Pretzel Salts Market Size

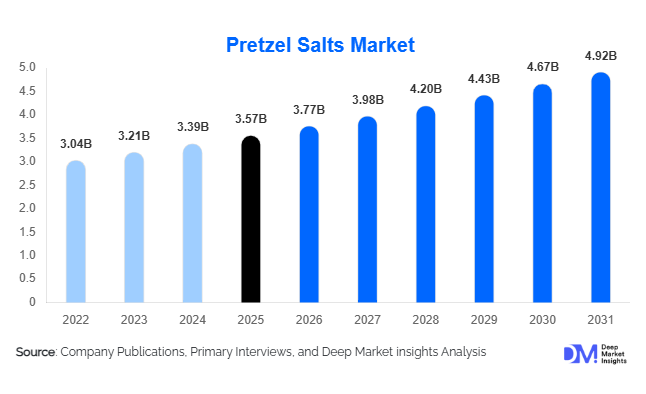

According to Deep Market Insights, the global pretzel salts market size was valued at USD 3.57 billion in 2025 and is projected to grow from USD 3.77 billion in 2026 to reach USD 4.92 billion by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The pretzel salts market growth is primarily driven by the increasing consumption of savory snacks, expanding commercial bakery production, and rising demand for premium bakery ingredients that enhance product appearance, texture, and flavor. Pretzel salt remains a critical specialty ingredient for soft pretzels, hard pretzels, artisan bakery products, and selected snack applications, owing to its unique crystal structure and baking stability.

Key Market Insights

- Demand for premium and specialty bakery ingredients is increasing globally, driving the adoption of customized pretzel salt crystal formats across industrial and artisan bakeries.

- Low-sodium pretzel salt formulations are gaining traction as food manufacturers seek compliance with sodium reduction regulations while maintaining product taste and appearance.

- North America dominates the global pretzel salts market, supported by the region's mature pretzel manufacturing industry and strong snack consumption culture.

- Asia-Pacific is the fastest-growing regional market, driven by the expansion of organized bakery chains, rising disposable incomes, and increasing consumption of Western-style snacks.

- Vacuum-evaporated pretzel salts account for the largest production share, owing to their superior purity, consistency, and performance in commercial baking operations.

- Technological advancements in crystal engineering and particle design are enabling manufacturers to develop premium, low-sodium, and customized pretzel salt solutions.

Pretzel Salts Market Latest Trends

Premiumization of Bakery and Snack Products

The global bakery and snack industries are increasingly embracing premiumization strategies to differentiate products in competitive retail environments. Pretzel manufacturers are adopting specialty salt varieties with unique crystal structures, mineral compositions, and visual characteristics to enhance product quality and consumer appeal. Premium pretzels featuring artisanal ingredients, gourmet flavors, and visually distinctive salt crystals are commanding higher retail prices and generating stronger margins for producers. This trend is particularly visible across North America and Europe, where consumers increasingly associate specialty ingredients with product authenticity, craftsmanship, and superior taste experiences.

Expansion of Low-Sodium Pretzel Salt Solutions

Growing health awareness and government-led sodium reduction initiatives are driving innovation in low-sodium pretzel salts. Manufacturers are investing in advanced crystal engineering technologies that optimize flavor delivery while reducing overall sodium content. Enhanced dissolution characteristics, modified particle sizes, and mineral-enriched formulations are enabling bakery companies to maintain taste perception while meeting nutritional targets. The trend is expected to accelerate as regulatory scrutiny surrounding sodium consumption increases across developed markets.

Pretzel Salts Market Drivers

Growing Global Consumption of Savory Snacks

The continued expansion of the global savory snacks industry remains one of the strongest growth drivers for the pretzel salts market. Consumers increasingly prefer convenient, portable, and shelf-stable snack products, supporting rising production volumes of pretzels and baked snack alternatives. Pretzels are often perceived as a healthier alternative to fried snacks, further boosting their popularity among health-conscious consumers. This trend directly increases demand for specialty pretzel salts used in product manufacturing.

Expansion of Commercial Bakery Production

Rapid urbanization, changing lifestyles, and increasing demand for packaged bakery products are fueling commercial bakery expansion worldwide. Large-scale bakery manufacturers require highly consistent ingredients to ensure uniform product quality and appearance. Pretzel salts provide superior adhesion, moisture resistance, and baking performance compared to conventional food-grade salts, making them indispensable for industrial baking applications. The growth of frozen bakery products and ready-to-eat snack categories is further strengthening market demand.

Pretzel Salts Market Restraints

Sodium Reduction Regulations and Health Concerns

Governments and public health organizations continue implementing sodium reduction targets and nutritional labeling requirements. While these initiatives create opportunities for low-sodium innovation, they may also reduce traditional salt consumption volumes and increase research and development costs for manufacturers. Compliance with evolving regulations requires continuous product reformulation and investment in alternative salt technologies.

Energy and Raw Material Cost Volatility

Pretzel salt production depends heavily on energy-intensive evaporation, processing, and packaging operations. Fluctuations in energy prices, transportation costs, and industrial operating expenses can significantly impact manufacturing profitability. Rising utility costs have become particularly challenging for producers operating in highly competitive markets where pricing flexibility remains limited.

Pretzel Salts Industry Key Opportunities

Emerging Market Expansion Across Asia-Pacific

Asia-Pacific presents substantial growth opportunities for pretzel salt manufacturers due to rapidly expanding bakery industries, increasing disposable incomes, and growing consumption of Western-style snacks. Countries such as China, India, Indonesia, and Vietnam are witnessing significant investments in commercial bakery infrastructure and modern retail channels. Establishing localized manufacturing facilities and distribution networks can help suppliers capture emerging demand while reducing logistics costs and supply chain risks.

Development of Functional and Mineral-Enriched Pretzel Salts

The growing consumer preference for healthier and value-added food ingredients creates opportunities for mineral-enriched and functional pretzel salt formulations. Manufacturers can develop specialty products incorporating potassium, magnesium, and trace minerals while maintaining desirable taste and texture characteristics. Such innovations align with clean-label trends and allow food producers to market premium products with enhanced nutritional profiles. These solutions are expected to gain traction among both bakery manufacturers and health-focused snack brands.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.57 Billion |

| Market Size in 2026 | USD 3.77 Billion |

| Market Size in 2031 | USD 4.92 Billion |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Natural pretzel salt continues to dominate the global market, contributing approximately 58% of total market revenue in 2025. The leadership of this segment is strongly driven by accelerating consumer preference for clean-label, minimally processed, and transparently sourced food ingredients. Industrial bakery manufacturers are increasingly aligning with natural salt formulations as they support premium product positioning, regulatory compliance expectations, and evolving food safety standards across major developed markets. The growing emphasis on ingredient authenticity in packaged snacks and artisan bakery goods further reinforces demand stability for natural variants, making them the foundational product type within the global pretzel salts ecosystem.Low-sodium pretzel salts represent the fastest-growing product category, primarily driven by rising global health awareness and reformulation initiatives among food manufacturers targeting sodium reduction commitments. This growth is further supported by regulatory pressures in multiple regions and the increasing adoption of healthier snacking habits among urban consumers. Mineral-enriched and organic-certified pretzel salts are also expanding steadily within premium bakery and specialty snack applications, where differentiation, nutritional enhancement, and premiumization strategies allow manufacturers to command higher price points and strengthen brand positioning in competitive retail environments.

Crystal Structure Insights

Compressed pretzel salt crystals account for the largest market share, representing approximately 46% of global consumption. The dominance of this segment is primarily driven by its superior adhesion properties, structural stability during high-temperature baking, and consistent performance in large-scale industrial production environments. These characteristics make compressed crystals the preferred choice for commercial pretzel manufacturers seeking uniform product appearance, reduced wastage, and efficient processing integration within automated baking systems.Coarse granular salts continue to maintain relevance in traditional and artisanal pretzel production, where texture authenticity and heritage baking practices remain important. Flake salts are gaining traction in premium bakery applications due to their distinctive visual appeal, delicate crunch, and enhanced sensory perception, which align with evolving consumer expectations for gourmet snack experiences. Additionally, customized crystal formats are emerging as a niche but strategically important segment, enabling manufacturers to differentiate products through proprietary textures and targeted sensory profiles that support brand innovation and product segmentation strategies.

Application Insights

Soft pretzels represent the largest application segment, accounting for nearly 34% of total pretzel salt demand. The leadership of this category is driven by strong consumption across foodservice channels, including quick-service restaurants, stadium concessions, cafés, and convenience retail formats, where soft pretzels remain a high-margin, high-frequency snack offering. The consistent demand from on-the-go consumption and experiential dining formats further strengthens the segment’s dominance within the broader application landscape.Hard pretzels represent a mature but stable application area, supported by strong packaged snack penetration and long shelf-life advantages that align with retail distribution models. Beyond traditional pretzel applications, pretzel salts are increasingly being incorporated into artisan breads, bagels, crackers, frozen bakery products, and seasoning blends. This diversification is driven by food manufacturers seeking to enhance texture contrast, visual appeal, and flavor complexity, particularly in premium and specialty food categories where differentiated ingredient usage contributes to product innovation and consumer engagement.

Distribution Channel Insights

Direct business-to-business sales remain the dominant distribution channel, accounting for approximately 41% of global revenue. This leadership is driven by long-term contractual relationships between large-scale food manufacturers and ingredient suppliers, ensuring consistent quality standards, supply reliability, and cost efficiency in high-volume production environments. The integration of procurement systems within industrial bakery operations further strengthens the importance of direct supply arrangements.Bakery ingredient distributors play a critical role in serving small and medium-sized bakery operators that require flexible order quantities and diversified ingredient access. Foodservice suppliers continue to support demand from restaurants, institutional kitchens, and catering services, where operational efficiency and rapid fulfillment are essential. Meanwhile, retail and e-commerce channels are expanding at a steady pace, supported by rising consumer interest in artisan baking, home cooking trends, and premium specialty salts, which are increasingly positioned as experiential culinary ingredients in digital marketplaces.

End-User Insights

Industrial pretzel manufacturers represent the largest end-user segment, accounting for nearly 38% of total market demand. Their dominance is driven by large-scale production requirements, standardized quality expectations, and the need for specialized salt formulations that ensure consistent baking performance, visual uniformity, and process efficiency. The scale-driven nature of this segment makes it the primary anchor of global pretzel salt consumption.Commercial bakeries constitute the second-largest end-user group, supported by increasing demand for premium baked goods and artisan-style products that emphasize texture, appearance, and ingredient transparency. Snack manufacturers are emerging as the fastest-growing end-user category, fueled by continuous product innovation, expansion of flavored snack portfolios, and the incorporation of pretzel salts into crackers, baked snacks, and hybrid snack formats. Foodservice operators and quick-service restaurants also contribute significantly to market growth, driven by menu diversification strategies and the rising popularity of pretzel-based offerings in casual dining and grab-and-go segments.

Explore more data points, trends and opportunities Download Free Sample Report

Pretzel Salts Market Segmentations

By Product Type

- Natural Pretzel Salt

- Iodized Pretzel Salt

- Low-Sodium Pretzel Salt

- Mineral-Enriched Pretzel Salt

- Organic Certified Pretzel Salt

By Crystal Structure / Form

- Compressed Pretzel Salt Crystals

- Coarse Granular Pretzel Salt

- Flake Pretzel Salt

- Cubic Crystal Pretzel Salt

- Specialty Custom-Shaped Pretzel Salt

By Source

- Vacuum-Evaporated Salt

- Sea Salt-Based Pretzel Salt

- Rock Salt-Based Pretzel Salt

- Solar-Evaporated Salt

By Application

- Soft Pretzels

- Hard Pretzels

- Bread & Rolls

- Bagels

- Crackers & Snack Bakery Products

- Frozen Bakery Products

- Foodservice Bakery Preparations

- Seasoning Blends

- Meat & Processed Food Applications

By Distribution Channel

- Direct B2B Sales to Food Manufacturers

- Bakery Ingredient Distributors

- Foodservice Suppliers

- Retail Stores

- Specialty Food Stores

- E-commerce Platforms

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 38% of global pretzel salts demand in 2025. The region’s leadership is primarily driven by a highly developed pretzel manufacturing industry, strong penetration of packaged snack foods, and a well-established foodservice ecosystem that continuously integrates savory baked products into mainstream consumption. The United States alone contributes nearly 31% of worldwide consumption, supported by large-scale industrial bakery operations, strong retail snack demand, and continuous product innovation from both established brands and private label manufacturers.Growth in the region is further supported by increasing consumer inclination toward premium, artisanal, and clean-label bakery products, along with sustained demand for convenient snacking formats. Canada contributes additional demand through expanding commercial bakery production and packaged snack manufacturing, with both markets benefiting from robust distribution infrastructure and high consumer spending on processed food categories.

Europe

Europe accounts for approximately 29% of global market demand, with Germany leading regional consumption due to its deep-rooted pretzel tradition and highly advanced bakery manufacturing ecosystem. The region’s growth is strongly driven by cultural affinity for baked snack products combined with increasing demand for clean-label, organic, and sustainably sourced ingredients across food categories.The United Kingdom, France, Italy, and Spain collectively contribute significant demand, supported by expanding premium bakery segments and growing interest in artisanal snack products. The regional market is further reinforced by strong regulatory emphasis on ingredient transparency and food quality standards, which encourages the adoption of high-quality specialty salts in both industrial and artisanal applications. Rising consumer preference for gourmet bakery experiences continues to support steady expansion across retail and foodservice channels.

Asia-Pacific

Asia-Pacific represents approximately 22% of global demand and is the fastest-growing regional market, projected to expand at a CAGR exceeding 6.5% through 2031. The region’s growth is primarily driven by rapid urbanization, expanding middle-class populations, and increasing Westernization of dietary habits, particularly in urban centers.China leads regional consumption due to the rapid expansion of its bakery industry and increasing adoption of Western-style snack products, supported by strong retail modernization and e-commerce penetration. India is emerging as a high-growth market, driven by rising disposable incomes, evolving food preferences, and expansion of organized retail and quick-service restaurant networks. Japan, South Korea, and Australia contribute stable demand for premium bakery ingredients, with growth supported by innovation in snack formats and increasing demand for high-quality, differentiated food products.

Latin America

Latin America contributes approximately 6% of global pretzel salts demand. The region’s growth is primarily driven by increasing urbanization, rising consumption of packaged snacks, and gradual expansion of modern retail infrastructure. Brazil leads regional demand, followed by Mexico and Argentina, supported by expanding bakery industries and growing consumer interest in convenience-oriented food products.The market is further supported by increasing penetration of international snack brands and rising disposable incomes in urban populations, which are driving demand for premium and processed bakery offerings. Expansion of foodservice channels and growing adoption of Western-style baked snacks continue to strengthen long-term growth prospects across the region.

Middle East & Africa

The Middle East and Africa collectively account for approximately 5% of global market demand. Growth in this region is driven by rapid expansion of the foodservice sector, increasing tourism activity, and rising investments in food manufacturing infrastructure. The United Arab Emirates and Saudi Arabia serve as key consumption hubs due to strong hospitality industries and high demand for imported premium bakery products.South Africa also plays a significant role in regional consumption, supported by a growing bakery sector and expanding retail penetration. Overall, increasing urbanization, rising disposable incomes, and growing exposure to international food trends are contributing to steady market development, while imports of specialty bakery ingredients continue to support product availability and category expansion.

Key Players in the Pretzel Salts Market

- Cargill

- Compass Minerals

- Morton Salt

- K+S AG

- Tata Chemicals

- SaltWorks

- Maldon Salt Company

- Windsor Salt

- AkzoNobel Salt

- Südwestdeutsche Salzwerke AG

- San Francisco Salt Company

- Sea Salt Superstore

- Murray River Salt

- Pyramid Salt

- Alaska Pure Sea Salt