Pet Supplements Market Size

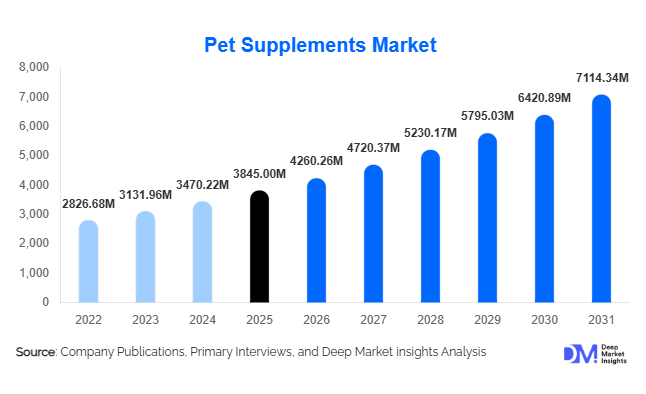

According to Deep Market Insights, the global pet supplements market size was valued at USD 3,845 million in 2025 and is projected to grow from USD 4,260.26 million in 2026 to reach USD 7,114.34 million by 2031, expanding at a CAGR of 10.8% during the forecast period (2026–2031). Market expansion is primarily driven by increasing pet humanization trends, rising veterinary healthcare awareness, and growing adoption of preventive nutrition solutions for companion animals. Pet owners worldwide are increasingly treating pets as family members, leading to higher spending on functional nutrition products targeting joint health, digestion, immunity, skin health, and cognitive wellness.

The market is transitioning from basic vitamin supplementation toward scientifically formulated nutraceutical solutions supported by veterinary recommendations and clinical validation. Growth is particularly strong in developed markets where premiumization trends dominate purchasing behavior, while emerging economies are witnessing rapid adoption due to rising disposable incomes and expanding urban pet ownership. E-commerce penetration, subscription-based pet wellness models, and personalized nutrition solutions are reshaping purchasing channels globally. Manufacturers are also investing heavily in palatable delivery formats such as soft chews, powders, and liquid supplements to improve compliance and repeat purchases. Overall, the pet supplements market is evolving into a preventive healthcare ecosystem aligned with long-term animal wellness rather than episodic treatment-based consumption.

Key Market Insights

- Preventive pet healthcare adoption is accelerating globally, positioning supplements as daily wellness essentials rather than optional products.

- Soft chews and functional treats dominate product innovation due to improved palatability and convenience.

- North America leads global demand, supported by high veterinary spending and premium pet nutrition adoption.

- Asia-Pacific is the fastest-growing region, driven by rising pet ownership in China and India.

- Veterinarian-backed formulations are increasingly influencing consumer purchasing decisions.

- Digital retail channels and subscription models are reshaping distribution strategies worldwide.

What are the latest trends in the pet supplements market?

Shift Toward Preventive and Functional Nutrition

Pet supplements are increasingly positioned as preventive healthcare tools rather than corrective treatments. Consumers are proactively investing in supplements targeting mobility, immunity, digestive health, and stress management. Functional ingredients such as probiotics, omega fatty acids, glucosamine, and CBD-alternative calming botanicals are becoming mainstream. Veterinary clinics are also recommending routine supplementation programs, further strengthening recurring demand. This preventive focus is reducing long-term healthcare costs while improving pet longevity, which continues to support sustained consumption growth.

Personalized and Breed-Specific Supplementation

Personalization represents one of the fastest-emerging trends within the market. Companies are leveraging pet health data, breed characteristics, age profiles, and lifestyle analytics to design customized supplement regimens. Subscription-based wellness kits tailored to individual pets are gaining traction, particularly in North America and Europe. Artificial intelligence-enabled pet health platforms are helping manufacturers recommend dosage plans and nutritional bundles, improving customer retention and brand loyalty.

What are the key drivers in the pet supplements market?

Rising Pet Humanization and Premium Spending

Globally, pets are increasingly regarded as family members, significantly influencing purchasing behavior. Owners are willing to spend on premium healthcare solutions, including organic and clinically validated supplements. Higher disposable incomes and lifestyle changes have contributed to increased expenditure per pet, particularly in urban households. Premium supplements offering clean-label ingredients and veterinary endorsements command higher margins and drive market expansion.

Growth in Veterinary Preventive Care Awareness

Veterinary professionals are actively promoting nutritional supplementation as part of preventive health programs. Routine wellness checkups increasingly include dietary recommendations, boosting supplement adoption rates. Educational campaigns highlighting joint degeneration, digestive disorders, and immunity challenges in aging pets have further increased demand.

Expansion of E-commerce and Direct-to-Consumer Channels

Online retail platforms have transformed accessibility and purchasing convenience. Subscription deliveries, bundled health kits, and auto-refill services are increasing repeat purchase frequency. Digital platforms also allow brands to educate consumers through targeted marketing and pet health content, accelerating adoption across younger pet owner demographics.

What are the restraints for the global market?

Regulatory Variability Across Regions

The pet supplements market faces inconsistent regulatory frameworks worldwide, creating compliance challenges for manufacturers. Ingredient approvals, labeling requirements, and health claims differ across regions, increasing product development costs and slowing global expansion strategies.

Limited Scientific Standardization

Although demand is rising, some supplement categories lack standardized clinical validation. Consumer skepticism regarding efficacy and inconsistent product quality among smaller brands can hinder long-term adoption. Strengthening scientific research and transparency remains critical for sustained credibility.

What are the key opportunities in the pet supplements industry?

Expansion in Emerging Pet Ownership Markets

Rapid urbanization and rising middle-class populations in Asia-Pacific and Latin America present substantial growth opportunities. Countries such as China, India, and Brazil are witnessing double-digit increases in pet adoption. Manufacturers entering these markets with affordable premium products and localized formulations can capture significant untapped demand.

Integration of Biotechnology and Nutraceutical Innovation

Advancements in microbiome science, precision nutrition, and plant-based bioactives are opening new product development avenues. Supplements targeting gut microbiota, cognitive health, and longevity are gaining attention. Biotechnology partnerships between supplement brands and research institutions are expected to generate high-margin innovation pipelines.

Veterinary Channel Partnerships and Prescription Supplements

Collaboration with veterinary networks represents a high-growth opportunity. Prescription-grade supplements and therapeutic nutraceuticals recommended by veterinarians are gaining credibility among pet owners. This channel improves trust, enhances clinical positioning, and creates recurring revenue streams for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3845 Million |

| Market Size in 2026 | USD 4260.26 Million |

| Market Size in 2031 | USD 7114.34 Million |

| CAGR | 10.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global pet supplements market is experiencing strong structural expansion as companion animal ownership increasingly aligns with human wellness trends, preventive healthcare awareness, and premium nutrition adoption. Among product categories, joint health supplements continue to dominate the market landscape, accounting for approximately 28% of total global market share in 2025. The leadership of this segment is primarily driven by the growing aging pet population worldwide, particularly among dogs, where mobility issues such as arthritis, hip dysplasia, and age-related inflammation are becoming more prevalent. Veterinary professionals increasingly recommend glucosamine, chondroitin, MSM, collagen, and omega-based formulations as long-term mobility management solutions, reinforcing recurring purchasing behavior among pet owners. The humanization of pets has also encouraged owners to proactively address mobility challenges before symptoms worsen, transforming joint health supplements from reactive treatment products into preventive wellness solutions. This shift significantly strengthens the segment’s long-term growth trajectory.Digestive health supplements represent the second-largest product category, supported by rising awareness of gut microbiome health and its connection to immunity, nutrient absorption, and overall vitality. Increasing incidences of food sensitivities, dietary transitions, and digestive disorders among pets have accelerated demand for probiotics, prebiotics, and enzyme-based supplements. Pet owners are becoming more educated about gastrointestinal wellness through veterinary consultations and digital content, encouraging routine supplementation rather than occasional use. Additionally, premium pet food brands increasingly promote digestive supplementation compatibility, creating cross-category demand synergy that further accelerates market penetration.Skin and coat supplements are witnessing notable expansion due to their visibly measurable results, which significantly influence consumer repurchase behavior. Products containing omega-3 fatty acids, biotin, zinc, and vitamin complexes deliver improvements in coat shine, shedding reduction, and skin irritation relief within relatively short timeframes. Because pet owners can directly observe outcomes, this category benefits from strong word-of-mouth marketing and social media influence. The increasing prevalence of allergies and dermatological conditions, particularly among urban pets exposed to pollution and indoor environments, further strengthens demand for skin-focused formulations.Multivitamins maintain a stable yet essential market position, particularly among first-time pet owners seeking comprehensive daily nutrition support. These products serve as entry-level supplements, providing balanced micronutrient coverage that complements commercial pet diets. The primary driver of this segment is convenience and perceived holistic care, as consumers increasingly seek simplified wellness routines that address multiple health needs simultaneously. While growth rates are moderate compared to specialized supplements, multivitamins benefit from broad adoption across demographic groups and price tiers, ensuring consistent baseline demand.

Application Insights

Based on animal type, dogs remain the dominant application segment, contributing nearly 62% of global demand in 2025. The leading driver behind this dominance is significantly higher healthcare expenditure per dog compared to other companion animals. Dogs typically require more frequent veterinary visits, mobility care, behavioral management, and performance nutrition, which directly increases supplement usage rates. Larger body sizes also require higher dosage volumes, further expanding revenue contribution. Additionally, dogs participate more actively in outdoor activities, which elevates the need for joint, immunity, and recovery supplements. The expansion of breed-specific health awareness has encouraged targeted supplementation strategies tailored to size, age, and genetic predispositions, reinforcing long-term consumption patterns.The cat supplement segment represents the fastest-growing application category. Rising indoor pet ownership, particularly in urban apartments, has significantly expanded global cat populations. Indoor cats often experience obesity, urinary health challenges, digestive sensitivity, and stress-related behaviors, creating strong demand for specialized nutritional support. Another important growth driver is the increasing availability of cat-specific supplement formulations designed to address feline taste preferences and metabolic requirements. Historically underpenetrated compared to dog supplements, the category is now benefiting from innovation and improved product palatability, accelerating adoption rates.Supplements for small mammals, birds, and exotic pets remain niche but steadily expanding segments. Growth is supported by increasing diversification of companion animal ownership and rising interest in specialty pet care. Retailers and online platforms are expanding assortments tailored to rabbits, guinea pigs, parrots, and reptiles, enabling manufacturers to capture previously underserved consumer groups. Although smaller in scale, these segments offer high-margin opportunities due to specialized formulations and limited competition.

Form Insights

In terms of product form, soft chews lead the global market with approximately 35% share in 2025, primarily driven by superior palatability and administration convenience. The leading driver of this segment is compliance, as pet owners increasingly prefer treat-like formats that eliminate the difficulty associated with tablets or capsules. Soft chews transform supplementation into a positive experience for pets, improving daily adherence and encouraging routine usage. Manufacturers are also incorporating functional ingredients into flavored chew bases, blending nutrition with reward-based feeding behavior, which further enhances consumer acceptance.Powder supplements represent another major segment due to dosage flexibility and formulation versatility. Powders allow pet owners to mix supplements directly with food, making them particularly effective for digestive health, multivitamin, and performance nutrition applications. The leading driver for powder formats is customization, as owners can adjust serving sizes according to pet weight and health condition. Additionally, powders often enable higher ingredient concentrations and easier formulation of probiotics and herbal compounds that may be difficult to stabilize in chew formats.Liquid supplements are gaining momentum, especially among senior pets and veterinary-administered treatments. Liquids provide rapid absorption and precise dosing, making them suitable for animals with dental issues, reduced appetite, or swallowing difficulties. Veterinary professionals frequently recommend liquid formulations during recovery periods, reinforcing their growing adoption within clinical settings. As aging pet populations increase globally, demand for easily administered supplement formats is expected to expand further.

Distribution Channel Insights

Distribution dynamics within the pet supplements market are evolving rapidly as digital commerce reshapes consumer purchasing behavior. Online retail channels dominate global sales, accounting for nearly 38% of total revenue. The leading growth driver for online distribution is subscription-based purchasing models, which encourage recurring deliveries and strengthen customer retention. E-commerce platforms provide extensive product variety, transparent reviews, and educational content, empowering consumers to compare formulations and make informed decisions. Cross-border e-commerce has also enabled international brands to enter emerging markets without extensive physical retail infrastructure, significantly expanding market accessibility.Veterinary clinics remain highly influential, particularly within premium and therapeutic supplement categories. Veterinarian recommendations strongly influence purchasing decisions, especially for joint, digestive, and anxiety-related supplements. Clinical endorsement enhances product credibility and supports higher price positioning. As preventive care becomes integrated into veterinary treatment protocols, clinics are increasingly stocking supplements as part of comprehensive wellness programs, reinforcing their strategic importance within the distribution ecosystem.Specialty pet stores continue to play a critical role in brand discovery and consumer education. Unlike online channels, physical stores provide personalized consultation, product demonstrations, and curated selections tailored to pet health needs. Knowledgeable staff recommendations and experiential retail environments help new brands build trust among consumers. Hybrid retail strategies combining physical presence with digital engagement are becoming increasingly common as manufacturers seek omnichannel visibility.

End-Use Insights

Household pet owners remain the primary end users of pet supplements, accounting for more than 70% of overall consumption. The leading driver of this segment is the continued humanization of pets, where animals are increasingly viewed as family members deserving preventive healthcare comparable to human wellness routines. Rising disposable incomes and emotional attachment to pets are encouraging owners to invest in long-term health management rather than reactive treatment.Veterinary hospitals represent the fastest-growing end-use segment as clinical nutrition becomes integrated into medical treatment strategies. Supplements are now routinely recommended alongside pharmaceuticals to support recovery, immunity enhancement, and chronic disease management. This integration reflects a broader shift toward holistic veterinary care models that emphasize prevention and nutritional support.Pet daycare centers, breeders, kennels, and animal shelters are also expanding supplement usage to maintain health standards and improve animal wellbeing. These institutional users increasingly adopt supplements to support immunity, coat quality, and stress reduction among animals housed in shared environments. Additionally, export-driven demand is rising as North American and European brands expand into Asia-Pacific markets through cross-border digital commerce. The broader companion animal healthcare industry itself is expanding at approximately 8–9% annually, reinforcing supplements as a complementary and rapidly scaling category within the overall ecosystem.

Explore more data points, trends and opportunities Download Free Sample Report

Pet Supplements Market Segmentations

By Product Type

- Joint Health Supplements

- Skin & Coat Supplements

- Digestive Health & Probiotics

- Calming & Anxiety Supplements

- Multivitamins & General Wellness Supplements

- Dental Health Supplements

- Immune Support Supplements

- Weight Management Supplements

By Pet Type

- Dogs

- Cats

- Birds

- Small Mammals

- Aquatic Pets

- Horses & Companion Livestock

By Form Type

- Chewable Tablets & Soft Chews

- Powders

- Liquids & Oils

- Capsules & Tablets

- Functional Treats

By Distribution Channel

- Veterinary Clinics & Hospitals

- Pet Specialty Stores

- Online Retail & E-commerce

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

By Ingredient Type

- Vitamins & Minerals

- Omega Fatty Acids

- Probiotics & Prebiotics

- Herbal & Botanical Extracts

- Protein & Amino Acid Supplements

Regional Insights

North America

North America holds the largest share of the global pet supplements market, accounting for approximately 41% of total demand in 2025, with the United States serving as the primary revenue contributor. Regional dominance is driven by exceptionally high pet healthcare expenditure, widespread pet insurance adoption, and advanced veterinary infrastructure. A major growth driver in North America is the strong cultural emphasis on preventive healthcare, where supplements are routinely incorporated into daily pet care routines rather than used only for treatment purposes. Consumers demonstrate high willingness to pay for premium, scientifically formulated products supported by clinical research and transparent ingredient sourcing.The region also benefits from mature e-commerce ecosystems and subscription-based purchasing models that encourage consistent product usage. Innovation pipelines remain strong, with manufacturers introducing functional blends targeting mobility, cognitive health, and emotional wellbeing. Canada contributes steady growth through increasing awareness of pet wellness and expanding insurance coverage, which indirectly supports supplement adoption by encouraging proactive health management. Regulatory clarity and established quality standards further enhance consumer confidence, allowing premium brands to thrive.

Europe

Europe accounts for nearly 27% of global market share, supported by strong demand across Germany, the United Kingdom, and France. One of the primary drivers of regional growth is consumer preference for natural, organic, and sustainably sourced formulations aligned with stringent European regulatory frameworks. Pet owners increasingly seek clean-label supplements free from artificial additives, mirroring broader human nutrition trends.Functional nutrition adoption continues rising across Western Europe as veterinary professionals emphasize preventive care and longevity-focused supplementation. Aging pet populations across developed European nations further strengthen demand for joint health and cognitive support products. Additionally, sustainability considerations such as recyclable packaging and ethically sourced ingredients influence purchasing decisions, encouraging manufacturers to innovate responsibly. Eastern Europe represents an emerging opportunity, where rising disposable incomes and expanding retail infrastructure are gradually increasing market penetration.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 13%. Rapid urbanization, increasing middle-class populations, and evolving lifestyles are key drivers fueling pet adoption across major economies such as China and India. Younger consumers living in urban apartments increasingly choose companion animals for emotional companionship, creating strong demand for accessible wellness products. The leading growth driver in the region is rising awareness of pet health combined with expanding digital retail ecosystems that improve product availability.China’s market growth is supported by premiumization trends and strong online retail penetration, while India is witnessing accelerated adoption driven by growing disposable income and expanding veterinary services. Japan remains a mature yet innovation-driven market focused on longevity and aging pet care, reflecting the country’s demographic structure. Regional manufacturers are increasingly localizing formulations to suit dietary habits and climate conditions, further enhancing adoption rates.

Latin America

Latin America is experiencing steady market expansion led by Brazil and Mexico, where rising pet ownership and improving retail infrastructure are driving supplement consumption. Urban middle-class growth and increasing exposure to global pet care trends are encouraging consumers to adopt preventive nutrition practices. The leading regional driver is gradual premiumization within metropolitan areas, where consumers are transitioning from basic pet food toward value-added wellness products.E-commerce expansion and international brand entry are improving product accessibility across the region. Veterinary awareness campaigns and growing availability of specialty pet retailers are further supporting market education, which remains critical for long-term adoption. While price sensitivity persists in certain markets, demand for functional supplements continues to rise as awareness improves.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth frontier, led by the United Arab Emirates and South Africa. Rising expatriate populations and increasing adoption of premium pet care practices are key drivers stimulating supplement demand. Urbanization and higher disposable incomes in major metropolitan centers are encouraging pet owners to invest in advanced healthcare products, including nutritional supplements.Another important regional growth driver is the expansion of veterinary infrastructure and specialized pet retail networks, which enhance product availability and professional recommendations. Awareness of preventive care remains in early stages compared to mature markets; however, rapid lifestyle modernization and exposure to global pet care standards are accelerating adoption rates. As distribution networks strengthen and consumer education improves, the region is expected to demonstrate sustained long-term growth potential within the global pet supplements industry.

Key Players in the Pet Supplements Market

- Nestlé Purina PetCare

- Mars Petcare

- Zoetis Inc.

- Hill’s Pet Nutrition

- Virbac

- Nutramax Laboratories

- Zesty Paws

- NOW Foods

- Ark Naturals

- PetHonesty

- Vetoquinol

- Swedencare AB

- Dechra Pharmaceuticals

- FoodScience LLC

- Beaphar