Organic Oat Fiber Market Size

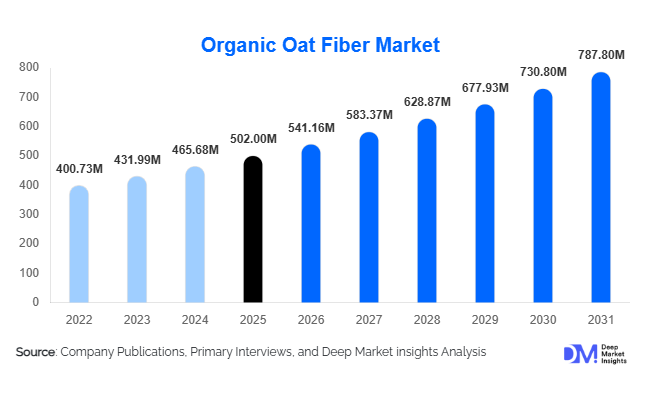

According to Deep Market Insights, the global organic oat fiber market size was valued at USD 502 million in 2025 and is projected to grow from USD 541.16 million in 2026 to reach USD 787.80 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The organic oat fiber market growth is primarily driven by rising demand for clean-label ingredients, increasing consumer awareness regarding digestive health and gut microbiome wellness, and the rapid expansion of organic and functional food categories worldwide. Organic oat fiber has become a preferred ingredient across bakery products, breakfast cereals, dairy alternatives, nutritional supplements, sports nutrition formulations, and pharmaceutical applications due to its multifunctional properties, including moisture retention, texture enhancement, fat replacement, and dietary fiber fortification.

Key Market Insights

- Food and beverage applications account for more than 70% of global demand, making them the largest application segment for organic oat fiber.

- Soluble organic oat fiber remains the leading product category, supported by growing demand for beta-glucan-rich ingredients associated with cholesterol management and digestive health.

- North America dominates the global market, accounting for approximately 38% of total demand due to its mature organic food industry and advanced functional nutrition sector.

- Asia-Pacific is the fastest-growing regional market, fueled by increasing health awareness, expanding middle-class populations, and rising consumption of functional foods.

- Plant-based food manufacturers are increasingly incorporating organic oat fiber into dairy alternatives, meat substitutes, and vegan nutrition products to improve texture and nutritional value.

- Supply chain sustainability and organic certification standards are becoming critical competitive differentiators among ingredient suppliers globally.

Organic Oat Fiber Market Latest Trends

Growing Adoption in Functional and Gut Health Nutrition

Consumer focus on digestive health continues to reshape the global nutrition landscape, creating strong demand for organic oat fiber. Manufacturers are increasingly incorporating oat-derived fiber into functional foods, dietary supplements, meal replacements, and medical nutrition products due to its recognized role in promoting gut health and improving digestive function. Beta-glucan-rich oat fiber formulations are particularly gaining traction in products targeting cholesterol reduction, glycemic management, and microbiome support. As consumers seek preventive healthcare solutions, food manufacturers are launching fiber-enriched products with clean-label claims that emphasize natural, plant-based nutrition. This trend is expected to remain one of the strongest growth drivers throughout the forecast period.

Expansion of Plant-Based Food Applications

The global shift toward plant-based diets is creating new opportunities for organic oat fiber across multiple food categories. Manufacturers of oat milk, plant-based yogurts, meat alternatives, and vegan snacks are increasingly utilizing organic oat fiber as a natural stabilizer, bulking agent, and texture enhancer. Compared to synthetic additives, organic oat fiber offers superior clean-label positioning while contributing additional nutritional value. Product developers are leveraging oat fiber to improve mouthfeel, water retention, and shelf stability without compromising organic certification requirements. As plant-based product innovation accelerates globally, organic oat fiber is becoming an essential formulation ingredient across multiple consumer categories.

Organic Oat Fiber Market Drivers

Increasing Demand for Clean-Label Ingredients

Consumers increasingly prefer products formulated with recognizable, natural ingredients and minimal processing. This shift has encouraged food manufacturers to replace artificial additives and synthetic stabilizers with plant-based alternatives such as organic oat fiber. The ingredient supports multiple formulation objectives while maintaining organic and clean-label claims, making it highly attractive across food, beverage, and supplement applications. Regulatory support for transparency in food labeling further reinforces this trend, driving continued adoption among manufacturers seeking to improve product positioning and consumer trust.

Growing Awareness of Digestive Health Benefits

The growing prevalence of digestive disorders and increasing understanding of gut microbiome health are driving demand for dietary fiber ingredients globally. Organic oat fiber offers scientifically recognized digestive health benefits while supporting broader wellness objectives. Health-conscious consumers are actively seeking fiber-enriched foods and supplements, encouraging manufacturers to increase incorporation rates across packaged foods, nutritional beverages, and specialized health products. Rising healthcare costs and preventive health trends are further accelerating demand for fiber-based nutritional solutions.

Expansion of the Organic Food Industry

Global organic food sales continue to increase across both developed and emerging economies. Organic oat fiber directly benefits from this expansion as manufacturers seek certified organic ingredients that comply with increasingly stringent sourcing requirements. Growth in organic bakery products, cereals, snacks, dairy alternatives, and infant nutrition categories is generating significant downstream demand for organic oat fiber suppliers. Investments in organic agriculture and improvements in certification infrastructure are expected to support long-term market expansion.

Organic Oat Fiber Market Restraints

Limited Availability of Organic Raw Materials

Organic oat cultivation remains significantly smaller than conventional oat production globally. Supply constraints often create volatility in raw material availability, particularly during periods of adverse weather conditions or lower harvest yields. These limitations can impact procurement costs and restrict production scalability for ingredient manufacturers, creating challenges for long-term supply planning.

Premium Pricing Compared to Conventional Fiber Ingredients

Organic oat fiber commands a substantial price premium due to certification requirements, lower agricultural yields, and specialized supply chain management. This cost differential may limit adoption in highly price-sensitive food categories, particularly in emerging markets where affordability remains a key purchasing factor. Manufacturers must continuously balance premium positioning with cost competitiveness to expand adoption across broader application segments.

Organic Oat Fiber Industry Key Opportunities

Growth of Functional Foods and Preventive Nutrition

The functional foods industry represents one of the most significant opportunities for organic oat fiber suppliers. Consumers increasingly seek products that provide measurable health benefits beyond basic nutrition. Organic oat fiber's role in supporting digestive health, cholesterol management, and satiety positions it favorably within functional food categories. Product innovation in cereals, beverages, bakery products, and nutritional snacks is expected to generate substantial demand over the next decade.

Expansion Across Plant-Based Food Categories

Plant-based foods continue to outperform many conventional food categories globally. Organic oat fiber offers manufacturers a multifunctional ingredient capable of improving texture, moisture retention, and nutritional profiles while maintaining organic certification. The rapid growth of dairy alternatives, vegan nutrition products, and meat substitutes provides significant opportunities for suppliers capable of developing application-specific fiber solutions.

Emerging Demand Across Asia-Pacific

Asia-Pacific presents considerable untapped market potential. Rising disposable incomes, growing awareness of preventive healthcare, and increasing consumption of functional foods are driving demand for organic nutritional ingredients. China, India, Japan, and South Korea are emerging as major consumption centers. Companies establishing localized supply chains, distribution networks, and technical support capabilities are likely to gain competitive advantages as regional demand accelerates.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 502.00 Million |

| Market Size in 2026 | USD 541.16 Million |

| Market Size in 2031 | USD 787.80 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The soluble organic oat fiber segment dominated the global organic oat fiber market in 2025, accounting for approximately 46% of total market value. The segment's leadership is primarily driven by the high concentration of beta-glucan, a clinically recognized soluble dietary fiber associated with cholesterol reduction, cardiovascular health support, blood glucose management, and digestive wellness. Growing consumer preference for functional ingredients with scientifically validated health benefits has significantly accelerated the incorporation of soluble oat fiber into functional foods, fortified beverages, dietary supplements, meal replacement products, and heart-health formulations. Regulatory approvals and health claims related to beta-glucan in several developed markets have further strengthened demand. In addition, food manufacturers increasingly favor soluble oat fiber because of its superior water-binding capacity, viscosity enhancement, and formulation flexibility across a broad range of applications.Meanwhile, mixed and standardized organic oat fiber blends are emerging as an increasingly attractive category among food and beverage manufacturers. These customized solutions combine the benefits of both soluble and insoluble fibers while delivering improved processing performance, nutritional enhancement, and sensory characteristics. Manufacturers are investing in advanced processing technologies to develop tailored fiber concentrations, particle sizes, and functional properties that address specific formulation requirements across bakery, dairy alternatives, beverages, sports nutrition, and nutraceutical applications. The growing trend toward multifunctional ingredients and clean-label product development is expected to further support demand for customized oat fiber solutions throughout the forecast period.

Application Insights

The food and beverage segment accounted for approximately 72% of global organic oat fiber consumption in 2025, making it the largest application area. The segment's dominance is driven by increasing consumer demand for fiber-enriched foods, clean-label ingredients, and functional nutrition products. Organic oat fiber is extensively incorporated into bakery products, breakfast cereals, snacks, dairy alternatives, plant-based foods, and functional beverages due to its ability to enhance nutritional value while improving texture, moisture retention, and shelf stability. The growing popularity of digestive wellness products and preventive nutrition continues to encourage manufacturers to increase fiber fortification across mainstream food categories.Nutraceutical and dietary supplement applications are among the fastest-growing segments, supported by rising consumer awareness regarding gut health, cardiovascular wellness, weight management, and preventive healthcare. Increasing demand for fiber supplements, digestive health products, and functional nutrition formulations continues to create significant opportunities for organic oat fiber manufacturers.Pharmaceutical applications are expanding steadily through medical nutrition products, clinical dietary formulations, and digestive health therapies. Furthermore, animal nutrition and premium pet food applications are emerging as attractive growth areas as manufacturers increasingly utilize natural and organic fiber ingredients to support digestive health, nutrient absorption, and overall animal well-being. Growing premiumization trends in pet nutrition are expected to further strengthen demand during the forecast period.

Physical Form Insights

Powdered organic oat fiber represented approximately 68% of the global market in 2025, making it the dominant physical form segment. The segment's leadership is attributed to its superior handling characteristics, excellent dispersibility, ease of storage, and compatibility with large-scale automated food processing systems. Powdered oat fiber enables uniform ingredient distribution and consistent product quality, making it highly suitable for bakery products, nutritional beverages, dietary supplements, meal replacements, and processed food formulations. Growing industrial demand for efficient manufacturing processes and standardized ingredient performance continues to support segment growth.Flake and particulate oat fiber formats account for a smaller yet steadily growing market share. These products are primarily utilized in breakfast cereals, granola products, specialty bakery formulations, and premium nutrition applications where natural appearance and texture enhancement are important purchasing factors. As food manufacturers increasingly seek customized ingredient solutions, suppliers are expanding their portfolios to offer a broader range of particle sizes and physical formats tailored to specific end-use requirements.

End-Use Industry Insights

The food processing industry remained the largest end-use sector in 2025, accounting for approximately 65% of total market demand. The segment's dominance is supported by rising consumer demand for healthier food products, growing clean-label trends, and increasing incorporation of functional ingredients into mainstream food categories. Food manufacturers are increasingly utilizing organic oat fiber to improve nutritional profiles, support fiber-related labeling claims, and maintain desirable sensory characteristics without compromising product quality. Expanding demand for plant-based foods, fortified products, and functional snacks continues to strengthen market penetration across the food processing sector.Pharmaceutical companies are steadily incorporating organic oat fiber into medical nutrition products, digestive health formulations, and specialized dietary interventions. The growing focus on preventive healthcare and clinical nutrition is expected to create additional opportunities within this segment.The animal nutrition industry is witnessing increasing adoption of organic oat fiber as livestock producers and pet food manufacturers seek premium natural ingredients that support digestive efficiency and overall animal health. In addition, personal care and cosmetic manufacturers are exploring oat-derived ingredients for skincare, cleansing, and wellness-focused formulations due to their natural positioning and consumer appeal. Emerging applications in sports nutrition, active lifestyle products, and healthy aging formulations are expected to generate further growth opportunities throughout the forecast period.

Distribution Channel Insights

Direct business-to-business (B2B) sales accounted for approximately 58% of global market revenue in 2025, making it the leading distribution channel. The segment's dominance reflects the importance of long-term supplier relationships, product customization capabilities, technical support services, and quality assurance requirements. Large food manufacturers and nutraceutical companies typically procure organic oat fiber through direct sourcing agreements to ensure supply continuity, product consistency, and regulatory compliance. Increasing demand for customized ingredient specifications and strategic sourcing partnerships continues to strengthen the position of direct sales channels.Specialty organic ingredient suppliers are also strengthening their market presence as consumer demand for certified organic, non-GMO, and clean-label products continues to increase. These suppliers provide value-added services including certification support, traceability assurance, and technical consulting. Additionally, digital procurement platforms and online ingredient marketplaces are gaining traction by improving supplier visibility, streamlining sourcing processes, and facilitating global trade among food and nutrition manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Oat Fiber Market Segmentations

By Product Type

- Soluble Organic Oat Fiber

- Insoluble Organic Oat Fiber

- Mixed/Standardized Organic Oat Fiber Blends

By Physical Form

- Powder

- Granules

- Flakes/Fiber Particulates

By Functional Property

- Water-Binding Fiber

- Fat-Replacement Fiber

- Texture & Stabilization Fiber

- Digestive Health/Prebiotic Fiber

- Cholesterol Management Fiber

By Application

- Food & Beverage

- Nutraceuticals & Dietary Supplements

- Pharmaceuticals

- Animal Nutrition

- Personal Care & Cosmetics

By Distribution Channel

- Direct B2B Sales

- Ingredient Distributors

- Online Ingredient Platforms

- Specialty Organic Ingredient Suppliers

Regional Insights

North America

North America accounted for approximately 38% of the global organic oat fiber market in 2025, making it the largest regional market. The United States alone represents nearly 31% of global demand, supported by a highly developed organic food industry, strong consumer awareness regarding digestive health, and widespread adoption of functional nutrition products. The region benefits from advanced food processing infrastructure, a mature dietary supplement industry, and extensive organic farming capabilities. Canada plays a strategically important role as a leading producer and exporter of organic oats, supporting supply chain stability and raw material availability across the region.Regional growth is being driven by increasing consumer demand for clean-label and fiber-enriched foods, rising prevalence of lifestyle-related health conditions such as obesity and cardiovascular diseases, growing adoption of plant-based diets, and expanding consumption of functional beverages and nutritional supplements. Strong retail penetration of organic products, favorable regulatory support for health-focused food innovation, and continued investment in functional ingredient development are further accelerating market expansion across North America.

Europe

Europe accounted for approximately 32% of global market demand in 2025, positioning it as the second-largest regional market. Germany, the United Kingdom, France, Italy, and the Nordic countries serve as major consumption centers, while Germany alone accounts for roughly 8% of global consumption. The region benefits from high levels of consumer awareness regarding nutrition, sustainability, and natural ingredients. Strong demand for organic bakery products, functional foods, and plant-based nutrition continues to support market development.Growth across Europe is primarily driven by stringent food quality and labeling regulations, increasing consumer preference for clean-label and minimally processed products, growing demand for organic and sustainable food ingredients, and rising adoption of preventive healthcare practices. Furthermore, the expansion of vegan and flexitarian lifestyles, coupled with substantial investments in sustainable food production and circular agriculture initiatives, continues to stimulate demand for organic oat fiber across food, nutraceutical, and specialty nutrition applications.

Asia-Pacific

Asia-Pacific accounted for approximately 20% of global demand in 2025 and represents the fastest-growing regional market, expanding at a forecast CAGR exceeding 9%. China leads regional consumption owing to rapid growth in functional food manufacturing, increasing health-consciousness, and expanding demand for preventive nutrition products. Japan continues to generate strong demand due to its aging population and growing focus on digestive wellness and healthy aging. India is emerging as one of the fastest-growing national markets, supported by rising disposable incomes, expanding middle-class populations, and increasing awareness regarding nutritional health. South Korea and Australia also contribute significantly through advanced health food industries and growing demand for clean-label ingredients.The region's rapid growth is being driven by urbanization, rising healthcare expenditure, increasing prevalence of digestive and lifestyle-related health disorders, expanding functional food and dietary supplement industries, and growing consumer awareness regarding preventive healthcare. The continued expansion of organized retail channels, e-commerce platforms, and premium health food categories is further enhancing accessibility and accelerating market penetration throughout the Asia-Pacific region.

Latin America

Latin America accounted for approximately 5% of global market value in 2025, led by Brazil, Argentina, and Chile. Brazil remains the largest regional consumer due to its sizeable food processing industry, growing health-conscious population, and increasing adoption of functional food products. Although the regional market remains comparatively smaller than developed economies, demand for organic and natural ingredients continues to increase steadily.Regional growth is supported by expanding awareness of healthy eating habits, increasing penetration of organic and functional food products, rising investments in food processing modernization, and growing availability of premium nutrition products through modern retail channels. Improvements in organic agriculture practices, expanding middle-income consumer groups, and increasing demand for clean-label ingredients among domestic food manufacturers are expected to support sustained market development over the forecast period.

Middle East & Africa

The Middle East & Africa region contributed approximately 5% of global demand in 2025. The United Arab Emirates and Saudi Arabia lead regional consumption through significant imports of premium health foods, dietary supplements, and functional nutrition products. South Africa remains the largest market within Africa due to its relatively developed food processing industry and growing health-conscious consumer base.Growth across the region is being driven by rising disposable incomes, increasing consumer awareness regarding nutrition and wellness, expanding premium food and beverage sectors, and growing demand for imported organic ingredients. Government initiatives promoting healthier lifestyles, increasing investment in modern retail infrastructure, and the gradual expansion of functional food and dietary supplement categories are expected to create new opportunities for organic oat fiber manufacturers. The growing popularity of preventive healthcare and wellness-oriented consumer spending patterns is likely to further support long-term market expansion across the Middle East and Africa.

Key Players in the Organic Oat Fiber Market

- Grain Millers

- Lantmännen

- J. Rettenmaier & Söhne (JRS)

- Swedish Oat Fiber

- La Crosse Milling

- Richardson International

- Avena Foods

- InterFiber

- Nature's Path Ingredients

- FutureCeuticals

- NuNaturals

- Healthy Food Ingredients

- Canadian Organic Oat Milling

- Golden Prairie Oats

- The Green Labs