Organic Shortening Powder Market Size

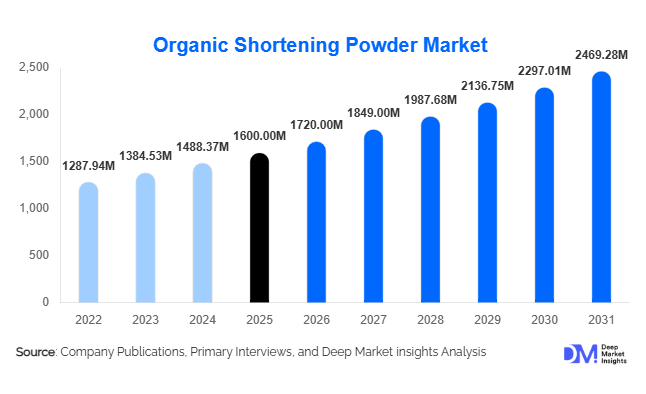

According to Deep Market Insights, the global organic shortening powder market size was valued at USD 1,600 million in 2025 and is projected to grow from USD 1,720 million in 2026 to reach USD 2,469.28 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The organic shortening powder market growth is primarily driven by increasing consumer demand for clean-label food products, rapid expansion of organic bakery and confectionery manufacturing, growing adoption of plant-based ingredients, and regulatory support for trans-fat-free food formulations. Food manufacturers are increasingly utilizing organic shortening powders due to their superior handling characteristics, extended shelf life, compatibility with dry food systems, and ability to support certified organic product claims.

Key Market Insights

- Bakery applications account for approximately 45% of global demand, making baked goods the largest application area for organic shortening powder worldwide.

- Non-hydrogenated organic shortening powders dominate product consumption, supported by global regulations limiting trans fats and increasing consumer preference for healthier ingredients.

- North America leads the global market with nearly 34% market share, driven by mature organic food industries and strong demand for premium bakery products.

- Asia-Pacific is the fastest-growing regional market, supported by expanding food processing industries, urbanization, and rising consumer awareness of organic foods.

- Plant-based and vegan food manufacturers are becoming major consumers of organic shortening powder for dairy-free and animal-free food formulations.

- Advanced spray-drying and microencapsulation technologies are improving ingredient functionality, storage stability, and processing efficiency across food manufacturing operations.

Organic Shortening Powder Market Latest Trends

Growing Adoption of Clean-Label and Organic Food Ingredients

The global food industry is witnessing a substantial shift toward clean-label ingredients, creating favorable conditions for organic shortening powder manufacturers. Food brands are reformulating products to eliminate artificial additives, partially hydrogenated oils, and synthetic ingredients while improving transparency in ingredient declarations. Organic shortening powders provide food processors with an effective solution to achieve clean-label positioning while maintaining functionality in bakery, confectionery, and processed food products. Major retailers and foodservice operators are increasingly prioritizing certified organic ingredients across private-label portfolios, accelerating demand for specialty organic fat systems. As consumer scrutiny of ingredient labels intensifies, manufacturers are expected to invest further in organic-certified shortening powder solutions capable of meeting both regulatory requirements and evolving consumer expectations.

Expansion of Plant-Based Food Manufacturing

Plant-based food production has emerged as one of the most influential trends shaping demand for organic shortening powders. Manufacturers of vegan baked goods, dairy alternatives, frozen desserts, nutritional foods, and snack products increasingly require plant-derived fat systems that align with organic certification standards. Organic shortening powders based on coconut oil, sunflower oil, canola oil, and soybean oil are becoming integral ingredients in next-generation plant-based formulations. Food companies are introducing innovative vegan product lines targeting flexitarian consumers, creating sustained demand for organic powdered fats. The expansion of vegan bakery chains, premium dairy alternatives, and functional nutrition products is expected to reinforce long-term market growth opportunities.

Organic Shortening Powder Market Drivers

Rising Demand for Organic Processed Foods

Consumer demand for organic packaged foods continues to increase globally as health-conscious buyers seek products perceived as safer, more sustainable, and less processed. Organic shortening powder plays a critical role in delivering functionality while preserving organic certification integrity. Food manufacturers are responding by expanding organic product portfolios across bakery, snacks, confectionery, and convenience foods. The premium pricing associated with organic products also enables manufacturers to offset higher ingredient costs, supporting widespread adoption throughout the value chain.

Growth of Industrial Bakery Production

The industrial bakery sector remains the largest consumer of organic shortening powder. Commercial bakery manufacturers benefit from the ingredient’s ease of storage, improved handling efficiency, reduced transportation costs, and enhanced shelf stability compared to conventional shortening formats. Growing global consumption of bread, pastries, cookies, cakes, and baking mixes continues to support robust demand. Large-scale bakery operators are increasingly utilizing powdered shortening systems to optimize production processes and improve formulation consistency across manufacturing facilities.

Expansion of Trans-Fat-Free Food Formulations

Governments and health authorities worldwide continue imposing restrictions on trans fats in food products. Organic shortening powder manufacturers have responded by developing non-hydrogenated and interesterified fat systems that deliver desired baking performance without trans-fat concerns. Food processors are actively reformulating products to comply with evolving regulations while maintaining texture, mouthfeel, and product quality. This trend has significantly accelerated adoption of organic shortening powders across premium and mainstream food categories.

Organic Shortening Powder Market Restraints

High Cost of Organic Raw Materials

Certified organic vegetable oils remain substantially more expensive than conventional alternatives due to certification requirements, traceability protocols, segregated supply chains, and limited agricultural production volumes. These elevated costs contribute to higher finished product prices, limiting adoption among price-sensitive food manufacturers and consumers. Cost competitiveness remains one of the primary challenges facing market expansion in developing economies.

Supply Chain and Feedstock Availability Challenges

The availability of certified organic palm oil, coconut oil, sunflower oil, and soybean oil is often influenced by weather conditions, agricultural yields, certification compliance, and regional production capacities. Supply disruptions can create pricing volatility and procurement challenges for manufacturers. Maintaining consistent quality standards and ensuring reliable organic feedstock sourcing remain critical operational concerns for industry participants.

Organic Shortening Powder Industry Key Opportunities

Growth Opportunities in Plant-Based and Vegan Foods

The rapid expansion of the global plant-based food industry presents a major opportunity for organic shortening powder suppliers. Manufacturers developing organic fat systems optimized for vegan bakery products, dairy alternatives, frozen desserts, and nutritional foods are well-positioned to capture emerging demand. As consumers increasingly embrace flexitarian lifestyles, food companies are investing heavily in plant-based product innovation. Organic shortening powders provide the required texture, stability, and functionality while supporting organic and vegan product claims. Long-term supply agreements with major plant-based food brands are expected to create significant revenue opportunities for ingredient suppliers.

Expansion into Emerging Asia-Pacific Markets

Asia-Pacific represents one of the most attractive growth opportunities due to rising disposable incomes, increasing urbanization, expanding bakery industries, and growing awareness of organic food products. Countries such as China, India, Indonesia, Thailand, and Vietnam are witnessing strong growth in packaged foods and modern retail channels. Food manufacturers in these markets are increasingly seeking premium ingredients that support product differentiation. Establishing regional manufacturing and sourcing capabilities can help suppliers capitalize on accelerating demand while reducing supply chain costs.

Clean-Label Reformulation Programs

Food manufacturers globally are engaged in large-scale reformulation initiatives to improve ingredient transparency and meet regulatory requirements. Organic shortening powder suppliers capable of delivering non-hydrogenated, clean-label, and specialty organic formulations can benefit from increasing demand across bakery, snack, and processed food categories. The trend toward ingredient simplification and premiumization is expected to create long-term growth opportunities for innovative suppliers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1600.00 Million |

| Market Size in 2026 | USD 1720.00 Million |

| Market Size in 2031 | USD 2469.28 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Palm-based organic shortening powder continues to dominate the global market, accounting for approximately 39% of total revenue in 2025. The segment's leadership is primarily driven by its superior oxidative stability, excellent shortening functionality, cost-effectiveness, and widespread availability within global food processing supply chains. Palm-based formulations provide consistent texture, enhanced mouthfeel, improved aeration, and extended shelf life, making them highly suitable for large-scale bakery, confectionery, and snack manufacturing applications. Additionally, the growing preference among food manufacturers for stable powdered fat ingredients that can withstand varying processing conditions further strengthens demand for palm-based products. Their ability to support clean-label formulations while maintaining performance characteristics comparable to conventional shortening ingredients continues to reinforce their position as the preferred product type across industrial food production.Soy-based and coconut-based organic shortening powders represent important secondary segments, benefiting from rising demand for plant-based, vegan-friendly, and allergen-conscious food products. These formulations are increasingly incorporated into specialty bakery products, dairy alternatives, nutritional foods, and premium confectionery applications. Furthermore, blended vegetable oil formulations are gaining traction as manufacturers seek customized functionality, improved nutritional profiles, and differentiated product positioning. Emerging demand for sunflower-based and canola-based organic shortening powders is expected to further diversify the market landscape, supported by increasing consumer preference for alternative vegetable oil sources and ongoing innovation in organic ingredient development.

Functional Formulation Insights

Non-hydrogenated organic shortening powders account for nearly 58% of global market demand, making them the largest functional formulation segment. The segment's dominance is primarily driven by increasing global consumer awareness regarding the health risks associated with trans fats, coupled with stringent regulatory restrictions on partially hydrogenated oils across major food markets. Food manufacturers increasingly prefer non-hydrogenated formulations because they enable clean-label product development while delivering the texture, stability, and processing performance required for commercial food production. The growing shift toward healthier ingredient profiles and transparent food labeling practices continues to accelerate adoption across bakery, confectionery, snack, and convenience food applications.Interesterified organic shortening powders are witnessing steady growth, particularly in premium bakery and confectionery products where manufacturers require enhanced melting characteristics, improved structure, and superior stability. These formulations offer greater flexibility in tailoring fat functionality without the need for hydrogenation. Meanwhile, trans-fat-free shortening powders continue gaining momentum across developed and emerging markets as food processors actively reformulate product portfolios to comply with evolving regulatory standards and meet consumer demand for healthier food products. The increasing focus on nutritional optimization and clean-label innovation is expected to support continued expansion of advanced functional shortening formulations throughout the forecast period.

Application Insights

Bakery products remain the largest application segment, contributing approximately 45% of global market revenue in 2025. The segment's leadership is primarily driven by the extensive use of organic shortening powder in bread, cakes, pastries, cookies, muffins, donuts, croissants, biscuits, and baking mixes, where it plays a critical role in enhancing texture, crumb softness, aeration, moisture retention, and shelf-life stability. The continued growth of artisanal baking, premium bakery products, and organic baked goods consumption worldwide further strengthens demand from this segment. Additionally, the increasing popularity of convenience bakery products and ready-to-bake solutions supports widespread adoption of powdered shortening ingredients due to their ease of handling, storage efficiency, and formulation consistency.Confectionery applications represent the second-largest segment, supported by growing utilization in fillings, creams, coatings, frostings, compound chocolates, and specialty confectionery products. Demand from dairy alternatives and plant-based food manufacturers is expanding rapidly as vegan and lactose-free product categories continue to gain global acceptance. Furthermore, dry premixes, nutritional foods, meal replacement products, frozen foods, and convenience food applications are emerging as attractive growth areas because powdered fat systems offer superior shelf stability, simplified transportation, and enhanced formulation flexibility. Increasing innovation in functional foods and fortified products is expected to create additional opportunities for organic shortening powder adoption across diverse food categories.

Distribution Channel Insights

Direct business-to-business (B2B) sales dominate the organic shortening powder market, accounting for approximately 61% of global revenue. The segment's leadership is primarily driven by the procurement strategies of large food manufacturers that establish long-term supply agreements with ingredient producers to ensure consistent quality, supply reliability, traceability, and cost optimization. Direct sourcing also enables manufacturers to collaborate closely with suppliers on customized formulations, product development initiatives, and regulatory compliance requirements, making it the preferred distribution model across industrial food processing operations.Ingredient distributors continue to play a vital role, particularly among small and medium-sized food manufacturers that require access to specialty ingredients without maintaining extensive procurement networks. Foodservice supply channels are expanding steadily as premium bakery chains, cafes, quick-service restaurants, and foodservice operators increasingly incorporate organic and clean-label ingredients into their product offerings. In addition, the emergence of digital ingredient marketplaces and online procurement platforms is improving market accessibility for smaller processors and regional manufacturers by streamlining sourcing processes, enhancing price transparency, and expanding supplier reach across global markets.

End User Insights

Industrial food manufacturers account for approximately 42% of global market demand, making them the largest end-user segment. The segment's dominance is primarily driven by the growing incorporation of organic shortening powder across large-scale bakery, confectionery, snack food, frozen food, nutritional food, and convenience food production facilities. Industrial manufacturers increasingly favor powdered shortening ingredients because they offer superior storage stability, simplified handling, reduced transportation costs, and consistent product performance across high-volume production environments. The ongoing expansion of packaged food consumption and clean-label product development initiatives further reinforces demand from this customer group.Commercial bakeries remain a major consumer segment owing to rising global demand for premium baked goods, artisanal bakery products, and organic bakery formulations. Confectionery manufacturers are increasingly utilizing organic powdered fats to improve product stability, optimize texture, and support organic certification requirements. Foodservice operators, private-label food producers, and contract manufacturers are emerging as high-growth customer categories as retailers expand organic product offerings and consumers increasingly seek healthier food alternatives. Household adoption remains comparatively limited but continues to grow steadily through specialty baking ingredients, home baking trends, and the increasing availability of organic food products in retail channels.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Shortening Powder Market Segmentations

By Product Type

- Palm-Based Organic Shortening Powder

- Soy-Based Organic Shortening Powder

- Coconut-Based Organic Shortening Powder

- Sunflower-Based Organic Shortening Powder

- Canola/Rapeseed-Based Organic Shortening Powder

- Blended Vegetable Organic Shortening Powder

- Other Organic Shortening Powders

By Functional Formulation

- Hydrogenated Organic Shortening Powder

- Non-Hydrogenated Organic Shortening Powder

- Interesterified Organic Shortening Powder

- Trans-Fat-Free Organic Shortening Powder

By Carrier System

- Maltodextrin-Based Carrier

- Gum Arabic-Based Carrier

- Starch-Based Carrier

- Protein-Based Carrier

- Carrier-Free Specialty Powder Systems

By Application

- Bakery Products

- Confectionery Products

- Dairy & Dairy Alternatives

- Snack Foods

- Dry Mixes & Premixes

- Processed Foods

- Nutritional & Functional Foods

By Organic Certification

- USDA Organic Certified

- EU Organic Certified

- JAS Organic Certified

- India Organic/NPOP Certified

- Other Regional Organic Certifications

Regional Insights

North America

North America accounted for approximately 34% of global market share in 2025, making it the largest regional market for organic shortening powder. The United States represented nearly 28% of global demand, supported by strong organic food consumption, a highly developed bakery and packaged food industry, widespread adoption of clean-label ingredients, and advanced food processing infrastructure. Canada contributes significant demand through its growing natural food sector, premium bakery manufacturing industry, and increasing consumer preference for sustainable food products.Regional growth is being driven by rising demand for organic and plant-based foods, increasing reformulation activities aimed at reducing trans fats and artificial ingredients, growing consumer awareness regarding ingredient transparency, and expanding investments in organic food manufacturing. The strong presence of leading food brands, well-established distribution networks, and increasing demand for premium bakery and convenience food products continue to strengthen North America's position as the leading regional market.

Europe

Europe accounted for nearly 29% of global market revenue in 2025, making it the second-largest regional market. Germany remains the largest country-level market owing to its well-established organic food sector, advanced bakery manufacturing capabilities, and strong consumer preference for clean-label products. The United Kingdom, France, Italy, Spain, and the Netherlands collectively contribute substantial demand through growing private-label organic product portfolios, premium bakery consumption, and innovation in sustainable food ingredients.Regional market growth is supported by stringent regulations promoting ingredient transparency, increasing adoption of organic certifications, rising consumer demand for sustainable and ethically sourced food ingredients, and continued expansion of premium bakery and confectionery markets. Furthermore, growing environmental awareness, strong retail penetration of organic food products, and government support for sustainable agriculture continue to create favorable conditions for market expansion across Europe.

Asia-Pacific

Asia-Pacific represented approximately 24% of global demand in 2025 and is projected to register the fastest growth rate, approaching 9% CAGR through 2031. China remains the largest market within the region, driven by rapid expansion of the food processing industry, increasing consumption of premium packaged foods, and growing interest in healthier food ingredients. India is emerging as one of the fastest-growing national markets due to accelerating urbanization, rising disposable incomes, expanding organized retail networks, and increasing consumption of bakery and convenience foods. Japan, South Korea, Australia, Indonesia, Thailand, and other Southeast Asian countries continue contributing to regional demand through expanding premium food manufacturing activities and increasing adoption of organic ingredients.The region's growth is being fueled by rapid urban population growth, changing dietary preferences, increasing demand for packaged and convenience foods, expanding middle-class consumer spending, and growing awareness of organic and clean-label food products. Rising investments in food manufacturing infrastructure, the expansion of modern retail channels, and increasing penetration of international food brands are further accelerating demand for organic shortening powder across Asia-Pacific.

Latin America

Latin America accounted for approximately 6% of global market share in 2025. Brazil leads regional consumption due to its large food processing sector, expanding bakery industry, and growing organic food market. Argentina and Chile are witnessing increasing adoption of organic shortening powder among bakery, confectionery, and snack food manufacturers as demand for premium food products continues to rise.Regional growth is supported by increasing consumer awareness regarding healthier food choices, expanding availability of organic products through modern retail channels, rising investments in food processing industries, and growing export opportunities for value-added food products. Additionally, increasing urbanization, improving economic conditions in key markets, and the gradual expansion of organic certification programs are expected to contribute to long-term market development throughout Latin America.

Middle East & Africa

The Middle East & Africa region contributed approximately 7% of global demand in 2025. The United Arab Emirates and Saudi Arabia represent major consumption centers due to strong imports of premium food ingredients, expanding bakery and confectionery industries, and a rapidly growing foodservice sector. South Africa remains the leading market within Africa, supported by an expanding food manufacturing base and increasing consumer awareness of organic and natural food products.Market growth across the region is being driven by rising disposable incomes, increasing demand for premium and imported food products, rapid expansion of the hospitality and foodservice sectors, and growing investments in food processing capabilities. The continued development of modern retail infrastructure, increasing tourism activity in Gulf countries, and rising consumer interest in healthier and clean-label food ingredients are expected to create significant growth opportunities for organic shortening powder suppliers across the Middle East and Africa.