Palm Butter Market Size

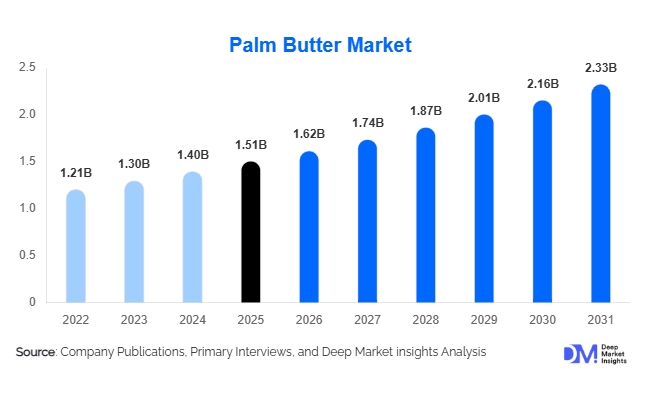

According to Deep Market Insights, the global palm butter market size was valued at USD 1.51 billion in 2025 and is projected to grow from USD 1.62 billion in 2026 to reach USD 2.33 billion by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The palm butter market growth is primarily driven by rising demand for plant-based fats, increasing consumption of natural cosmetic ingredients, and expanding applications in food processing, personal care, pharmaceuticals, and renewable fuel industries. The market is also benefiting from increasing consumer preference for sustainably sourced ingredients and growing investments in certified palm-derived products. Palm butter's excellent oxidative stability, multifunctional properties, and cost competitiveness compared to alternative vegetable butters such as shea and cocoa butter continue to support its adoption across diverse industrial applications. Emerging economies in Asia-Pacific and Africa, coupled with growing demand from the cosmetics industry in North America and Europe, are expected to further accelerate market expansion during the forecast period.

Key Market Insights

- The palm butter industry is increasingly transitioning toward certified sustainable and traceable products, driven by consumer awareness and stringent procurement standards among multinational food and cosmetics manufacturers.

- Cosmetic and personal care applications are emerging as the fastest-growing demand segment, with manufacturers increasingly utilizing palm butter in moisturizers, soaps, hair care products, and premium skincare formulations.

- Asia-Pacific dominates the global market, accounting for approximately 45% of global demand, supported by extensive production capabilities and large-scale consumption in food and biodiesel applications.

- Europe is witnessing rapid growth in sustainable palm butter consumption, driven by stringent environmental regulations and increasing demand for certified ingredients.

- Food and beverage applications remain the largest end-use segment, benefiting from increasing consumption of processed foods, bakery products, and plant-based alternatives.

- Technological advancements in processing, fractionation, and traceability systems are improving product quality and enabling manufacturers to target high-margin specialty applications.

Palm Butter Market Latest Trends

Sustainable and Certified Palm Butter Demand Accelerating

Sustainability has become one of the defining trends in the global palm butter market. Food and personal care manufacturers are increasingly requiring RSPO-certified and traceable palm butter to meet environmental, social, and governance (ESG) commitments. The implementation of the European Union Deforestation Regulation and growing consumer preference for ethically sourced ingredients have accelerated demand for certified products. Manufacturers are investing heavily in traceability technologies, sustainable plantations, and transparent supply chains to ensure compliance with international sustainability standards. Premium pricing for certified products and increasing procurement requirements from multinational corporations are encouraging further investment across the value chain.

Expansion of Palm Butter in Natural Cosmetics and Personal Care Products

The global shift toward natural and plant-based beauty products is creating substantial opportunities for palm butter manufacturers. Cosmetic-grade palm butter is increasingly being utilized in moisturizers, anti-aging creams, soaps, body lotions, and hair care products due to its excellent emollient and moisturizing properties. Manufacturers are developing specialty formulations and premium blends targeting clean-label and organic beauty segments. Demand is particularly strong in North America, Europe, Japan, and South Korea, where consumers increasingly prefer naturally derived ingredients with sustainable sourcing credentials.

Palm Butter Market Drivers

Growing Demand for Plant-Based and Vegan Ingredients

The increasing popularity of vegan and plant-based diets is significantly supporting demand for palm butter. Food manufacturers are increasingly incorporating plant-derived fats into spreads, bakery products, confectionery, and dairy alternatives to satisfy changing consumer preferences. Palm butter offers superior functionality and cost advantages compared with several alternative vegetable fats, making it an attractive ingredient across multiple food applications.

Rapid Expansion of the Natural Cosmetics Industry

The global natural cosmetics industry continues to experience strong growth, directly supporting palm butter consumption. Palm butter's antioxidant, moisturizing, and skin-conditioning properties make it a preferred ingredient in skincare and personal care products. Rising disposable incomes and increasing consumer awareness regarding natural ingredients are encouraging cosmetics manufacturers to expand their portfolios using palm-derived ingredients.

Increasing Biodiesel Production and Renewable Fuel Mandates

Governments worldwide are increasing renewable energy targets and implementing biodiesel blending mandates. Palm-derived feedstocks remain among the most economical sources for biodiesel production, particularly in Indonesia and Malaysia. Growing investments in renewable energy infrastructure and increasing demand for sustainable fuels are creating additional growth opportunities for palm butter and related derivatives.

Palm Butter Market Restraints

Environmental and Deforestation Concerns

The palm industry continues to face scrutiny regarding deforestation, biodiversity loss, and greenhouse gas emissions associated with oil palm cultivation. Environmental concerns have resulted in stricter regulations, certification requirements, and reputational challenges for market participants, particularly in developed economies.

Raw Material Price Volatility

Palm butter prices remain highly dependent on fluctuations in crude palm oil prices, weather conditions, labor availability, and export regulations in major producing countries. Volatility in raw material prices creates procurement uncertainties and affects profit margins for downstream manufacturers.

Palm Butter Industry Key Opportunities

Premium Sustainable and Organic Product Development

Certified sustainable and organic palm butter products represent one of the most attractive opportunities in the market. Increasing demand from food, cosmetics, and personal care manufacturers for ethically sourced ingredients has created premium pricing opportunities. Companies investing in certification, traceability, and sustainable sourcing systems can access high-value markets across Europe and North America while improving long-term competitiveness.

Expansion into High-Margin Cosmetic Applications

The premium skincare and natural cosmetics sectors present significant opportunities for palm butter manufacturers. Cosmetic-grade palm butter generates higher profit margins compared to food-grade products and continues to witness increasing demand due to the growing popularity of clean-label beauty products. Manufacturers are increasingly focusing on product innovation and specialty formulations targeting anti-aging, moisturizing, and organic skincare applications.

Growing Renewable Energy and Biofuel Applications

Renewable energy initiatives and biodiesel mandates across Asia-Pacific and Europe are creating substantial long-term demand opportunities. Investments in renewable diesel and sustainable aviation fuel technologies are expected to increase the utilization of palm-based feedstocks, supporting future demand growth for palm butter derivatives.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.51 Billion |

| Market Size in 2026 | USD 1.62 Billion |

| Market Size in 2031 | USD 2.33 Billion |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The pure palm butter segment dominated the global palm butter market and accounted for approximately 48% of total revenue in 2025. The segment's leadership is primarily attributed to rising demand from food processors, bakery manufacturers, confectionery producers, and personal care companies seeking minimally processed, natural, and multifunctional ingredients with superior stability and cost efficiency. Growing consumer preference for clean-label products and naturally derived ingredients has further accelerated the adoption of pure palm butter across both food and non-food applications. In addition, manufacturers increasingly prefer pure formulations due to their versatility in product development and ease of incorporation into a wide range of formulations.Blended palm butter products are witnessing robust growth owing to their enhanced functional properties, improved texture, and formulation flexibility. These products are increasingly utilized in specialty food products, spreads, plant-based formulations, and premium cosmetic applications where customized functionality is essential. Meanwhile, specialty palm butter variants, including cosmetic-grade, pharmaceutical-grade, and high-purity formulations, are expanding rapidly due to their higher value addition, superior performance characteristics, and premium pricing potential. The market is also experiencing increasing demand for organic, sustainably sourced, and certified palm butter products as manufacturers and consumers place greater emphasis on environmental responsibility, traceability, and ethical sourcing practices.

Application Insights

The food and beverage segment remained the largest application category and accounted for approximately 46% of global market revenue in 2025. The segment's dominance is driven by the extensive use of palm butter in bakery products, confectionery, chocolate fillings, spreads, dairy alternatives, and plant-based food formulations due to its excellent oxidative stability, desirable texture characteristics, and cost competitiveness compared with alternative vegetable fats. The continued expansion of processed food manufacturing, increasing demand for convenience foods, and growing consumption of plant-based products are expected to sustain strong demand across this segment throughout the forecast period.Cosmetics and personal care applications represent the fastest-growing segment of the market, supported by rising consumer preference for natural skincare products, organic beauty formulations, and plant-derived ingredients. Palm butter is increasingly incorporated into moisturizers, creams, lotions, soaps, lip care products, and hair care formulations owing to its emollient properties and high content of beneficial fatty acids. Pharmaceutical applications are also expanding steadily as manufacturers increasingly utilize palm butter in medicinal creams, ointments, topical formulations, and carrier bases. Furthermore, biodiesel production and industrial applications, including surfactants, lubricants, and oleochemical manufacturing, are emerging as important demand centers as governments and industries increasingly prioritize renewable energy sources and sustainable industrial feedstocks.

Distribution Channel Insights

Direct business-to-business (B2B) sales dominated the global palm butter market and accounted for approximately 58% of total industry revenues in 2025. The segment's leadership is largely attributed to the procurement practices of large food manufacturers, cosmetic companies, pharmaceutical producers, and biodiesel processors that prefer long-term supply agreements and direct sourcing arrangements to ensure stable pricing, quality consistency, and uninterrupted raw material availability. Increasing vertical integration and strategic partnerships between producers and end users are further supporting the growth of this channel.Specialty ingredient distributors continue to play an important role in the market by supplying small and medium-sized manufacturers, particularly in developed economies where customized formulations and smaller procurement volumes are common. Retail and e-commerce channels are gradually gaining traction, especially in household and personal care applications, driven by rising consumer awareness of natural ingredients and increasing demand for premium and organic products. The growing adoption of digital procurement platforms, online ingredient marketplaces, and direct manufacturer websites is further improving supply chain efficiency, expanding market accessibility, and facilitating global trade.

End-Use Industry Insights

Food processing companies remained the largest end-use segment, accounting for approximately 41% of global demand in 2025. The segment's dominance is supported by the continued expansion of processed food manufacturing, increasing consumption of bakery and confectionery products, and rapid growth in plant-based food categories that require stable and multifunctional vegetable fats. Palm butter's favorable functional characteristics, including texture enhancement, oxidative stability, and cost-effectiveness, continue to drive its widespread adoption across the food industry.Cosmetic manufacturers represent the fastest-growing end-user segment due to the increasing demand for natural and organic beauty products, clean-label personal care formulations, and sustainably sourced ingredients. Pharmaceutical companies are also increasing their utilization of palm butter in topical treatments, medicinal creams, and functional formulations owing to its compatibility with various active ingredients and favorable sensory properties. In addition, biodiesel producers and industrial chemical manufacturers are emerging as important end users as governments worldwide continue to promote renewable energy development, decarbonization strategies, and the adoption of sustainable industrial feedstocks.

Packaging Insights

Bulk industrial packaging dominated the global market and accounted for nearly 63% of total demand in 2025. The segment's leadership is primarily driven by the procurement requirements of large-scale food processors, cosmetics manufacturers, pharmaceutical companies, and biodiesel producers that purchase palm butter in drums, intermediate bulk containers, and large storage units to improve logistics efficiency and reduce overall packaging costs. The increasing scale of industrial production and the need for cost-effective transportation solutions continue to reinforce the dominance of this segment.Plastic containers, jars, and smaller packaging formats are steadily gaining popularity in retail and specialty applications, particularly among personal care manufacturers and household consumers seeking convenience and product accessibility. Additionally, growing environmental concerns and increasing corporate sustainability commitments are encouraging the development and adoption of recyclable, reusable, and eco-friendly packaging solutions across the value chain.

Explore more data points, trends and opportunities Download Free Sample Report

Palm Butter Market Segmentations

By Product Type

- Pure Palm Butter

- Blended Palm Butter

- Specialty Palm Butter

By Processing Type

- Raw/Unrefined Palm Butter

- Refined Palm Butter

- Fractionated Palm Butter

- Fortified Palm Butter

By Source Certification

- Conventional Palm Butter

- RSPO-Certified Sustainable Palm Butter

- Organic Certified Palm Butter

- Fair Trade Certified Palm Butter

By Application

- Food & Beverage

- Cosmetics & Personal Care

- Industrial Applications

- Biofuel Applications

- Pharmaceuticals & Nutraceuticals

By Distribution Channel

- Direct B2B Sales

- Specialty Ingredient Distributors

- Modern Retail

- E-commerce Platforms

- Institutional Procurement

Regional Insights

Asia-Pacific

Asia-Pacific dominated the global palm butter market and accounted for approximately 45% of total revenues in 2025. The region benefits from abundant raw material availability, extensive palm cultivation, well-established processing infrastructure, and integrated supply chains, particularly in Indonesia and Malaysia, which collectively represent the world's largest producers and exporters of palm-based products. China and India continue to emerge as major consumption centers due to rapid urbanization, rising disposable incomes, expanding food processing industries, and increasing demand for cosmetics and personal care products. The growing adoption of biodiesel blending programs across Southeast Asia, significant investments in downstream oleochemical manufacturing, and increasing production of plant-based foods are further accelerating regional demand. Moreover, Japan and South Korea are increasingly emphasizing sustainably sourced and certified palm butter products, creating significant opportunities for premium and value-added suppliers.

Europe

Europe accounted for approximately 28% of the global market in 2025 and remains one of the fastest-growing regions for sustainable palm butter consumption. Germany, France, the United Kingdom, and the Netherlands represent major demand centers due to their strong food processing, confectionery, and cosmetics industries. Market growth is being driven by stringent environmental regulations, increasing consumer preference for ethically sourced ingredients, and widespread adoption of certified sustainable palm products. The region is also benefiting from rising demand for natural cosmetic ingredients, clean-label food formulations, and plant-based products. In addition, corporate sustainability commitments and regulatory initiatives promoting supply chain transparency and responsible sourcing continue to accelerate demand for certified palm butter products across Europe.

North America

North America accounted for approximately 15% of global demand in 2025, with the United States representing nearly 12% of the total market. Regional demand is primarily driven by increasing utilization of palm butter in natural cosmetics, premium skincare products, processed foods, and plant-based formulations. Growing consumer awareness regarding clean-label ingredients, rising demand for organic and sustainably sourced products, and expanding investments in natural personal care products are creating favorable market conditions. The region is also witnessing increasing product innovation in vegan foods and functional ingredients, further supporting the adoption of palm butter across multiple end-use industries.

Latin America

Brazil and Mexico dominate regional demand, supported by expanding food processing, confectionery, and personal care industries. Rising consumer spending, improving living standards, and increasing industrialization are expected to support further market growth across the region. The growing penetration of modern retail channels, increasing consumption of processed and packaged foods, and rising demand for affordable cosmetic products are contributing significantly to market expansion. Furthermore, favorable agricultural conditions and increasing investments in domestic edible oil processing and oleochemical industries are expected to strengthen the region's long-term growth prospects.

Middle East & Africa

The Middle East and Africa region continues to experience steady demand growth driven by food manufacturing, cosmetics production, and industrial applications. Gulf countries increasingly rely on imported palm butter products to meet the growing requirements of their food processing and personal care sectors, while African markets are witnessing rising domestic consumption supported by rapid urbanization, population growth, and increasing disposable incomes. Expanding investments in food manufacturing infrastructure, growing demand for packaged foods and personal care products, and the gradual development of local processing capabilities are further supporting regional market growth. Additionally, increasing industrial diversification initiatives and the expansion of downstream consumer goods industries are expected to create new opportunities for palm butter manufacturers across the region.

Key Players in the Palm Butter Market

- Wilmar International

- Sime Darby Plantation

- Golden Agri-Resources

- IOI Corporation

- Musim Mas

- Kuala Lumpur Kepong Berhad

- First Resources Limited

- Bumitama Agri Ltd.

- Astra Agro Lestari

- FGV Holdings Berhad

- Indofood Agri Resources Ltd.

- AAK AB

- Cargill Incorporated

- Bunge Global SA

- Olam Group Limited