Meat and Bone Meal Market Size

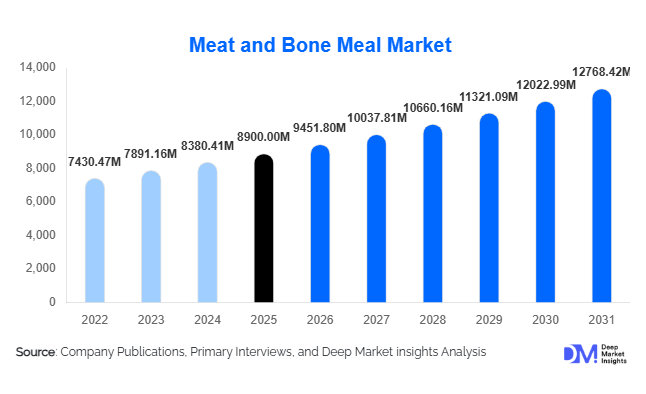

According to Deep Market Insights, the global meat and bone meal market size was valued at USD 8,900 million in 2025 and is projected to grow from USD 9,451.80 million in 2026 to reach USD 12,768.42 million by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The market growth is primarily driven by rising global demand for cost-effective animal protein ingredients, expanding livestock production, and increasing adoption of circular economy practices that convert animal by-products into valuable feed and fertilizer inputs. Growing pressure on feed cost optimization across poultry, swine, and aquaculture industries is further accelerating demand for meat and bone meal as a high-protein, nutrient-rich alternative to conventional feed ingredients such as soybean meal and fish meal.

The market is also benefiting from technological advancements in rendering processes, which have significantly improved product safety, digestibility, and regulatory compliance. In addition, rising meat consumption in emerging economies is boosting slaughterhouse output, ensuring a steady supply of raw materials for MBM production. While regulatory restrictions in certain regions remain a challenge, expanding applications in aquaculture feed, pet food, and organic fertilizers continue to broaden the market scope globally. Overall, the MBM market is positioned as a critical component of sustainable protein sourcing within the global animal nutrition ecosystem.

Key Market Insights

- Animal feed remains the dominant application, accounting for the majority of global meat and bone meal consumption, especially in poultry and swine feed formulations.

- Asia-Pacific leads global demand due to large livestock populations, expanding aquaculture production, and strong feed manufacturing industries in China and India.

- Dry rendering technology dominates production due to efficiency, scalability, and ability to produce pathogen-free output suitable for feed applications.

- Poultry-based meat and bone meal is the leading source segment, supported by rapid expansion of global poultry farming.

- Powdered MBM is the most widely used form, preferred for ease of blending in compound feed formulations.

- Export-driven trade flows are increasing, with North America and Europe supplying MBM to high-demand regions in Asia and the Middle East.

What are the latest trends in the meat and bone meal market?

Expansion of Sustainable Feed Ingredients

The shift toward sustainable animal nutrition is one of the most prominent trends shaping the MBM market. Feed manufacturers are increasingly incorporating meat and bone meal as part of circular economy strategies that reduce reliance on resource-intensive protein sources like fish meal and soybean meal. This trend is especially strong in regions facing feed cost volatility. Governments are also promoting waste-to-value initiatives, encouraging rendering companies to convert animal by-products into safe, high-protein feed ingredients. As sustainability becomes a core purchasing criterion, MBM is gaining wider acceptance in integrated livestock production systems.

Growth in Aquaculture and Pet Food Applications

Aquaculture expansion is driving significant demand for alternative protein sources, and meat and bone meal is increasingly being used in fish feed formulations due to its cost efficiency and nutritional composition. At the same time, the global pet food industry is evolving toward high-protein, nutrient-dense formulations, where MBM is used in controlled, high-quality processing environments. Premiumization trends in pet nutrition are encouraging manufacturers to improve rendering standards, enabling MBM to be used in more value-added applications. This dual expansion in aquaculture and pet food is significantly diversifying demand sources.

What are the key drivers in the meat and bone meal market?

Rising Global Demand for Animal Protein

Increasing consumption of meat, dairy, and seafood is driving global livestock production, which in turn fuels demand for animal feed ingredients. Poultry and swine industries, in particular, require large volumes of cost-effective protein inputs. Meat and bone meal provides a high-protein and mineral-rich solution that supports animal growth while reducing feed formulation costs. Rapid urbanization and dietary shifts in emerging economies are further strengthening livestock production cycles, directly boosting MBM consumption.

Cost Advantage Over Conventional Protein Sources

Fluctuating prices of soybean meal and fish meal have encouraged feed manufacturers to adopt more stable and economical alternatives. Meat and bone meal offers a competitive cost structure while maintaining nutritional efficiency, making it highly attractive in price-sensitive markets. Feed producers increasingly use MBM to optimize formulation economics without compromising animal health or productivity. This cost advantage is particularly significant in Asia-Pacific and Latin America, where feed affordability is a key industry concern.

Advancements in Rendering and Processing Technologies

Modern rendering technologies have significantly improved the safety, quality, and digestibility of meat and bone meal. Advanced sterilization and dry rendering systems ensure pathogen reduction and consistent nutrient retention. These improvements have helped overcome historical concerns related to safety and disease transmission, increasing acceptance across regulated markets. Technological upgrades are also enabling better resource efficiency, reducing production waste and enhancing overall yield from animal by-products.

What are the restraints for the global market?

Regulatory Restrictions on Animal By-Products

Strict regulations in regions such as Europe limit the use of animal-derived proteins in certain livestock feed applications due to disease control and biosecurity concerns. These restrictions reduce market penetration potential and create compliance challenges for manufacturers operating across multiple geographies. Variations in regulatory frameworks across countries further complicate international trade flows.

Raw Material Supply Volatility

Meat and bone meal production depends heavily on slaughterhouse waste availability, which fluctuates based on livestock cycles, seasonal demand, and meat consumption trends. This variability can lead to inconsistent supply, impacting pricing stability and production planning. Manufacturers often face challenges in maintaining continuous feedstock availability, particularly in regions with underdeveloped meat processing infrastructure.

What are the key opportunities in the meat and bone meal industry?

Expansion in Aquaculture Feed Demand

The rapid growth of aquaculture presents a major opportunity for MBM producers. As global seafood demand rises, fish farming operations are scaling up and seeking cost-effective protein substitutes for fish meal. Meat and bone meal provides a stable and economical alternative, especially in Asia-Pacific, where aquaculture production is expanding rapidly. This shift is expected to significantly increase MBM penetration in compound fish feed formulations.

Growth of Circular Economy and Waste Valorization Models

Governments worldwide are promoting sustainable waste management practices, encouraging industries to convert animal by-products into usable materials. Meat and bone meal production aligns directly with these initiatives, creating strong opportunities for investment in rendering infrastructure. Advanced processing technologies are further improving output quality, enabling expansion into premium applications such as pet food and organic fertilizers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8900 Million |

| Market Size in 2026 | USD 9451.80 Million |

| Market Size in 2031 | USD 12768.42 Million |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segment Analysis

The global meat and bone meal (MBM) market demonstrates a highly structured segmentation landscape defined by source, application, form, and processing type, each contributing distinctly to overall market expansion. By source, poultry-based meat and bone meal continues to dominate the global market with an estimated 38% share in 2025, largely attributed to the rapid acceleration of global poultry production, integrated broiler farming systems, and consistently high slaughter volumes across both developed and emerging economies. The poultry segment benefits from its cost efficiency, shorter production cycles, and increasing consumer preference for chicken meat as a primary protein source. These structural dynamics result in a continuous and stable supply of poultry by-products, which directly feed into MBM production. Additionally, poultry-derived MBM is increasingly preferred in feed formulations due to its balanced amino acid profile and relatively consistent nutrient composition compared to other animal sources, thereby strengthening its adoption across feed manufacturers globally.By processing type, dry rendering dominates the market with approximately 66% share, supported by its operational efficiency, scalability, and compliance with stringent global safety and biosecurity standards. Dry rendering is widely preferred due to its ability to efficiently process large volumes of animal by-products while preserving protein integrity and minimizing energy consumption compared to wet rendering systems. This method also significantly reduces microbial contamination risks, making it more suitable for feed-grade MBM production. The increasing emphasis on sustainable waste management practices in the meat processing industry has further reinforced the adoption of dry rendering systems, as they enable the conversion of slaughterhouse waste into valuable feed ingredients while minimizing environmental impact.

End-Use Insights

The animal feed industry continues to represent the largest and most influential end-use segment for meat and bone meal globally, driven by the expanding livestock population, rising demand for animal protein, and increasing industrialization of animal husbandry practices. Within this segment, poultry feed remains the fastest-growing sub-category, supported by the affordability of chicken meat, shorter production cycles, and rapid expansion of integrated poultry farming systems across Asia-Pacific, Latin America, and parts of Africa. Swine feed also contributes significantly to overall demand, particularly in regions with high pork consumption such as China and Europe, where MBM is widely used to improve feed efficiency and reduce dependency on plant-based protein sources.Beyond feed applications, the use of MBM in organic fertilizers is gaining traction due to its rich phosphorus, nitrogen, and calcium content, which supports soil fertility and sustainable agriculture practices. The growing global emphasis on circular economy models and waste valorization is further strengthening this segment. Export-driven demand also plays a crucial role in shaping end-use dynamics, with surplus-producing regions such as North America and Europe supplying MBM to import-dependent markets in Asia-Pacific and the Middle East. This cross-regional trade flow is essential in balancing global supply-demand gaps and ensuring feed security in regions with limited rendering capacity.

Explore more data points, trends and opportunities Download Free Sample Report

Meat and Bone Meal Market Segmentations

By Source

- Poultry-Based Meat and Bone Meal

- Beef-Based Meat and Bone Meal

- Pork-Based Meat and Bone Meal

- Mixed Animal By-Product Meal

By Application

- Animal Feed

- Poultry Feed

- Swine Feed

- Aquaculture Feed

- Pet Food

- Organic Fertilizers

By Form

- Powdered Meat and Bone Meal

- Pelletized Meat and Bone Meal

- Granular Meat and Bone Meal

By Processing Type

- Dry Rendering Process

- Wet Rendering Process

By End-Use Industry

- Livestock Feed Industry

- Aquaculture Industry

- Pet Food Industry

- Agriculture and Fertilizer Industry

- Export and Trading Industry

Regional Insights

North America

North America holds approximately 24% of the global MBM market share in 2025, with the United States serving as the primary production and export hub. The region’s leadership is strongly supported by its highly advanced rendering infrastructure, vertically integrated meat processing industry, and large-scale livestock production systems. One of the most significant drivers of regional growth is the presence of highly efficient supply chain networks that enable seamless conversion of animal by-products into value-added feed ingredients. The strong regulatory framework governing feed safety and biosecurity has also contributed to high-quality MBM production standards, making North America a preferred exporter to global markets. Export demand from Asia-Pacific and the Middle East continues to rise, supported by consistent product quality and compliance with international feed safety standards. Furthermore, the region benefits from strong integration between livestock farming and meat processing industries, ensuring a stable raw material supply base for MBM production.

Europe

Europe accounts for around 21% of the global market share in 2025, with major demand concentrated in countries such as Germany, France, Spain, and the United Kingdom. Although the region operates under strict regulatory frameworks regarding the use of animal by-products in feed, demand remains stable due to well-established livestock industries and increasing focus on sustainable feed alternatives. The European Union’s emphasis on circular economy principles has significantly contributed to the controlled and regulated use of processed animal proteins, including MBM, in selected feed applications.The region also plays a critical role in global trade, exporting significant volumes of MBM to Asia-Pacific and the Middle East, where demand outpaces local production capabilities. Furthermore, increasing demand for organic fertilizers and soil enhancers is supporting additional non-feed applications of MBM within European agricultural systems.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing regional market, driven by rapidly expanding livestock production, rising protein consumption, and increasing feed manufacturing capacity. China alone accounts for nearly 18% of global demand, supported by its massive pork and poultry industries. India, Vietnam, Indonesia, and Thailand are also emerging as key growth markets due to rising population, urbanization, and dietary shifts toward animal-based protein consumption. The region’s rapid expansion of integrated farming systems has significantly increased demand for cost-effective feed ingredients such as MBM.Additionally, the region’s growing feed manufacturing industry, supported by rising investments in industrial livestock farming, is further boosting MBM consumption. Import dependence in several countries also fuels trade flows from North America and Europe, ensuring consistent supply despite domestic production limitations. Government initiatives aimed at improving food security and livestock productivity are further accelerating market expansion across the region.

Latin America

Latin America is witnessing steady and structurally supported growth in the MBM market, with Brazil and Argentina emerging as the primary production and consumption hubs. The region’s strong livestock base, particularly in poultry and beef production, provides a consistent supply of raw materials for rendering operations. One of the key growth drivers is the expansion of export-oriented meat production industries, which generate significant volumes of by-products that are efficiently converted into MBM.The region is also increasingly integrated into global trade networks, exporting MBM to feed-deficient markets in Asia and the Middle East. Agricultural modernization, coupled with improvements in rendering infrastructure, has enhanced production efficiency and product quality. Additionally, the rising adoption of intensive livestock farming practices has increased demand for high-protein feed ingredients, further supporting MBM consumption. The region’s favorable climatic conditions and strong agricultural output base provide a stable foundation for continued market growth.

Middle East & Africa

The Middle East & Africa region represents an emerging and import-dependent market for meat and bone meal, with significant demand concentrated in countries such as Saudi Arabia, the United Arab Emirates, and South Africa. The primary driver of regional growth is the increasing expansion of livestock farming activities aimed at achieving food security and reducing dependency on imported meat products. However, limited domestic rendering infrastructure necessitates substantial imports of MBM from North America, Europe, and Latin America.Rapid population growth, urbanization, and rising income levels are contributing to increased consumption of meat and animal-derived products, thereby boosting demand for high-quality feed ingredients. The region is also witnessing gradual development of feed manufacturing industries, which is expected to enhance future demand for MBM. Government initiatives aimed at strengthening agricultural resilience and promoting domestic livestock production are further supporting market expansion. Additionally, the growing focus on cost-efficient feed solutions in arid and resource-constrained environments makes MBM an attractive protein source for regional feed formulators.

Key Players in the Global Meat and Bone Meal Market

- Darling Ingredients Inc.

- Tyson Foods Inc.

- JBS S.A.

- SARIA Group

- Valley Proteins Inc.

- Terramar International

- Ridley Corporation

- Sanimax

- Allanasons Pvt. Ltd.

- Baker Commodities Inc.

- West Coast Reduction Ltd.

- Ten Kate Holding B.V.

- ForFarmers N.V.

- NuTerra

- K-Pro International