Bird Food Market Size

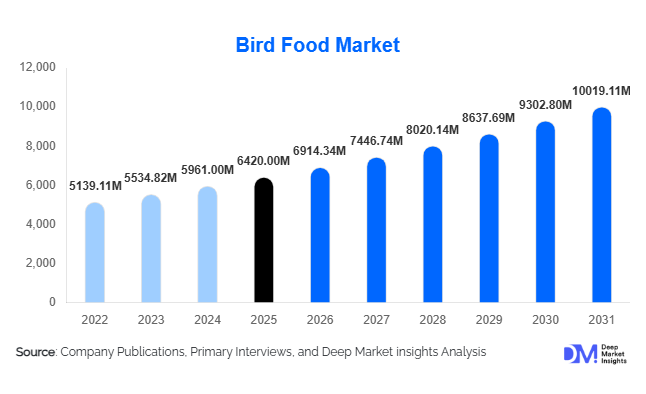

According to Deep Market Insights, the global bird food market size was valued at USD 6,420 million in 2025 and is projected to grow from USD 6,914.34 million in 2026 to reach USD 10,019.11 million by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The market expansion is primarily driven by increasing pet bird ownership, rising consumer awareness regarding avian nutrition, and the growing popularity of backyard bird feeding activities across developed and emerging economies. Market size estimates are derived using averaged industry benchmarks with a calculated variance range to reflect realistic global valuation trends.

Key Market Insights

- Premium and nutritionally fortified bird food products are gaining traction, supported by rising pet humanization trends and veterinary-backed feeding practices.

- Backyard bird feeding culture is expanding globally, especially across North America and Europe, boosting demand for seed blends and specialty feeds.

- Asia-Pacific is emerging as the fastest-growing consumption region, driven by urban pet adoption and rising disposable incomes.

- E-commerce channels are reshaping distribution, allowing niche brands and specialty formulations to reach global consumers.

- Sustainability-driven sourcing, including organic seeds and eco-friendly packaging, is becoming a key differentiator among manufacturers.

- Functional nutrition trends, including immune-support and molting-support formulas, are accelerating product innovation.

What are the latest trends in the bird food market?

Shift Toward Functional and Species-Specific Nutrition

Bird food manufacturers are increasingly developing species-specific diets tailored to parrots, finches, canaries, cockatiels, and wild birds. Consumers are moving away from generic seed mixes toward scientifically balanced formulations enriched with vitamins, minerals, probiotics, and amino acids. Functional formulations designed for feather health, digestion improvement, and immunity enhancement are witnessing strong adoption. Veterinary recommendations and educational campaigns are influencing purchasing behavior, encouraging long-term subscription-based feeding models.

Growth of Backyard Bird Feeding and Wildlife Engagement

The growing interest in wildlife conservation and nature engagement has accelerated backyard bird feeding trends globally. Urban households are investing in feeders, bird-friendly gardens, and seasonal feed variations to attract migratory species. This trend surged after lifestyle shifts toward home-based recreation and continues to expand as consumers seek mental wellness through nature interaction. Seasonal demand cycles—particularly winter feeding in colder climates—are creating predictable consumption patterns for manufacturers and retailers.

What are the key drivers in the bird food market?

Rising Pet Bird Ownership and Companion Animal Trends

Pet birds are increasingly viewed as low-maintenance companion animals suitable for urban living environments. Smaller housing spaces and rising apartment living favor birds over larger pets. Countries across Asia and Latin America are witnessing growing adoption of parrots, budgerigars, and ornamental birds, driving steady demand for packaged feed products. Increasing awareness of balanced nutrition further supports premium product uptake.

Expansion of Premiumization and Specialized Feed Products

Consumers are willing to spend more on high-quality bird food products that promise improved longevity and health outcomes. Organic seed blends, non-GMO grains, and fortified pellet diets are gaining market share. Premium offerings also benefit from branding strategies emphasizing sustainability, traceability, and veterinary validation.

Growth of Online Retail and Subscription Feeding Models

E-commerce platforms have transformed accessibility to bird food products. Direct-to-consumer brands now offer automated delivery subscriptions, personalized feeding recommendations, and bundled feeding accessories. Digital retail expansion enables global brands to penetrate emerging markets without heavy physical infrastructure investments.

What are the restraints for the global market?

Volatility in Raw Material Prices

Bird food production heavily depends on agricultural commodities such as sunflower seeds, millet, corn, and safflower. Climate variability, supply chain disruptions, and fluctuating agricultural yields directly impact production costs and profit margins. Manufacturers often face challenges maintaining price stability while preserving product quality.

Regulatory Compliance and Quality Standardization

Pet food safety regulations vary significantly across regions, requiring extensive labeling compliance and nutritional testing. Smaller manufacturers may struggle with certification costs, slowing innovation and market entry in highly regulated markets such as Europe and North America.

What are the key opportunities in the bird food industry?

Emerging Market Expansion

Rapid urbanization in India, Southeast Asia, and Latin America presents substantial growth opportunities. Rising disposable incomes and expanding middle-class populations are increasing pet ownership rates. Localization of feed blends tailored to regional bird species offers strong market entry potential.

Integration of Sustainable and Organic Feed Solutions

Eco-conscious consumers increasingly prefer sustainably sourced ingredients and recyclable packaging. Companies investing in regenerative agriculture sourcing and carbon-neutral production processes are expected to capture premium market segments.

Technology-Driven Smart Feeding Ecosystems

Integration of IoT-enabled feeders, AI-based feeding recommendations, and mobile monitoring applications creates opportunities for ecosystem-based revenue models. Data-driven feeding solutions can encourage recurring purchases and enhance customer loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6420 Million |

| Market Size in 2026 | USD 6914.34 Million |

| Market Size in 2031 | USD 10019.11 Million |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global bird food market is characterized by a diverse range of product types, with seed mixes dominating approximately 42% of the market share by 2025. Seed mixes remain highly popular due to their affordability, versatility, and adaptability for both pet and wild bird consumption. They provide essential macronutrients and allow consumers to feed multiple species without tailoring specialized diets, making them particularly appealing for cost-conscious households and large-scale aviary operations. Moreover, the convenience of mixed seeds contributes to their widespread adoption, especially in regions with established backyard bird feeding cultures, such as North America and Europe.Pellet-based nutrition represents the fastest-growing product category. These feeds are increasingly recommended by veterinarians and avian nutritionists due to their scientifically formulated, balanced nutrient profiles. Unlike selective seed feeding, pellets ensure that birds receive all essential vitamins, minerals, and amino acids, reducing the risk of malnutrition and selective feeding behaviors. The rising awareness among pet owners about avian health and longevity is driving growth in this segment, particularly in regions with high urban pet ownership like North America, Europe, and parts of Asia-Pacific.Treats and dietary supplements are also witnessing strong expansion. Premiumization trends, coupled with increasing engagement between owners and pets, encourage the purchase of specialized treats designed for behavioral enrichment, training, and nutritional supplementation. Health-focused supplements, fortified with probiotics, vitamins, and antioxidants, appeal to a growing segment of informed consumers who seek to optimize the overall well-being of their birds.In addition, organic and fortified feeds are gaining traction globally, driven by a shift toward health-conscious consumption and demand for ingredient transparency. Consumers are increasingly scrutinizing product labels for chemical-free, ethically sourced, and non-GMO ingredients. This trend is most pronounced in Western Europe, North America, and emerging affluent urban centers in Asia-Pacific, where organic certification and premium branding are influential in purchase decisions. Manufacturers are responding by launching organic seed mixes, enriched pellets, and specialized supplements, further diversifying the product portfolio and reinforcing brand differentiation.

Application Insights

Pet bird feeding remains the largest application segment, accounting for nearly 58% of global demand in 2025. The surge in pet bird ownership worldwide is driven by urbanization, increasing disposable incomes, and the growing perception of birds as companion animals. Small parrot species, finches, canaries, and exotic birds are particularly popular in urban households, creating steady demand for both standard and premium feed products.Wild bird feeding, while seasonal, constitutes a significant portion of regional demand, particularly in North America and Europe, where backyard birdwatching is a popular recreational activity. Bird feeders, seed stations, and community feeding programs contribute to predictable seasonal spikes in product sales, especially during winter months when natural food sources are scarce. Environmental awareness and wildlife conservation campaigns amplify this trend by promoting responsible feeding practices, which often include specialized seed mixes and nutrient-enriched blends to support local avian populations.Aviaries and breeding centers represent a stable institutional segment. Commercial breeding facilities, conservation programs, and educational aviaries purchase feeds in bulk and require standardized, high-quality formulations to ensure consistent growth, reproduction, and health. This segment is characterized by long-term contracts and predictable procurement patterns, offering manufacturers a reliable revenue stream and incentivizing investment in product innovation and nutritional research.

Distribution Channel Insights

Offline retail channels, including pet specialty stores, supermarkets, and hypermarkets, accounted for approximately 55% of global sales in 2025. These channels remain preferred for consumers who value in-store product comparison, personalized recommendations from store personnel, and the tactile evaluation of feed quality. Traditional retail dominance is particularly evident in Europe and North America, where well-established retail infrastructures and widespread urban availability reinforce consumer loyalty.Online retail is the fastest-growing distribution channel due to the convenience, broader product availability, and innovative subscription models. E-commerce platforms allow consumers to access niche products, including premium organic feeds, exotic seed mixes, and customized formulations, which may not be readily available in physical stores. Direct-to-consumer brand websites also increasingly capture premium buyers by offering exclusive blends, loyalty programs, and personalized nutrition advice. In Asia-Pacific, rapid digital adoption and increasing internet penetration are accelerating online sales, making e-commerce a strategic focus for market players targeting urban, tech-savvy consumers.

End-Use Insights

Household consumers dominate the global bird food market, representing nearly 70% of total consumption. Rising interest in pet ownership, coupled with changing lifestyles that emphasize home-based companionship, continues to drive demand. Bird owners are investing in higher-quality nutrition, behavioral enrichment, and specialized supplements, reflecting a willingness to pay premium prices for products that enhance avian health and longevity.Commercial aviaries and breeding facilities are witnessing faster growth rates due to the expanding ornamental bird trade, conservation programs, and the emergence of boutique bird farms. Facilities catering to exotic species and endangered bird conservation require scientifically formulated feeds that support breeding success and overall health, generating steady demand for specialized and premium products. Additionally, cross-border trade in specialty bird foods is on the rise, as Europe and North America import high-quality blends from Asia and Latin America to meet niche market requirements.The growth of the global pet care industry, projected to expand above 6% annually, further supports bird food consumption. Integrated pet nutrition solutions, cross-selling of related products, and bundled offerings enhance household spending on bird foods. Manufacturers are leveraging brand synergies across multiple pet categories to capitalize on rising consumer engagement and premiumization trends.

Explore more data points, trends and opportunities Download Free Sample Report

Bird Food Market Segmentations

By Product Type

- Seed Mixes

- Pellet-Based Feed

- Treats & Supplements

- Organic & Fortified Bird Feed

By Application

- Pet Bird Feeding

- Wild Bird Feeding

- Aviaries & Breeding Centers

By Distribution Channel

- Online Retail

- Pet Specialty Stores

- Supermarkets & Hypermarkets

- Direct-to-Consumer

By End Use

- Household Consumers

- Commercial Aviaries

- Bird Breeders

- Wildlife Conservation Organizations

Regional Insights

North America

North America held approximately 34% of the global bird food market in 2025, with the United States leading due to the deeply entrenched cultural practice of backyard bird feeding. High levels of disposable income, strong pet ownership rates, and advanced retail infrastructure sustain the region’s market dominance. Seasonal feeding patterns, environmental awareness campaigns, and widespread availability of diverse feed types—including organic, fortified, and pellet-based options—further enhance demand. Canada also contributes significantly, with a focus on wild bird feeding during colder months and urban pet bird ownership in metropolitan areas. Growth drivers include increasing urbanization, eco-tourism, and the rising trend of pet humanization, which encourages owners to invest in premium and nutritionally balanced bird foods.

Europe

Europe accounted for nearly 27% of global market share, with Germany, the United Kingdom, France, and the Netherlands as leading consumers. Environmental consciousness and active wildlife conservation initiatives strongly influence purchasing patterns. Consumers in Western Europe show high adoption of organic and fortified bird food products, driven by increasing awareness of avian health and sustainability. The rising popularity of exotic and companion birds in urban households, coupled with strong retail networks and e-commerce growth, supports consistent demand. Key regional growth drivers include government-backed wildlife protection programs, increasing participation in birdwatching activities, and consumer preference for ethically sourced, chemical-free feed ingredients. Additionally, regulatory standards promoting labeling transparency and quality control reinforce consumer trust and willingness to pay a premium for trusted brands.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the bird food market, driven by countries such as China, India, Japan, and Australia. Rapid urbanization, expanding middle-class populations, and rising disposable incomes are propelling pet bird adoption and household spending on premium feeds. Urban dwellers increasingly consider birds as companion animals, elevating demand for scientifically formulated pellets, supplements, and enrichment treats. India and China together are projected to contribute over 35% of incremental demand by 2031. Growth is supported by the increasing availability of modern retail channels, e-commerce penetration, and marketing campaigns emphasizing bird health and wellness. Additionally, cultural affinity for birds in certain Asian societies—such as songbirds in China or ornamental birds in India—fosters continued interest in specialized feeds, while governmental regulations on animal welfare and food safety further boost consumer confidence.

Middle East & Africa

The Middle East and Africa region demonstrates strong niche demand, with the UAE and Saudi Arabia leading in ornamental bird ownership. Falconry traditions in the Gulf countries support a market for premium feeds specifically designed for raptors and exotic species. In South Africa, wild bird feeding adoption is on the rise, driven by eco-tourism initiatives, community bird conservation programs, and a growing middle class interested in sustainable leisure activities. Regional growth is fueled by high disposable incomes in urban centers, investment in luxury pet care, and cultural significance of birds in recreational and sporting contexts. Additionally, increasing participation in environmental awareness campaigns and wildlife conservation contributes to rising demand for fortified and nutritionally complete feeds.

Latin America

Brazil and Mexico dominate bird food consumption in Latin America, supported by growing pet ownership and increasing penetration of modern retail channels. Strong regional production capabilities in seed crops enable competitive pricing for both domestic and export markets. Urbanization and rising awareness about pet health are key drivers, along with cultural affinity for birds in household and outdoor environments. Latin American consumers are increasingly adopting pellet-based feeds and nutritional supplements for companion birds, while bulk seed mixes continue to serve rural and semi-urban populations. Additional factors driving growth include government initiatives to promote domestic agricultural production, improved logistics networks enhancing product availability, and regional trade agreements facilitating cross-border supply chains.

Key Players in the Bird Food Market

- Mars Incorporated

- Vitakraft Pet Care GmbH & Co. KG

- Kaytee Products Inc.

- Spectrum Brands Holdings Inc.

- ZuPreem

- Harrison’s Bird Foods

- Roudybush Inc.

- Versele-Laga NV

- Brown’s Pet Nutrition

- Pretty Bird International

- Witte Molen

- Lafeber Company

- Volkman Seed Factory

- Higgins Premium Pet Foods

- TRIXIE Heimtierbedarf GmbH