Grass Fed Milk Market Size

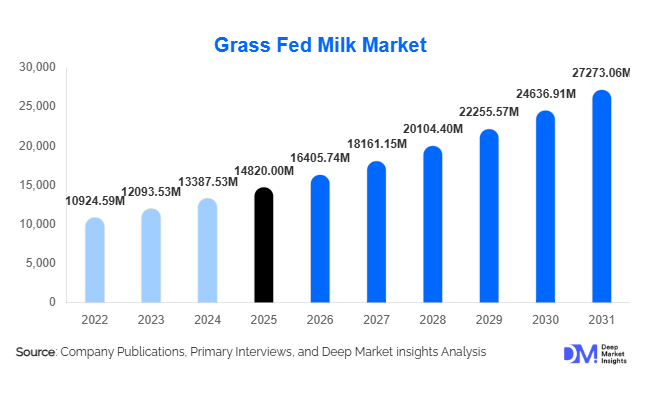

According to Deep Market Insights, the global grass fed milk market size was valued at USD 14,820 million in 2025 and is projected to grow from USD 16,405.74 million in 2026 to reach USD 27,273.06 million by 2031, expanding at a CAGR of 10.7% during the forecast period (2026–2031). Market expansion is primarily driven by rising consumer preference for clean-label dairy products, increasing awareness of animal welfare and sustainable farming practices, and growing demand for nutrient-dense milk products perceived as natural and minimally processed. Grass fed milk is increasingly positioned as a premium dairy category, supported by health-conscious consumers seeking higher omega-3 fatty acids, improved nutritional profiles, and environmentally responsible sourcing.

Key Market Insights

- Premiumization of dairy consumption is accelerating adoption of grass fed milk across developed economies.

- Retail private labels and organic certifications are expanding product accessibility and consumer trust.

- North America dominates global demand, supported by strong organic food penetration and transparent labeling standards.

- Asia-Pacific is the fastest-growing region due to rising disposable income and increasing health awareness.

- E-commerce dairy distribution is improving cold-chain accessibility and subscription-based consumption models.

- Sustainability-driven farming practices are reshaping procurement strategies among dairy processors globally.

What are the latest trends in the grass fed milk market?

Shift Toward Clean-Label and Ethical Dairy

Consumers globally are prioritizing transparency in food sourcing, leading to significant growth in clean-label dairy categories. Grass fed milk aligns strongly with this trend because it emphasizes natural grazing, reduced antibiotic use, and humane livestock management practices. Certifications verifying pasture-based feeding are becoming major purchase drivers, particularly in North America and Europe. Retailers increasingly dedicate shelf space to ethical dairy alternatives, positioning grass fed milk as a premium yet everyday consumable product. Brands are investing in storytelling, farm traceability technologies, and QR-based sourcing transparency to strengthen consumer trust and justify higher price points.

Expansion of Value-Added Dairy Formats

Grass fed milk is no longer limited to fluid milk products. Companies are expanding into grass fed butter, cheese, yogurt, infant nutrition, and protein beverages. This diversification improves margins and stabilizes revenues against raw milk price volatility. Functional dairy products enriched with probiotics and high-protein formulations are attracting fitness-oriented consumers, while lactose-free grass fed variants are gaining traction among urban populations. Innovation across packaging formats, including recyclable cartons and extended shelf-life processing, is enabling wider geographic distribution.

What are the key drivers in the grass fed milk market?

Rising Health Awareness and Nutritional Differentiation

Grass fed milk contains higher levels of omega-3 fatty acids, conjugated linoleic acid (CLA), and fat-soluble vitamins compared with conventional milk. Growing consumer awareness around preventive healthcare and functional nutrition has significantly increased demand for nutritionally differentiated dairy products. Health-focused consumers increasingly view grass fed milk as a natural alternative to fortified dairy beverages, supporting premium pricing and sustained category growth.

Sustainability and Animal Welfare Regulations

Governments and food regulators are encouraging sustainable agricultural practices, indirectly benefiting pasture-based dairy systems. Grass fed dairy farming typically involves lower reliance on intensive feed production and aligns with regenerative agriculture principles. Retailers and multinational food companies are integrating sustainability metrics into sourcing policies, accelerating adoption among dairy cooperatives.

Growth of Organic and Specialty Food Retail Channels

Expansion of specialty grocery chains, organic supermarkets, and online dairy delivery platforms has improved market accessibility. Subscription-based milk delivery models in urban markets are strengthening recurring consumption patterns. Premium dairy brands are leveraging direct-to-consumer channels to enhance margins and consumer engagement.

What are the restraints for the global market?

Higher Production Costs

Grass fed dairy production requires extensive pasture land, seasonal grazing management, and lower herd productivity compared with conventional dairy systems. These factors increase operational costs and retail prices, limiting adoption among price-sensitive consumers in developing markets.

Supply Chain and Certification Challenges

Maintaining verified grass fed standards across regions is complex due to varying certification frameworks and climatic limitations. Seasonal feed shortages and inconsistent pasture availability can affect production stability, creating supply-side constraints for processors and retailers.

What are the key opportunities in the grass fed milk industry?

Expansion in Emerging Asian Markets

Rapid urbanization and rising middle-class populations across China, India, and Southeast Asia present strong opportunities for premium dairy adoption. Consumers in these regions increasingly associate imported and specialty dairy with superior quality and safety standards. Local dairy cooperatives are beginning to transition toward pasture-based farming systems, supported by government initiatives promoting sustainable agriculture.

Integration with Functional Nutrition and Infant Dairy

The infant nutrition and clinical nutrition segments represent high-margin opportunities for grass fed dairy producers. Parents increasingly seek minimally processed and naturally sourced ingredients, creating strong demand for grass fed milk powders and toddler nutrition formulations. Partnerships between dairy processors and nutrition brands are expanding innovation pipelines.

Carbon-Neutral and Regenerative Dairy Branding

Climate-conscious consumers are encouraging companies to adopt regenerative grazing practices. Producers implementing carbon sequestration programs and methane reduction strategies can command premium pricing while qualifying for sustainability incentives and ESG-driven investments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14820 Million |

| Market Size in 2026 | USD 16405.74 Million |

| Market Size in 2031 | USD 27273.06 Million |

| CAGR | 10.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global grass fed milk market is predominantly led by whole grass fed milk, which accounts for approximately 46% of the 2025 market share. This dominance is primarily driven by consumer perception of superior taste, creaminess, and nutritional richness compared to conventional milk. Whole grass fed milk is increasingly preferred by health-conscious consumers who associate it with higher levels of omega-3 fatty acids, vitamins A and E, and conjugated linoleic acid (CLA), which are believed to offer cardiovascular and anti-inflammatory benefits. Premium dairy brands are leveraging these nutritional advantages in their marketing campaigns, reinforcing the product’s value proposition.Organic-certified grass fed milk follows closely, representing nearly 28% of the market. The growth of this segment is fueled by stringent regulatory labeling, rising consumer interest in chemical-free and sustainable farming practices, and the willingness of consumers to pay a premium for certified organic products. Retailers are increasingly positioning these products in specialty organic aisles and promoting them as part of a clean-label and environmentally sustainable lifestyle.Lactose-free grass fed milk is emerging as the fastest-growing niche within the market, driven by rising awareness around digestive health and lactose intolerance. Consumers seeking functional benefits, such as easier digestion and reduced bloating, are adopting these products. Flavored grass fed variants, including chocolate, vanilla, and coffee-infused milk, are gaining traction among younger consumers and millennials, who prefer functional and indulgent beverages that also deliver nutritional benefits.

Application Insights

Household consumption continues to be the leading application segment, contributing nearly 52% of total market demand in 2025. Grass fed milk is increasingly integrated into daily diets, consumed as a standalone beverage, incorporated into coffee and tea, or used in home cooking and baking. This consistent household demand is supported by increasing consumer awareness of the health benefits associated with natural, pasture-raised dairy products.The foodservice sector is expanding rapidly as premium cafés, boutique bakeries, and health-oriented restaurants adopt grass fed milk to differentiate their offerings. The growing trend of “premiumization” in foodservice, coupled with consumer preference for natural and functional ingredients, is driving institutional adoption. Additionally, infant nutrition products and functional beverages represent emerging high-growth applications. Manufacturers are increasingly sourcing grass fed milk to meet clean-label requirements, offering infant formulas and protein-enriched beverages that align with parent and consumer expectations for nutritional safety and functional value.

Distribution Channel Insights

Supermarkets and hypermarkets dominate distribution channels, accounting for approximately 48% of the market. These outlets benefit from strong cold-chain infrastructure, wide consumer reach, and strategic promotional activities. Retailers are increasingly highlighting grass fed milk through dedicated shelf space and point-of-sale marketing to reinforce perceived premium value.Online retail channels are the fastest-growing segment, expanding at double-digit growth rates due to the proliferation of digital grocery platforms and subscription delivery services. Consumers increasingly prefer the convenience of home delivery, particularly for premium and specialty products that may not be widely available in local stores. Specialty organic and health-focused stores continue to hold influence among high-income and premium consumers seeking certified, sustainable, and ethically sourced grass fed products.

End-Use Insights

Retail household consumption remains the dominant end-use segment, reflecting strong daily integration. However, the food processing industry is experiencing the fastest growth, driven by increasing demand for premium dairy ingredients in yogurt, cheese, and protein beverage manufacturing. Grass fed milk’s rich nutrient profile makes it a preferred input for manufacturers aiming to deliver high-quality, functional, and clean-label dairy products.Export-driven demand is also increasing, particularly from Asian markets, which are importing premium dairy products to meet rising urban consumer expectations for health-oriented nutrition. The global functional dairy industry, valued above USD 120 billion, is integrating grass fed milk and dairy ingredients to develop enriched beverages, fortified yogurts, and protein supplements. This integration is expected to drive long-term demand, particularly in segments where consumer willingness to pay for quality and nutrition is high.

Explore more data points, trends and opportunities Download Free Sample Report

Grass Fed Milk Market Segmentations

By Product Type

- Whole Grass Fed Milk

- Semi-Skimmed Grass Fed Milk

- Skimmed Grass Fed Milk

- Organic Certified Grass Fed Milk

- A2 Grass Fed Milk

- Fortified Grass Fed Milk

By Packaging Type

- Carton Packaging

- Glass Bottles

- Plastic Bottles

- Bulk & Institutional Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Specialty & Organic Stores

- Foodservice Distribution Channels

By End Use

- Household/Retail Consumption

- Food & Beverage Processing

- Nutraceuticals & Functional Foods

- Foodservice & Hospitality Industry

Regional Insights

North America

North America accounted for approximately 38% of the global market share in 2025, with the United States leading due to high consumer awareness and well-established pasture-raised dairy practices. U.S. consumers increasingly associate grass fed milk with environmental sustainability, animal welfare, and superior taste. The growth is further supported by regulatory initiatives that promote organic labeling and natural ingredient transparency. Canada demonstrates robust growth, driven by government-backed sustainable agriculture policies, expansion of premium retail networks, and increasing interest in functional and lactose-free dairy products. Consumer education campaigns emphasizing health benefits and farm-to-table sourcing also contribute to regional demand expansion.

Europe

Europe holds nearly 30% market share, with Germany, the United Kingdom, Ireland, and France as leading markets. The European consumer base is increasingly inclined toward clean-label, ethically sourced, and organic dairy products. Ireland’s traditional pasture-based grazing systems serve as a model for large-scale grass fed milk production, influencing broader European dairy practices. Regulatory standards across the EU support product labeling transparency, fostering consumer confidence. Premiumization trends in foodservice, such as organic cafés and boutique dessert shops, further drive uptake of grass fed dairy. Functional beverages and lactose-free milk are experiencing high growth, encouraged by health-conscious consumers seeking alternatives to conventional dairy.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR above 12%. China leads import demand for premium dairy, driven by urbanization, rising disposable incomes, and increasing consumer focus on child nutrition and natural ingredients. India shows notable growth as urban middle-class households adopt higher-protein, natural dairy alternatives to support overall health and immunity. Japan’s growth is propelled by an aging population seeking nutrient-rich, easily digestible dairy options. Australia and New Zealand remain major exporters to Asia-Pacific markets, leveraging well-established grass fed dairy systems and quality certifications that meet regional standards. Expansion of cold-chain infrastructure and retail modernization in Asia-Pacific further support market penetration.

Latin America

Latin America is emerging as a strategic growth region, with Brazil and Argentina benefiting from favorable climate and expansive grazing lands. Improving dairy infrastructure, coupled with growing exports to North America and Europe, strengthens the region’s global participation. Domestic demand is increasing due to urbanization and rising health awareness, with premium retail channels and foodservice establishments integrating grass fed milk to meet consumer expectations. Technological adoption in dairy farming, such as automated milking systems and pasture management tools, is enhancing productivity and milk quality, supporting the region’s competitive position in global trade.

Middle East & Africa

Demand in the Middle East and Africa is rising, particularly in the UAE and Saudi Arabia, where reliance on imported premium dairy products is high due to limited domestic production. Urbanization, increasing disposable incomes, and Western-influenced dietary trends are contributing to the adoption of grass fed milk in both household and foodservice segments. South Africa is emerging as a regional production hub, leveraging abundant pasturelands and progressive farming practices. Investments in cold-chain logistics and retail modernization are enhancing accessibility to premium dairy products, supporting consistent market growth across the region.Overall, the grass fed milk market is witnessing robust growth globally, fueled by health consciousness, premiumization, clean-label trends, and increasing adoption across multiple consumer touchpoints. Regional variations in consumer behavior, infrastructure readiness, and regulatory frameworks create distinct growth drivers, with North America and Europe leading in mature adoption, Asia-Pacific driving high growth, and emerging regions like Latin America and the Middle East & Africa steadily expanding participation. The continued emphasis on functional dairy applications, specialty retail channels, and export-driven demand is expected to sustain long-term market expansion well beyond 2030.

Key Players in the Grass Fed Milk Market

- Arla Foods

- Organic Valley

- Danone S.A.

- Nestlé S.A.

- Fonterra Co-operative Group

- Maple Hill Creamery

- Aurora Organic Dairy

- Lactalis Group

- Yeo Valley Farms

- Clover Sonoma

- Straus Family Creamery

- Horizon Organic

- Emmi Group

- Meiji Holdings Co., Ltd.

- Saputo Inc.