Animal Feed Ingredients Market Size

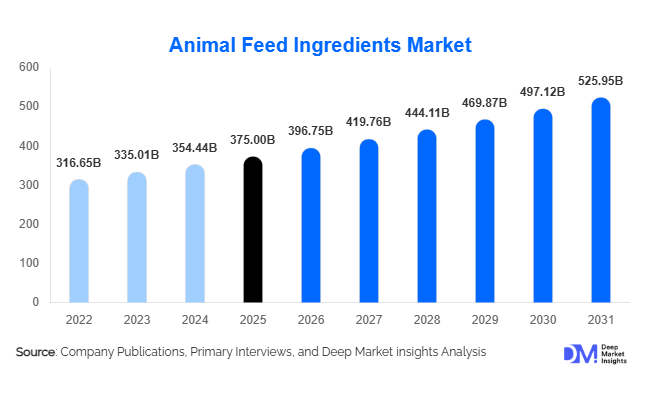

According to Deep Market Insights, the global animal feed ingredients market size was valued at USD 375.00 Billion in 2025 and is projected to grow from USD 396.75 Billion in 2026 to reach USD 525.95 Billion by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The market growth is primarily driven by rising global demand for animal protein, increasing industrialization of livestock farming, and the need for high-efficiency feed solutions. Growing consumption of poultry, dairy, and aquaculture products, particularly in emerging economies, is significantly boosting the demand for feed ingredients such as cereals, oilseed meals, and functional additives.

Key Market Insights

- Cereals and grains dominate feed formulations, accounting for the largest share due to their role as primary energy sources in livestock diets.

- Poultry remains the leading livestock segment, driven by high global consumption of chicken meat and eggs.

- Asia-Pacific dominates the global market, supported by large-scale livestock production in China and India.

- Aquaculture is the fastest-growing segment, fueled by rising seafood demand and depletion of wild fish stocks.

- Alternative proteins such as insect meal and algae are gaining traction as sustainable feed solutions.

- Technological advancements in precision nutrition are improving feed efficiency and reducing production costs.

What are the latest trends in the animal feed ingredients market?

Shift Toward Sustainable and Alternative Feed Ingredients

The market is increasingly shifting toward sustainable alternatives such as insect protein, algae-based feed, and single-cell proteins. These alternatives are gaining popularity due to their lower environmental footprint and high nutritional value. With growing concerns over the sustainability of traditional feed sources like soybean meal and fishmeal, manufacturers are investing in scalable production technologies for alternative proteins. Regulatory support in regions like Europe is further accelerating adoption, particularly in aquaculture and poultry feed applications. This trend is expected to reshape supply chains and reduce dependency on conventional agricultural commodities.

Precision Nutrition and Digital Feed Optimization

Advancements in data analytics, artificial intelligence, and IoT are transforming feed formulation and livestock management. Precision nutrition enables customized feed solutions tailored to specific animal requirements, improving feed conversion ratios and reducing waste. Automated feeding systems, real-time monitoring tools, and AI-driven formulation software are being widely adopted by large-scale livestock producers. This trend not only enhances productivity but also supports sustainability goals by minimizing resource utilization and emissions.

What are the key drivers in the animal feed ingredients market?

Rising Global Demand for Animal Protein

Increasing population, urbanization, and rising disposable incomes are driving higher consumption of meat, dairy, and seafood products. Emerging economies, particularly in Asia and Latin America, are witnessing a dietary shift toward protein-rich foods, significantly boosting demand for feed ingredients.

Industrialization of Livestock Farming

The transition from traditional farming to large-scale commercial livestock operations is a major growth driver. Industrial farms require consistent, high-quality feed inputs to ensure productivity and efficiency, leading to increased demand for scientifically formulated feed ingredients.

Growing Focus on Animal Health and Feed Efficiency

Feed additives such as amino acids, enzymes, and probiotics are gaining importance as they improve nutrient absorption, enhance immunity, and reduce feed costs. This trend is particularly strong in poultry and aquaculture sectors, where efficiency directly impacts profitability.

What are the restraints for the global market?

Volatility in Raw Material Prices

Prices of key feed ingredients such as corn and soybean are highly volatile due to weather conditions, geopolitical tensions, and trade policies. This volatility affects production costs and profit margins for feed manufacturers.

Stringent Regulatory Frameworks

Strict regulations regarding feed safety, quality standards, and the use of additives, particularly in Europe and North America, pose challenges for manufacturers. Compliance increases operational costs and limits flexibility in product formulation.

What are the key opportunities in the animal feed ingredients industry?

Expansion of Aquaculture Feed Demand

The rapid growth of aquaculture presents significant opportunities for feed ingredient manufacturers. With global seafood consumption rising and wild fish stocks declining, aquaculture is becoming a primary source of protein. This drives demand for specialized feed ingredients such as high-protein meals, omega-rich additives, and digestibility enhancers.

Adoption of Alternative Protein Sources

Alternative proteins such as insect meal and algae are emerging as viable solutions to address sustainability challenges. These ingredients offer high nutritional value and lower environmental impact, making them attractive for next-generation feed formulations.

Integration of Digital and Smart Feeding Systems

The adoption of digital technologies in feed management is creating new growth opportunities. AI-driven formulation tools, automated feeding systems, and real-time monitoring solutions enable producers to optimize feed efficiency and reduce costs, enhancing overall productivity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 375.00 Billion |

| Market Size in 2026 | USD 396.75 Billion |

| Market Size in 2031 | USD 525.95 Billion |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ingredient Type Insights

The ingredient type segment remains the structural backbone of the global feed ingredients market, with cereals and grains continuing to dominate due to their fundamental role in livestock nutrition and energy supply. In 2025, cereals and grains account for approximately 42% of the global market share, reflecting their indispensable position in feed formulations across all major livestock categories. Corn, in particular, stands out as the most widely utilized ingredient globally, owing to its superior calorific value, digestibility, and consistent availability across key agricultural economies. The scalability of corn production in major exporting countries, combined with its cost-effectiveness, reinforces its dominance and ensures its continued preference among feed manufacturers.Alternative proteins, while currently representing a smaller share of the market, are gaining increasing attention due to rising sustainability concerns and the need to reduce dependence on conventional protein sources. Innovations in feed technology, including insect-based protein, algae-derived ingredients, and fermentation-based solutions, are gradually reshaping the ingredient landscape. These alternatives offer promising benefits such as lower environmental impact, reduced land and water usage, and enhanced nutrient efficiency. As regulatory frameworks evolve and production costs decrease, alternative proteins are expected to play a more prominent role in the long-term transformation of the feed ingredients market.The leading driver within the ingredient segment remains the growing demand for cost-efficient, nutritionally optimized feed formulations that can support high-performance livestock production. This demand is being fueled by rising global consumption of animal protein, increasing pressure on farmers to improve productivity, and the need to balance profitability with sustainability. As a result, ingredient innovation, supply chain optimization, and technological advancements in feed formulation are becoming critical factors shaping the competitive dynamics of this segment.

Livestock Insights

The livestock segment provides a comprehensive view of demand distribution across different animal categories, with poultry emerging as the dominant segment, accounting for approximately 38% of the global market share. The strong position of poultry is primarily attributed to its relatively short production cycles, high feed conversion efficiency, and widespread consumer acceptance across diverse cultural and economic contexts. Poultry meat is often more affordable compared to other animal proteins, making it a preferred choice in both developed and developing markets, thereby driving consistent demand for feed ingredients tailored to poultry nutrition.The swine segment continues to contribute significantly to the overall market, particularly in regions with high pork consumption. Meanwhile, the pet food segment is experiencing notable growth, driven by rising pet ownership, increasing humanization of pets, and growing demand for premium and specialized nutrition products. These trends are encouraging the development of high-quality, customized feed solutions that cater to specific dietary requirements and health conditions.The primary driver within the livestock segment is the increasing global demand for animal protein, which is directly linked to population growth, urbanization, and rising disposable incomes. As consumers seek higher-quality and more diverse protein sources, livestock producers are under pressure to enhance productivity and efficiency, thereby driving sustained demand for advanced feed ingredients and nutritional solutions.

Distribution Channel Insights

The distribution channel landscape is characterized by the dominance of direct sales to feed manufacturers, which account for over 55% of total distribution. This dominance is largely driven by the operational efficiencies associated with bulk procurement, including cost savings, supply consistency, and better quality control. Large-scale feed producers and integrated livestock operations prefer direct sourcing arrangements as they enable long-term contracts, stable pricing, and improved traceability of raw materials.Integrated livestock farms are increasingly adopting direct sourcing models, reflecting a broader trend toward vertical integration within the industry. By controlling multiple stages of the production process, from feed procurement to livestock rearing and product distribution, these operations can achieve greater efficiency, reduce dependency on external suppliers, and enhance overall profitability.Digitalization and supply chain modernization are also beginning to influence distribution dynamics, with the adoption of online procurement platforms, data-driven inventory management, and real-time tracking systems. These advancements are improving transparency, reducing lead times, and enabling more responsive supply chain operations.The leading driver in this segment is the growing emphasis on supply chain efficiency and cost optimization. As feed ingredient prices remain subject to volatility due to factors such as climate change, trade policies, and geopolitical developments, stakeholders are increasingly prioritizing streamlined distribution channels that can ensure reliability, affordability, and scalability.

End-Use Insights

The end-use segment highlights the diverse applications of feed ingredients across various industries, with the poultry sector emerging as the largest contributor. With a global market size exceeding USD 300 billion, the poultry industry generates substantial demand for feed ingredients, driven by its scale, efficiency, and widespread consumer demand. The need for high-performance feed formulations that can support rapid growth and optimal health in poultry continues to drive innovation and investment in this segment.Aquaculture stands out as the fastest-growing end-use industry, supported by a CAGR above 7%. The increasing global appetite for seafood, coupled with the expansion of export-oriented fish farming operations, is fueling demand for specialized aquafeed formulations. These feeds are designed to meet the specific nutritional requirements of different species, ensuring optimal growth, feed conversion, and disease resistance.The dairy and beef industries maintain steady demand for feed ingredients, particularly in regions with established livestock sectors. In these industries, feed quality plays a critical role in determining product yield, quality, and profitability. As a result, there is a growing focus on precision nutrition and the use of advanced feed additives to enhance performance outcomes.Emerging applications in pet food and specialty livestock feed are also contributing to market expansion, particularly in developed economies. The increasing trend toward premiumization, along with rising awareness of animal health and nutrition, is driving demand for high-quality, functional, and customized feed solutions.The primary driver in the end-use segment is the continuous expansion of the global animal protein industry, supported by demographic and economic trends. As consumer preferences evolve and demand for high-quality protein sources increases, end-use industries are investing in advanced feed solutions to enhance productivity, sustainability, and product quality.

Explore more data points, trends and opportunities Download Free Sample Report

Animal Feed Ingredients Market Segmentations

By Ingredient Type

- Cereals & Grains

- Oilseed Meals & Cakes

- Animal-Based Ingredients

- Feed Additives

- Forage & Roughage

- Alternative Proteins

By Livestock Type

- Poultry

- Ruminants

- Swine

- Aquaculture

- Pets

- Others

By Form

- Dry

- Liquid

By Function

- Energy Sources

- Protein Sources

- Health Enhancers

- Digestibility Enhancers

- Palatability Enhancers

By Distribution Channel

- Direct Sales

- Distributors & Traders

- Integrated Livestock Farms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global feed ingredients market, accounting for approximately 42% of the market share in 2025. The region's leadership is underpinned by its large and rapidly growing population, rising income levels, and increasing consumption of animal protein. China remains the largest contributor, driven by its extensive pork and poultry industries, which require substantial volumes of feed inputs. The country's ongoing efforts to modernize its livestock sector and improve biosecurity measures are further supporting market growth.Key drivers in the Asia-Pacific region include rapid urbanization, rising middle-class population, increasing demand for affordable protein sources, and strong government support for agricultural and aquaculture development. Additionally, the growing adoption of modern farming practices and feed technologies is contributing to improved efficiency and productivity across the region.

North America

North America holds approximately 24% of the global market share, with the United States serving as the primary contributor. The region benefits from highly advanced agricultural infrastructure, widespread adoption of modern farming practices, and strong integration across the feed and livestock value chain. The presence of major feed manufacturers and technology providers further enhances the region's competitive position.Regional growth is driven by technological innovation, high productivity standards, strong research and development capabilities, and increasing demand for premium and sustainable animal products. The emphasis on precision nutrition and data-driven farming practices is also contributing to the evolution of the market in this region.

Europe

Europe accounts for nearly 20% of the global feed ingredients market, characterized by stringent quality standards, regulatory frameworks, and a strong focus on sustainability. Countries such as Germany, France, and the Netherlands are leading contributors, supported by well-established livestock industries and advanced feed production capabilities.The region places significant emphasis on environmental sustainability, animal welfare, and food safety, which influences the composition and sourcing of feed ingredients. The increasing adoption of alternative proteins and eco-friendly feed solutions reflects the region's commitment to reducing the environmental impact of livestock production.Growth drivers in Europe include regulatory support for sustainable practices, rising demand for high-quality animal products, increasing consumer awareness, and continuous innovation in feed technology. The region's focus on reducing antibiotic usage and promoting natural growth enhancers is also shaping market trends.

Latin America

Latin America is a key player in the global feed ingredients market, with countries such as Brazil and Argentina serving as major exporters of meat and animal products. The region benefits from abundant agricultural resources, favorable climatic conditions, and competitive production costs, which support large-scale livestock farming.The expansion of poultry and beef production, driven by strong export demand, is a major factor contributing to the growth of the feed ingredients market in this region. Additionally, increasing investments in agricultural infrastructure and feed production capacity are enhancing the region's competitiveness.Key growth drivers include expanding export markets, rising global demand for protein, availability of raw materials, and government support for agricultural development. The region's ability to scale production efficiently positions it as a critical supplier in the global food supply chain.

Middle East & Africa

The Middle East & Africa region is the fastest-growing market, with growth rates exceeding 6.5%. This growth is driven by increasing investments in food security, rising demand for animal protein, and the gradual development of the livestock sector. Countries such as Saudi Arabia, South Africa, and Nigeria are leading the expansion, supported by government initiatives and private sector investments.The region's reliance on imports for feed ingredients presents both challenges and opportunities, encouraging the development of local production capabilities and supply chain infrastructure. Efforts to enhance self-sufficiency in food production are driving demand for high-quality feed inputs and modern farming practices.Major growth drivers include population growth, urbanization, increasing income levels, government support for food security, and the expansion of commercial livestock farming. The adoption of advanced feed technologies and the establishment of integrated farming systems are expected to further accelerate market growth in the coming years.

Key Players in the Animal Feed Ingredients Market

- Cargill Inc.

- Archer Daniels Midland Company

- Bunge Limited

- Louis Dreyfus Company

- Alltech Inc.

- Nutreco N.V.

- Land O’Lakes Inc.

- ForFarmers N.V.

- Charoen Pokphand Foods

- DSM-Firmenich

- BASF SE

- Evonik Industries AG

- Kemin Industries

- Adisseo

- Novus International