Mocktails Market Size

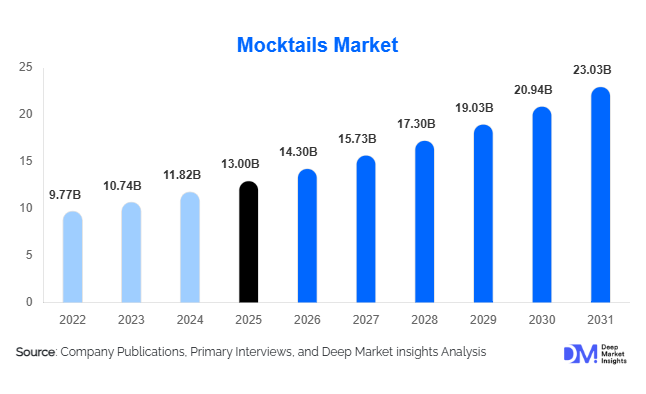

According to Deep Market Insights, the global mocktails market size was valued at USD 13.0 billion in 2025 and is projected to grow from USD 14.30 billion in 2026 to reach USD 23.03 billion by 2031, expanding at a CAGR of 10.0% during the forecast period (2026–2031). The mocktails market growth is primarily driven by increasing consumer preference for alcohol-free beverages, the rapid expansion of the sober-curious movement, rising health and wellness awareness, and growing demand for premium beverage experiences across hospitality, retail, and foodservice channels. The market has evolved beyond traditional fruit-based drinks into a sophisticated category encompassing ready-to-drink (RTD) mocktails, alcohol-free spirits, botanical beverages, and functional formulations enriched with adaptogens, probiotics, vitamins, and natural extracts.

Key Market Insights

- Ready-to-drink mocktails account for the largest market share, supported by convenience, retail availability, and increasing consumer preference for premium packaged beverages.

- Functional mocktails are among the fastest-growing segments, driven by rising demand for wellness beverages containing adaptogens, probiotics, botanicals, and nutritional ingredients.

- North America dominates the global market, led by strong adoption of alcohol moderation trends and premium beverage consumption in the United States and Canada.

- Asia-Pacific represents the fastest-growing regional market, supported by urbanization, increasing disposable incomes, and expanding health-conscious consumer populations in China, India, and Southeast Asia.

- Premiumization continues to reshape the industry, with consumers increasingly seeking sophisticated alcohol-free alternatives that replicate cocktail experiences.

- Hospitality, restaurants, bars, and hotels are rapidly expanding mocktail menus, creating new revenue streams while catering to broader consumer demographics.

Mocktails Market Latest Trends

Functional and Wellness-Oriented Mocktails Gaining Momentum

The mocktails industry is increasingly converging with the global functional beverage sector. Consumers are no longer seeking alcohol-free alternatives solely for social occasions but are actively looking for beverages that deliver tangible health benefits. Manufacturers are responding by introducing formulations enriched with adaptogens, nootropics, probiotics, vitamins, electrolytes, and botanical extracts. Functional mocktails are being positioned as products that support immunity, stress management, hydration, gut health, and cognitive wellness. Premium beverage brands are investing heavily in ingredient innovation to differentiate their offerings while capitalizing on growing consumer interest in preventive healthcare and holistic wellness. This trend is particularly prominent among Millennials and Generation Z consumers who prioritize ingredient transparency and clean-label formulations.

Premium Alcohol-Free Spirits and Craft Mocktails Expanding Globally

Premiumization has become a defining characteristic of the global mocktails market. Beverage companies are increasingly launching alcohol-free spirits, botanical distillates, and craft mocktail formulations designed to replicate the complexity and sophistication of traditional cocktails. Restaurants, hotels, bars, and luxury hospitality operators are dedicating entire menu sections to premium mocktails, often featuring artisanal ingredients, seasonal flavors, and advanced preparation techniques. The trend is creating opportunities for brands to command higher price points while improving profit margins. Innovations in botanical extraction, fermentation technologies, and flavor engineering are enabling manufacturers to deliver increasingly authentic alcohol-free drinking experiences, accelerating category acceptance among mainstream consumers.

Mocktails Market Drivers

Growing Adoption of Alcohol Moderation and Sober-Curious Lifestyles

The global rise of alcohol moderation is one of the most significant drivers supporting mocktails market growth. Consumers across developed and emerging economies are reducing alcohol consumption due to growing awareness of its long-term health impacts. The sober-curious movement has gained substantial momentum among younger demographics who seek balanced lifestyles without completely abandoning social experiences. Mocktails offer an attractive alternative by providing sophisticated beverage options that align with wellness goals while maintaining social inclusivity. This shift is encouraging retailers, restaurants, and beverage manufacturers to significantly expand their alcohol-free portfolios.

Rising Consumer Focus on Health and Wellness

Health-conscious purchasing behavior continues to drive demand across the mocktails industry. Consumers increasingly prefer beverages containing natural ingredients, reduced sugar content, clean-label formulations, and functional benefits. As awareness of obesity, diabetes, cardiovascular health, and overall wellness grows globally, consumers are actively replacing traditional soft drinks and alcoholic beverages with healthier alternatives. Mocktails positioned around hydration, immunity, stress reduction, and nutritional support are experiencing particularly strong demand, creating significant opportunities for innovation and product diversification.

Mocktails Market Restraints

Premium Pricing Compared to Conventional Soft Drinks

Despite strong demand growth, premium mocktails remain significantly more expensive than traditional carbonated beverages and fruit drinks. The use of high-quality ingredients, botanical extracts, alcohol-free distillation processes, and premium packaging contributes to elevated production costs. This pricing disparity may limit adoption among price-sensitive consumers, particularly in emerging markets where affordability remains a key purchasing consideration.

Consumer Perception and Category Awareness Challenges

Although awareness is improving, some consumers continue to perceive mocktails as simple fruit juices rather than premium beverage alternatives. This perception challenge can slow adoption rates and reduce consumers’ willingness to pay premium prices. Industry participants must continue investing in branding, education, and product innovation to reinforce mocktails as sophisticated lifestyle beverages capable of delivering experiences comparable to traditional cocktails.

Mocktails Industry Key Opportunities

Expansion Across Emerging Markets

Emerging economies present substantial growth opportunities for mocktail manufacturers. Countries such as India, China, Indonesia, Vietnam, Saudi Arabia, and the United Arab Emirates are experiencing rising disposable incomes, urbanization, and increasing health awareness. These factors are creating favorable conditions for premium beverage adoption. The rapid expansion of modern retail infrastructure, e-commerce channels, and international foodservice chains is further supporting market penetration. As awareness of alcohol-free lifestyles increases, emerging markets are expected to contribute a significant share of incremental industry revenues over the forecast period.

Hospitality and Foodservice Premiumization

The hospitality sector offers considerable growth potential for mocktail brands. Hotels, restaurants, cafes, bars, cruise operators, airlines, and event management companies are increasingly introducing premium mocktail menus to cater to evolving consumer preferences. Mocktails often generate margins comparable to alcoholic beverages while appealing to a broader audience, including health-conscious consumers, designated drivers, pregnant women, and individuals who abstain from alcohol for religious or cultural reasons. This creates opportunities for manufacturers to establish long-term partnerships with hospitality operators and expand brand visibility in premium consumption environments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.00 Billion |

| Market Size in 2026 | USD 14.30 Billion |

| Market Size in 2031 | USD 23.03 Billion |

| CAGR | 10% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ready-to-drink (RTD) mocktails dominated the global mocktails market in 2025, accounting for approximately 38.5% of total revenue. The segment’s leadership is primarily driven by growing consumer preference for convenience-oriented beverage solutions, increasing on-the-go consumption patterns, expanding retail shelf presence, and the rising popularity of alcohol-free alternatives that require no preparation. RTD mocktails have gained widespread acceptance across supermarkets, convenience stores, specialty retailers, and e-commerce platforms due to their accessibility, portability, and consistent taste profiles. The rapid expansion of premium canned beverages and single-serve formats has further strengthened demand, particularly among urban consumers seeking convenient yet sophisticated drinking experiences.Premium crafted mocktails continue to gain significant traction within restaurants, bars, hotels, and hospitality establishments as consumers increasingly seek elevated beverage experiences that mirror the complexity and presentation of traditional cocktails. The segment benefits from growing premiumization trends, rising consumer willingness to pay for artisanal ingredients, and increasing demand for experiential dining and social occasions. Functional mocktails are emerging as one of the fastest-growing product categories, supported by rising health consciousness, increasing interest in immunity-enhancing and wellness-oriented beverages, and growing incorporation of vitamins, botanicals, adaptogens, probiotics, and natural ingredients. Alcohol-free spirit-based mocktails are also witnessing strong adoption as consumers pursue authentic cocktail experiences without alcohol consumption. Frozen mocktails and concentrated mixes continue to maintain relevance in foodservice, catering, entertainment venues, and event management applications where customized beverage preparation and large-volume serving requirements remain important.

Flavor Profile Insights

Fruity mocktails accounted for approximately 34.2% of global demand in 2025, making them the largest flavor category within the market. The segment’s dominance is driven by broad consumer acceptance across all age groups, natural flavor appeal, versatility across product formats, and strong alignment with consumer preferences for refreshing and approachable beverage experiences. Fruit-based flavors also benefit from their compatibility with wellness-focused positioning, natural ingredient trends, and seasonal product innovations. Manufacturers continue introducing diverse fruit combinations and exotic fruit variants to enhance consumer engagement and differentiate product portfolios.Citrus-based mocktails maintain a strong market presence due to their refreshing taste profiles, perceived health benefits, and association with hydration and vitality. Botanical and herbal flavor categories are experiencing accelerated growth as consumers increasingly seek sophisticated and premium beverage experiences inspired by mixology trends. Floral, tropical, tea-based, coffee-infused, and fusion flavor profiles are gaining momentum through continuous product innovation and premium beverage development. Demand for unique flavor combinations featuring herbs, spices, exotic fruits, and globally inspired ingredients is particularly strong among younger consumers, who actively seek novel and differentiated consumption experiences. As beverage manufacturers continue to focus on flavor innovation, premium flavor profiles are expected to play an increasingly important role in market expansion.

Packaging Format Insights

Aluminum cans represented the largest packaging format in 2025, accounting for approximately 32% of global market revenues. The segment’s leadership is supported by increasing consumer preference for lightweight and portable packaging, growing environmental sustainability initiatives, superior recyclability, and the continued expansion of the RTD mocktail category. Beverage manufacturers increasingly favor aluminum cans due to lower transportation costs, enhanced shelf efficiency, and strong compatibility with modern retail and convenience channels. The format has also gained popularity among younger consumers who associate canned beverages with convenience and contemporary lifestyle preferences.Glass bottles continue to occupy a significant position within premium and super-premium mocktail categories due to their premium appearance, product preservation capabilities, and strong consumer perception of quality. PET bottles remain widely utilized in mass-market applications where affordability, durability, and portability are important purchasing considerations. Cartons and flexible pouches are gradually gaining market share as sustainability concerns encourage the adoption of lightweight packaging alternatives with lower environmental footprints. Kegs and bulk packaging formats remain essential within hospitality, catering, event management, and foodservice sectors where large-volume beverage dispensing and operational efficiency are key requirements.

Distribution Channel Insights

Supermarkets and hypermarkets accounted for approximately 29% of global market revenues in 2025, making them the leading distribution channel. The segment’s dominance is driven by extensive product availability, strong consumer footfall, attractive promotional activities, competitive pricing strategies, and the ability to offer a wide assortment of domestic and international brands under a single retail environment. The continued expansion of organized retail infrastructure and increasing consumer preference for one-stop shopping experiences have further strengthened the position of supermarkets and hypermarkets within the global mocktails market.E-commerce is emerging as one of the fastest-growing distribution channels, supported by increasing digital adoption, expanding direct-to-consumer sales models, growing availability of subscription-based beverage services, and consumer demand for convenient home delivery options. Specialty beverage retailers and health-focused stores continue to play a vital role in promoting premium, organic, and functional mocktail products while facilitating consumer education regarding alcohol-free alternatives. Within the on-trade segment, restaurants, bars, hotels, cafes, and entertainment venues are significantly expanding their mocktail offerings to address rising demand for premium alcohol-free beverages and inclusive drinking experiences that cater to diverse consumer preferences.

Consumer Demographic Insights

Millennials represented approximately 36% of global mocktail consumption in 2025, making them the largest consumer demographic. Growth within this segment is primarily driven by increasing health consciousness, growing preference for moderation and mindful drinking, strong interest in premium experiences, and heightened awareness regarding sustainability and ingredient transparency. Millennials actively seek products that align with balanced lifestyle choices while still delivering sophisticated flavor experiences and social engagement opportunities, positioning them as a key driver of category expansion.Generation Z represents the fastest-growing consumer group within the mocktails market due to increasing alcohol avoidance, strong preference for wellness-oriented products, and growing interest in functional beverages that offer additional health benefits. Digital influence, social media trends, and greater acceptance of sober-curious lifestyles continue to accelerate adoption among younger consumers. Generation X remains an important contributor to market revenues, particularly within premium beverage categories and hospitality-driven consumption occasions. Baby Boomers also support market growth through increasing interest in healthier lifestyle choices, reduced alcohol consumption, and preventive wellness practices that encourage the adoption of alcohol-free beverage alternatives.

End-Use Insights

The foodservice industry accounted for approximately 31% of global market demand in 2025, making it the largest end-use segment. The segment’s leadership is primarily driven by the rapid expansion of alcohol-free menu offerings, growing consumer demand for inclusive beverage options, increasing emphasis on premium dining experiences, and rising adoption of mocktails across restaurants, cafes, bars, quick-service chains, and entertainment venues. Foodservice operators are increasingly leveraging mocktails to attract health-conscious consumers, designated drivers, and individuals seeking sophisticated alcohol-free alternatives during social occasions.Hospitality establishments, including hotels, resorts, luxury venues, and event destinations, are expanding premium mocktail programs as part of broader beverage diversification strategies aimed at enhancing guest experiences. Household consumption remains a major contributor to market growth due to increasing retail availability of RTD products, greater accessibility through online platforms, and growing demand for at-home socialization and entertaining occasions. Additional growth opportunities are emerging across corporate catering, event management, aviation services, cruise operators, and travel retail channels, where inclusive beverage offerings are becoming increasingly important for serving diverse consumer demographics.

Explore more data points, trends and opportunities Download Free Sample Report

Mocktails Market Segmentations

By Product Type

- Ready-to-Drink (RTD) Mocktails

- Mocktail Mixes & Concentrates

- Premium Crafted Mocktails

- Functional Mocktails

- Alcohol-Free Spirit-Based Mocktails

- Frozen Mocktails

- Fountain/Dispensed Mocktails

By Flavor Profile

- Fruity

- Citrus

- Botanical & Herbal

- Tropical

- Spice-Based

- Tea & Coffee-Based

- Floral

- Exotic/Fusion Flavors

By Packaging Format

- Glass Bottles

- Aluminum Cans

- PET Bottles

- Cartons

- Pouches

- Kegs & Bulk Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Beverage Stores

- Health & Wellness Retailers

- E-commerce

- Restaurants

- Bars & Lounges

- Hotels

- Cafes

- Event Catering

By Consumer Demographic

- Gen Z Consumers

- Millennials

- Generation X

- Baby Boomers

Regional Insights

North America

North America accounted for approximately 34.8% of the global mocktails market in 2025, making it the largest regional market. The United States alone represented nearly 29% of global revenues, supported by strong adoption of sober-curious lifestyles, premium beverage spending, and a highly developed foodservice ecosystem. Canada continues to experience increasing demand for alcohol-free alternatives as consumers prioritize wellness-focused lifestyles and healthier consumption patterns. The region benefits from a mature retail landscape, advanced beverage innovation capabilities, and strong participation from leading beverage manufacturers.Regional growth is primarily driven by increasing alcohol moderation trends, rising demand for premium and craft beverages, growing consumer awareness regarding health and wellness, expanding availability of functional beverage formulations, and the strong influence of social movements promoting mindful drinking. The rapid expansion of e-commerce beverage sales, extensive distribution networks, increasing investments in product innovation, and growing presence of alcohol-free offerings across restaurants, bars, and hospitality establishments further support market expansion throughout North America.

Europe

Europe represented approximately 28.7% of global mocktails demand in 2025. The United Kingdom remains the region’s largest market, accounting for nearly 7.2% of global revenues, while Germany, France, Spain, Italy, and the Netherlands continue to contribute significantly to regional growth. Strong consumer awareness regarding health and wellness, coupled with widespread participation in alcohol reduction initiatives such as Dry January and mindful drinking campaigns, continues to strengthen market demand across the region.The region’s growth is driven by increasing adoption of alcohol-free lifestyles, rising demand for premium botanical beverages, strong consumer acceptance of alcohol-free spirits, expanding product availability within retail and hospitality channels, and supportive regulatory environments encouraging healthier consumption behaviors. Additionally, Europe’s established café culture, premium beverage heritage, and growing consumer preference for natural and clean-label ingredients continue to create favorable conditions for long-term market development.

Asia-Pacific

Asia-Pacific accounted for approximately 24.5% of global market revenues in 2025 and represents the fastest-growing regional market, with annual growth exceeding 12%. China and India are emerging as major demand centers due to rising disposable incomes, rapid urbanization, expanding middle-class populations, and increasing awareness of health and wellness. Japan, South Korea, Australia, Indonesia, Thailand, and Vietnam also contribute significantly to regional expansion through evolving consumer preferences and growing demand for premium beverage offerings.Growth across Asia-Pacific is supported by rapid modernization of retail infrastructure, increasing penetration of international foodservice chains, rising influence of Western beverage trends, expanding e-commerce adoption, and growing demand for premium non-alcoholic alternatives among younger consumers. The region is also benefiting from increasing health consciousness, rising participation in social drinking occasions without alcohol consumption, and continuous investments by domestic and international beverage manufacturers seeking to capitalize on the region’s large consumer base and favorable demographic profile.

Latin America

Latin America accounted for approximately 4.9% of global market revenues in 2025. Brazil and Mexico dominate regional demand, supported by increasing urbanization, expanding middle-class populations, and rising interest in premium beverage experiences. Argentina, Chile, and Colombia are also witnessing gradual growth as awareness of alcohol-free alternatives continues to increase across key urban markets.Regional growth is driven by improving consumer purchasing power, increasing exposure to global beverage trends, expansion of organized retail networks, growing health awareness among younger consumers, and rising investments in hospitality and foodservice sectors. The increasing popularity of premium dining experiences, tourism development, and growing availability of innovative alcohol-free beverages are expected to create substantial long-term growth opportunities throughout the region.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.1% of global market demand in 2025. The United Arab Emirates and Saudi Arabia represent the largest markets due to strong cultural acceptance of alcohol-free beverages, expanding hospitality sectors, and rapidly growing tourism industries. South Africa remains an important market within Africa, while several emerging economies are witnessing increasing demand for premium non-alcoholic beverage options.Regional growth is primarily supported by cultural and religious preferences favoring alcohol-free consumption, substantial investments in hospitality and tourism infrastructure, increasing international visitor arrivals, rising disposable incomes, and growing consumer interest in wellness-oriented beverages. The expansion of luxury hotels, restaurants, entertainment destinations, and premium retail channels across the Gulf Cooperation Council (GCC) countries, combined with increasing product innovation and wider distribution availability, continues to strengthen market growth prospects throughout the Middle East and Africa.

Key Players in the Mocktails Market

- Diageo (Seedlip)

- Lyre's Spirit Co.

- Fever-Tree Drinks

- The Coca-Cola Company

- PepsiCo

- Keurig Dr Pepper

- Ritual Zero Proof

- Monday Distillery

- Three Spirit Drinks

- Ceder's

- Mocktail Club

- Mingle Mocktails

- DRY Botanical Bubbly

- Free AF

- Abstinence Spirits