Organic Apple Juice Market Size

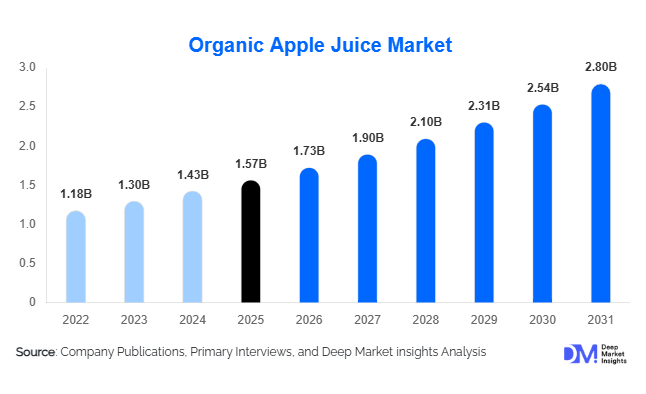

According to Deep Market Insights, the global organic apple juice market size was valued at USD 1.57 billion in 2025 and is projected to grow from USD 1.73 billion in 2026 to reach USD 2.80 billion by 2031, expanding at a CAGR of 10.1% during the forecast period (2026–2031). The organic apple juice market growth is primarily driven by increasing consumer preference for clean-label beverages, rising demand for organic and pesticide-free food products, expanding awareness of health and wellness, and growing adoption of sustainable agricultural practices. Consumers worldwide are increasingly shifting away from carbonated beverages and artificial fruit drinks toward natural juice products that offer perceived nutritional benefits and align with organic lifestyles. Furthermore, premiumization trends in the beverage industry, coupled with expanding retail availability and e-commerce penetration, are supporting long-term market expansion.

Key Market Insights

- Organic apple juice is increasingly positioned as a premium health beverage, benefiting from consumer demand for clean-label, non-GMO, and pesticide-free products.

- Not-from-concentrate (NFC) and cold-pressed organic apple juice categories are witnessing rapid adoption, particularly among health-conscious consumers seeking minimally processed beverages.

- North America dominates the global market, supported by high organic food consumption, strong retail infrastructure, and premium consumer spending.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, expanding middle-class populations, and growing awareness of organic nutrition.

- Functional organic beverages are creating new revenue streams, with manufacturers introducing vitamin-enriched, antioxidant-fortified, and probiotic-infused apple juice variants.

- Sustainable packaging innovations, including recyclable cartons, biodegradable materials, and carbon-neutral production initiatives, are becoming major differentiators among leading brands.

Organic Apple Juice Market Latest Trends

Functional Organic Beverages Transforming Product Innovation

The organic apple juice industry is increasingly converging with the functional beverage sector. Manufacturers are launching products fortified with probiotics, vitamins, minerals, botanical extracts, and immunity-supporting ingredients to meet evolving consumer preferences. Health-conscious consumers are seeking beverages that provide benefits beyond hydration, creating strong demand for functional organic juice products. Premium juice brands are introducing formulations focused on digestive health, immune support, antioxidant enhancement, and sports recovery. This trend is allowing producers to command higher margins while differentiating their offerings in an increasingly competitive marketplace. The integration of functional ingredients is particularly gaining traction in North America, Europe, Japan, and South Korea, where consumers actively seek wellness-oriented food and beverage products.

Sustainable Packaging and Regenerative Agriculture Gaining Momentum

Sustainability is becoming a central purchasing criterion across global beverage markets. Organic apple juice producers are increasingly investing in recyclable cartons, lightweight packaging materials, renewable energy-powered manufacturing facilities, and sustainable sourcing programs. Several brands are adopting regenerative agriculture practices that improve soil health, biodiversity, and carbon sequestration. Consumers are responding positively to products that combine organic certification with broader environmental commitments. Retailers are also prioritizing suppliers with strong environmental, social, and governance (ESG) credentials. Carbon footprint disclosures, traceability systems, and transparent sourcing initiatives are becoming important competitive differentiators within premium organic beverage categories.

Organic Apple Juice Market Drivers

Growing Consumer Preference for Organic and Clean-Label Products

Global demand for organic food and beverages continues to expand as consumers increasingly prioritize health, nutrition, and food safety. Organic apple juice benefits from strong consumer perceptions regarding purity, sustainability, and nutritional quality. Growing awareness of pesticide residues, artificial additives, and synthetic ingredients in conventional food products is encouraging consumers to switch toward certified organic alternatives. The trend is particularly strong among millennials, families with children, and affluent urban consumers who are willing to pay premium prices for healthier beverage options.

Shift Away from Carbonated and Sugary Beverages

Consumers are actively reducing consumption of carbonated soft drinks and beverages containing artificial sweeteners. Organic apple juice is benefiting from this shift by positioning itself as a naturally sweet and healthier alternative. Increasing concerns regarding obesity, diabetes, and lifestyle-related health conditions are driving demand for beverages perceived as more natural and nutritious. Many consumers are replacing traditional sugary drinks with organic fruit juices as part of broader wellness-focused dietary changes.

Expansion of Retail and E-Commerce Distribution Networks

The rapid growth of organized retail, specialty organic stores, and online grocery platforms has significantly improved product accessibility. Major supermarket chains are expanding organic product assortments, while digital commerce platforms enable consumers to access premium organic beverages regardless of location. Subscription models, direct-to-consumer channels, and online health food retailers are further supporting market growth by improving convenience and product availability.

Organic Apple Juice Market Restraints

High Production and Certification Costs

Organic apple cultivation requires adherence to strict farming standards, lower chemical inputs, and extensive certification requirements. These factors increase production costs compared with conventional apple juice manufacturing. Certification audits, traceability systems, and compliance requirements further add to operational expenses. Consequently, organic apple juice products often carry significant price premiums, which can limit adoption among price-sensitive consumers.

Supply Chain Constraints and Raw Material Availability

The availability of certified organic apples remains limited in several regions. Seasonal fluctuations, adverse weather conditions, climate-related production risks, and supply chain disruptions can impact raw material availability and pricing. Maintaining organic integrity throughout cultivation, processing, storage, and transportation also presents logistical challenges for manufacturers operating across multiple markets.

Organic Apple Juice Industry Key Opportunities

Expansion Across Emerging Asian Markets

Asia-Pacific represents the most significant growth opportunity for organic apple juice producers. Rising middle-class populations, increasing disposable incomes, growing urbanization, and greater health awareness are driving demand for premium organic beverages across China, India, Southeast Asia, and South Korea. Companies investing in local production, regional distribution networks, and market-specific product development are expected to capture substantial growth opportunities. The increasing popularity of imported organic products further supports premium positioning strategies in these markets.

Development of Functional and Premium Product Categories

The convergence of organic beverages and functional nutrition presents substantial opportunities for market participants. Manufacturers can introduce premium formulations featuring probiotics, antioxidants, adaptogens, and vitamin enrichment to address consumer demand for health-focused beverages. Functional organic apple juice products command higher average selling prices and offer opportunities to improve profitability. Innovations targeting immunity support, digestive wellness, sports nutrition, and healthy aging are expected to drive future market differentiation and revenue growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.57 Billion |

| Market Size in 2026 | USD 1.73 Billion |

| Market Size in 2031 | USD 2.80 Billion |

| CAGR | 10.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

The 100% organic apple juice segment continues to dominate the global organic apple juice market, accounting for approximately 39% of total market revenue in 2025. The segment’s leadership is primarily driven by growing consumer preference for clean-label beverages that contain no artificial preservatives, additives, sweeteners, or synthetic ingredients. Rising awareness regarding natural nutrition, digestive health, and immunity support has encouraged consumers to shift toward minimally processed fruit-based beverages, further strengthening demand for pure organic apple juice products. In both developed and emerging markets, consumers increasingly perceive 100% organic juice as a healthier alternative to carbonated soft drinks and artificially flavored beverages.Organic apple juice concentrate continues to maintain a significant share of the market due to its extensive use across food processing, beverage manufacturing, bakery products, dairy applications, and functional beverage formulations. The segment benefits from cost efficiency, extended shelf life, ease of transportation, and versatility in industrial applications. Meanwhile, not-from-concentrate (NFC) organic apple juice is emerging as one of the fastest-growing product categories as consumers increasingly associate NFC products with superior taste, freshness, authenticity, and nutritional quality. Premiumization trends across North America, Europe, and Asia-Pacific are accelerating demand for NFC offerings.Cloudy organic apple juice is also witnessing substantial growth as consumers increasingly associate naturally cloudy products with higher fiber content, greater retention of phytonutrients, and lower levels of processing. Manufacturers are actively leveraging these perceptions to position cloudy juice products as more natural and nutritionally superior alternatives. In addition, premium single-origin, artisanal, and farm-traceable organic apple juice products are expanding rapidly within mature markets, supported by rising consumer interest in product transparency, sustainability, local sourcing, and traceability throughout the supply chain.

Processing Technology Insights

Pasteurized organic apple juice accounted for approximately 42% of global market revenue in 2025, making it the leading processing technology segment. The segment's dominance is driven by its ability to ensure product safety, maintain quality consistency, extend shelf life, and support large-scale distribution through modern retail and international trade channels. Pasteurization remains the preferred technology among major manufacturers because it enables efficient transportation and storage while meeting stringent food safety regulations across key markets.At the same time, changing consumer preferences toward fresh, minimally processed beverages are creating significant growth opportunities for advanced processing technologies. Cold-pressed organic apple juice continues to gain traction among health-conscious consumers due to its perceived nutritional superiority, enhanced flavor retention, and premium positioning. Similarly, high-pressure processing (HPP) technology is experiencing strong adoption because it effectively extends shelf life while preserving vitamins, antioxidants, color, aroma, and fresh juice characteristics. These technologies are increasingly being utilized by premium organic beverage manufacturers seeking product differentiation and higher value realization.Unpasteurized organic apple juice remains a relatively niche segment, primarily serving specialty organic stores, local farmers’ markets, and direct-to-consumer distribution channels. However, rising investments in innovative processing technologies, automation, and preservation solutions are expected to enhance product quality and support premiumization strategies across the organic apple juice industry over the forecast period.

Packaging Format Insights

Carton packaging remains the leading packaging format in the global organic apple juice market, representing approximately 34% of total revenue in 2025. The segment’s leadership is supported by growing consumer and retailer preference for environmentally responsible packaging solutions. Cartons offer advantages including lower transportation costs, lightweight design, high recyclability, reduced carbon footprint, and improved shelf efficiency. Increasing regulatory emphasis on sustainable packaging and corporate sustainability initiatives are further accelerating carton adoption across major beverage manufacturers.Glass bottles continue to maintain a strong presence within premium and artisanal organic apple juice categories, particularly across Europe and North America. Consumers often associate glass packaging with superior product quality, premium positioning, and preservation of flavor integrity. As a result, premium brands frequently utilize glass packaging to reinforce product authenticity and sustainability credentials.PET bottles remain widely used due to their affordability, durability, convenience, and widespread compatibility with modern retail distribution systems. Meanwhile, pouches and cans are gaining popularity among younger consumers and urban populations seeking portable, single-serve beverage solutions. Across all packaging formats, manufacturers are increasingly investing in renewable materials, recycled content, lightweight packaging technologies, and circular economy initiatives to align with evolving sustainability expectations and regulatory requirements.

Distribution Channel Insights

Supermarkets and hypermarkets accounted for approximately 37% of global organic apple juice sales in 2025, making them the largest distribution channel. The segment’s dominance is primarily driven by extensive product availability, strong consumer footfall, established supply chain networks, and increasing shelf space dedicated to organic food and beverage products. Major retail chains continue expanding their organic product portfolios, allowing consumers greater access to a broad range of organic apple juice offerings across multiple price points and packaging formats.Specialty organic stores remain an important distribution channel, particularly for premium and niche brands targeting health-conscious consumers seeking certified organic, locally sourced, and sustainably produced products. These stores play a critical role in educating consumers and supporting premium product positioning.Online retail represents one of the fastest-growing distribution channels as digital commerce adoption continues to accelerate globally. The increasing popularity of e-commerce platforms, subscription-based beverage services, mobile shopping applications, and direct home delivery models is expanding market reach and improving product accessibility. Direct-to-consumer distribution models are also gaining momentum as brands seek stronger customer relationships, enhanced consumer insights, improved brand loyalty, and higher profit margins through reduced dependence on intermediaries.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for approximately 61% of global market demand in 2025. The segment's leadership is primarily driven by rising health awareness, growing preference for natural beverages among families, increasing demand for nutritious breakfast beverages, and consumer efforts to reduce consumption of sugary soft drinks. Parents are increasingly choosing organic fruit juices as healthier beverage alternatives for children, while adult consumers continue seeking functional and naturally sourced nutritional products.The foodservice sector represents a growing opportunity for market participants as restaurants, cafés, hotels, resorts, and premium dining establishments increasingly incorporate organic beverages into their menus to meet changing consumer preferences. Growing demand for premium dining experiences and clean-label beverage options is supporting steady expansion within this segment.The nutraceutical and functional beverage industries are witnessing particularly strong growth as manufacturers increasingly utilize organic apple juice as a natural base ingredient for health-oriented formulations. Organic apple juice is being incorporated into immunity-support beverages, wellness drinks, probiotic formulations, fortified juices, and functional nutrition products. Beverage manufacturers are also increasing utilization of organic apple juice in blended fruit juices, kombucha products, plant-based beverages, fermented drinks, and other value-added beverage applications, creating additional demand across industrial end-use categories.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Apple Juice Market Segmentations

By Product Form

- 100% Organic Apple Juice

- Organic Apple Juice Concentrate

- Organic Not-From-Concentrate (NFC) Apple Juice

- Organic Cloudy Apple Juice

- Organic Clear Apple Juice

By Processing Technology

- Cold-Pressed Organic Apple Juice

- Conventional Pressed Organic Apple Juice

- High Pressure Processed (HPP) Organic Apple Juice

- Pasteurized Organic Apple Juice

- Unpasteurized Organic Apple Juice

By Packaging Format

- Glass Bottles

- PET Bottles

- Carton Packaging

- Pouches

- Cans

- Bulk Industrial Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Organic Stores

- Online Retail/E-Commerce

- Direct-to-Consumer Channels

- Foodservice & HoReCa

- Institutional Sales

By End Use

- Household Consumption

- Foodservice Industry

- Beverage Manufacturing

- Dairy & Plant-Based Beverage Industry

- Bakery & Confectionery Industry

- Nutraceutical & Functional Beverage Industry

- Hospitality Industry

Regional Insights

North America

North America accounted for approximately 36% of global organic apple juice market revenue in 2025, making it the largest regional market. The United States alone represented nearly 29% of global revenue, supported by strong organic food penetration, high consumer purchasing power, advanced retail infrastructure, and widespread product availability across supermarkets, specialty stores, and e-commerce channels. The region benefits from a highly developed organic certification framework and strong consumer trust in organic labeling standards.Market growth across North America is being driven by increasing demand for clean-label beverages, growing health and wellness awareness, rising concerns regarding artificial ingredients and added sugars, and expanding consumer preference for sustainably sourced products. The rapid growth of premium organic beverages, functional nutrition products, and direct-to-consumer retail channels is further supporting market expansion. Additionally, strong investments in sustainable packaging, product innovation, and advanced processing technologies continue to strengthen regional competitiveness. Canada also contributes significantly to regional demand, supported by growing environmental awareness, expanding organic food consumption, and favorable government support for sustainable agriculture.

Europe

Europe represented approximately 31% of global organic apple juice market revenue in 2025, making it the second-largest regional market. Germany remains the largest market within the region, accounting for nearly 9% of global demand, supported by high levels of organic food consumption, strong environmental consciousness, and established sustainability practices. France, the United Kingdom, Italy, and Spain continue to experience steady growth as consumers increasingly prioritize natural and organic food products.The region’s growth is driven by stringent food quality regulations, strong adoption of organic certification standards, increasing consumer preference for sustainable products, and growing demand for premium fruit-based beverages. Europe also benefits from high levels of environmental awareness and widespread support for circular economy initiatives, which encourage sustainable production and packaging practices. Poland plays a strategic role as both a major producer and exporter of organic apple juice products, benefiting from extensive apple cultivation, competitive production costs, and strong export-oriented manufacturing capabilities. Rising demand for traceable, locally sourced, and minimally processed beverages is expected to further support regional market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR of approximately 12.4% through 2031. China remains the largest market within the region, driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing awareness of premium health-oriented beverages. Consumers are increasingly shifting toward organic and natural products as concerns regarding food quality, nutrition, and wellness continue to rise.The region’s strong growth is supported by increasing health consciousness, expanding modern retail infrastructure, rapid e-commerce penetration, growing demand for imported premium food products, and rising government initiatives promoting organic agriculture. India represents the fastest-growing country globally, with forecast growth exceeding 13.5%, driven by increasing organic food adoption, rising household incomes, growing awareness of preventive healthcare, and expanding availability of organic products through both retail and digital channels. Japan and South Korea continue supporting demand for premium, high-quality organic beverages, while Australia remains a mature market characterized by strong organic food consumption, sustainability-focused purchasing behavior, and high consumer willingness to pay for premium products.

Latin America

Latin America accounted for approximately 6% of global organic apple juice demand in 2025. Brazil remains the largest market in the region, supported by increasing health awareness, expanding middle-class consumption, modern retail development, and growing interest in premium beverage products. Argentina and Chile are also witnessing gradual growth as consumer awareness of organic nutrition and healthy lifestyles continues to improve.Regional market growth is being driven by increasing urbanization, rising disposable incomes, expanding supermarket penetration, growing demand for natural beverages, and strengthening export opportunities for organic agricultural products. Improvements in organic farming practices, greater participation in international organic trade, and rising investments in sustainable agriculture are expected to further enhance market development across the region over the forecast period.

Middle East & Africa

The Middle East and Africa accounted for approximately 5% of global organic apple juice market revenue in 2025. The United Arab Emirates and Saudi Arabia represent key growth markets due to high purchasing power, increasing demand for imported premium food products, and expanding consumer interest in health-focused lifestyles. South Africa remains the most developed organic beverage market in the region, supported by rising health awareness, improving retail infrastructure, and increasing product availability.Regional growth is being driven by expanding premium food retail networks, growing expatriate populations, increasing awareness of nutrition and wellness, rising demand for clean-label imported products, and continued modernization of food distribution systems. Furthermore, increasing investments in organized retail, hospitality, tourism, and premium grocery channels are creating favorable conditions for the expansion of organic beverage consumption. As consumer education regarding organic products continues to improve, the region is expected to witness sustained long-term market growth.

Key Players in the Organic Apple Juice Market

- Tree Top Inc.

- Martinelli's

- Eden Foods

- Voelkel GmbH

- James White Drinks

- Biona Organic

- Hollinger

- Beutelsbacher Fruchtsaftkelterei

- Manzana Products

- Lakewood Organic

- Rabenhorst

- Bioitalia

- Uncle Matt's Organic

- Whole Earth Brands

- Nature's Finest Foods