and international demand for high-quality sesame products.

Key Players in the Sesame Seeds Market

- Olam Group

- ETG (Export Trading Group)

- Dipasa Group

- Tradin Organic Agriculture

- Virdhara International

- Shyam Industries

- SunOpta Inc.

- Selet Hulling PLC

- Gansu Dunhuang Seed Group

- Humera Sesame PLC

- Fuji Oil Holdings

- Archer Daniels Midland (ADM)

- Bunge Global

- McCormick & Company

- Unicorn Ingredients Limited