Mengshan Tea Market Size

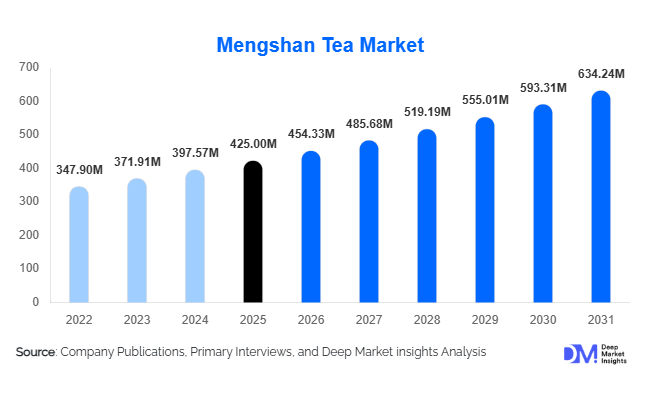

According to Deep Market Insights, the global Mengshan tea market size was valued at approximately USD 425 million in 2025 and is projected to grow from USD 454.33 million in 2026 to reach USD 634.24 million by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The market is benefiting from growing consumer preference for premium specialty teas, increasing awareness regarding the health benefits of traditional Chinese teas, rising demand for geographically authentic products, and expansion of cross-border e-commerce channels. As consumers increasingly seek natural wellness beverages and traceable agricultural products, Mengshan tea is emerging as a premium segment within the global specialty tea industry. The combination of heritage branding, limited cultivation geography, and strong demand from health-conscious consumers continues to support market expansion across both mature and emerging tea-consuming regions.

Key Market Insights

- Premium loose-leaf Mengshan tea accounts for the largest share of global demand, supported by growing consumer preference for authentic and minimally processed tea products.

- Organic-certified Mengshan tea is among the fastest-growing categories, driven by rising health consciousness and clean-label purchasing behavior.

- Asia-Pacific dominates the global market, accounting for approximately 67% of global consumption due to strong domestic demand in China and growing premium tea adoption across East Asia.

- North America represents the fastest-growing regional market, supported by specialty tea culture, wellness beverage trends, and expanding online distribution.

- E-commerce has become a critical sales channel, enabling producers to directly access premium consumers worldwide while improving product traceability and margins.

- Functional beverage applications are expanding, with tea extracts increasingly utilized in wellness drinks, nutraceuticals, and premium RTD beverage formulations.

Mengshan Tea Market Latest Trends

Premiumization of Traditional Chinese Tea Consumption

The global tea industry is experiencing a premiumization trend, benefiting heritage tea categories such as Mengshan tea. Consumers increasingly associate origin-specific teas with superior quality, authenticity, and health benefits. High-income consumers are shifting away from commodity tea products toward premium loose-leaf varieties featuring geographical indication certifications and transparent sourcing. Premium gift packaging, collector editions, and limited-harvest offerings are gaining popularity across China, Japan, South Korea, Europe, and North America. Producers are also investing heavily in branding strategies emphasizing cultural heritage and centuries-old cultivation practices, helping elevate Mengshan tea's positioning within the luxury beverage segment.

Growth of Functional and Wellness-Oriented Tea Products

The growing global wellness movement has significantly increased demand for teas perceived as natural functional beverages. Mengshan tea is increasingly marketed based on its antioxidant content, polyphenol profile, and potential wellness benefits. Beverage manufacturers are incorporating Mengshan tea extracts into functional drinks targeting immunity support, stress management, digestive health, and healthy aging. Premium RTD tea products featuring Mengshan tea are expanding across Asia-Pacific and North America. This trend is further supported by consumer preferences for natural alternatives to sugary beverages and synthetic supplements, positioning Mengshan tea favorably within the broader health and wellness industry.

Mengshan Tea Market Drivers

Growing Global Demand for Premium Specialty Teas

The premium tea segment continues to outperform the broader tea market. Consumers are increasingly willing to pay higher prices for single-origin products that offer unique flavor profiles, cultural heritage, and verified provenance. Mengshan tea benefits from this trend due to its historical significance and limited production geography. Specialty tea retailers, luxury hospitality operators, and premium gifting segments continue to expand procurement of high-grade Mengshan tea, supporting both volume and value growth.

Expansion of Cross-Border E-Commerce Platforms

Digital commerce platforms have dramatically improved accessibility to premium Chinese tea products. Previously limited to domestic Chinese consumers and specialty importers, Mengshan tea is now reaching customers globally through direct-to-consumer sales models. Producers can bypass traditional distribution layers, improving profitability while offering consumers greater product transparency. Online marketplaces have also enabled small and medium-sized tea producers to compete globally through targeted branding and consumer education initiatives.

Rising Consumer Focus on Natural Wellness Products

Global consumers increasingly seek natural products that support preventive health and overall wellness. Tea consumption has benefited from growing awareness of antioxidants, polyphenols, and plant-based nutrition. Mengshan tea's positioning as a traditional premium green tea aligns closely with these consumer preferences. Demand from wellness-focused consumers, nutrition-conscious millennials, and aging populations continues to strengthen the market's long-term growth prospects.

Mengshan Tea Market Restraints

Limited Production Geography and Supply Constraints

Mengshan tea is cultivated within a relatively restricted geographic region, limiting production scalability. Unlike commodity teas that can rapidly expand acreage, Mengshan tea's authenticity and quality depend heavily on specific terroir conditions. This restricts supply availability and contributes to price volatility during unfavorable harvest seasons.

Counterfeit Products and Authentication Challenges

The premium pricing associated with Mengshan tea has encouraged the proliferation of counterfeit and falsely labeled products. In international markets, consumers often face challenges verifying product authenticity. Insufficient traceability standards and inconsistent labeling practices can undermine consumer confidence and create barriers to market expansion. Industry stakeholders continue to invest in certification systems, blockchain traceability solutions, and geographical indication protections to address these concerns.

Mengshan Tea Industry Key Opportunities

Expansion into Functional Beverage Manufacturing

The functional beverage sector presents substantial growth opportunities for Mengshan tea producers. Global functional beverage sales continue to grow at rates exceeding traditional beverage categories, creating opportunities for tea-based formulations. Beverage companies are increasingly incorporating premium tea extracts into energy drinks, immunity beverages, and wellness products. The strong antioxidant profile of Mengshan tea supports premium positioning within this rapidly growing industry.

Growth of Organic and Sustainable Tea Production

Consumer demand for organic food and beverage products continues to accelerate globally. Organic-certified Mengshan tea commands premium pricing and attracts environmentally conscious consumers. Producers investing in organic cultivation, sustainable farming practices, and carbon-conscious production methods can access higher-margin customer segments while strengthening export competitiveness.

Rising Premium Gift Market Demand

Premium tea gifting has become a major demand driver, particularly across Asia-Pacific. Corporate gifting, holiday celebrations, luxury hospitality, and cultural gifting traditions increasingly feature premium tea products. High-end packaging innovations, customized gift collections, and limited-edition harvest releases provide opportunities for producers to significantly increase average selling prices while expanding brand recognition.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 425.00 Million |

| Market Size in 2026 | USD 454.33 Million |

| Market Size in 2031 | USD 634.24 Million |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Loose-leaf Mengshan tea continues to dominate the global market, accounting for approximately 52% of total revenue in 2025. This leadership is primarily driven by strong consumer perception of superior quality, authenticity, and enhanced flavor retention compared to processed alternatives. The segment benefits from a growing global preference for artisanal and origin-specific teas, where provenance and traditional processing methods significantly influence purchasing decisions. Rising premiumization across the tea industry further strengthens loose-leaf demand, as consumers increasingly associate whole-leaf formats with higher nutritional integrity and a more refined sensory experience. Additionally, expanding specialty tea retail networks and online tea education content have reinforced consumer willingness to trade up from mass-market formats.Tea bags represent nearly 24% of the market, with growth driven by urbanization, fast-paced lifestyles, and increasing adoption in Western markets where convenience remains a key purchase determinant. Improvements in pyramid bag technology and better-quality leaf incorporation have also elevated consumer acceptance of bagged tea, narrowing the perceived quality gap with loose-leaf products. Ready-to-drink Mengshan tea is emerging as the fastest-growing format, expanding at an estimated CAGR above 9%, supported by strong demand for functional beverages, on-the-go consumption, and premiumization of bottled tea products. This segment is further propelled by beverage manufacturers introducing health-oriented formulations with reduced sugar content and added botanical ingredients. Instant tea continues to serve industrial and institutional demand where scalability, shelf stability, and cost efficiency are primary purchasing drivers, particularly in foodservice and bulk preparation environments.

Grade Insights

Premium-grade Mengshan tea accounted for approximately 41% of global market revenue in 2025, establishing itself as the leading quality tier. Its dominance is driven by increasing consumer willingness to pay for consistent quality, certified sourcing, and refined flavor profiles that align with evolving lifestyle-oriented consumption patterns. The growth of premium tea culture in both developed and emerging markets has further accelerated demand, supported by rising disposable incomes and expanding specialty retail channels that actively promote higher-grade offerings through curated experiences and expert-led tastings.Imperial and tribute-grade teas, while representing nearly 18% of market value, derive their strength from extreme scarcity, heritage positioning, and strong cultural prestige, particularly in Asian markets where gifting traditions significantly influence demand. Commercial-grade tea remains essential for institutional buyers and export-oriented bulk supply chains, with its demand driven by cost efficiency, large-scale blending applications, and consistent availability. Mass-market grades continue to play a foundational role in expanding tea consumption in emerging economies, where affordability and accessibility remain the primary adoption drivers, enabling first-time consumers to enter the category before transitioning to higher-quality segments over time.

Distribution Channel Insights

E-commerce platforms accounted for approximately 29% of global sales in 2025, making them the leading distribution channel for Mengshan tea. Their dominance is driven by increasing digital penetration, improved cross-border logistics, and the ability of online platforms to offer extensive product variety alongside transparent sourcing information. Digital marketplaces have also enabled smaller producers and specialty brands to directly access global consumers, reducing traditional distribution barriers and enhancing price competitiveness in premium tea categories.Specialty tea stores represent approximately 24% of market revenue, supported by growing consumer preference for experiential retail environments where education, tasting, and product storytelling enhance perceived value. Direct-to-consumer channels are expanding rapidly as producers invest in brand-owned ecosystems, subscription models, and personalized marketing strategies that strengthen customer retention and lifetime value. Supermarkets and hypermarkets continue to play a critical role in mainstream penetration, particularly in Asia-Pacific, where high retail density and established consumer habits ensure strong baseline demand for both premium and everyday tea products.

End-Use Insights

Household consumers accounted for nearly 58% of total market demand in 2025, reinforcing residential consumption as the dominant end-use segment. Growth in this category is driven by rising health consciousness, increased home-based consumption rituals, and a broader shift toward natural and functional beverages. The expansion of wellness-oriented lifestyles has further strengthened household tea consumption, with consumers integrating premium tea into daily hydration and relaxation routines.Foodservice applications contribute approximately 22% of market revenue, supported by the expansion of premium cafes, tea houses, and luxury hospitality establishments that position tea as a high-value experiential beverage. Beverage manufacturers represent the fastest-growing end-use segment, expanding at an estimated CAGR above 8%, driven by increasing incorporation of tea extracts into functional beverages, ready-to-drink products, and nutraceutical formulations. This growth is strongly supported by innovation in beverage formulation, where tea is used as a base for energy, detox, and immunity-focused drinks targeting health-conscious consumers.

Application Insights

Traditional tea consumption remains the leading application, accounting for approximately 63% of global market value in 2025. This dominance is sustained by deeply embedded cultural consumption habits, particularly in Asia, where tea continues to serve as both a daily beverage and a symbol of hospitality. The segment is further strengthened by the global expansion of premium tea appreciation, where traditional brewing methods are increasingly adopted in Western markets seeking authentic cultural experiences.Wellness and functional beverage applications account for nearly 16% of demand and represent the fastest-growing application area, driven by rising consumer focus on immunity, stress reduction, and natural health solutions. Premium gifting contributes approximately 11% of revenue, with strong seasonal spikes in East Asian markets where tea is closely associated with respect, tradition, and social exchange. Ingredient applications are also expanding steadily as food and beverage manufacturers integrate tea extracts into dairy products, confectionery, and health-focused formulations, leveraging tea’s antioxidant properties and natural positioning to appeal to premium health-conscious consumers.

Explore more data points, trends and opportunities Download Free Sample Report

Mengshan Tea Market Segmentations

By Product Type

- Loose Leaf Mengshan Tea

- Tea Bag Mengshan Tea

- Ready-to-Drink (RTD) Mengshan Tea

- Instant Mengshan Tea Products

By Grade / Quality

- Imperial / Tribute Grade

- Premium Grade

- Commercial Grade

- Mass-Market Grade

By Certification Type

- Conventional

- Organic Certified

- Geographical Indication (GI) Certified

- Sustainable / Eco-Certified

By Distribution Channel

- E-commerce Platforms

- Specialty Tea Stores

- Supermarkets & Hypermarkets

- Direct-to-Consumer (DTC)

- Duty-Free & Travel Retail

By End User

- Household Consumers

- Foodservice Sector

- Beverage Manufacturing Industry

- Corporate & Institutional Buyers

Regional Insights

Asia-Pacific

Asia-Pacific dominated the global Mengshan tea market with approximately 67% market share in 2025, supported by deeply rooted cultural consumption patterns and highly developed tea production ecosystems. The region’s leadership is driven by strong domestic demand in China, where Mengshan tea benefits from heritage recognition, premium gifting traditions, and extensive specialty retail distribution networks. Rising disposable incomes and rapid urbanization continue to expand premium consumption beyond tier-one cities into emerging urban centers. Japan and South Korea contribute additional demand through strong appreciation for high-quality green teas, while Southeast Asia is emerging as a new growth frontier supported by expanding middle-class populations, increasing health awareness, and growing exposure to premium imported tea products through modern retail channels and e-commerce platforms.

North America

North America accounted for approximately 14% of global market revenue in 2025 and is projected to remain the fastest-growing region through 2031. Growth is primarily driven by increasing consumer shift toward functional beverages, wellness-oriented lifestyles, and natural alternatives to carbonated drinks. The United States leads regional demand due to strong specialty tea culture, rapid e-commerce adoption, and rising interest in premium and artisanal beverage categories. Canada is also experiencing steady expansion supported by multicultural consumption trends and growing availability of imported premium teas through online and specialty retail channels. The region’s growth is further reinforced by innovation in ready-to-drink formats and strong marketing emphasis on health benefits associated with tea consumption.

Europe

Europe represented approximately 11% of global consumption, with demand driven by mature yet evolving tea cultures across key markets such as Germany, the United Kingdom, France, and the Netherlands. Growth in the region is strongly influenced by increasing consumer preference for organic certification, sustainable sourcing, and traceability across supply chains. European consumers are increasingly prioritizing ethically sourced premium teas, which has encouraged importers and retailers to focus on transparency and quality differentiation. The expansion of specialty tea houses and premium retail concepts continues to support category premiumization, while wellness trends are gradually reshaping traditional coffee-dominant consumption patterns in favor of high-quality tea alternatives.

Middle East & Africa

The Middle East and Africa accounted for approximately 5% of global demand, with growth driven by rising luxury consumption and increasing exposure to international beverage trends. The United Arab Emirates serves as a strategic trading and redistribution hub for premium tea products, benefiting from strong tourism and hospitality sectors that emphasize high-end beverage experiences. Saudi Arabia continues to show rising demand for premium and imported teas, supported by growing disposable incomes and evolving lifestyle preferences. In Africa, South Africa leads regional consumption, driven by expanding middle-class populations, increasing urbanization, and gradual retail modernization that is improving access to specialty tea products.

Latin America

Latin America represented approximately 3% of global market revenue, with Brazil and Mexico serving as the primary demand centers. Growth in the region is driven by increasing awareness of specialty teas, gradual expansion of premium beverage retail channels, and rising interest in health-oriented drinks. Although the market remains relatively small compared to other regions, long-term growth potential is supported by improving distribution infrastructure, growing café culture, and increasing consumer experimentation with non-traditional tea varieties as disposable incomes continue to rise.

Key Players in the Mengshan Tea Market

- Sichuan Mengshan Tea Group

- Sichuan Tea Industry Group

- Zhuyeqing Tea Company

- China Tea Co., Ltd.

- Wuyutai Tea Company

- Tianfu Tea Group

- Weee!

- Tenfu Corporation

- Dayi Tea Group

- Huaxi Tea Industry

- Luzhou Tea Industry Group

- Mingxuan Tea Co.

- Sichuan Ya'an Tea Company

- Yibin Early Tea Group

- Chinatea Industrial Co.