Orange Juice Market Size

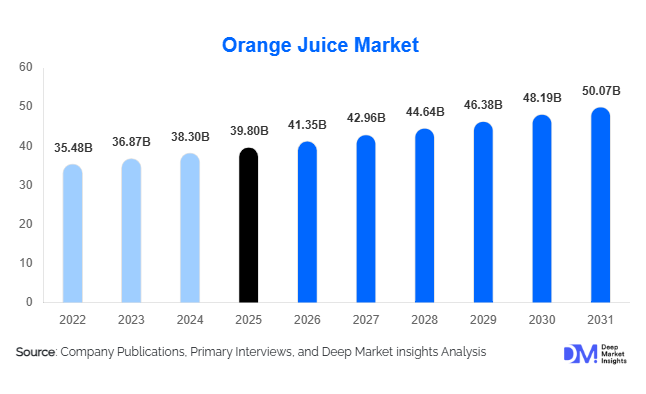

According to Deep Market Insights, the global orange juice market size was valued at approximately USD 39.8 billion in 2025 and is projected to grow from USD 41.35 billion in 2026 to reach USD 50.07 billion by 2031, expanding at a CAGR of 3.9% during the forecast period (2026–2031). The orange juice market growth is supported by increasing consumer preference for natural and functional beverages, rising awareness of immunity-enhancing nutrition, and growing demand for premium Not-From-Concentrate (NFC) juice products. Market expansion is further driven by innovations in cold-pressed and high-pressure processing technologies, increasing penetration of organized retail channels, and rising consumption across emerging economies. Despite challenges associated with citrus supply volatility and raw material pricing fluctuations, orange juice continues to maintain a strong position within the global fruit beverage industry due to its established consumer base and nutritional profile.

Key Market Insights

- Not-From-Concentrate (NFC) orange juice remains the largest product category, accounting for approximately 42% of global market value due to premium positioning and consumer preference for minimally processed beverages.

- Functional and fortified orange juice products are witnessing accelerated demand, particularly formulations enriched with vitamin D, probiotics, zinc, and immunity-support ingredients.

- North America dominates the global market, supported by high household consumption, premium product adoption, and established breakfast beverage habits.

- Asia-Pacific represents the fastest-growing regional market, led by increasing consumption in China, India, Indonesia, and South Korea.

- Supermarkets and hypermarkets account for the largest distribution share, contributing approximately 38% of global orange juice sales.

- Sustainability initiatives and recyclable packaging adoption are increasingly influencing purchasing decisions across developed markets.

- Supply-side investments in processing automation and disease-resistant citrus cultivation are becoming critical for long-term industry stability.

Orange Juice Market Latest Trends

Premium Not-From-Concentrate (NFC) Products Continue to Gain Market Share

Consumer demand for premium beverage products has significantly accelerated the adoption of NFC orange juice globally. Compared to concentrate-based alternatives, NFC products are perceived as fresher, less processed, and nutritionally superior. Major beverage manufacturers are expanding their premium juice portfolios through cold-chain distribution, advanced aseptic packaging, and clean-label formulations. In developed markets such as the United States, Germany, the United Kingdom, and Canada, consumers are increasingly willing to pay premium prices for authentic fruit content and minimal processing. The trend is also spreading across emerging economies where rising disposable incomes are supporting premium beverage purchases. As a result, NFC products are expected to remain the fastest-growing segment throughout the forecast period.

Functional and Health-Oriented Beverage Innovation

Orange juice manufacturers are increasingly integrating functional ingredients to meet evolving consumer wellness preferences. Products fortified with probiotics, vitamins, minerals, collagen, electrolytes, and immune-support compounds are becoming mainstream across retail shelves. This trend is particularly prominent in North America, Europe, Japan, and South Korea, where consumers actively seek beverages that provide health benefits beyond hydration. Companies are also introducing low-sugar and reduced-calorie formulations to address growing concerns regarding sugar intake. The convergence of traditional fruit juice and functional nutrition is creating premiumization opportunities and supporting higher margins across the industry.

Orange Juice Market Drivers

Growing Consumer Focus on Health and Immunity

Health-conscious consumers continue to prioritize beverages perceived as natural sources of essential nutrients. Orange juice remains strongly associated with vitamin C intake, immune system support, and overall wellness. Following increased health awareness globally, consumers are actively replacing carbonated soft drinks with healthier beverage alternatives. The market benefits from strong nutritional positioning, particularly among households seeking natural products for daily consumption. Rising awareness regarding preventive health management is expected to sustain demand across both developed and emerging markets.

Expansion of Organized Retail and E-Commerce Channels

The growth of supermarkets, hypermarkets, convenience retail networks, and online grocery platforms has significantly improved orange juice accessibility worldwide. Modern retail formats provide manufacturers with greater shelf visibility, promotional opportunities, and product differentiation capabilities. E-commerce channels have become particularly important for premium and organic juice brands, allowing direct consumer engagement and subscription-based purchasing models. Emerging markets including India, China, and Southeast Asia are witnessing rapid retail modernization, which is expected to support future market expansion.

Premiumization and Product Innovation

Consumers increasingly value premium beverage experiences that emphasize freshness, authenticity, and nutritional quality. This trend has encouraged manufacturers to launch organic, cold-pressed, NFC, and fortified orange juice products. Product innovation allows brands to capture higher-value consumer segments while differentiating themselves in an increasingly competitive marketplace. Investments in processing technologies such as High Pressure Processing (HPP) and aseptic filling systems are enabling producers to maintain product quality while extending shelf life.

Orange Juice Market Restraints

Raw Material Supply Volatility and Citrus Disease

Orange juice production remains heavily dependent on orange harvest yields, which are increasingly affected by climate variability, drought conditions, hurricanes, and citrus greening disease. Major producing regions such as Brazil and Florida have experienced production disruptions that have impacted global concentrate availability and pricing. These supply uncertainties create margin pressure for manufacturers and increase market volatility.

Competition from Alternative Beverage Categories

The market faces increasing competition from flavored water, plant-based beverages, kombucha, sports drinks, energy beverages, and functional wellness products. Many competing categories promote lower sugar content and innovative health benefits, attracting younger consumers. To maintain market relevance, orange juice producers must continue innovating through functional formulations, reduced-sugar variants, and premium product offerings.

Orange Juice Industry Key Opportunities

Expansion of Functional and Fortified Orange Juice Products

The functional beverage segment represents one of the most attractive opportunities within the global orange juice market. Consumers increasingly seek beverages that support immunity, digestive health, hydration, and overall wellness. Orange juice fortified with probiotics, vitamin D, zinc, magnesium, collagen, and plant-based nutrients can command premium pricing while enhancing brand differentiation. Existing market participants can leverage established manufacturing infrastructure to launch value-added products, while new entrants can focus on specialized health-oriented formulations targeting specific consumer needs. Functional beverage growth is expected to outperform conventional juice categories throughout the forecast period.

Untapped Growth Potential Across Asia-Pacific Markets

Asia-Pacific remains significantly underpenetrated compared with North America and Europe in terms of per-capita orange juice consumption. Rising urbanization, expanding middle-class populations, increasing disposable incomes, and growing awareness regarding healthy beverage choices are creating substantial growth opportunities. Countries such as China, India, Indonesia, Vietnam, and the Philippines are witnessing strong demand for packaged beverages. Premium imported products and locally produced NFC variants are increasingly gaining consumer acceptance, making the region one of the most attractive investment destinations for global orange juice manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 39.80 Billion |

| Market Size in 2026 | USD 41.35 Billion |

| Market Size in 2031 | USD 50.07 Billion |

| CAGR | 3.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global orange juice market is segmented into Not-From-Concentrate (NFC), From-Concentrate (FC), functional and fortified orange juice, and fresh-squeezed orange juice products. Among these, Not-From-Concentrate (NFC) orange juice dominates the market, accounting for approximately 42% of total market value in 2025. The segment’s leadership is primarily driven by growing consumer preference for products perceived as fresh, natural, and minimally processed. Increasing awareness regarding nutritional retention, authentic taste profiles, and clean-label formulations has further strengthened demand for NFC products across developed and emerging markets. Premiumization trends within the beverage industry continue to encourage consumers to shift toward higher-value NFC offerings, particularly in North America and Europe.Fresh-squeezed orange juice continues to generate strong demand across foodservice establishments, premium cafés, hotels, restaurants, juice bars, and specialty retail outlets. Consumers increasingly associate freshly prepared juices with superior quality, authenticity, and nutritional value, supporting premium pricing opportunities within this segment. The rising popularity of experiential dining, healthy beverage consumption, and customized nutrition trends is expected to further support demand for fresh-squeezed orange juice over the forecast period.

Processing Technology Insights

The market is categorized into conventional pasteurization, High Pressure Processing (HPP), cold-pressed processing, and aseptic processing technologies. Conventional pasteurization remains the leading processing technology, accounting for nearly 58% of global market revenue. Its dominance is attributed to proven food safety performance, cost efficiency, scalability, and compatibility with large-scale industrial production systems. The technology remains widely adopted by major manufacturers due to its ability to ensure product stability while supporting global distribution networks.However, changing consumer preferences toward minimally processed beverages are accelerating the adoption of High Pressure Processing (HPP) and cold-pressed technologies. These advanced processing methods enable manufacturers to preserve flavor integrity, color, aroma, and nutritional content more effectively than traditional thermal processing techniques. As consumers increasingly prioritize freshness and clean-label products, premium beverage brands are investing heavily in HPP and cold-pressed production capabilities to differentiate their offerings and capture higher-margin market opportunities.Aseptic processing technologies continue to gain traction globally due to their ability to extend shelf life without excessive preservative use while maintaining product quality. The technology also supports efficient international distribution and reduces cold-chain dependency in certain markets. Continuous technological innovation across processing systems is enabling manufacturers to improve operational efficiency, reduce food waste, enhance product safety, and meet growing consumer demand for high-quality, minimally processed orange juice products.

Distribution Channel Insights

The orange juice market is distributed through supermarkets and hypermarkets, convenience stores, online retail platforms, specialty stores, and foodservice distributors. Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 38% of global orange juice sales. The segment benefits from extensive product assortments, strong promotional activities, established consumer trust, and the ability to offer products across multiple price points and packaging formats. Large retail chains also provide manufacturers with significant visibility and shelf presence, further reinforcing channel dominance.Online retail and direct-to-consumer channels are emerging as the fastest-growing distribution segment, driven by increasing internet penetration, smartphone adoption, digital payment infrastructure, and changing grocery purchasing behaviors. Consumers are increasingly utilizing e-commerce platforms for beverage purchases due to convenience, broader product selection, subscription-based purchasing options, and home delivery services. Foodservice distributors also represent a strategically important channel, supplying hotels, restaurants, cafés, quick-service restaurants, catering operators, and institutional buyers with both fresh and packaged orange juice products. The continued recovery and expansion of the global hospitality industry is expected to further support demand through foodservice distribution networks.

End-Use Insights

Based on end use, the market is segmented into household consumption, foodservice applications, beverage manufacturing, and institutional consumption. Household consumption represents the largest end-use segment, accounting for approximately 61% of global demand. The segment's dominance is primarily driven by orange juice's long-established position as a staple breakfast beverage, combined with increasing consumer focus on healthy lifestyle choices and nutritional intake. Rising awareness regarding vitamin C content, immune health benefits, and natural fruit-based nutrition continues to support strong household consumption patterns worldwide.Beverage manufacturers increasingly utilize orange juice as a key ingredient in smoothies, blended fruit beverages, sports drinks, functional beverages, wellness formulations, and premium juice blends. The growing popularity of functional nutrition and value-added beverages is creating new opportunities for orange juice incorporation across multiple beverage categories. Institutional demand from schools, hospitals, corporate cafeterias, and healthcare facilities also contributes significantly to overall consumption, supported by initiatives promoting healthier beverage alternatives within institutional foodservice environments.

Price Positioning Insights

The market is segmented into economy, mid-priced, premium, and super-premium product categories. Mid-priced orange juice products account for the largest market share, representing approximately 44% of global revenue. The segment benefits from its ability to balance affordability, quality perception, product accessibility, and brand recognition. Consumers increasingly seek products that deliver both value and nutritional benefits, making mid-priced offerings particularly attractive across a broad range of income groups.Premium and super-premium categories are witnessing robust expansion, driven by growing demand for organic certification, cold-pressed processing methods, NFC positioning, sustainable sourcing, clean-label formulations, and functional ingredient enrichment. Consumers are increasingly willing to pay premium prices for products that align with health, wellness, sustainability, and quality expectations. As a result, premium segments are generating higher profit margins and becoming increasingly important for leading beverage companies seeking value-based growth and product differentiation strategies.

Explore more data points, trends and opportunities Download Free Sample Report

Orange Juice Market Segmentations

By Product Type

- Not-From-Concentrate (NFC) Orange Juice

- From-Concentrate (FC) Orange Juice

- Fresh-Squeezed Orange Juice

- Functional & Fortified Orange Juice

By Processing Technology

- Conventional Pasteurized

- High Pressure Processing (HPP)

- Cold-Pressed

- Aseptic Processed

- Flash Pasteurized

By Nature

- Conventional

- Organic

By Packaging Format

- Cartons (Tetra Pak)

- PET Bottles

- Glass Bottles

- Cans

- Flexible Pouches

- Bag-in-Box Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Grocery Chains

- Club Stores & Cash-and-Carry

- Online Retail / E-Commerce

- Direct-to-Consumer (D2C)

- Foodservice Distributors

Regional Insights

North America

North America accounts for approximately 31% of the global orange juice market, making it the largest regional contributor. The United States alone represents nearly 24% of global demand, supported by strong household consumption, widespread retail penetration, and high consumer awareness regarding fruit-based nutrition. Canada continues to experience rising demand for organic, functional, and premium juice offerings as consumers increasingly prioritize wellness-focused beverage choices.Regional growth is primarily driven by growing demand for Not-From-Concentrate (NFC) products, increasing premiumization across beverage categories, rising adoption of functional and fortified juices, and continuous product innovation from leading manufacturers. Strong retail infrastructure, advanced cold-chain logistics, expanding e-commerce grocery sales, and increasing consumer willingness to pay for clean-label and minimally processed beverages further support market expansion. Additionally, growing health consciousness, aging populations seeking nutritional beverages, and sustained innovation in packaging formats continue to create favorable market conditions across North America.

Europe

Europe represents approximately 28% of global market value, with Germany, France, the United Kingdom, Spain, Italy, and the Netherlands serving as major consumption centers. Germany accounts for nearly 7% of global demand and remains one of the world's largest per-capita consumers of orange juice. The region is characterized by mature consumption patterns, strong brand presence, and well-developed retail distribution networks.Regional growth is being supported by increasing consumer preference for organic beverages, sustainability-focused purchasing decisions, and growing demand for clean-label products. Rising environmental awareness has encouraged manufacturers to invest in recyclable packaging, sustainable sourcing initiatives, and reduced-carbon supply chains. Demand for premium NFC and cold-pressed products continues to increase as consumers seek higher-quality beverage options with perceived nutritional advantages. Furthermore, Europe's advanced retail ecosystem, stringent quality standards, and high consumer awareness regarding health and nutrition continue to provide a stable foundation for long-term market growth.

Asia-Pacific

Asia-Pacific accounts for approximately 22% of global demand and represents the fastest-growing regional market, with an estimated CAGR exceeding 5.5% through 2031. China remains the largest regional market, while India is projected to be the fastest-growing country globally due to its expanding middle-class population, rising disposable incomes, and increasing health awareness. Japan and South Korea continue to drive demand for premium, fortified, and functional juice products.The region's growth is being fueled by rapid urbanization, expanding modern retail infrastructure, rising consumption of packaged beverages, and increasing awareness of preventive healthcare and nutritional wellness. Growing youth populations, changing dietary habits, and greater exposure to global beverage trends are encouraging consumers to incorporate fruit-based drinks into daily consumption patterns. The rapid expansion of e-commerce channels, convenience retail networks, and organized foodservice sectors across Southeast Asia is further accelerating market penetration. Additionally, increasing demand for immunity-supporting beverages and functional nutrition products continues to create substantial growth opportunities throughout the region.

Latin America

Latin America contributes approximately 12% of global market value and remains strategically important due to its substantial orange production capabilities and integrated processing infrastructure. Brazil dominates both regional production and consumption while maintaining its position as the world's largest orange juice exporter. Mexico and Argentina continue to demonstrate stable demand growth driven by urban consumption patterns and expanding foodservice sectors.Regional growth is supported by abundant citrus cultivation, strong export-oriented production capacity, favorable climatic conditions for orange farming, and continuous investments in juice processing technologies. Rising urbanization, increasing disposable incomes, and growing adoption of packaged beverages are contributing to higher domestic consumption across several countries. In addition, the region's critical role in global orange juice exports, combined with ongoing investments in agricultural productivity, supply chain modernization, and processing efficiency, continues to strengthen its strategic importance within the global market.

Middle East & Africa

The Middle East and Africa account for approximately 7% of global market demand. Key markets include the UAE, Saudi Arabia, South Africa, Egypt, and Morocco, where consumer demand for packaged beverages continues to rise steadily. The region remains highly dependent on imports for premium orange juice products, particularly within Gulf Cooperation Council (GCC) countries.Regional growth is primarily driven by rising disposable incomes, expanding urban populations, increasing health awareness, and ongoing investments in modern retail infrastructure. The rapid expansion of supermarkets, hypermarkets, and convenience retail formats is improving product accessibility across major metropolitan areas. Demand for premium imported juices, functional beverages, and health-oriented products continues to strengthen among affluent consumers. Furthermore, growing tourism activity, expanding hospitality sectors, and increasing adoption of Western dietary and beverage consumption patterns are supporting long-term growth opportunities throughout the Middle East and Africa orange juice market.

Key Players in the Orange Juice Market

- PepsiCo (Tropicana)

- The Coca-Cola Company (Minute Maid)

- Cutrale Group

- Citrosuco

- Louis Dreyfus Company

- Lassonde Industries

- Eckes-Granini Group

- Refresco

- Döhler Group

- Suntory Holdings

- Innocent Drinks

- Del Monte Foods

- Florida's Natural Growers

- Ocean Spray Cranberries

- Kirin Holdings