Frozen and Freeze-Dried Pet Food Market Size

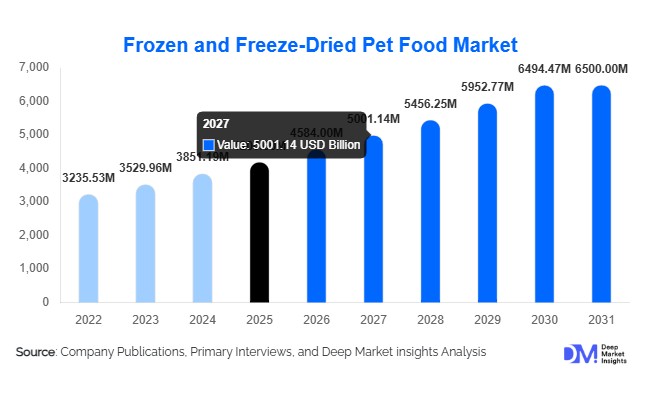

According to Deep Market Insights, the global frozen and freeze-dried pet food market size was valued at USD 4,200 million in 2026 and is projected to grow from USD 4,584 million in 2027 to reach USD 6,500 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing pet humanization, rising demand for biologically appropriate raw diets, and the rapid expansion of premium and subscription-based pet nutrition models. Freeze-dried formats are gaining strong traction due to their convenience, long shelf life, and ability to retain nutritional integrity, while frozen pet food continues to appeal to consumers seeking minimally processed, fresh feeding alternatives.

Key Market Insights

- Freeze-dried complete meals dominate premium adoption, supported by long shelf stability, portability, and global distribution efficiency.

- Dogs remain the primary consumer segment, accounting for the highest per-pet consumption volume globally.

- North America leads global demand, driven by strong raw feeding culture and high pet healthcare spending.

- Asia-Pacific is the fastest-growing region, supported by rising disposable income and increasing pet adoption rates.

- E-commerce and subscription models are reshaping distribution, enabling direct-to-consumer personalized pet nutrition delivery.

- Clean-label, high-protein, and grain-free formulations are becoming standard expectations among premium pet owners.

What are the latest trends in the frozen and freeze-dried pet food market?

Premiumization and Humanization of Pet Diets

Pet owners increasingly view pets as family members, driving demand for premium nutrition formats such as frozen raw meals and freeze-dried diets. Consumers are prioritizing high-protein, minimally processed, and functional ingredients that closely resemble human-grade food standards. This has led to strong growth in biologically appropriate raw food (BARF) diets and clean-label formulations. Brands are responding by introducing novel proteins, grain-free recipes, and veterinary-formulated blends targeting specific health needs such as digestion, skin health, and weight management.

Expansion of Direct-to-Consumer Subscription Models

Subscription-based delivery systems are transforming the pet food industry. Companies are leveraging data-driven personalization to design customized meal plans based on breed, age, weight, and health conditions. These models ensure recurring revenue while improving customer retention. Cold-chain logistics advancements now enable frozen pet food delivery directly to households, expanding access in urban markets. This trend is also encouraging smaller premium brands to scale globally without relying heavily on traditional retail distribution networks.

Technological Advancements in Preservation and Packaging

Freeze-drying technology innovations, vacuum sealing, and advanced cold-chain systems are improving product shelf life and reducing spoilage risks. Smart packaging solutions with temperature indicators and freshness tracking are enhancing consumer trust. These advancements are enabling manufacturers to expand exports and penetrate emerging markets where cold storage infrastructure was previously limited.

What are the key drivers in the frozen and freeze-dried pet food market?

Rising Pet Humanization and Premium Nutrition Demand

The increasing emotional bond between pet owners and pets is driving higher spending on premium nutrition products. Owners are shifting away from traditional kibble toward fresh, raw, and freeze-dried diets perceived as healthier and more natural. This trend is particularly strong among urban households and millennial pet owners who prioritize wellness-oriented pet care.

Growth in Raw and Minimally Processed Feeding Trends

Awareness of the benefits of high-protein, minimally processed diets is fueling demand for frozen and freeze-dried pet food. These products preserve natural nutrients without artificial preservatives, making them highly attractive to health-conscious consumers. Veterinary endorsements and online education platforms are further accelerating adoption globally.

Expansion of E-commerce and Pet Food Delivery Ecosystems

The rapid growth of online retail channels and subscription platforms is significantly boosting market accessibility. Consumers can now access a wide range of premium frozen and freeze-dried products through digital platforms. This has reduced geographical barriers and enabled niche brands to scale quickly across international markets.

What are the restraints for the global market?

High Production and Cold-Chain Costs

Frozen and freeze-dried pet food requires advanced processing technologies and temperature-controlled logistics, resulting in high operational costs. These costs translate into premium retail pricing, limiting adoption among price-sensitive consumers and restricting mass-market penetration.

Regulatory and Food Safety Compliance Challenges

Strict regulations governing raw meat handling, microbial safety, and international pet food standards increase compliance complexity for manufacturers. Varying regulations across regions create additional barriers for global expansion and increase certification costs for exporters.

What are the key opportunities in the frozen and freeze-dried pet food industry?

Expansion of Veterinary Therapeutic Diets

The growing prevalence of pet obesity, allergies, and digestive disorders is creating strong demand for veterinary-recommended frozen and freeze-dried therapeutic diets. These specialized formulations offer high-margin opportunities for manufacturers and are increasingly being distributed through veterinary clinics and pet hospitals.

Emergence of Novel Protein and Functional Nutrition Products

There is rising demand for alternative protein sources such as duck, venison, rabbit, and insect-based formulations. These ingredients help address allergy concerns while supporting sustainability goals. Functional nutrition products enriched with probiotics, omega fatty acids, and joint-support ingredients are also gaining traction.

Expansion into Emerging Markets

Rapid urbanization and rising disposable income in Asia-Pacific, Latin America, and parts of the Middle East are opening new growth avenues. As pet ownership increases in these regions, demand for premium pet nutrition is expected to grow significantly, especially in urban centers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4200 Million |

| Market Size in 2026 | USD 4584 Million |

| Market Size in 2031 | USD 6500 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen and freeze-dried pet food market is strongly shaped by evolving consumer preferences toward minimally processed, nutrient-dense, and biologically appropriate diets for companion animals. Within this landscape, freeze-dried complete meals represent the most dominant product category, accounting for approximately 34% of the total market share. The leading growth driver for this segment is the increasing willingness of pet owners to invest in premium, convenience-oriented nutrition solutions that closely replicate raw feeding benefits without the logistical challenges of refrigeration or spoilage. Freeze-dried complete meals offer extended shelf stability, lightweight portability, and ease of storage, making them especially attractive to urban households and frequent travelers. Additionally, growing awareness of pet obesity and chronic health issues has accelerated demand for balanced formulations that preserve natural nutrients while eliminating artificial preservatives.Freeze-dried treats and meal toppers represent one of the fastest-growing sub-segments within the product category, driven by increasing humanization of pets and the rising trend of functional snacking. Veterinary prescription frozen diets form a high-value but relatively niche category, with growth driven primarily by the increasing prevalence of pet chronic diseases such as kidney disorders, obesity, diabetes, and gastrointestinal sensitivities. Veterinary professionals are playing an increasingly influential role in shaping dietary decisions, and prescription-based nutrition is becoming an integral part of preventive and therapeutic animal healthcare. Hybrid formats combining frozen and freeze-dried components are also emerging, supported by innovation in pet nutrition science. These hybrid offerings are driven by demand for dietary variety and functional customization, particularly among premium pet owners seeking tailored feeding solutions that balance convenience with nutritional optimization.

Pet Type Insights

Dogs dominate the global market with approximately 62% share, primarily due to their higher consumption volume, larger population base in urban households, and stronger emotional bonding with owners, which translates into higher spending on premium nutrition. The key driver for this segment is the rapid humanization of dogs, where pets are increasingly viewed as family members, leading to greater willingness to invest in high-quality, functional, and premium food products. The expansion of specialized dog diets addressing breed-specific, age-specific, and health-specific requirements further reinforces this dominance. Additionally, dogs have higher caloric needs than other companion animals, directly influencing overall market volume consumption.Cats represent a rapidly expanding segment, driven by increasing urbanization and lifestyle shifts that favor low-maintenance pets. The primary growth driver for the cat segment is the rising adoption of cats in apartment-based living environments, especially in densely populated cities where space constraints limit dog ownership. Cat owners are increasingly seeking premium nutrition solutions focused on urinary health, weight management, and digestive sensitivity, contributing to growing demand for specialized frozen and freeze-dried formulations. Furthermore, increasing awareness of feline dietary sensitivities is encouraging owners to shift from conventional dry food to minimally processed alternatives.Other companion animals, including small mammals, birds, and exotic pets, account for a smaller but steadily growing market share. The key driver for this segment is the diversification of pet ownership globally, particularly among younger demographics seeking unconventional pets. Although consumption volumes remain limited compared to dogs and cats, the segment is witnessing gradual expansion due to rising availability of specialized nutritional products. Manufacturers are increasingly exploring niche formulations to cater to exotic species, which is expected to support long-term incremental growth in this category.

Distribution Channel Insights

E-commerce platforms dominate global distribution, accounting for nearly 41% of total sales, and are expected to maintain their leadership position throughout the forecast period. The primary driver of this segment is the convenience of online purchasing combined with the expansion of subscription-based delivery models that ensure consistent supply of frozen and freeze-dried pet food. Digital platforms also provide consumers with extensive product variety, transparent ingredient information, and easy price comparison, which significantly enhances purchasing confidence. The integration of cold-chain logistics and last-mile delivery innovations has further strengthened the viability of online frozen pet food sales.Pet specialty stores continue to play a crucial role in the market, particularly in premium product discovery and consumer education. The main driver of this channel is the trust factor associated with in-store expert guidance, where trained staff assist pet owners in selecting appropriate dietary solutions based on pet health and nutritional needs. These stores also serve as key touchpoints for new product launches and brand visibility, particularly for premium and niche offerings.Supermarkets and hypermarkets continue to serve mass-market consumers, particularly in developing regions, driven by accessibility and impulse purchasing behavior. Direct-to-consumer brands are also expanding rapidly, leveraging digital engagement strategies and personalized subscription models that enhance customer retention and brand loyalty. These channels collectively contribute to a highly diversified distribution ecosystem.

End-Use Insights

Household pet owners represent the largest end-use segment, driven by the global rise in pet ownership and increasing expenditure on premium pet nutrition. The key driver for this segment is the emotional humanization of pets, which has fundamentally transformed purchasing behavior from basic sustenance feeding to wellness-oriented nutrition planning. Pet owners are increasingly prioritizing high-quality ingredients, functional health benefits, and long-term well-being outcomes, which is fueling sustained demand for frozen and freeze-dried diets.Veterinary clinics represent the fastest-growing institutional segment, supported by the expanding role of veterinarians in preventive healthcare and dietary management. The main driver is the rising incidence of pet health conditions that require specialized nutritional interventions. Veterinary professionals are increasingly prescribing therapeutic diets as part of holistic treatment plans, which is accelerating demand for medically formulated frozen pet food products.Pet boarding facilities and premium pet care centers are also contributing to market growth by offering high-quality, ready-to-serve frozen meals. The key driver in this segment is the growing expectation of continuity in premium nutrition even during temporary pet stays outside the home. As pet care services become more sophisticated, nutrition is being integrated into overall care experiences, further strengthening demand across institutional channels.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen and Freeze-Dried Pet Food Market Segmentations

By Product Type

- Frozen Raw Pet Food

- Frozen Cooked Pet Food

- Freeze-Dried Complete Meals

- Freeze-Dried Treats & Meal Toppers

- Frozen Veterinary / Prescription Diets

By Pet Type

- Dogs

- Cats

- Others

By Ingredient Type

- Animal-Based

- Novel Protein-Based

- Mixed Protein Formulations

- Plant-Augmented Hybrid Recipes

By Distribution Channel

- Pet Specialty Stores

- Supermarkets & Hypermarkets

- Online Retail

- E-commerce Platforms

- Veterinary Clinics

- Direct-to-Consumer Subscription Models

By Form

- Bulk Frozen Packs

- Single-Serve Frozen Portions

- Freeze-Dried Pouches

- Hybrid Meal Kits

Regional Insights

North America

North America leads the global market with approximately 38% share, driven by deeply entrenched pet humanization trends, high disposable income levels, and widespread acceptance of premium and raw feeding diets. The United States remains the dominant contributor, supported by a mature pet food industry, strong brand penetration, and highly developed cold-chain infrastructure. The primary growth driver in this region is the increasing shift toward health-focused pet nutrition, where consumers actively seek clean-label, minimally processed, and functional diets. Additionally, high awareness of pet obesity and chronic diseases has further accelerated demand for scientifically formulated frozen and freeze-dried meals. The presence of established e-commerce ecosystems and subscription-based pet food services continues to reinforce market expansion.

Europe

Europe accounts for approximately 27% of the global market, with strong contributions from Germany, the United Kingdom, and France. The key driver in this region is the growing consumer preference for natural, organic, and ethically sourced pet food products. Strict regulatory frameworks promoting transparency, sustainability, and clean-label ingredients have significantly influenced product innovation and adoption patterns. European consumers are highly sensitive to environmental sustainability, which has led to increased demand for responsibly sourced proteins and eco-friendly packaging in frozen and freeze-dried pet food categories. Additionally, the rising adoption of premium pet nutrition as part of preventive healthcare practices continues to strengthen market penetration.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, and increasing pet adoption across China, India, Japan, and South Korea. The leading growth driver is the expanding middle-class population that is increasingly adopting companion animals and investing in premium pet care products. Changing lifestyle patterns, coupled with growing awareness of pet health and nutrition, are significantly accelerating demand for frozen and freeze-dried diets. The expansion of e-commerce platforms across the region has played a crucial role in improving accessibility to premium international brands, particularly in urban centers. Additionally, increasing influence of Western pet care trends is reshaping dietary preferences across the region.

Latin America

Latin America is experiencing steady but gradual market growth, primarily driven by Brazil and Mexico. The key driver in this region is the increasing urban pet population combined with rising awareness of pet health and wellness. As disposable incomes grow in urban centers, consumers are gradually shifting from conventional pet food products toward premium nutrition options. However, market penetration remains concentrated among affluent households due to higher price sensitivity in broader consumer segments. The expansion of retail infrastructure and growing presence of international pet food brands are supporting gradual adoption of frozen and freeze-dried pet nutrition products.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential market, particularly driven by luxury pet ownership trends in the UAE and Saudi Arabia. The primary growth driver is the rising adoption of premium lifestyles among affluent populations, where pets are increasingly viewed as luxury companions requiring high-end care and nutrition. In Africa, growth is more gradual but steadily increasing, supported by urbanization and rising middle-class populations in countries such as South Africa and Kenya. However, the region remains highly import-dependent, which influences pricing and product availability. Despite these challenges, increasing awareness of pet wellness and expanding retail penetration are expected to support long-term market growth.

Key Players in the Global Market

- Nestlé Purina PetCare

- Mars Petcare

- Hill’s Pet Nutrition

- Freshpet

- Champion Petfoods

- Stella & Chewy’s

- Open Farm

- Primal Pet Foods

- The Honest Kitchen

- Instinct (Nature’s Variety)

- WellPet LLC

- Vital Essentials

- K9 Natural

- Blue Buffalo

- Addiction Foods