Prescription Dog Food Market Size

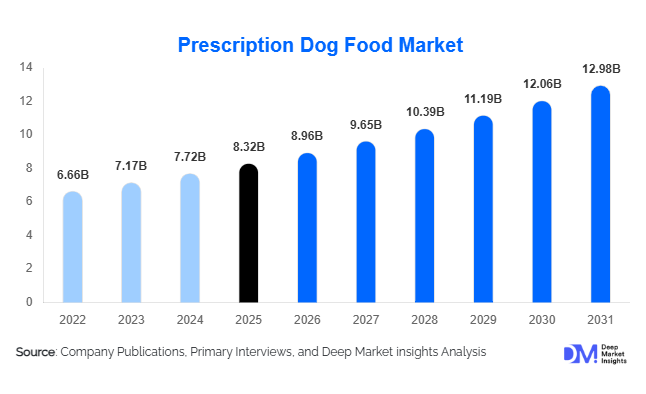

According to Deep Market Insights, the global prescription dog food market size was valued at USD 8.32 billion in 2025 and is projected to grow from USD 8.96 billion in 2026 to reach USD 12.98 billion by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The prescription dog food market growth is primarily driven by the rising prevalence of chronic diseases among companion dogs, increasing pet humanization trends, growing veterinary healthcare expenditure, and expanding awareness regarding the role of therapeutic nutrition in disease management. Veterinary-prescribed diets are increasingly becoming a critical component of treatment plans for conditions such as gastrointestinal disorders, obesity, diabetes, kidney disease, urinary tract disorders, food allergies, and age-related health complications. As pet owners continue to prioritize preventive healthcare and long-term wellness for companion animals, demand for clinically formulated therapeutic diets is expected to witness sustained growth globally.

Key Market Insights

- Gastrointestinal therapeutic diets remain the largest category, accounting for nearly 24% of global prescription dog food demand due to the high incidence of digestive disorders in companion dogs.

- Dry prescription dog food dominates product consumption, representing approximately 63% of market revenue because of its convenience, affordability, and suitability for long-term disease management.

- North America dominates the global prescription dog food market, supported by advanced veterinary infrastructure, high pet healthcare spending, and strong adoption of premium therapeutic nutrition.

- Asia-Pacific is the fastest-growing regional market, driven by rising pet ownership, expanding veterinary services, and increasing disposable incomes across China, India, and Southeast Asia.

- Veterinary clinics and hospitals remain the leading distribution channel, accounting for nearly 48% of global sales owing to veterinarian-led product recommendations.

- Innovation in microbiome-focused nutrition, hydrolyzed proteins, and personalized veterinary diets is creating new growth opportunities for manufacturers globally.

Prescription Dog Food Market Latest Trends

Personalized Veterinary Nutrition Gaining Momentum

The prescription dog food industry is increasingly moving toward personalized therapeutic nutrition solutions. Advances in canine genetics, microbiome science, and veterinary diagnostics are enabling manufacturers to develop disease-specific formulations tailored to individual health profiles. Veterinary professionals are recommending customized nutritional interventions based on breed characteristics, age, digestive health, allergy sensitivity, and metabolic requirements. Subscription-based nutrition programs and direct-to-consumer therapeutic feeding platforms are also gaining traction. Companies investing in personalized nutrition technologies are achieving stronger customer retention rates while creating premium pricing opportunities. The trend is particularly visible in North America and Western Europe, where pet owners increasingly seek highly specialized solutions for chronic disease management and preventive care.

Microbiome-Focused and Functional Therapeutic Diets

Gut health has emerged as a major area of innovation within prescription dog food formulations. Manufacturers are incorporating prebiotics, probiotics, postbiotics, omega fatty acids, antioxidants, and digestive enzymes into veterinary diets to improve treatment outcomes. Growing scientific evidence linking gut microbiome health to immune function, digestion, allergy management, and metabolic health is driving adoption of functional nutrition solutions. Therapeutic diets designed to improve gastrointestinal health, skin conditions, and immune resilience are witnessing particularly strong demand. Veterinary practitioners increasingly view nutrition as a complementary treatment strategy that can reduce medication dependency while improving overall canine health outcomes.

Prescription Dog Food Market Drivers

Growing Prevalence of Chronic Health Conditions in Dogs

The increasing incidence of obesity, diabetes, gastrointestinal disorders, kidney disease, urinary tract complications, and food allergies among companion dogs remains one of the strongest drivers for prescription dog food demand. Veterinary studies indicate that obesity alone affects a significant percentage of pet dogs globally, creating long-term health complications that require specialized nutritional management. Therapeutic diets are increasingly prescribed as first-line interventions for disease control and symptom management. As diagnosis rates continue to improve through advanced veterinary screening technologies, demand for condition-specific nutrition is expected to increase substantially throughout the forecast period.

Rising Pet Humanization and Healthcare Spending

Pet owners increasingly consider dogs as family members and are willing to spend more on preventive healthcare and premium nutrition. The growing willingness to invest in specialized diets, advanced veterinary treatments, and wellness programs is significantly expanding the addressable market for prescription nutrition products. Premiumization trends are particularly strong in developed economies where consumers prioritize long-term health outcomes over product cost considerations. This shift in consumer behavior has enabled manufacturers to introduce scientifically validated therapeutic products with higher profit margins and recurring revenue streams.

Expansion of Veterinary Healthcare Infrastructure

The growing number of veterinary hospitals, specialty clinics, and referral centers worldwide is increasing disease diagnosis rates and strengthening therapeutic diet adoption. Veterinary professionals play a critical role in prescribing and monitoring prescription nutrition programs. Improvements in diagnostic capabilities, preventive screening, and chronic disease management protocols have elevated nutrition from a supplementary treatment to an essential component of veterinary care. Emerging markets are also witnessing rapid expansion in veterinary healthcare infrastructure, creating significant opportunities for prescription dog food manufacturers.

Prescription Dog Food Market Restraints

Premium Product Pricing and Affordability Challenges

Prescription dog food products typically command significantly higher prices than conventional pet food due to specialized ingredients, research investments, and clinical validation requirements. In many developing economies, affordability remains a key barrier limiting widespread adoption. Economic uncertainty, inflationary pressures, and fluctuations in disposable income can impact purchasing decisions, particularly among middle-income households. Manufacturers must balance product efficacy with pricing competitiveness to expand penetration into emerging markets.

Complex Regulatory and Veterinary Compliance Requirements

Prescription dog food products are subject to stringent regulatory standards related to nutritional composition, ingredient sourcing, product claims, labeling, and veterinary oversight. Compliance requirements vary across countries and regions, creating challenges for multinational manufacturers. Product approval timelines, clinical validation requirements, and evolving regulatory frameworks can increase commercialization costs and delay market entry. Maintaining compliance while continuously innovating remains a significant challenge for industry participants.

Prescription Dog Food Industry Key Opportunities

Expansion Across Emerging Asia-Pacific Markets

Asia-Pacific presents one of the largest untapped growth opportunities for prescription dog food manufacturers. Rising pet ownership, increasing urbanization, growing disposable incomes, and expanding veterinary healthcare infrastructure are accelerating demand for premium pet nutrition products. Countries such as China, India, Indonesia, Thailand, and Vietnam remain significantly underpenetrated compared to North America and Western Europe. Companies establishing localized manufacturing facilities, veterinary partnerships, and educational initiatives can capture substantial market share while benefiting from long-term growth trends. The region's growing middle-class population is expected to drive significant increases in therapeutic pet food consumption over the next decade.

Digital Veterinary Healthcare and Subscription-Based Nutrition

The rapid adoption of tele-veterinary services and digital healthcare platforms is creating new opportunities for prescription dog food distribution. Online consultations allow veterinarians to prescribe therapeutic diets remotely, increasing accessibility and convenience for pet owners. Subscription-based nutrition services are also emerging as an effective customer retention strategy by ensuring continuous product supply and treatment adherence. Integration of veterinary software platforms, mobile health applications, and direct-to-consumer logistics networks is expected to create a more connected pet healthcare ecosystem while generating recurring revenue opportunities for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.32 Billion |

| Market Size in 2026 | USD 8.96 Billion |

| Market Size in 2031 | USD 12.98 Billion |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Therapeutic Indication Insights

The gastrointestinal health segment dominates the global prescription dog food market, accounting for approximately 24% of total revenue in 2025. Its leadership is primarily driven by the rising prevalence of digestive disorders, food intolerances, inflammatory bowel disease, pancreatitis, chronic enteropathies, and gastrointestinal sensitivities among companion dogs. Increasing veterinary emphasis on nutritional intervention as a first-line treatment approach for digestive conditions has further accelerated demand for specialized gastrointestinal formulations. These diets are designed to enhance nutrient absorption, support gut microbiome balance, improve stool quality, and reduce digestive stress, making them a critical component of long-term disease management. As awareness of digestive health continues to increase among pet owners and veterinarians, gastrointestinal prescription diets are expected to maintain their leading position throughout the forecast period.Weight management diets continue to gain substantial traction due to the growing prevalence of canine obesity, which has emerged as one of the most common health concerns among companion animals globally. Rising sedentary lifestyles, overfeeding practices, and increasing pet humanization trends have contributed to higher obesity rates, encouraging demand for calorie-controlled, high-fiber, and metabolically optimized prescription nutrition products.Recovery and critical care diets are witnessing increasing adoption in veterinary hospitals and specialty care facilities. These formulations are widely utilized during post-surgical recovery, trauma management, intensive care treatment, and severe illness rehabilitation. Their ability to provide concentrated nutrition, support immune function, and accelerate recovery outcomes continues to strengthen demand across veterinary healthcare settings.

Product Form Insights

Dry prescription dog food remains the dominant product form, accounting for approximately 63% of global market revenue in 2025. The segment's leadership is driven by its superior affordability, convenience, extended shelf life, ease of storage, and suitability for long-term therapeutic feeding regimens. Dry formulations also offer logistical advantages throughout the supply chain, including lower transportation costs, improved inventory management, and reduced spoilage risks. Furthermore, advances in extrusion technologies and ingredient processing have enabled manufacturers to incorporate increasingly sophisticated therapeutic formulations into dry food products without compromising efficacy, further strengthening market adoption.Semi-moist therapeutic diets serve specialized niche applications by providing improved taste acceptance and feeding convenience for selective eaters. Although their overall market share remains comparatively smaller, ongoing product innovation is supporting gradual adoption in targeted therapeutic categories.Liquid recovery nutrition products are primarily utilized within veterinary hospitals, emergency care facilities, and critical care environments where assisted feeding and rapid nutritional intervention are necessary. Meanwhile, therapeutic treats are emerging as a complementary category that supports treatment compliance, medication administration, behavioral reinforcement, and long-term disease management strategies, creating additional opportunities for market expansion.

Protein Source Insights

Chicken-based prescription diets account for approximately 35% of global demand, making them the leading protein source segment within the prescription dog food market. The segment's dominance is supported by the high digestibility of chicken protein, broad canine acceptance, favorable nutritional profile, cost-effectiveness, and formulation versatility across multiple therapeutic indications. Manufacturers also benefit from well-established supply chains and extensive clinical validation supporting the use of chicken-based ingredients in therapeutic nutrition products.Fish-based prescription diets continue to gain market share due to their rich omega-3 fatty acid content and demonstrated benefits in managing inflammatory conditions, skin disorders, joint health concerns, and cardiovascular support requirements. Growing consumer preference for functional nutrition solutions is further contributing to segment growth.Novel protein formulations incorporating venison, duck, rabbit, kangaroo, and other alternative protein sources are expanding rapidly as veterinarians increasingly prescribe elimination diets for food allergy diagnosis and long-term allergy management. Rising awareness of adverse food reactions among pet owners is creating substantial opportunities within this category.Hydrolyzed protein diets represent one of the fastest-growing segments across the market. Their ability to minimize immune system responses by breaking proteins into smaller components has made them highly effective for managing food hypersensitivities, gastrointestinal disorders, and chronic dermatological conditions. Continued clinical evidence supporting hydrolyzed protein efficacy is expected to sustain strong future growth.

Sales Channel Insights

Veterinary clinics and hospitals remain the leading distribution channel, accounting for nearly 48% of global market revenue in 2025. The segment's dominance is primarily driven by the influential role veterinarians play in diagnosing diseases, prescribing therapeutic nutrition plans, and monitoring treatment outcomes. Since prescription diets are often integrated into comprehensive disease management programs, veterinary recommendations remain a key factor influencing consumer purchasing decisions and brand selection.Pet specialty retailers continue to serve as important replenishment channels for pet owners requiring ongoing access to prescription nutrition products. Their ability to provide specialized product assortments, knowledgeable staff, and convenient retail experiences supports continued demand across both developed and emerging markets.E-commerce platforms represent the fastest-growing sales channel, benefiting from increasing digital adoption, subscription-based purchasing models, competitive pricing, product availability, and convenient home delivery services. The expansion of online veterinary consultations and digital pet healthcare ecosystems is further accelerating channel growth.Direct-to-consumer distribution models are gaining traction among premium manufacturers seeking stronger customer engagement, improved retention rates, and recurring revenue generation. Animal health pharmacies also contribute meaningfully to market distribution, particularly in regions characterized by highly developed veterinary healthcare systems and established prescription fulfillment networks.

Age Group Insights

Adult dogs account for approximately 56% of global prescription dog food demand, making them the largest age-based segment in the market. The segment's leadership is primarily driven by the higher prevalence of obesity, food allergies, gastrointestinal disorders, dermatological conditions, diabetes, and metabolic diseases that commonly emerge during adulthood. As veterinary diagnosis rates continue to improve globally, demand for therapeutic nutrition solutions targeting adult canine health conditions is expected to remain strong.Senior dogs represent one of the fastest-growing age segments due to increasing canine life expectancy and advances in veterinary healthcare. Older dogs frequently require specialized nutritional support for kidney disease, mobility challenges, cognitive decline, cardiac disorders, and immune system maintenance. The expanding senior pet population across developed markets is creating substantial opportunities for manufacturers focused on age-specific therapeutic nutrition.Puppy prescription diets account for a smaller share of overall demand but remain an important category for managing congenital disorders, developmental health conditions, digestive sensitivities, and early-stage nutritional deficiencies. Growing awareness of preventive healthcare and early intervention strategies is expected to support steady demand within this segment over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Prescription Dog Food Market Segmentations

By Therapeutic Indication

- Gastrointestinal Health Diets

- Weight Management Diets

- Renal Care Diets

- Urinary Health Diets

- Dermatology & Allergy Diets

- Diabetes Management Diets

- Hepatic Care Diets

- Joint & Mobility Diets

- Cardiac Care Diets

- Neurological & Cognitive Health Diets

- Recovery & Critical Care Diets

- Multi-condition Therapeutic Diets

By Product Form

- Dry Prescription Dog Food

- Wet/Canned Prescription Dog Food

- Semi-Moist Prescription Dog Food

- Prescription Therapeutic Treats

- Liquid Recovery Nutrition

By Protein Source

- Chicken-Based

- Fish-Based

- Lamb-Based

- Beef-Based

- Novel Protein-Based

- Plant-Based Therapeutic Formulations

By Age Group

- Puppy Prescription Diets

- Adult Dog Prescription Diets

- Senior Dog Prescription Diets

By Sales Channel

- Veterinary Clinics & Hospitals

- Pet Specialty Retail Stores

- E-commerce Platforms

- Direct-to-Consumer Subscription Platforms

- Pharmacy & Animal Health Stores

Regional Insights

North America

North America accounted for approximately 39% of global prescription dog food market revenue in 2025, making it the largest regional market. The United States alone represented nearly 31% of global demand, supported by high pet ownership rates, sophisticated veterinary healthcare infrastructure, extensive availability of specialized nutrition products, and strong consumer willingness to invest in premium pet care solutions. Canada also contributes significantly to regional demand through increasing adoption of clinically formulated veterinary diets and rising expenditure on companion animal health.Regional growth is being driven by the continued humanization of pets, growing awareness of preventive healthcare, increasing prevalence of chronic canine diseases, expanding pet insurance coverage, and higher rates of veterinary consultations. The strong presence of leading prescription pet food manufacturers, advanced veterinary diagnostic capabilities, and growing adoption of personalized nutrition approaches further support long-term market expansion across North America.

Europe

Europe accounted for approximately 28% of global market revenue in 2025, positioning it as the second-largest regional market. Germany, the United Kingdom, France, Italy, and Spain represent the region's largest country-level markets. Strong veterinary healthcare systems, high premium pet food penetration, and increasing pet humanization trends continue to support sustained market growth throughout the region.Regional expansion is driven by rising demand for scientifically validated nutrition solutions, increasing awareness of food allergies and digestive disorders, growing adoption of preventive veterinary care, and strong consumer preference for premium and specialized pet nutrition products. Sustainability considerations, clean-label product preferences, and demand for responsibly sourced ingredients are also influencing purchasing behavior. Furthermore, the increasing utilization of hydrolyzed protein diets and allergy-management formulations across Western Europe continues to create attractive growth opportunities for manufacturers.

Asia-Pacific

Asia-Pacific accounted for approximately 22% of global market revenue in 2025 and represents the fastest-growing regional market, with projected annual growth exceeding 9% during the forecast period. China leads regional demand due to rapid pet ownership growth, rising disposable incomes, and increasing consumer spending on companion animal healthcare. Japan remains a mature market characterized by strong adoption of premium therapeutic nutrition products, while India is emerging as one of the fastest-growing national markets globally.The region's rapid growth is supported by accelerating urbanization, expanding middle-class populations, increasing pet humanization, rising veterinary clinic penetration, growing awareness of disease-specific nutrition, and substantial improvements in pet healthcare infrastructure. The continued expansion of e-commerce platforms, greater availability of premium imported pet foods, and increasing expenditure on preventive pet wellness are further strengthening market development. South Korea and Australia also contribute significantly through high pet care spending and strong demand for advanced therapeutic nutrition products.

Latin America

Latin America is experiencing steady market expansion, led primarily by Brazil, Mexico, and Argentina. Brazil accounts for the largest share of regional demand owing to its substantial companion animal population, growing premium pet food industry, and increasing consumer focus on pet health and wellness. Veterinary healthcare improvements across major urban centers are supporting broader adoption of prescription nutrition products.Regional growth is being driven by rising disposable incomes, increasing pet humanization trends, expanding veterinary service availability, growing awareness of chronic pet health conditions, and greater penetration of premium pet food brands. Although market growth remains comparatively moderate relative to Asia-Pacific, improving economic conditions and rising investment in pet healthcare infrastructure continue to create significant long-term opportunities for manufacturers seeking geographic diversification.

Middle East & Africa

The Middle East & Africa region represents a smaller but increasingly important market for prescription dog food. The United Arab Emirates, Saudi Arabia, and South Africa are among the leading contributors to regional demand, supported by rising pet ownership rates, expanding veterinary healthcare services, and increasing expenditure on premium pet care products.Market growth across the region is being driven by rapid urbanization, improving living standards, growing awareness of pet wellness, expansion of organized pet retail networks, and increasing availability of specialized veterinary nutrition products. Economic diversification initiatives in several Gulf countries, coupled with investments in veterinary healthcare infrastructure and growing acceptance of companion animal ownership, are supporting market development. While overall penetration remains lower than in North America and Europe, rising healthcare awareness and expanding access to advanced pet nutrition solutions are expected to sustain future growth across the region.

Key Players in the Prescription Dog Food Market

- Hill's Pet Nutrition

- Mars Petcare (Royal Canin)

- Nestlé Purina PetCare

- Virbac

- Dechra Veterinary Products

- Affinity Petcare

- Farmina Pet Foods

- Monge & C. S.p.A.

- Wellness Pet Company

- Diamond Pet Foods

- ADM Pet Solutions

- United Petfood

- Partner in Pet Food

- Aller Petfood

- Trovet