Methoxyacetic Acid Market Size

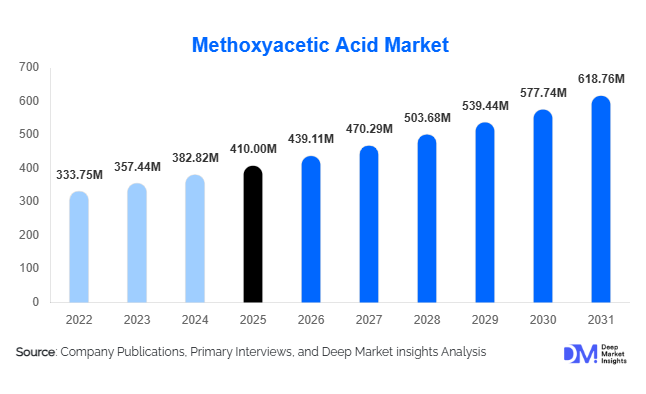

According to Deep Market Insights, the global methoxyacetic acid market size was valued at approximately USD 410 million in 2025 and is projected to grow from USD 439.11 million in 2026 to reach USD 618.76 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). Market growth is primarily driven by rising consumption of pharmaceutical intermediates, increasing agrochemical production, and expanding applications in specialty chemical synthesis. Methoxyacetic acid plays a critical role as a high-value organic intermediate used in pharmaceutical manufacturing, crop protection chemicals, performance materials, and custom chemical formulations. As pharmaceutical supply chains continue to diversify globally and governments promote domestic chemical manufacturing capabilities, demand for high-purity methoxyacetic acid is expected to remain robust.

The market is witnessing increasing investment in specialty chemical production facilities, particularly across Asia-Pacific, where China and India have emerged as major manufacturing hubs. High-purity grades continue to command premium pricing due to stringent quality requirements from pharmaceutical and advanced chemical manufacturers. Meanwhile, sustainability initiatives, process optimization technologies, and environmental compliance investments are reshaping production practices. The growing importance of contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs) is further strengthening long-term demand for specialty intermediates such as methoxyacetic acid. As end-use industries increasingly prioritize supply security and regulatory compliance, the global methoxyacetic acid market is expected to experience steady expansion throughout the forecast period.

Key Market Insights

- Pharmaceutical intermediates account for nearly 38% of global methoxyacetic acid consumption, making healthcare applications the primary demand driver.

- Asia-Pacific dominates the market with approximately 42% share, supported by large-scale chemical manufacturing capacity in China and India.

- High-purity grades represent around 65% of market revenue, reflecting increasing demand from regulated pharmaceutical and specialty chemical applications.

- India is emerging as the fastest-growing national market, supported by API manufacturing expansion and specialty chemical investments.

- Direct manufacturer sales account for nearly 58% of global distribution, driven by long-term procurement agreements from pharmaceutical and agrochemical producers.

- Specialty chemical manufacturers are increasingly adopting customized synthesis routes, creating new opportunities for premium methoxyacetic acid suppliers.

Methoxyacetic Acid Market Latest Trends

Rising Adoption of High-Purity Specialty Chemical Intermediates

Demand for high-purity methoxyacetic acid continues to increase as pharmaceutical manufacturers, CDMOs, and specialty chemical producers seek consistent raw materials that comply with increasingly stringent quality standards. Pharmaceutical companies are prioritizing intermediates that support regulatory compliance and improve process efficiency. Consequently, producers are investing in purification technologies, advanced quality-control systems, and dedicated production lines for pharmaceutical-grade methoxyacetic acid. High-purity products not only command premium pricing but also generate stronger long-term customer relationships due to qualification requirements and regulatory approvals.

Shift Toward Asia-Centric Manufacturing Ecosystems

Asia-Pacific has become the center of global methoxyacetic acid production and consumption growth. China continues to dominate manufacturing output, while India is rapidly expanding its pharmaceutical intermediate and specialty chemical sectors. Global customers are increasingly adopting China+1 sourcing strategies to diversify supply chains and reduce procurement risks. This trend is encouraging investments in new chemical plants, backward integration projects, and export-oriented manufacturing facilities throughout South and Southeast Asia. As a result, Asia-Pacific is expected to maintain its leadership position throughout the forecast period.

Methoxyacetic Acid Market Drivers

Expansion of Pharmaceutical Intermediate Manufacturing

Pharmaceutical manufacturing remains the strongest growth driver for the methoxyacetic acid market. The compound serves as an important intermediate in various synthesis processes used for active pharmaceutical ingredients and specialty drug compounds. Growing healthcare expenditures, rising generic drug production, and increasing investments in pharmaceutical self-sufficiency are driving intermediate demand globally. Countries such as India, China, and the United States continue expanding pharmaceutical production capacities, directly supporting methoxyacetic acid consumption.

Growing Agrochemical Production Worldwide

Increasing food demand and pressure to improve agricultural productivity are driving agrochemical consumption worldwide. Methoxyacetic acid is utilized in the synthesis of various crop protection compounds and specialty agricultural chemicals. Rapid growth in pesticide, herbicide, and fungicide production across Asia-Pacific and Latin America is generating significant opportunities for methoxyacetic acid manufacturers. Emerging economies are investing heavily in agricultural modernization, which is expected to further strengthen demand over the coming years.

Growth of Specialty Chemicals and Custom Synthesis

The specialty chemicals industry is increasingly shifting toward customized formulations, performance materials, and advanced synthesis applications. Methoxyacetic acid is widely used in specialty chemical production due to its favorable reaction properties and versatility. Rising investments in electronic chemicals, advanced coatings, performance polymers, and custom manufacturing services are creating new demand channels beyond traditional pharmaceutical and agrochemical applications.

Methoxyacetic Acid Market Restraints

Stringent Environmental and Occupational Safety Regulations

Methoxyacetic acid requires careful handling due to its hazardous nature and associated occupational exposure concerns. Regulatory agencies in North America, Europe, and Asia continue tightening environmental compliance standards and worker safety requirements. Manufacturers must invest in emission-control technologies, waste treatment systems, and workplace monitoring infrastructure, increasing operating costs and creating barriers for smaller producers.

Feedstock and Raw Material Price Volatility

Production economics remain sensitive to fluctuations in methanol derivatives, petrochemical feedstocks, and energy costs. Volatile raw material pricing can significantly impact profit margins and create uncertainty for long-term supply contracts. Manufacturers increasingly seek process optimization and procurement diversification strategies to mitigate exposure to commodity price fluctuations.

Methoxyacetic Acid Industry Key Opportunities

Pharmaceutical Capacity Expansion in Emerging Markets

Governments worldwide are encouraging domestic pharmaceutical manufacturing to improve healthcare security and reduce import dependence. India’s Production Linked Incentive (PLI) program, expanding pharmaceutical infrastructure in Southeast Asia, and increased API investments across the Middle East are creating substantial opportunities for methoxyacetic acid suppliers. Companies capable of providing pharmaceutical-grade material can secure high-margin, long-term supply agreements with API manufacturers and CDMOs.

Growth in Advanced Agrochemical Technologies

The transition toward more efficient and environmentally responsible crop protection solutions is creating new demand for specialty intermediates. Methoxyacetic acid producers can benefit from increasing investments in next-generation agrochemicals, biological formulations, and advanced pesticide development programs. Emerging agricultural markets in Brazil, Indonesia, Vietnam, and Africa represent particularly attractive growth opportunities.

Expansion of Contract Manufacturing and Custom Synthesis Services

The growing role of contract manufacturing organizations and custom synthesis providers presents a significant opportunity for specialty chemical suppliers. These organizations increasingly require consistent, high-quality intermediates for complex synthesis processes. Manufacturers that offer customized specifications, technical support, and flexible production capabilities can establish strong competitive positions within this rapidly expanding segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 410.00 Million |

| Market Size in 2026 | USD 439.11 Million |

| Market Size in 2031 | USD 618.76 Million |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Purity Grade Insights

High-purity methoxyacetic acid (≥99%) accounts for approximately 65% of global market revenue in 2025, making it the dominant purity grade segment. The segment’s leadership is primarily attributed to the increasing quality requirements of pharmaceutical manufacturers, where stringent regulatory standards, process consistency, and impurity control are critical for active pharmaceutical ingredient (API) production and specialty synthesis applications. The growing emphasis on Good Manufacturing Practices (GMP), product traceability, and regulatory compliance across global pharmaceutical supply chains continues to accelerate demand for high-purity grades. Additionally, specialty chemical manufacturers increasingly favor premium-grade methoxyacetic acid to improve reaction efficiency, minimize contamination risks, and ensure consistent product performance. Technical-grade products continue to maintain significant demand in agrochemical intermediates and industrial synthesis applications where ultra-high purity is not mandatory, while industrial-grade variants remain relevant in cost-sensitive manufacturing operations. Nevertheless, the overall market is witnessing a gradual transition toward higher-purity products as end users prioritize quality assurance, production efficiency, and regulatory compliance across increasingly sophisticated manufacturing processes.

Application Insights

Pharmaceutical intermediates represent the largest application segment, accounting for approximately 38% of global methoxyacetic acid demand in 2025. The segment’s dominance is driven by the rapid expansion of global API manufacturing, increasing generic drug production, rising pharmaceutical outsourcing activities, and growing investments in specialty therapeutics. Methoxyacetic acid serves as an important intermediate in the synthesis of various pharmaceutical compounds, making it a critical raw material for drug manufacturers seeking reliable and high-purity chemical inputs. The expansion of contract development and manufacturing organizations (CDMOs), particularly across Asia-Pacific, further strengthens demand within this segment. Agrochemical intermediates constitute the second-largest application category, supported by rising global food security concerns, increasing crop protection requirements, and the growing adoption of advanced agricultural chemicals. Specialty chemical synthesis applications are also experiencing robust growth as manufacturers focus on developing high-performance materials, customized formulations, electronic chemicals, and advanced industrial compounds. Furthermore, emerging applications in specialty coatings, research reagents, and fine chemical synthesis are creating new opportunities for market expansion, particularly in technologically advanced economies.

End-Use Industry Insights

The specialty chemicals industry accounts for nearly 42% of total global methoxyacetic acid consumption, making it the leading end-use industry segment. The segment’s leadership is supported by the increasing use of methoxyacetic acid in custom synthesis pathways, specialty formulations, performance chemicals, and advanced material production. Growing demand for high-value chemicals across electronics, coatings, polymers, and industrial processing applications continues to drive consumption within the specialty chemicals sector. Pharmaceutical manufacturers remain the most influential end-use sector from a value perspective due to their preference for premium-grade products and strict quality specifications. The agrochemical industry continues to expand its utilization of methoxyacetic acid as global agricultural productivity requirements intensify and crop protection strategies become increasingly sophisticated. In addition, research institutions, contract research organizations, and custom synthesis laboratories contribute to market growth through ongoing innovation activities, particularly in developed markets characterized by strong research infrastructure and significant investments in chemical and pharmaceutical development.

Distribution Channel Insights

Direct manufacturer sales account for approximately 58% of global market revenue, making them the dominant distribution channel. The leading position of this channel is driven by the need for quality assurance, regulatory compliance, supply reliability, and long-term procurement agreements among large pharmaceutical, agrochemical, and specialty chemical manufacturers. Direct purchasing enables end users to maintain greater control over product specifications, traceability requirements, and supply chain security, which are increasingly important in highly regulated industries. Long-term strategic supply contracts have gained prominence as manufacturers seek protection from raw material price volatility and supply disruptions. Chemical distributors and traders account for nearly 30% of market activity and play an important role in serving regional markets, small and medium-sized enterprises, and customers requiring flexible purchasing volumes. Meanwhile, digital procurement platforms are gradually emerging as an alternative sourcing channel, supported by growing digitalization across the chemical industry, although their contribution to overall market revenue remains relatively limited compared to traditional procurement structures.

Production Route Insights

Methanol carbonylation-based production represents approximately 55% of global methoxyacetic acid output, making it the leading production route. The dominance of this method is primarily attributed to its superior scalability, cost efficiency, established industrial infrastructure, and suitability for large-volume commercial production. The route enables manufacturers to achieve competitive production economics while maintaining consistent product quality, making it the preferred choice for major producers worldwide. Alternative production pathways, including ester hydrolysis and glycolic acid derivative routes, continue to serve specialized applications and niche production requirements where specific process characteristics or feedstock availability provide advantages. Across the industry, manufacturers are increasingly investing in process optimization technologies, continuous manufacturing systems, advanced catalysts, and sustainable production practices to improve operational efficiency, reduce environmental impact, and comply with evolving regulatory standards. These technological advancements are expected to further enhance production yields and strengthen long-term competitiveness within the market.

Explore more data points, trends and opportunities Download Free Sample Report

Methoxyacetic Acid Market Segmentations

By Purity Grade

- High Purity Grade

- Technical Grade

- Industrial Grade

By Application

- Pharmaceutical Intermediates

- Agrochemical Intermediates

- Dye & Pigment Intermediates

- Specialty Chemical Synthesis

- Polymer & Resin Additives

- Solvent Formulations

- Laboratory & Research Reagents

- Other Industrial Applications

By End-Use Industry

- Pharmaceutical Industry

- Agrochemical Industry

- Specialty Chemicals Industry

- Paints, Coatings & Pigments Industry

- Polymer & Plastics Industry

- Research & Academic Institutions

- Other Industrial Manufacturing

By Distribution Channel

- Direct Manufacturer Sales

- Chemical Distributors & Traders

- Contract Supply Agreements

- E-commerce & Digital Chemical Platforms

By Production Route

- Methanol Carbonylation-Based Route

- Glycolic Acid Derivative Route

- Ester Hydrolysis Route

- Other Proprietary Synthesis Routes

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 42% of the global methoxyacetic acid market in 2025, making it the largest regional market. The region’s dominance is supported by its extensive pharmaceutical manufacturing base, rapidly expanding agrochemical industry, growing specialty chemical production capacity, and competitive manufacturing economics. China contributes nearly 24% of worldwide demand and remains the leading producer and consumer due to its integrated chemical supply chains, large-scale pharmaceutical production capabilities, and strong export-oriented chemical sector. India accounts for roughly 10% of global demand and represents the fastest-growing national market, driven by accelerating API manufacturing investments, expanding specialty chemical production, increasing contract manufacturing activity, and supportive government initiatives promoting domestic chemical and pharmaceutical industries. Japan and South Korea continue to generate stable demand through advanced chemical manufacturing, high-value specialty applications, and innovation-driven industrial sectors. Additional growth drivers across the region include rising healthcare expenditures, expanding generic drug production, increasing agricultural productivity requirements, foreign direct investment in chemical manufacturing, and ongoing capacity expansions by regional producers. The continued shift of global pharmaceutical and specialty chemical production toward Asia-Pacific is expected to reinforce the region’s market leadership throughout the forecast period.

North America

North America represents approximately 28% of global methoxyacetic acid market revenue. The United States dominates regional consumption, contributing nearly 24% of worldwide demand, supported by its advanced pharmaceutical industry, robust specialty chemical sector, and strong research and development ecosystem. Demand growth is primarily driven by increasing investments in drug development, expanding biologics and specialty therapeutics manufacturing, and the growing need for high-purity chemical intermediates. The region also benefits from stringent quality and regulatory standards that favor premium-grade methoxyacetic acid products. Ongoing reshoring initiatives aimed at strengthening domestic pharmaceutical and chemical supply chains are creating additional demand opportunities. Canada and Mexico contribute supplementary growth through pharmaceutical manufacturing, industrial chemical production, and increasing participation in North American supply chains. Rising investments in specialty materials, advanced manufacturing technologies, and chemical innovation are expected to support long-term market expansion across the region.

Europe

Europe accounts for nearly 20% of global methoxyacetic acid demand. The region benefits from a mature pharmaceutical industry, highly developed specialty chemical manufacturing capabilities, and strong regulatory frameworks emphasizing product quality and sustainability. Germany leads regional consumption due to its extensive chemical manufacturing infrastructure and position as one of the world's largest chemical producers. France, the United Kingdom, Italy, and the Netherlands also maintain substantial demand driven by pharmaceutical intermediates, fine chemical synthesis, and specialty manufacturing applications. Key growth drivers include increasing investments in high-value specialty chemicals, rising demand for advanced pharmaceutical ingredients, and continued innovation in sustainable chemical processes. Furthermore, stringent environmental regulations are encouraging manufacturers to adopt cleaner production technologies, improve process efficiency, and invest in environmentally responsible manufacturing practices. The region’s focus on innovation, sustainability, and premium chemical products is expected to support steady market growth over the coming years.

Latin America

Latin America contributes approximately 6% of global methoxyacetic acid market revenue. Brazil dominates regional demand owing to its large agricultural sector, significant agrochemical consumption, and expanding specialty chemical industry. The country’s position as a major agricultural exporter continues to support demand for crop protection chemicals and related intermediates. Argentina and Chile represent important emerging markets, benefiting from increasing agricultural modernization, rising agrochemical utilization rates, and growing investments in industrial chemical production. Additional regional growth drivers include expanding pharmaceutical manufacturing activities, improving industrial infrastructure, increasing foreign investment in chemical production, and government initiatives aimed at enhancing agricultural productivity. As agricultural modernization programs continue to advance and chemical manufacturing capabilities expand, regional demand for methoxyacetic acid is expected to strengthen steadily throughout the forecast period.

Middle East & Africa

The Middle East & Africa accounts for approximately 4% of global methoxyacetic acid demand. Although currently the smallest regional market, the region is emerging as an important growth area due to increasing investments in downstream chemical diversification and industrial development. Saudi Arabia and the United Arab Emirates are actively expanding their petrochemical and specialty chemical manufacturing capabilities as part of broader economic diversification strategies, creating new opportunities for methoxyacetic acid consumption. South Africa remains the largest market within Sub-Saharan Africa, supported by pharmaceutical manufacturing activities, industrial chemical applications, and growing healthcare sector requirements. Additional growth drivers include rising industrialization, expanding pharmaceutical production, increasing agricultural chemical demand, infrastructure development, and government initiatives aimed at reducing dependence on imported chemical products. As regional economies continue investing in value-added chemical manufacturing and industrial diversification, demand for methoxyacetic acid is expected to witness steady growth over the long term.

Key Players in the Methoxyacetic Acid Market

- BASF SE

- Dow Inc.

- Eastman Chemical Company

- INEOS Group

- Mitsubishi Chemical Group

- SABIC

- Celanese Corporation

- Evonik Industries

- LANXESS

- Arkema

- Clariant

- Solvay

- LG Chem

- Sumitomo Chemical

- Chevron Phillips Chemical