Dog Food Subscription Boxes Market Size

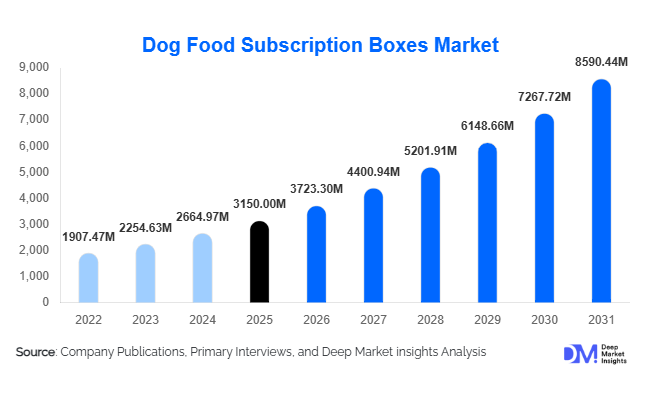

According to Deep Market Insights, the global dog food subscription boxes market size was valued at USD 3,150 million in 2025 and is projected to grow from USD 3,723.30 million in 2026 to reach USD 8,590.44 million by 2031, expanding at a CAGR of 18.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing pet humanization, rising demand for premium and personalized pet nutrition, and the growing adoption of convenient direct-to-consumer subscription models. The shift toward fresh, organic, and functional pet food, coupled with digital platform penetration, is accelerating recurring revenue models globally.

Key Market Insights

- Personalized nutrition is becoming the cornerstone of subscription services, with AI-driven meal planning and breed-specific formulations gaining traction globally.

- Fresh and human-grade dog food subscriptions are rapidly expanding, driven by consumer preference for minimally processed and high-quality ingredients.

- North America dominates the market due to strong pet ownership rates and advanced DTC ecosystems.

- Asia-Pacific is the fastest-growing region, supported by rising pet adoption and increasing disposable income in countries such as China and India.

- Direct-to-consumer channels account for the majority of sales, enabling better margins and customer engagement for brands.

- Sustainability trends, including eco-friendly packaging and ethical sourcing, are influencing purchasing decisions among younger consumers.

What are the latest trends in the dog food subscription boxes market?

Rise of Hyper-Personalized Pet Nutrition

The dog food subscription boxes market is witnessing a strong shift toward hyper-personalization, where companies leverage pet data such as breed, age, weight, and health conditions to curate customized meal plans. This trend is supported by advancements in artificial intelligence and data analytics, allowing brands to create highly tailored offerings that enhance pet health outcomes. Subscription platforms are increasingly integrating mobile apps and digital dashboards where pet owners can track nutrition, adjust plans, and receive recommendations. This level of personalization not only improves customer satisfaction but also increases retention rates, making it a key growth driver in the market.

Premiumization and Fresh Food Adoption

Consumers are increasingly opting for premium dog food subscription boxes that emphasize fresh, organic, and human-grade ingredients. Fresh and refrigerated meal kits are gaining popularity due to their perceived health benefits and higher nutritional value compared to traditional kibble. Brands are investing in cold-chain logistics and sustainable sourcing practices to meet this demand. The premiumization trend is also reflected in higher price points and improved profit margins, with consumers willing to pay more for quality and transparency. This shift is particularly prominent in developed markets, where pet owners prioritize wellness and longevity for their pets.

What are the key drivers in the dog food subscription boxes market?

Growing Pet Humanization Trend

The increasing tendency of pet owners to treat dogs as family members is a major driver of the market. This behavioral shift has led to higher spending on premium pet care products, including subscription-based food services. Consumers are prioritizing quality, safety, and nutrition, which aligns with the offerings of subscription models. The demand for specialized diets, including grain-free and functional formulations, is also rising as pet owners become more health-conscious.

Convenience and Recurring Delivery Models

The convenience offered by subscription services is another key growth driver. Busy lifestyles and urbanization have increased the demand for hassle-free solutions that ensure consistent delivery of pet food. Subscription models eliminate the need for frequent store visits and provide flexibility in delivery schedules. This has led to strong adoption among urban consumers, particularly in metropolitan regions with high e-commerce penetration.

What are the restraints for the global market?

High Cost of Premium Subscriptions

One of the major challenges in the market is the high cost associated with premium and fresh dog food subscription boxes. These products often require high-quality ingredients and complex logistics, resulting in higher prices compared to traditional pet food. This limits adoption among price-sensitive consumers, especially in emerging markets where affordability remains a concern.

Logistics and Cold Chain Constraints

The distribution of fresh and refrigerated dog food requires robust cold chain infrastructure, which can increase operational costs and complexity. Ensuring timely delivery while maintaining product quality is a significant challenge, particularly in regions with underdeveloped logistics networks. These constraints can hinder market expansion and scalability.

What are the key opportunities in the dog food subscription boxes industry?

Expansion into Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising pet ownership and increasing disposable income. Companies that localize their offerings and adopt flexible pricing strategies can tap into these markets effectively. Early entry into these regions can provide a competitive advantage as subscription models are still in the nascent stage.

Integration with Veterinary and Wellness Services

Collaborations with veterinary clinics and pet wellness platforms offer new avenues for growth. Subscription services can be integrated with prescription diets, preventive healthcare packages, and diagnostic tools, creating a comprehensive pet care ecosystem. This approach enhances customer trust and opens up new revenue streams for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3150.00 Million |

| Market Size in 2026 | USD 3723.30 Million |

| Market Size in 2031 | USD 8590.44 Million |

| CAGR | 18.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product type landscape within the dog food subscription box market is evolving rapidly, driven by changing consumer expectations around convenience, nutrition, and personalization. Fresh and refrigerated dog food subscription boxes dominate the market, accounting for approximately 32% of the global market share in 2025. This leadership position is primarily attributed to the growing perception among pet owners that fresh food closely mirrors a natural diet, thereby supporting better digestion, improved coat health, and overall vitality in dogs. The increasing humanization of pets has led consumers to extend their own dietary preferences—such as minimally processed and preservative-free meals—to their pets, further strengthening demand for fresh formats. Additionally, advancements in cold-chain logistics and packaging technologies have enabled companies to deliver fresh meals efficiently, maintaining quality and safety while scaling operations.Mixed meal kits are emerging as a dynamic and flexible solution, catering to pet owners who seek variety and balanced nutrition. These kits often combine fresh, dry, and freeze-dried components, allowing for customized feeding routines that can adapt to a dog’s preferences and health requirements. This flexibility is particularly attractive to consumers experimenting with hybrid feeding approaches, where traditional kibble is supplemented with fresh or raw elements. The ability to rotate meals and introduce dietary diversity is a key driver supporting growth in this segment.Freeze-dried and dehydrated dog food formats are also gaining traction, supported by their unique combination of convenience and nutritional preservation. These products retain most of the nutrients found in fresh ingredients while offering extended shelf life and easy storage. For consumers who prioritize portability, especially those who travel frequently with pets, these formats present a compelling value proposition. The segment’s growth is further fueled by advancements in dehydration technologies that enhance taste, texture, and rehydration quality, making these options increasingly competitive with fresh alternatives.

Ingredient Profile Insights

Ingredient preferences are playing a pivotal role in shaping purchasing decisions in the dog food subscription box market. Grain-free formulations lead the ingredient segment with around 28% market share, driven by rising concerns over food sensitivities, allergies, and digestive issues among dogs. Pet owners are becoming more informed about ingredient labels and are actively seeking diets that exclude common allergens such as wheat, corn, and soy. The perception that grain-free diets align more closely with ancestral canine diets has further reinforced their popularity, despite ongoing debates within the veterinary community.Functional diets represent another rapidly expanding segment, reflecting a shift toward preventive healthcare for pets. These diets are specifically formulated to address targeted health concerns, including weight management, joint health, digestive support, skin and coat improvement, and immune system enhancement. The integration of functional ingredients such as omega fatty acids, probiotics, glucosamine, and antioxidants is becoming increasingly common. As veterinary recommendations increasingly influence consumer decisions, subscription services offering tailored functional diets are experiencing higher adoption rates. The leading driver within this segment is the growing awareness among pet owners that nutrition can significantly impact long-term health outcomes, reducing the need for medical interventions.Additionally, novel protein sources such as duck, venison, and plant-based alternatives are gaining attention, particularly among pets with protein sensitivities. These innovations not only diversify product offerings but also cater to evolving consumer concerns around sustainability and environmental impact. As the market matures, ingredient differentiation will continue to serve as a key lever for brand positioning and customer retention.

Subscription Model Insights

The subscription model segment is at the core of the market’s value proposition, offering convenience, personalization, and consistency. Customized and personalized subscription plans dominate this segment, contributing nearly 38% of the market share. The primary driver of this dominance is the increasing use of data-driven technologies that enable companies to tailor meal plans based on a dog’s breed, age, weight, activity level, and health conditions. This high degree of personalization enhances customer satisfaction, fosters brand loyalty, and reduces churn rates. Consumers are increasingly willing to pay a premium for solutions that simplify decision-making while ensuring optimal nutrition for their pets.Flexible subscription models are gaining popularity as they address the need for adaptability in modern lifestyles. These plans allow customers to modify delivery frequency, pause subscriptions, or switch meal types without penalties. This flexibility is particularly valuable in households with changing routines or multiple pets with varying dietary needs. The increasing demand for control and convenience is pushing companies to invest in user-friendly digital platforms that facilitate seamless subscription management.Furthermore, the integration of artificial intelligence and machine learning into subscription platforms is enhancing the personalization experience. Predictive analytics can anticipate changes in a pet’s dietary needs and recommend adjustments proactively. As technological capabilities continue to advance, the subscription model segment is expected to become even more sophisticated, further strengthening its role as a key growth driver in the market.

Distribution Channel Insights

Distribution channels in the dog food subscription box market are heavily influenced by digital transformation and changing consumer purchasing behaviors. Direct-to-consumer channels account for approximately 62% of the market, driven by the widespread adoption of e-commerce and the ability of brands to establish direct relationships with customers. By bypassing traditional retail intermediaries, companies can offer competitive pricing, personalized experiences, and greater control over branding and customer engagement. The leading driver for this segment is the convenience of home delivery combined with subscription-based replenishment, which eliminates the need for repetitive purchasing decisions.Third-party e-commerce platforms also play a crucial role in expanding market reach, particularly for emerging brands seeking visibility and customer acquisition. These platforms provide access to a large and diverse customer base, along with established logistics networks. While margins may be lower compared to direct sales, the scale and exposure offered by these platforms make them an important component of the overall distribution strategy. Consumer trust in well-known online marketplaces further supports their continued relevance.Veterinary clinics are emerging as niche but influential distribution channels, especially for therapeutic and prescription-based diets. Pet owners often rely on veterinary recommendations when addressing specific health concerns, making clinics a trusted point of purchase. The growth of this channel is driven by increasing awareness of specialized nutrition and the role of diet in managing medical conditions. As collaboration between pet food companies and veterinary professionals strengthens, this channel is expected to gain further prominence.Additionally, the integration of omnichannel strategies is becoming increasingly important. Brands are combining online platforms with offline touchpoints such as pop-up stores and experiential events to enhance customer engagement. This holistic approach not only improves accessibility but also strengthens brand loyalty in a competitive market.

End-Use Insights

The end-use segment is dominated by individual pet owners, who contribute over 80% of total demand. This dominance is driven by the emotional bond between pets and their owners, which often translates into a willingness to invest in high-quality nutrition. The humanization of pets has led to a shift in perception, with dogs increasingly regarded as family members rather than companions. This cultural shift is a key driver supporting the adoption of premium subscription-based food solutions.Pet care services, including boarding facilities, daycare centers, and grooming services, represent the fastest-growing end-use segment. These establishments require consistent and high-quality nutrition to maintain the health and well-being of the animals under their care. Subscription models offer a reliable and convenient solution, ensuring timely delivery and standardized meal quality. The rapid growth of this segment is closely linked to urbanization and the increasing number of dual-income households, where pet owners rely on professional services for pet care.Veterinary clinics are also gaining importance as end users, particularly for specialized and prescription-based diets. As preventive healthcare becomes a priority, veterinarians are playing a more active role in guiding nutritional choices. Subscription services that cater to medical needs, such as renal diets or weight management programs, are experiencing increased demand within this segment. The leading driver here is the growing recognition of nutrition as a critical component of overall pet health and disease management.

Explore more data points, trends and opportunities Download Free Sample Report

Dog Food Subscription Boxes Market Segmentations

By Product Type

- Dry Dog Food Subscription Boxes

- Wet Dog Food Subscription Boxes

- Fresh

- Refrigerated Dog Food Subscription Boxes

- Freeze-Dried & Dehydrated Dog Food Subscription Boxes

- Mixed Meal Kits

By Ingredient Profile

- Grain-Free Formulations

- Grain-Inclusive Formulations

- Organic & Natural Ingredient-Based

- Functional

- Therapeutic Diets

- High-Protein

- Specialty Diets

By Subscription Model

- Fixed Meal Plans

- Customized

- Personalized Plans

- Flexible

- On-Demand Subscriptions

- Tier-Based Subscriptions

By Distribution Channel

- Direct-to-Consumer

- Third-Party E-commerce Platforms

- Pet Specialty Retailers

- Veterinary Clinics

Regional Insights

North America

North America holds the largest share of the market, accounting for approximately 38% in 2025, with the United States leading demand. The region’s dominance is underpinned by a combination of high pet ownership rates, strong purchasing power, and a well-established e-commerce ecosystem. Consumers in North America are early adopters of innovative pet care solutions, including subscription-based services. The widespread availability of high-speed internet and digital payment systems further facilitates seamless online transactions.Another key driver of regional growth is the increasing humanization of pets, which has led to higher spending on premium products and services. The presence of leading market players and continuous product innovation also contribute to the region’s leadership position. Additionally, the growing awareness of pet health and wellness, supported by extensive marketing and educational campaigns, is driving demand for specialized and functional diets. The integration of advanced technologies such as AI-driven personalization and data analytics is further enhancing the customer experience, solidifying North America’s position as a mature and highly competitive market.

Europe

Europe represents around 27% of the global market, with significant demand from countries such as the United Kingdom, Germany, and France. The region is characterized by stringent regulatory standards that ensure product quality and safety, fostering consumer trust. One of the primary drivers of growth in Europe is the increasing preference for sustainable and ethically sourced pet food products. Consumers are highly conscious of environmental impact and are more likely to support brands that align with their values.The rising popularity of organic and natural diets is another key factor supporting market expansion. European consumers tend to prioritize transparency and traceability, leading to increased demand for clean-label products. Additionally, the growing trend of pet humanization is influencing purchasing behavior, with pet owners seeking premium and customized nutrition solutions. The expansion of e-commerce platforms and improvements in logistics infrastructure are further facilitating market growth, enabling companies to reach a broader customer base across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 21%. Countries such as China, India, and Japan are driving growth due to rising pet adoption rates and increasing awareness of pet health and nutrition. Rapid urbanization and changing lifestyles are leading to a shift toward nuclear families and single-person households, where pets often serve as companions. This demographic trend is significantly boosting demand for convenient and high-quality pet care solutions.The expanding middle class and rising disposable incomes are also key drivers, enabling consumers to spend more on premium products. Additionally, the growing influence of Western lifestyles and dietary preferences is shaping consumer expectations, leading to increased adoption of subscription-based models. The proliferation of smartphones and digital payment systems is further accelerating the growth of e-commerce, making it easier for consumers to access subscription services. As awareness continues to grow and infrastructure improves, Asia-Pacific is expected to remain a key growth engine for the global market.

Latin America

Latin America is witnessing gradual growth, particularly in countries such as Brazil and Mexico. The region’s expansion is supported by increasing urbanization and rising disposable incomes, which are enabling consumers to explore premium pet care options. The growing popularity of pets as companions is driving demand for high-quality nutrition, although price sensitivity remains a key consideration.Another important driver is the gradual shift toward modern retail and e-commerce channels, which are improving product accessibility. While the market is still in a developing stage compared to North America and Europe, increasing awareness of pet health and nutrition is expected to support long-term growth. Local players are also entering the market with region-specific offerings, further contributing to its expansion.

Middle East & Africa

The Middle East & Africa region is an emerging market, with growth driven by rising pet ownership in countries such as the United Arab Emirates and South Africa. Increasing urbanization and higher income levels are enabling consumers to spend more on premium pet food products. The growing expatriate population in the Middle East is also influencing demand, as many expatriates bring established pet care practices from their home countries.Changing consumer preferences, particularly among younger demographics, are contributing to the adoption of subscription-based models. The expansion of e-commerce platforms and improvements in logistics infrastructure are further supporting market growth. While the region faces challenges such as limited awareness and price sensitivity, ongoing economic development and increasing exposure to global trends are expected to drive gradual but steady expansion in the coming years.

Key Players in the Dog Food Subscription Boxes Market

- Mars Incorporated

- Nestlé Purina PetCare

- Hill’s Pet Nutrition

- The Farmer’s Dog

- Nom Nom

- Ollie Pets

- JustFoodForDogs

- PetPlate

- Spot & Tango

- Butternut Box

- Tails.com

- Chewy Inc.

- Wellness Pet Company

- Blue Buffalo

- Freshpet Inc.