Direct Fed Microbials (DFM) Market Size

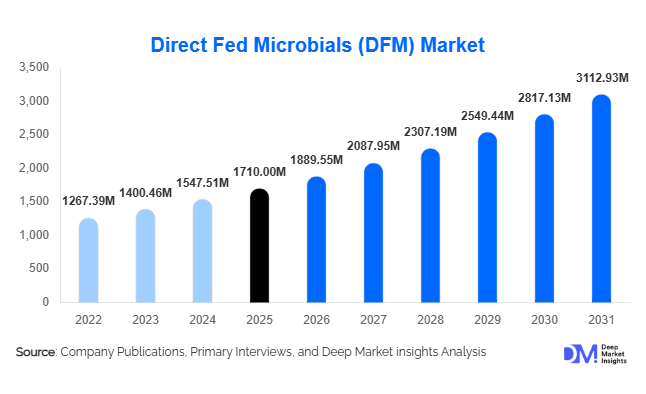

According to Deep Market Insights, the global direct fed microbials (DFM) market size was valued at USD 1,710 million in 2025 and is projected to grow from USD 1,890 million in 2026 to reach USD 3,120 million by 2031, expanding at a CAGR of 10.5% during the forecast period (2026–2031). The direct fed microbials market growth is primarily driven by increasing restrictions on antibiotic growth promoters, rising global demand for animal protein, and growing adoption of sustainable livestock nutrition solutions. DFMs are increasingly used to improve gut health, enhance feed conversion efficiency, and support immune performance across poultry, ruminants, swine, aquaculture, and companion animal production systems.

Key Market Insights

- Antibiotic-free livestock production is accelerating DFM adoption globally, as producers seek natural performance-enhancing feed additives.

- Poultry production remains the largest consumption segment, driven by intensive farming practices and high feed efficiency requirements.

- Asia-Pacific dominates global demand, supported by expanding livestock industries in China, India, and Southeast Asia.

- Aquaculture is emerging as the fastest-growing application, as DFMs help reduce disease outbreaks and improve feed utilization.

- Encapsulation and multi-strain microbial technologies are improving product stability and efficacy during feed processing.

- Integration of microbiome science and precision nutrition is transforming product innovation and premiumization strategies.

What are the latest trends in the direct fed microbials market?

Shift Toward Antibiotic Alternatives in Animal Nutrition

The global livestock industry is transitioning toward antibiotic-free production systems, significantly increasing demand for direct fed microbials. DFMs support gut microbiota balance and immune function, allowing producers to maintain productivity while complying with regulatory restrictions. Retailers and food brands increasingly require antibiotic-free labeling, encouraging integrators and feed manufacturers to incorporate microbial feed additives as standard nutritional components. This shift is particularly strong in poultry and swine production, where disease management and feed efficiency are critical performance factors.

Technology-Driven Microbial Formulations

Technological advancements are reshaping DFM product development. Encapsulation technologies enhance microbial survivability during pelleting and digestion, while genomic sequencing enables strain-specific formulation tailored to species and environmental conditions. Companies are investing in microbiome analytics, enabling precision nutrition models that optimize animal performance. Digital monitoring platforms now allow producers to measure feed efficiency improvements linked to microbial supplementation, strengthening return-on-investment validation and supporting premium product pricing.

What are the key drivers in the direct fed microbials market?

Rising Global Demand for Animal Protein

Growing populations and rising incomes in emerging economies are increasing consumption of poultry, dairy, pork, and seafood products. Producers are under pressure to maximize feed efficiency while controlling production costs. Direct fed microbials improve nutrient absorption and digestion efficiency, enabling measurable productivity gains and making them an attractive solution for commercial livestock operations worldwide.

Expansion of Sustainable Livestock Practices

Sustainability goals across the agriculture sector are encouraging adoption of biologically derived feed additives. DFMs help reduce digestive disorders, lower environmental waste outputs, and support methane reduction strategies in ruminants. Governments and food companies promoting ESG-aligned supply chains are increasingly supporting microbial nutrition solutions as part of climate-smart agriculture initiatives.

What are the restraints for the global market?

Variability in Performance Across Farming Conditions

The effectiveness of DFMs can vary depending on feed composition, climate, animal genetics, and farm management practices. This variability creates hesitation among smaller producers who require consistent performance outcomes before transitioning away from traditional additives.

Stability and Storage Challenges

Because DFMs contain live microorganisms, maintaining viability during processing, transportation, and storage remains technically challenging. Heat exposure during feed pelleting and improper storage conditions may reduce microbial effectiveness, increasing formulation complexity and production costs for manufacturers.

What are the key opportunities in the direct fed microbials industry?

Aquaculture Industry Expansion

Rapid growth in global aquaculture production presents major opportunities for DFM suppliers. Microbial solutions help control pathogens, improve digestion, and enhance survival rates in shrimp and fish farming. Export-driven seafood markets increasingly rely on DFMs to meet sustainability and antibiotic-free certification requirements, creating strong long-term demand potential.

Precision Nutrition and Customized Microbial Solutions

Advances in microbiome research allow companies to develop customized microbial blends tailored to specific livestock species and production environments. Precision nutrition models supported by data analytics enable higher-value offerings and recurring revenue models through integrated nutrition advisory services, opening new opportunities for innovation-driven market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1710 Million |

| Market Size in 2026 | USD 1889.55 Million |

| Market Size in 2031 | USD 3112.93 Million |

| CAGR | 10.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Microbial Type Insights

The microbial type segment represents the technological foundation of the Direct-Fed Microbials (DFM) market, with bacterial-based DFMs maintaining clear leadership due to extensive scientific validation, regulatory acceptance, and broad applicability across multiple livestock species. Bacillus and Lactobacillus strains dominate commercial adoption owing to their high thermal stability during feed pelleting processes and their ability to survive harsh gastrointestinal environments. These microbial strains enhance nutrient absorption, support gut microbiome balance, and improve immune response, making them particularly valuable in antibiotic-reduction feeding programs. The leading segment driver for bacterial DFMs is their proven capability to improve feed conversion ratios while supporting disease prevention, enabling producers to achieve productivity gains under increasingly restrictive antibiotic regulations.Yeast-based DFMs represent a strong complementary segment, particularly within ruminant nutrition systems where fermentation efficiency directly influences productivity outcomes. Yeast cultures help stabilize rumen pH, enhance fiber digestion, and improve milk yield performance, which supports their continued adoption in dairy and beef production systems. Meanwhile, multi-strain microbial blends are gaining accelerated traction as livestock producers shift toward holistic gut health management strategies. These formulations combine bacteria and yeast strains to deliver synergistic benefits including pathogen suppression, improved digestion efficiency, and enhanced immune resilience. Increasing research into microbiome optimization and precision nutrition continues to expand innovation within this segment, reinforcing long-term market expansion.

Livestock Type Insights

The livestock type segment reflects varying adoption patterns based on production intensity and economic efficiency requirements, with poultry emerging as the leading segment globally. Poultry production operates on short growth cycles and narrow profitability margins, making feed efficiency optimization critical. The leading segment driver for poultry applications is the need to maximize feed conversion efficiency and flock health while complying with antibiotic-free production standards increasingly demanded by retailers and consumers. DFMs help reduce pathogen load, improve nutrient utilization, and enhance weight gain consistency, supporting widespread adoption across broiler and layer operations.Ruminants represent a substantial and stable market share, particularly within dairy cattle systems where rumen microbial balance plays a direct role in milk productivity and animal longevity. DFMs support improved fiber digestion and metabolic efficiency, allowing producers to optimize feed costs while maintaining milk quality standards. Swine production is increasingly integrating microbial feed additives to address post-weaning stress, gut health challenges, and growth variability, especially in intensive farming environments. Aquaculture stands as the fastest-growing livestock category, driven by rising global seafood demand and increasing pressure to minimize antibiotic usage. DFMs in aquaculture improve water quality, disease resistance, and feed utilization efficiency, making them central to sustainable aquaculture expansion strategies.

Formulation Insights

Formulation type plays a critical role in product stability, application flexibility, and logistical efficiency within the DFM market. Dry formulations dominate global revenues due to their operational advantages in large-scale feed manufacturing environments. The leading segment driver for dry formulations is their extended shelf life and compatibility with existing feed premix and compound feed production infrastructure. Powdered and granulated DFMs integrate seamlessly into automated feed processing systems, reducing handling complexity while maintaining microbial viability.Liquid formulations are gradually expanding their presence, particularly in specialized livestock operations that utilize on-farm dosing systems or water-based supplementation methods. These formats allow precise administration during stress periods such as vaccination, transportation, or environmental transitions. Encapsulated DFMs represent a rapidly advancing innovation segment, designed to protect microbial cultures from heat, moisture, and digestive degradation. Encapsulation technologies significantly improve microbial survival rates through feed processing and gastrointestinal transit, enhancing efficacy and supporting premium product positioning. Continuous investment in delivery technologies is expected to further diversify formulation strategies across livestock categories.

Distribution Channel Insights

Distribution channels in the DFM market are closely aligned with the structure of modern feed supply chains, with feed premix manufacturers accounting for the largest share. The leading segment driver for this channel is the growing integration of functional additives directly into compound feed formulations, enabling standardized nutrition programs across industrial livestock operations. Feed manufacturers increasingly partner with microbial technology providers to deliver value-added feed solutions that enhance animal performance and reduce health risks.Integrated livestock companies represent another major distribution pathway, leveraging long-term procurement agreements to ensure consistent microbial supplementation across vertically integrated production systems. Veterinary and animal health suppliers continue to play an essential role in servicing small and medium-scale farms, where advisory support and technical guidance influence purchasing decisions. Additionally, direct sales models and digital B2B procurement platforms are expanding rapidly in emerging markets, improving accessibility and enabling manufacturers to reach previously underserved producer segments. Digitalization of agricultural supply chains is expected to further reshape distribution dynamics over the forecast period.

End-Use Insights

End-use adoption of DFMs is strongly correlated with production scale and efficiency objectives, with commercial livestock farms representing the dominant segment globally. The leading segment driver for commercial farms is the increasing need to enhance productivity while maintaining animal health under antibiotic-restricted production frameworks. Large-scale operations prioritize consistent performance outcomes, making DFMs an essential component of preventive nutrition strategies.Integrated meat producers are increasingly standardizing microbial supplementation across their supply chains to ensure uniform animal health outcomes and predictable product quality. Dairy operations continue expanding DFM usage to improve feed digestibility, reduce metabolic disorders, and enhance milk yield efficiency. Aquaculture farms are rapidly increasing adoption as export markets impose stricter quality and antibiotic residue standards, encouraging preventive microbial solutions. Beyond traditional livestock applications, pet nutrition manufacturers are emerging as a premium niche end-use segment, incorporating probiotic-based DFMs into functional pet food formulations aligned with growing consumer demand for digestive health and wellness-oriented pet products.

Explore more data points, trends and opportunities Download Free Sample Report

Direct Fed Microbials (DFM) Market Segmentations

By Microbial Type

- Bacterial-Based DFMs

- Yeast-Based DFMs

- Fungal-Based DFMs

- Multi-Strain Microbial Consortia

By Livestock Type

- Poultry

- Ruminants

- Swine

- Aquaculture

- Companion Animals

By Formulation

- Dry Formulations

- Liquid Formulations

- Encapsulated Microbial Products

By Distribution Channel

- Feed Premix Manufacturers

- Integrated Livestock Producers

- Veterinary & Animal Health Suppliers

- Direct Manufacturer Sales

- Online & Digital Procurement Platforms

By End Use

- Commercial Livestock Farms

- Integrated Meat Producers

- Dairy Operations

- Aquaculture Farms

- Pet Nutrition Manufacturers

Regional Insights

North America

North America accounts for a significant share of the global DFM market, supported by advanced feed technologies, strong research infrastructure, and widespread adoption of antibiotic-free livestock production systems. The United States leads regional demand due to its highly industrialized poultry, swine, and dairy industries, where performance optimization and disease prevention are key economic priorities. Regional growth is driven by increasing regulatory scrutiny on antibiotic usage, rising consumer demand for clean-label animal protein, and continuous innovation by feed additive manufacturers. Canada contributes steady growth through technologically advanced dairy operations focused on sustainability, feed efficiency improvements, and reduced environmental impact. Strong collaboration between academic institutions, feed companies, and livestock producers further accelerates product innovation and adoption across the region.

Europe

Europe represents a mature yet innovation-driven DFM market characterized by stringent regulatory frameworks that restrict antibiotic growth promoters. Regional growth is primarily driven by regulatory compliance requirements, strong emphasis on animal welfare, and sustainability-focused agricultural policies promoted by the European Union. Countries such as Germany, France, Spain, and the Netherlands lead adoption due to highly developed poultry and swine industries seeking alternative performance-enhancing solutions. Increasing investment in precision livestock farming and environmentally sustainable feed strategies further supports demand for microbial solutions that improve nutrient efficiency and reduce emissions associated with livestock production.

Asia-Pacific

Asia-Pacific dominates the global DFM market and represents the fastest-growing regional segment. Growth is driven by rapid livestock industrialization, expanding middle-class populations, and rising consumption of animal protein across China, India, Vietnam, and Thailand. Governments across the region are actively promoting food security initiatives and modernization of livestock farming practices, encouraging adoption of advanced feed additives. Expansion of aquaculture production, particularly in Southeast Asia, serves as a major growth catalyst as producers seek disease prevention strategies and improved feed efficiency. Additionally, increasing awareness of antibiotic resistance and export compliance requirements is accelerating the transition toward microbial-based feed solutions across both large-scale commercial farms and emerging mid-sized producers.

Latin America

Latin America is experiencing strong DFM market growth supported by export-oriented livestock industries and competitive global protein trade dynamics. Brazil leads regional consumption due to its position as one of the world’s largest poultry and beef exporters, where productivity optimization and disease management are essential for maintaining export competitiveness. Regional growth drivers include increasing feed efficiency requirements, expansion of commercial farming operations, and adoption of advanced nutrition technologies to meet international quality standards. Mexico and Argentina are also expanding microbial feed additive usage as producers modernize production systems and strengthen supply chain resilience to meet global demand.

Middle East & Africa

The Middle East and Africa region is emerging as a high-potential growth market driven by rising investments in domestic food production and livestock self-sufficiency initiatives. Governments in Saudi Arabia, South Africa, and the United Arab Emirates are promoting modernization of poultry and dairy industries to reduce dependence on imports. Regional growth is supported by increasing adoption of commercial feed systems, expansion of intensive poultry farming, and growing awareness of animal health management practices. Climate-related production challenges and disease risks further encourage adoption of DFMs as preventive nutritional solutions that enhance animal resilience and production stability. As infrastructure and feed manufacturing capabilities continue to improve, microbial feed additives are expected to play an increasingly important role in regional livestock productivity strategies.

Key Players in the Direct Fed Microbials Market

- Cargill Incorporated

- DSM-Firmenich

- Archer Daniels Midland (ADM)

- Evonik Industries AG

- Chr. Hansen Holding A/S

- Lallemand Inc.

- Kemin Industries

- Novozymes A/S

- Alltech Inc.

- Lesaffre Group

- Novus International

- Adisseo

- Calpis Co. Ltd.

- Provita Eurotech

- Biomin