Pangasius Market Size

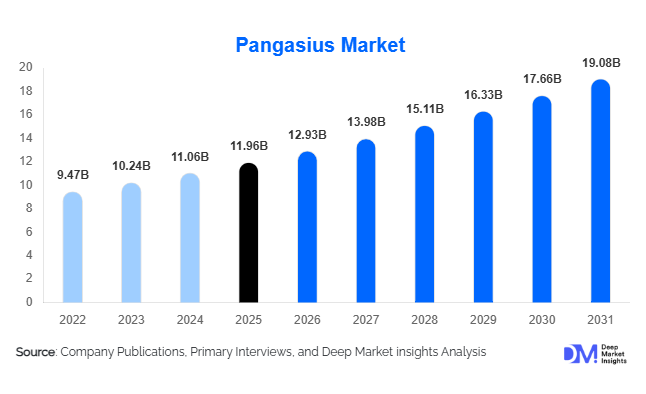

According to Deep Market Insights, the global pangasius market size was valued at USD 11.96 billion in 2025 and is projected to grow from USD 12.93 billion in 2026 to reach USD 19.08 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The pangasius market growth is primarily driven by rising global seafood consumption, increasing demand for affordable whitefish protein, expansion of frozen seafood processing industries, and technological advancements in aquaculture farming systems.

Key Market Insights

- Frozen pangasius fillets dominate global consumption, accounting for the majority of export-oriented seafood trade due to their affordability, shelf stability, and compatibility with foodservice applications.

- Vietnam remains the global production and export leader, supported by advanced aquaculture infrastructure, integrated seafood processing facilities, and strong export-oriented government policies.

- Sustainability-certified pangasius products are gaining rapid traction, particularly in Europe and North America where retailers increasingly prioritize traceability and responsible aquaculture sourcing.

- Foodservice and institutional catering industries are major demand generators, with quick-service restaurants and frozen meal manufacturers increasingly utilizing pangasius as a cost-effective whitefish alternative.

- Asia-Pacific dominates the global market, while the Middle East and Latin America are emerging as high-growth import destinations due to increasing seafood affordability concerns.

- Technological integration in aquaculture, including automated feeding systems, IoT-enabled water monitoring, and AI-assisted disease management, is significantly improving production efficiency and export competitiveness.

Pangasius Market Latest Trends

Expansion of Value-Added Seafood Products

The pangasius industry is increasingly shifting beyond commodity fish exports toward value-added seafood processing. Manufacturers are introducing breaded fillets, marinated seafood portions, ready-to-cook meals, frozen seafood snacks, and premium packaged products tailored for supermarkets and quick-service restaurants. This trend is allowing producers to improve profit margins while differentiating products in highly competitive international seafood markets. Retailers are also increasing private-label seafood offerings, driving demand for standardized pangasius processing solutions. The growing popularity of convenience foods and frozen ready meals across urban populations is accelerating demand for processed pangasius globally.

Sustainable Aquaculture and Certification Adoption

Sustainability certifications are becoming increasingly important across the global pangasius industry. International buyers, particularly in Europe and North America, are prioritizing ASC-certified, BAP-certified, and traceable seafood sourcing practices. Producers are investing heavily in environmentally responsible aquaculture systems, wastewater management infrastructure, feed optimization technologies, and traceability software to strengthen export access and premium product positioning. Governments in Southeast Asia are also supporting sustainable aquaculture modernization programs through subsidies, infrastructure investments, and export promotion policies. This trend is expected to reshape long-term competitiveness within the global pangasius market.

Pangasius Market Drivers

Rising Global Demand for Affordable Seafood Protein

Increasing global seafood consumption and rising food inflation are driving demand for affordable fish protein alternatives such as pangasius. Consumers across both developed and emerging economies are increasingly shifting toward cost-effective whitefish varieties that offer nutritional value at lower prices compared to salmon, cod, and tuna. Pangasius has gained strong popularity within retail seafood channels, institutional catering, and frozen food industries because of its mild flavor, versatility, and low production cost. Expanding middle-class populations and increasing urbanization are further supporting seafood demand growth globally.

Growth of Frozen and Processed Food Industries

The rapid expansion of frozen food manufacturing and ready-to-cook meal industries is significantly supporting pangasius demand. Food processors and restaurant operators increasingly utilize pangasius because of its high fillet yield, consistent supply availability, and compatibility with processed seafood products. Frozen seafood consumption continues expanding across supermarkets, hypermarkets, and online grocery platforms worldwide. Quick-service restaurants and institutional catering providers are also integrating pangasius into menus due to its cost advantages and operational flexibility. These factors continue strengthening the market’s long-term growth outlook.

Pangasius Market Restraints

Environmental and Regulatory Compliance Challenges

The pangasius market faces increasing regulatory scrutiny related to environmental sustainability, antibiotic usage, wastewater discharge, and seafood traceability. Importing countries are implementing stricter food safety standards and sustainability compliance requirements, creating operational challenges for smaller aquaculture producers. Certification costs and infrastructure investments required for export compliance may restrict participation among small-scale farmers. Concerns regarding environmental impacts of intensive fish farming systems also remain an important challenge for long-term market sustainability.

Volatility in Feed and Export Costs

Fish feed prices remain one of the largest operational cost factors within the pangasius industry. Fluctuations in soybean meal, fishmeal, grain prices, and transportation costs can significantly affect producer profitability. International freight rates, currency fluctuations, and trade barriers also contribute to export pricing volatility. Rising cold-chain logistics costs and geopolitical trade uncertainties continue creating supply chain risks for seafood exporters operating across global markets.

Pangasius Industry Key Opportunities

Expansion into Emerging Import Markets

Emerging economies across the Middle East, Latin America, and South Asia are creating substantial growth opportunities for pangasius exporters. Rising urbanization, population growth, and increasing protein consumption are driving seafood import demand in countries such as Saudi Arabia, Brazil, UAE, and Egypt. Pangasius is increasingly preferred because it offers an affordable protein source with strong processing flexibility. Expanding cold-chain infrastructure and organized retail channels within these regions are expected to accelerate import growth over the coming years.

Growth of Sustainable and Premium Seafood Segments

The rising consumer preference for responsibly sourced seafood is creating opportunities for premium certified pangasius products. Producers investing in sustainable aquaculture systems, eco-friendly processing, and traceability technologies can gain stronger access to high-value retail and foodservice markets. Supermarkets and restaurant chains are increasingly prioritizing sustainability-focused seafood procurement, enabling certified exporters to achieve pricing premiums and long-term supply partnerships. The expansion of premium seafood retail channels is expected to support higher-value pangasius product categories globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.96 Billion |

| Market Size in 2026 | USD 12.93 Billion |

| Market Size in 2031 | USD 19.08 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Frozen pangasius fillets dominate the market, accounting for nearly 46% of global market revenue due to strong export suitability, extended shelf life, and widespread utilization within retail and foodservice industries. Skinless and trimmed fillets are particularly popular across North America and Europe where consumers prefer easy-to-cook seafood formats. Whole pangasius products maintain strong demand in domestic Asian markets and traditional wet market channels. Processed and value-added pangasius products such as breaded fillets, seafood snacks, ready-to-cook meals, and fish burgers are rapidly gaining popularity due to rising convenience food demand. Pangasius by-products including fish oil, collagen, and fishmeal are also creating additional revenue opportunities for processors by improving full-fish utilization rates.

Application Insights

Foodservice applications remain the largest demand segment within the global pangasius market, accounting for approximately 39% of total consumption. Restaurants, hotels, institutional caterers, and quick-service restaurant chains increasingly utilize pangasius due to its affordability and versatility across cuisines. Frozen meal manufacturing is another rapidly expanding application area, supported by rising demand for convenience foods and packaged seafood products. Pangasius is also increasingly utilized in processed seafood snacks, surimi products, and ready-to-cook meal kits. Emerging applications in nutraceuticals, animal feed, and fish oil extraction are further expanding the commercial utilization of pangasius processing by-products.

Distribution Channel Insights

Business-to-business (B2B) channels dominate global pangasius sales, contributing nearly 68% of market revenue due to large procurement volumes from foodservice operators, seafood processors, and institutional buyers. Long-term export contracts between major seafood exporters and international distributors continue supporting this segment. Supermarkets and hypermarkets remain the leading retail distribution channels for packaged frozen pangasius products, particularly across developed economies. Online seafood retail and e-commerce grocery platforms are emerging rapidly, especially in Asia-Pacific and North America, enabling broader consumer access to frozen seafood products. Specialty seafood retailers and wet markets continue maintaining importance within traditional Asian consumption markets.

End-Use Industry Insights

The foodservice industry remains the largest end-use segment for pangasius globally, driven by increasing demand from restaurants, hotel chains, institutional catering providers, and quick-service restaurants. Frozen seafood manufacturing is also experiencing strong growth due to expanding demand for ready meals, seafood snacks, and convenience foods. Retail household consumption continues increasing in emerging economies where seafood consumption is rising alongside urbanization and disposable income growth. Animal feed and nutraceutical industries are emerging as important secondary end-use sectors through the utilization of pangasius processing by-products such as fishmeal, fish oil, and collagen extracts. Increasing diversification of end-use applications is expected to improve profitability and reduce processing waste across the industry.

Explore more data points, trends and opportunities Download Free Sample Report

Pangasius Market Segmentations

By Product Type

- Frozen Pangasius Fillets

- Whole Pangasius

- Processed Pangasius

- Value-Added Pangasius Products

- Pangasius By-Products

By Species

- Pangasius Hypophthalmus

- Pangasius Bocourti

- Hybrid Pangasius Varieties

By Nature

- Conventional Pangasius

- Organic Pangasius

- Sustainably Certified Pangasius

By Farming Method

- Intensive Aquaculture

- Semi-Intensive Aquaculture

- Extensive Aquaculture

- Biofloc Farming Systems

- Recirculating Aquaculture Systems (RAS)

By Form

- Fresh/Chilled

- Frozen

- Canned

- Dried

- Powdered/Extract Form

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global pangasius market, accounting for nearly 54% of total market share in 2025. Vietnam remains the world’s largest pangasius producer and exporter due to its advanced aquaculture infrastructure, integrated seafood processing ecosystem, and favorable river systems. China represents a major import market and an increasingly important domestic producer. India, Thailand, and Indonesia are also witnessing rapid growth in freshwater aquaculture investments and seafood consumption. Rising middle-class incomes, expanding urban populations, and increasing frozen seafood retail penetration continue supporting regional market expansion.

Europe

Europe accounts for approximately 21% of global pangasius demand and remains one of the largest import destinations for frozen fillets. Germany, the Netherlands, Spain, France, and the United Kingdom represent major consumption hubs due to strong retail seafood demand and preference for affordable whitefish products. European retailers increasingly prioritize sustainability-certified seafood products, accelerating demand for ASC-certified pangasius exports. The region also benefits from strong frozen food consumption and highly developed seafood distribution infrastructure.

North America

North America represents nearly 14% of the global market, led primarily by the United States and Canada. Demand is supported by institutional catering, quick-service restaurants, and frozen seafood retail channels. Consumers increasingly prefer affordable seafood alternatives amid rising food prices, positively impacting pangasius imports. Sustainability certifications and food safety compliance remain critical purchasing criteria among North American importers and retailers. Growth in online seafood retail is also supporting higher market penetration.

Latin America

Latin America is gradually emerging as an important growth market for pangasius imports, particularly in Brazil, Colombia, Argentina, and Chile. Rising seafood consumption, retail modernization, and affordability concerns are encouraging consumers to shift toward imported frozen whitefish products. Brazil is expected to remain one of the region’s fastest-growing import markets due to increasing middle-class demand and expanding organized food retail infrastructure.

Middle East & Africa

The Middle East & Africa region is projected to witness one of the fastest growth rates during the forecast period. Countries including Saudi Arabia, UAE, Egypt, and South Africa are increasingly importing pangasius products due to rising seafood consumption and dependence on imported protein sources. Growth in tourism, hospitality industries, and institutional catering demand is supporting market expansion. Halal-certified seafood processing compatibility also strengthens pangasius demand across Islamic markets within the region.

Key Players in the Pangasius Market

- Vinh Hoan Corporation

- Nam Viet Corporation (NAVICO)

- IDI Corporation

- Bien Dong Seafood

- Hung Ca Co. Ltd.

- Sao Ta Foods

- Godaco Seafood

- Hung Vuong Corporation

- Green Farms Seafood

- Cadovimex Seafood

- Agifish

- Cuu Long Fish Joint Stock Company

- Dai Thanh Seafoods

- East Sea Seafoods

- Truong Giang Fishery Holdings